The Cockroaches are Multiplying – Fat Tail Daily

And I probably shouldn’t say this, but when you see one cockroach, there are probably more… Everyone should be forewarned on this.’

— Jamie Dimon, Oct 2025

Six weeks ago, I asked whether private credit was the new subprime. The short answer: maybe.

The longer answer hinged on Blue Owl’s fund liquidation, collapsing share prices across the private credit complex, and uncomfortable parallels with the mid-2000s housing market.

Since then, the case has only strengthened. The trouble is, most people talking about it are dead boring.

As an example, the Bank of England Governor Andrew Bailey. Speaking as chair of the International Financial Stability Board, told European lawmakers this week:

‘Private credit has not yet, because of its relative newness, actually come under stress. We may be seeing that now.’

Case in point. Another carefully worded statement from a central banker whose job is not to cause panic.

Read between the lines. The system is being tested, and nobody is sure it will hold.

Right now, we’re watching a collision. Private credit stress is slamming into financial market volatility from the Iran conflict.

Volatile markets plus a cracking credit sector is exactly the kind of feedback loop that turned local problems into a systemic crisis in 2008.

The similarities go one deeper. Higher oil prices due to US adventurism in the Middle East also has a familiar ring.

(Crude went from US$25 a barrel in 2002 to US$147 a barrel by mid-2008.)

Back to the here and now, what makes this more alarming is the timing.

Dismantling the Warning System

This month, the US Treasury moved forward with plans to gut the Office of Financial Research (OFR). The agency was created after 2008 specifically to monitor risks like this.

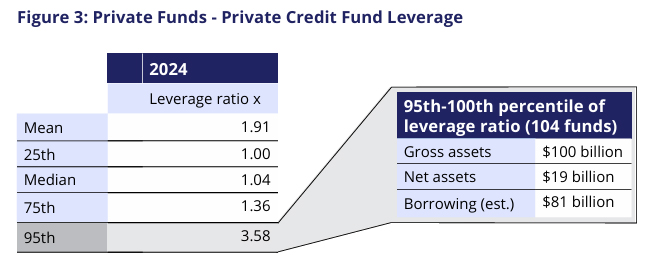

The irony is almost too neat. Just last month, the OFR published a report estimating that in 2024, US bank and non-bank lending exposure to private credit entities was between US$410 billion and US$540 billion.

And within these private credit groups, the average leverage was 1.91x — not dire on its own. However, the edge cases are where the trouble lies. At the 95th percentile of lenders, leverage hits 3.58x.

Source: OFR

Sadly, this data is from 2024. Private credit has been growing twice as fast as banking credit since then, so the current picture is likely worse.

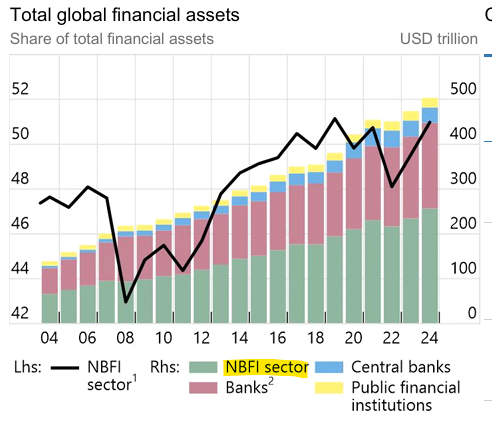

The latest review from the Financial Stability Board said non-bank financial intermediaries (NBFI), including hedge funds, private credit, pension funds, and insurers, now account for 51% of global assets.

Source: Financial Stability Board

Said another way, the ‘shadow banking’ system is now larger than traditional banks worldwide.

At US$256.8 trillion, that’s five times larger than when Lehman Brothers collapsed, and it nearly destroyed the global economy.

And now Washington’s firing the people paid to watch it.

The Cockroaches Keep Coming

Remember Jamie Dimon’s cockroach warning from October?

That was after subprime auto lender Tricolor went bust, followed by auto parts maker First Brands and its hidden US$2.3 billion in loans.

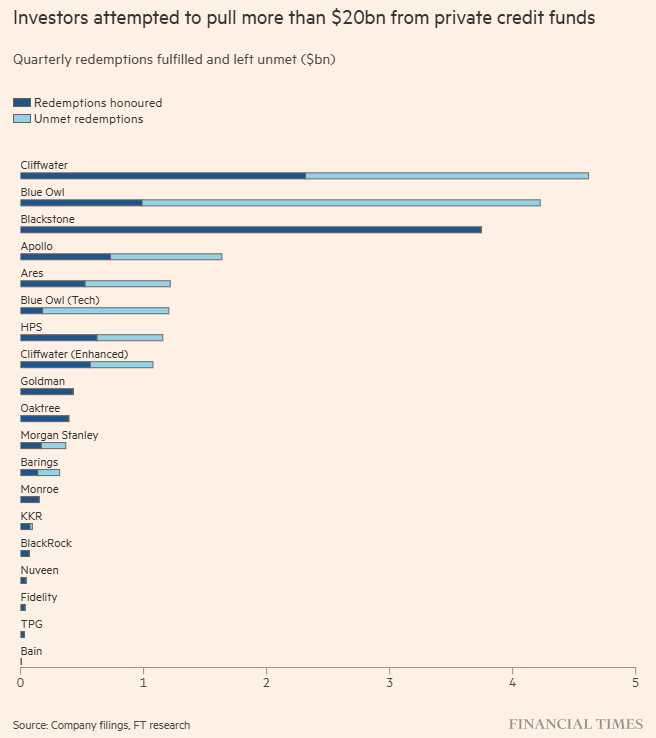

He was right. Since then, multiple private credit funds have had to restrict withdrawals from investors following a slew of mini panics.

Blue Owl’s Technology fund put the brakes on after investors pulled more than 40% of net assets in a single quarter. But it’s not alone.

Source: Financial Times

Now, BlackRock, Apollo, Ares, Blue Owl and Morgan Stanley have all limited redemptions.

Of those publicly listed, they’re now sporting share price declines of 30% this year alone.

The question going forward is: Is this systemic?

The latest Bank of America global fund manager survey is showing clear unease.

‘[Surveyed Institutional Investors] Cash allocations climbed to 4.2%–4.3%, marking the largest monthly increase since 2020, while the bank’s broader sentiment gauge fell to a six-month low…

…Risk perceptions have also changed. Geopolitical conflict is now seen as the biggest tail risk, cited by 37% of respondents, while 63% identified private equity and private credit as the most likely source of a systemic event.’

That last number is the one to sit with. Nearly two-thirds of professional fund managers now believe that if something breaks, it will break in private credit.

That’s not a fringe view. That’s consensus.

What This Means for Us

Australian super funds have been pushing up their allocations to private credit in recent years.

And our own $200 billion in private credit AUM has its own headaches.

After a widely negative surveillance report in November, by the Australian Securities & Investments Commission (ASIC), the watchdog is on the offensive.

A new probe into the sector this week is the opening salvo for further regulation to come. But will those changes come before it’s too late?

It’s worth remembering that if the sector enters a downturn, the pain will be felt here, even if the headline blowups are American.

If private credit stress spills into wider markets, the impact on equity portfolios (particularly growth), bond funds, and super balances could be severe.

Watch the redemption queues. Watch the default rates.

And watch what happens when the people paid to worry about this stuff are no longer on the payroll.

Source link