PFFR: REIT Preferreds ETF – Strong, Stable 7.9% Yield

Dragon Claws

The InfraCap REIT Preferred ETF (NYSEARCA:PFFR) is exactly what it says on the tin: a REIT preferred shares ETF. PFFR’s strong, stable 7.9% dividend yield makes the fund a buy. As the fund focuses on a small market niche, position sizes should be kept relatively small, in my opinion at least.

PFFR – Basics

- Investment Manager: Infrastructure Capital Advisors

- Underlying Index: Indxx REIT Preferred Stock Index

- Dividend Yield: 7.86%

- Expense Ratio: 0.45%

- Total Returns 5Y CAGR: 1.26%

PFFR – Overview and Analysis

Index and Portfolio

PFFR is a REIT preferred shares index ETF. The fund’s preferred behave quite similarly to high-yield corporate bonds, offering investors strong, albeit risky, yields, but little possibility of significant, long-lasting capital gains. These characteristics and tradeoffs should be of particular interest to income investors and retirees, although the risks might be excessive for more conservative, risk-averse investors.

PFFR’s underlying index is quite simple, including all U.S. REIT preferred shares meeting a basic set of inclusion criteria. Securities with yields lower than 3.0% are excluded. Not too many of these right now, but I’m sure there were many when rates were at zero. It is a market-cap weighted index, with issuer and sub-sector caps meant to ensure some diversification.

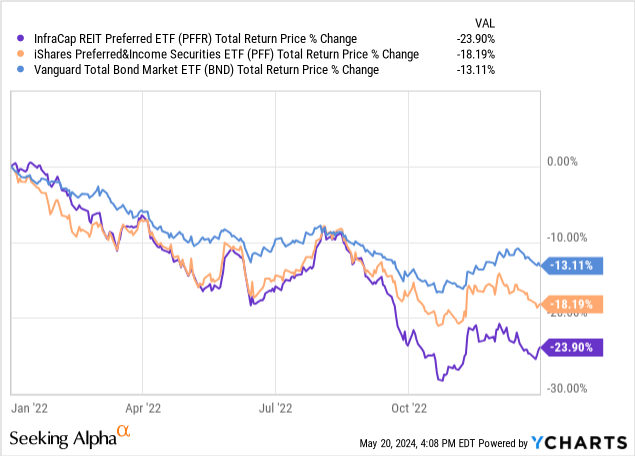

PFFR is an incredibly niche fund, investing in a subsegment, REITs, of a subsegment, preferred shares, of the fixed-income market. Due to this, diversification is quite low, and the fund’s performance could materially differ from that of broader bond or preferred indexes. Significant underperformance is possible. As an example, the fund posted significant losses and underperformance during 2022. Losses were due to a combination of higher rates leading to lower bond prices, and real estate industry weakness. Underperformance was mostly due to the latter.

Data by YCharts

Due to the above, PFFR is a much riskier choice than average. In my opinion, position sizes should be kept relatively small, so as to minimize the risk of significant underperformance at the portfolio level.

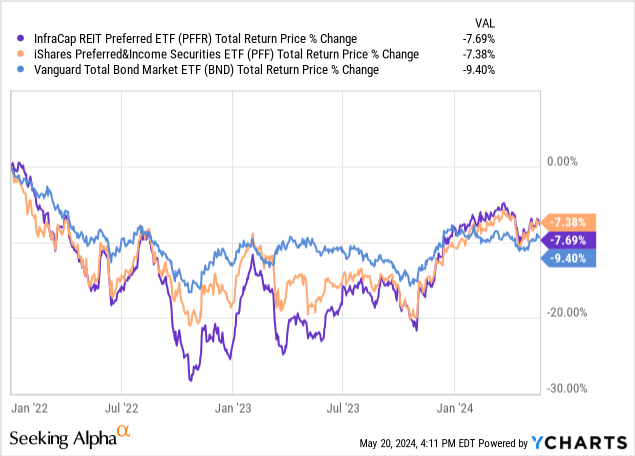

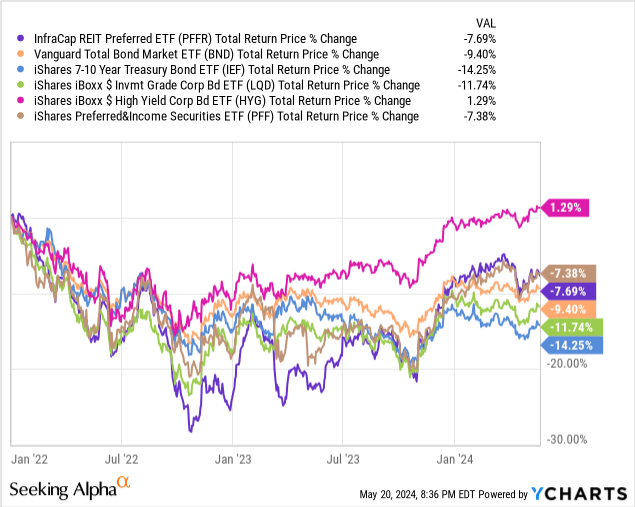

On a more positive note, underperformance was short-lived though, with the fund seeing comparable returns to its peers since 2022. It was still down though, as rates were up / remain high.

Data by YCharts

PFFR does provide diversified exposure to its market niche, with investments in over 100 securities, and with the top ten of these accounting for only 20% of its portfolio. It remains a niche, undiversified fund as a whole, however.

PFFR

Credit Risk Analysis

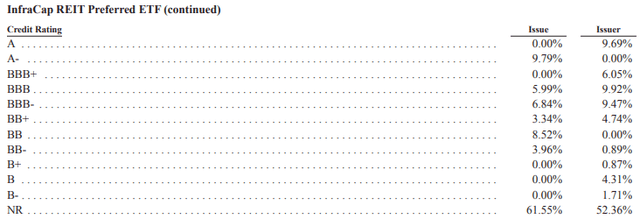

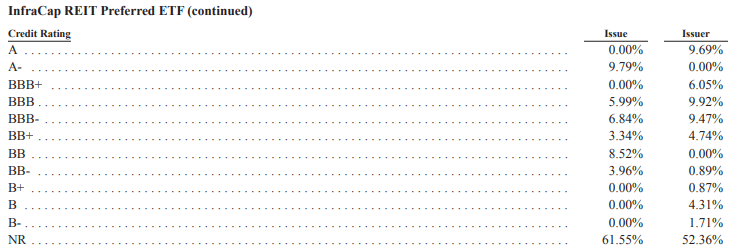

PFFR’s overall credit quality seems low. Most of its securities have no credit ratings. Of those that do, the average rating is BBB-, the lowest investment-grade rating available. Unrated securities tend to be riskier than average, so PFFR’s average security quite likely has the risk of a BB, perhaps B, rated preferred.

PFFR

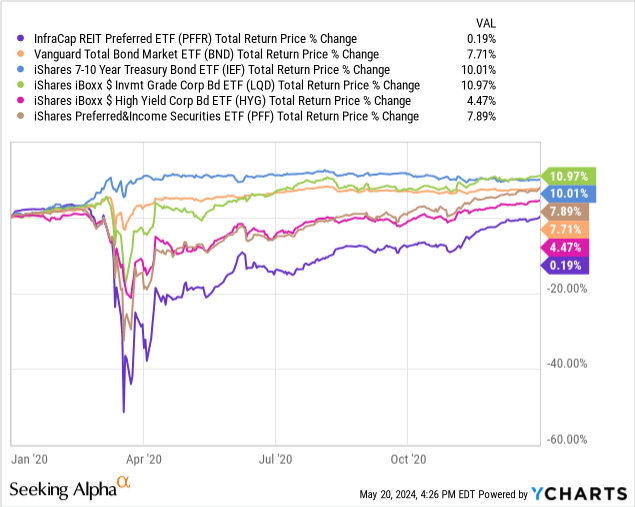

Due to the above, expect significant, above-average losses during downturns and recessions. As an example, the fund suffered a 50% drawdown during early 2020, the onset of the coronavirus pandemic. Losses were much higher than most bonds and bond sub-asset classes, including (broader) preferred shares. PFFR did start to recover by late March but remained behind its peers by year’s end.

Data by YCharts

Overall, PFFR’s credit risk seems quite high, higher than that of most bonds and bond sub-asset classes, including most other preferred and high-yield corporate bonds. I don’t find the fund’s credit risk to be excessive, considering it did mostly recover from pandemic losses within a year. More risk-averse investors might disagree.

Interest Rate Risk Analysis

Preferred shares have interest rate risk, same as bonds and other fixed-income securities. Unlike these other securities, I’ve had difficulties in finding detailed information about their duration or rate risk, as well as calculating or estimating these myself. Some preferred shares have extremely long maturities, some are perpetuals, some have fixed coupon rates, some variable, some fixed to variable. The situation is complicated and unclear.

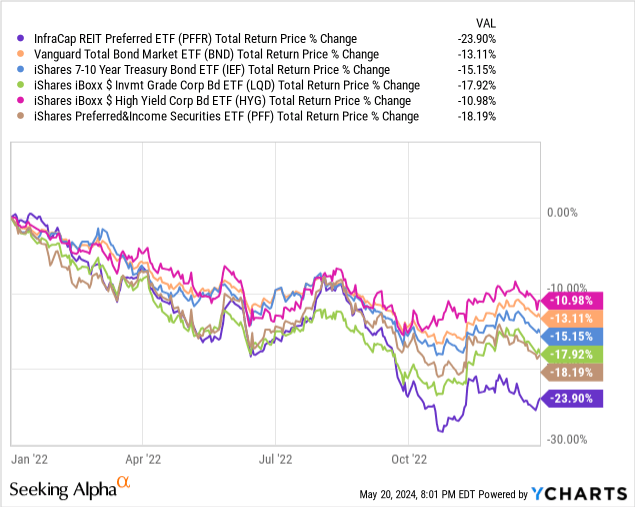

PFFR saw above-average losses during 2022 when the Fed started to hike. Results are consistent with above-average rate risk, but also with real estate sector weakness. I think sector weakness was key, but that is simply an educated guess from my part.

Data by YCharts

On a more positive note, PFFR has posted much stronger returns since, and the fund has actually slightly outperformed the average bond since 2022. It is still down though, same as most bonds.

Data by YCharts

Considering the above, I think it would be fair to characterize PFFR’s interest rate risk as moderate / average. Lots of uncertainty here though.

Dividend Analysis

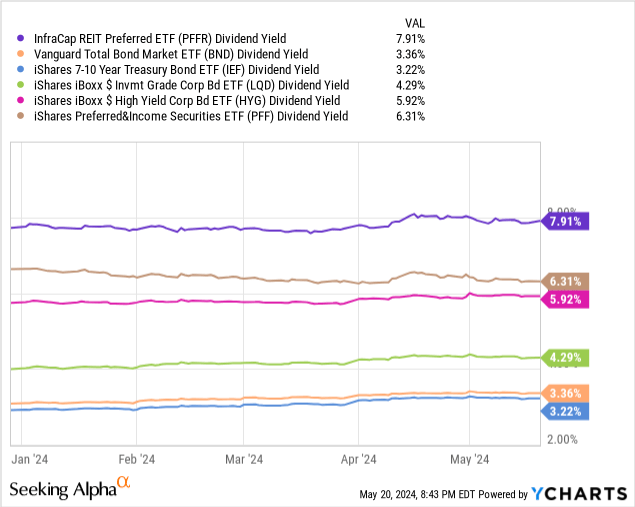

PFFR sports a 7.9% dividend yield, quite strong on an absolute basis, and higher than that of most bonds and bond sub-asset classes, including most other preferred shares and high-yield corporate bonds (there are exceptions).

Data by YCharts

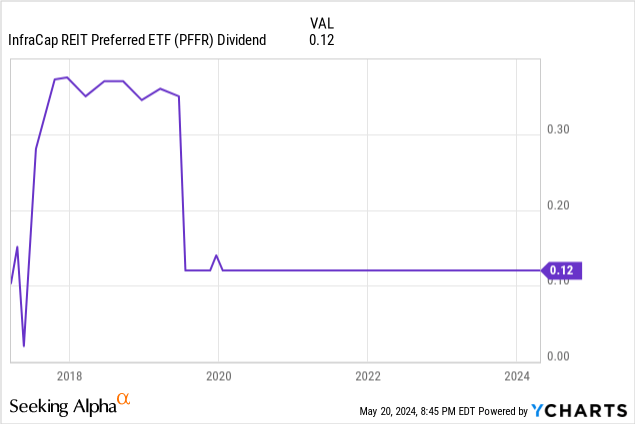

PFFR’s dividends have remained stable since early 2020, a bit after the fund shifted from quarterly to monthly dividend payments. Dividends fluctuated before, with no clear trendline.

Data by YCharts

PFFR’s dividend stability is at least partly a management choice. ETFs can choose to have stable dividends, same as CEFs, although they rarely do so, and there are some legal / regulatory considerations (ETFs must generally distribute any income and realized capital gains to shareholders). PFFR chose stable dividends, most ETFs do not.

Stable dividends are, of course, a positive for investors, especially retirees, as these ensure easy retirement planning.

PFFR’s dividends seem sustainable, although the situation is complicated.

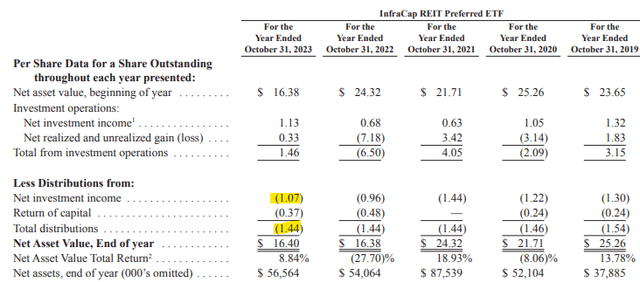

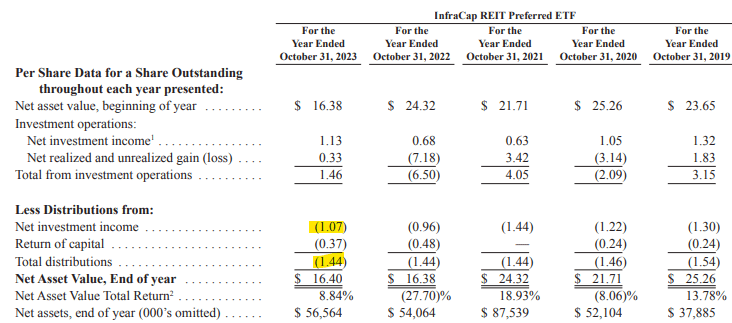

Latest figures show a 74% coverage ratio, which isn’t terrible, but definitely lower than desired. Coverage ratios were much lower in the past, too.

PFFR

Some REITs are able to classify their distributions as ROC due to favorable tax regulations, so the figures above understate PFFR’s ‘actual’ income. By my calculations, and from the fund’s holdings, the fund sports a 92% coverage ratio, a much more sustainable figure.

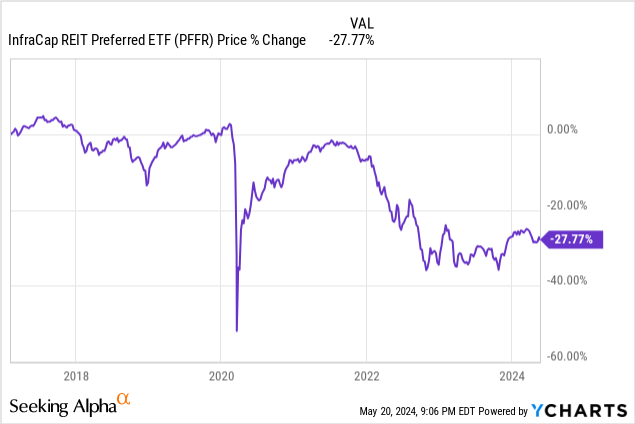

In my opinion, analyzing a fund’s share price can tell us a lot about its dividend sustainability. Declining share prices are indicative of unsustainable dividends, and vice versa. PFFR’s share price remained steady from 2017 to 2021, even though rates declined. Share prices went tumbling down from 2022 onwards, as rates rose. Results seem broadly consistent with some slight ROC / unsustainable dividends, but the significant rate volatility makes it difficult to know for certain.

Data by YCharts

In any case, PFFR offers investors a strong, stable 7.9% dividend yield. Dividends do seem sustainable, mostly.

Performance Track-Record

PFFR’s performance track-record seems adequate, with some complications.

Long-term returns are about average. Returns were boosted by the fund’s above-average dividends, harmed by above-average losses during the pandemic / early 2022.

Medium-term returns are similar to the above.

Short-term returns are much stronger, as rates have stabilized at a relatively high level.

There were significant, above-average losses during early 2020 and 2022, the two most recent down markets.

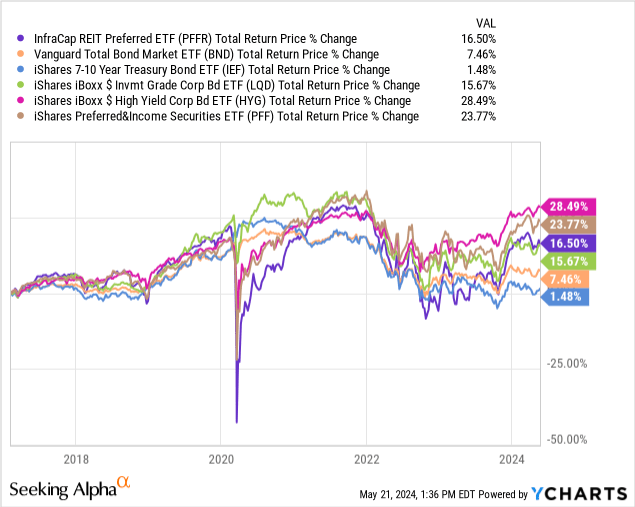

Returns are as follows.

Data by YCharts

In my opinion, prospective returns for the fund are quite strong, as dividend yields are quite high. These are ultimately dependent on many factors, including interest rate (movements), default rates, credit spreads, broader economic and industry conditions. I’m quite bullish, especially considering the fact that some of the prior losses and underperformance were due to idiosyncratic factors (REITs have been negatively impacted by higher rates much more than average).

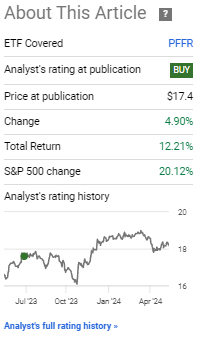

As a final point, I wrote a similar bullish article on PFFR in mid-2023. The fund has performed quite well since, seeing double-digit annual returns. Not too bad for a preferred shares ETF.

PFFR Previous Article

Conclusion

PFFR is a REIT preferred shares ETF. In my opinion, PFFR’s strong, stable 7.9% dividend yield makes the fund a buy. As the fund focuses on a small market niche, position sizes should be kept relatively small.

Source link