BSCO ETF: Time To Crystallize Your Gains (Rating Downgrade) (NASDAQ:BSCO)

William_Potter

Thesis

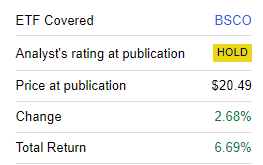

The Invesco BulletShares 2024 Corporate Bond ETF (NASDAQ:BSCO) is a fixed income exchange traded fund we covered before last year here. In our original piece we highlighted how the name was a term fund with matched maturity collateral, and thus represented a good risk/reward from a drawdown perspective for investors looking for yield. The fund has delivered since we voiced our opinion to continue holding the name:

Prior Rating (Seeking Alpha)

The original argument was around a steady, upsloping total return for the name given its analytics. Those parameters have been met.

In light of the fund’s maturity later this year and the extremely tight credit spread environment, we are going to revisit the name and analytics and opine on why it is better to sell now and invest in true risk free funds for the rest of the year as a cash alternative.

Term funds provide for lower risks

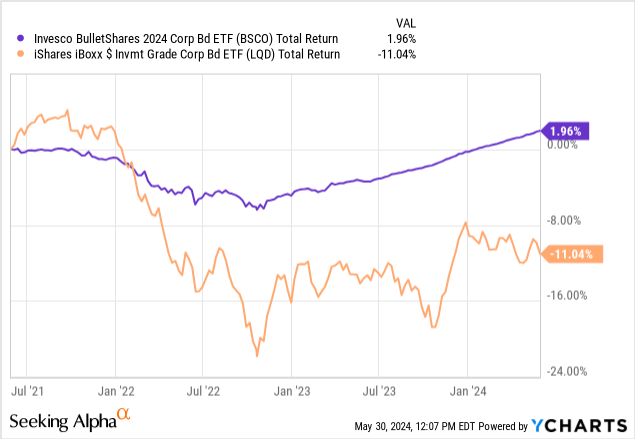

Properly structured term funds provide for better risk/reward metrics via shallower drawdowns. This is because the duration of the fund is ever decreasing, and the holders have a well defined view on how the collateral will perform going forward. BSCO fell in this category, and when compared to longer duration instruments from the investment grade fixed income space it has delivered:

When compared to the very popular iShares iBoxx Investment Grade Corporate Bond ETF (LQD), the fund has a very shallow drawdown profile, and has posted a positive total return in the past three years despite the violent move up in rates.

The beauty of maturity matched term funds is that in effect a retail investor buys into a ‘diversified bond’. The holdings are diverse, but they all have very similar maturity dates, thus you get the roll effect with the duration decreasing every year. The closer you get to the maturity date, the lower the sensitivity to interest rates, and you are guaranteed the original portfolio yield to maturity if there are no defaults in the underlying portfolio.

BSCO has delivered on those promises, even during a very adverse period of time from an interest rate perspective. Kindly note the fund is set to mature later this year:

The Fund will terminate on or about December 15, 2024 without requiring additional approval by the Board of Trustees (the “Board”) of Invesco Exchange-Traded Self-Indexed Fund Trust (the “Trust”) or Fund shareholders, although the Board may change the termination date. In connection with the termination of the Fund, the Fund will make a cash distribution of its net assets to then-current shareholders after making appropriate provisions for any liabilities of the Fund.

Source: Prospectus

While the fund has performed, let us have a look at its current analytics and see if an investor is best served to sell here and invest in a similar product.

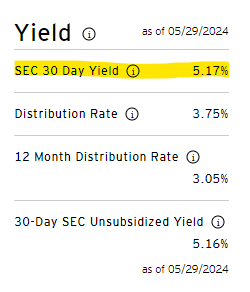

30-day yield is now below treasuries

If we look at the fund’s current 30-day SEC yield we will notice that it is below treasuries:

Yield (Fund Website)

The reason behind this occurrence is two pronged: on one hand it is a term fund with a very close maturity date and no reinvestment, and secondly spreads have tightened significantly. Basically the underlying bonds have already pulled back to par, thus the fund will not be able to make more than its cash flow yield going forward. Because the vehicle was structured in a lower rate environment, the portfolio yield is now below what risk free assets currently offer.

The fund contains only investment grade bonds, and thus has a very low credit risk, but it is not risk-less. At any point in time an investor should prefer treasuries over corporate bonds if they both yield the same. In our case BSCO is now riskier than treasuries and yields less. There is no reason to hold BSCO here because there is no upside, with the fund having already realized the vast majority of the capital gains from its portfolio. There is only downside via an unexpected default if a significant risk-off event would occur.

Unless there is a default in the portfolio, however, any small loss in the fund’s price will eventually be gained back as the maturity date approaches. Why take that risk though for a negative spread to treasuries with no upside whatsoever? People buy equities or long duration fixed income because there can be sizable capital gains. There are none to be had for BSCO from here to its maturity date. Just clipping the dividend yield.

Where should you put your cash if you sell?

BSCO was originally an investment grade corporate bond fund with a defined maturity date, and thus a defined duration profile. If investors are looking to re-allocate cash to duration IG bonds, there are several alternatives, such as LQD or the PIMCO Investment Grade Corporate Bond ETF (CORP) covered here.

As articulated in the CORP article, we are of the opinion that while rates duration is appealing here (i.e. rates are at historic highs), corporate spreads are too tight. The corporate bond market is pricing an immaculate soft-landing, with no room for error. IG bond spreads can easily double from current levels in a risk-off environment, hence our opinion to ‘Hold’ CORP rather than buy.

We would be more inclined to sell BSCO here and park that cash in treasury funds like the WisdomTree Floating Rate Treasury Fund ETF (USFR) covered here. USFR yields 5.32% and has no credit risk nor any duration risk.

Conclusion

BSCO is a fixed income fund. The vehicle contains investment grade corporate bonds, and has a term maturity in December 2024. The fund has a maturity matched portfolio, meaning the underlying credits are also set to mature by the end of the year. While this structuring choice reduces risk, it also caps any upside since the bonds are virtually trading at par currently. A holder in the name can only expect to clip the dividend yield for the rest of the year, yield which is now lower than what is offered by treasuries. With no upside, a lower yield than treasuries and the outside risk of a portfolio name default, one would be well served to sell BSCO here and buy USFR.

Source link