Metalla Royalty & Streaming: Valuation Starting To Improve (NYSE:MTA)

Falcor

While the gold miners group is finally starting to claw back lost margins after three years of elevated inflationary pressures with help from the gold price, the royalty/streaming group continues to report record margins. Simultaneously, several of them have been bulking up their portfolios and adding assets at deep discounts to fair value. Unfortunately, while Metalla (NYSE:MTA) has succeeded in growing its royalty portfolio, new additions haven’t done much from a cash flow standpoint, and we’ve seen a mountain of dilution with shares going out the door at a deep discount to NAV as well, which has partially offset NAV/share growth. In this update, we’ll dig into the Q1 results, recent developments, and how Metalla’s valuation stacks up vs. some of its peers.

All figures are in United States Dollars unless otherwise noted. G/T = grams per tonne of gold. GEOs = gold-equivalent ounces

Q1 & FY2023 Results

Metalla Royalty & Streaming (“Metalla”) released its Q4 and Q1 results in March and May, respectively. Beginning with its annual results, the company ended the year with 102 total royalties and streams after a busy year for acquisitions (Lama Project royalty, Alamos royalty portfolio, Nova Royalty acquisition), up from 73 previously. And while this didn’t do much for near-term cash flow with only one producing royalty at Aranzazu, the acquisitions have complemented an already deep pipeline of royalty assets with multiple copper royalties added that could come online by the end of the decade. Elsewhere, the company sold its JR mineral claims that make up its Pine Valley property (part of Cortez Complex in Nevada) to Barrick/Newmont and retained a 3.0% NSR after the receipt of $5.0 million in cash.

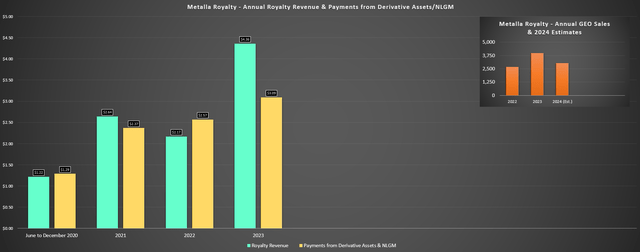

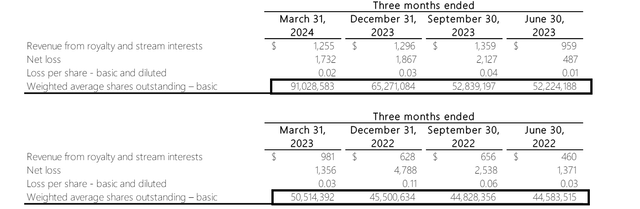

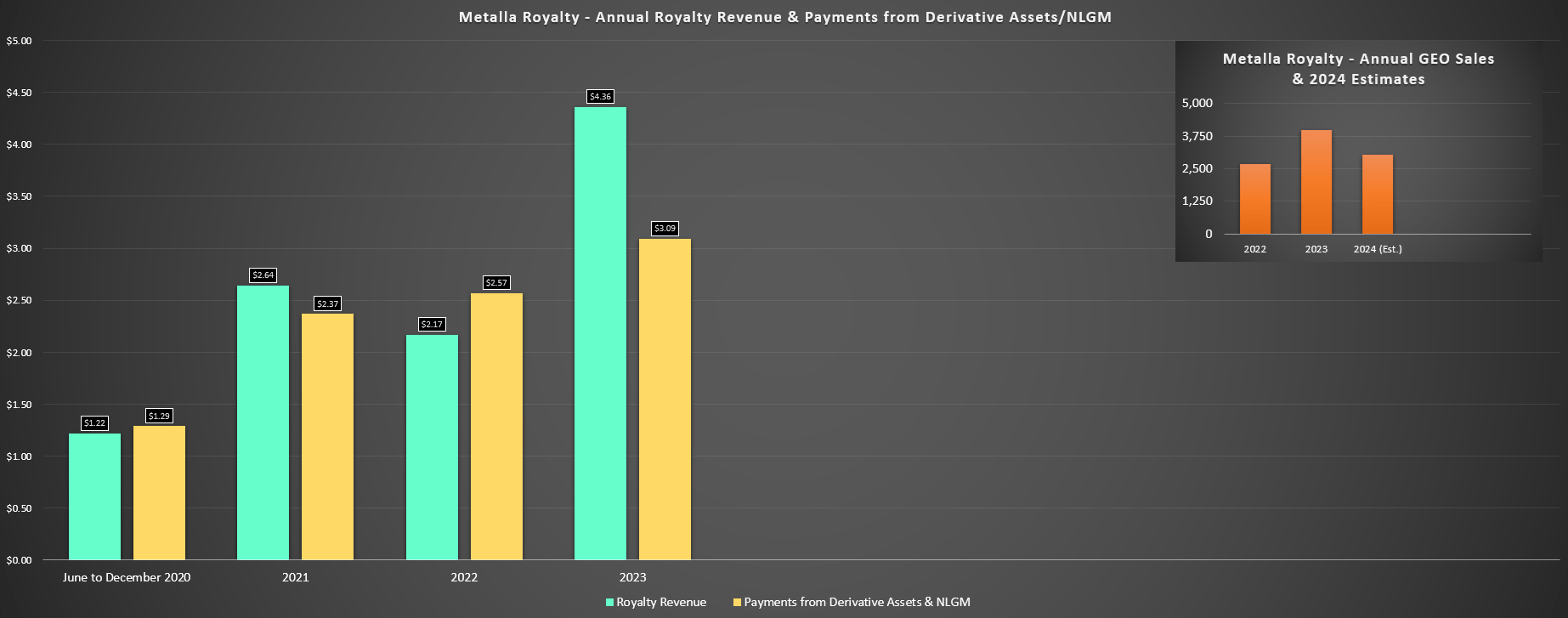

Looking at Metalla’s FY2023 financial results, the company reported gold-equivalent ounce volumes of 3,989 GEOs at $1,867/oz, with revenue from royalty/stream interests and fixed payments of $4.6 million. The company also received payments from its Higginsville derivative royalty asset of $2.9 million, but this flagship royalty, which contributed nearly 40% of 2023 GEOs has since hit its cap and will no longer contribute to Metalla’s results. Despite the increase in revenue and attributable GEOs, Metalla reported a net loss of $5.8 million for the year, with $2.4 million in royalty interest impairments, higher G&A expenses (~$4.9 million vs. ~$3.9 million), partially offset by higher gross profit (~$2.2 million) and the one-time gain on its JR mineral claims sale.

Metalla Annual Royalty Revenue & Payments From Derivative Assets + Annual GEO Sales – Company Filings, Author’s Chart & Estimates

While it was positive to see royalty revenue and GEOs trending in the right direction the past two years given the significant capital outlays by the company and doubling of the share count, 2024 is expected to be a softer year with guidance of 2,500 to 3,500 GEOs. The lower GEO sales is related to no contribution from its Higginsville royalty which was its most significant contributor in 2023 and declining royalty revenue from El Realito which has moved into residual leaching, offset by new contributions from Aranzazu (1.0% NSR) and new contribution from Tocantinzinho which is set to start commercial production by Q4 of this year. Hence, while we will see a 20%+ dip in GEOs this year, we should see a solid recovery in 2025.

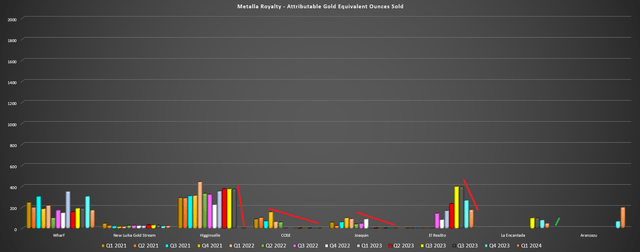

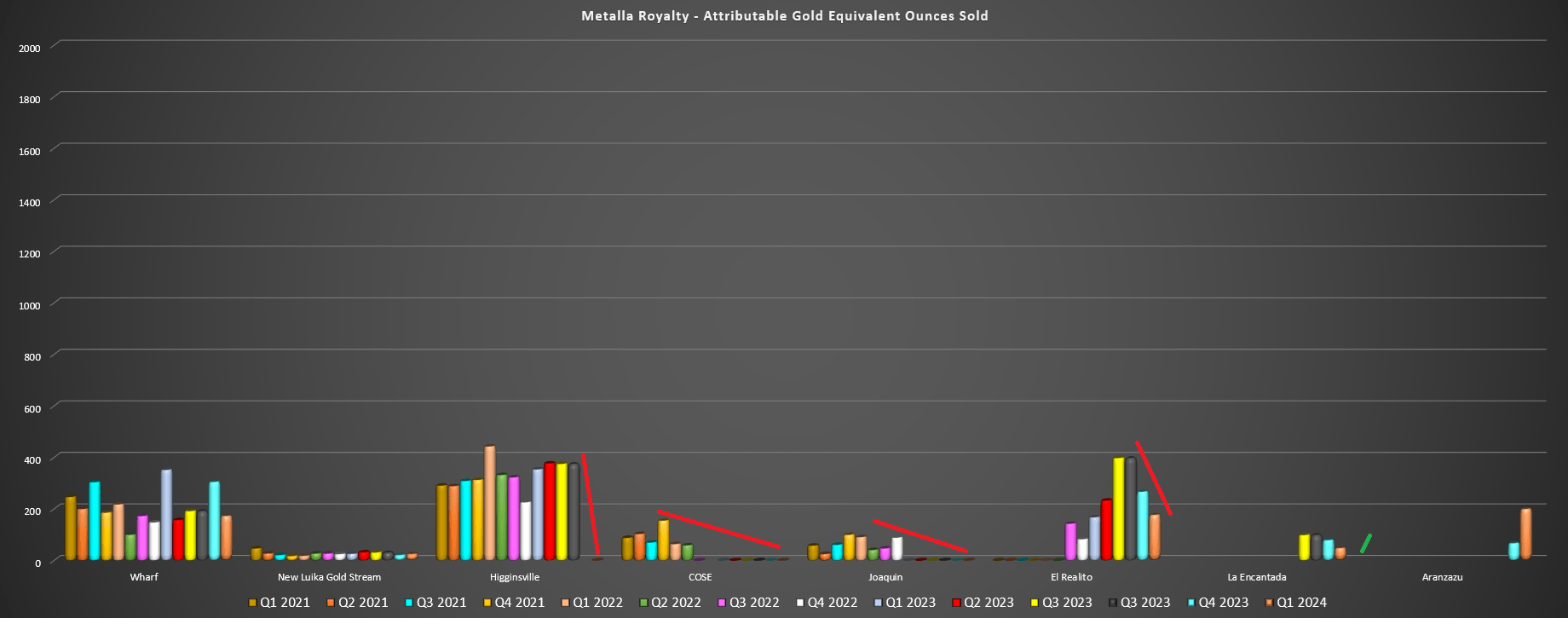

Metalla Quarterly GEOs by Asset – Company Filings, Author’s Chart

Moving to the quarterly results, Metalla has had a tough couple of years as shown above, with COSE and Joaquin moved into care and maintenance, water issues at La Encantada that have weighed on production, its Higginsville payments hitting their cap, and El Realito production also winding down (La India Mine). Fortunately, the company did get some good news with First Majestic (AG) uncovering a new water source at La Encantada that will result in operations moving back to normal throughput rates in Q3. Meanwhile, Agnico Eagle (AEM) shared that its relatively small AK deposit will head into production by year-end, providing a small boost to GEO sales on top of contributions from Aranzazu and Tocantinzinho (new producing assets).

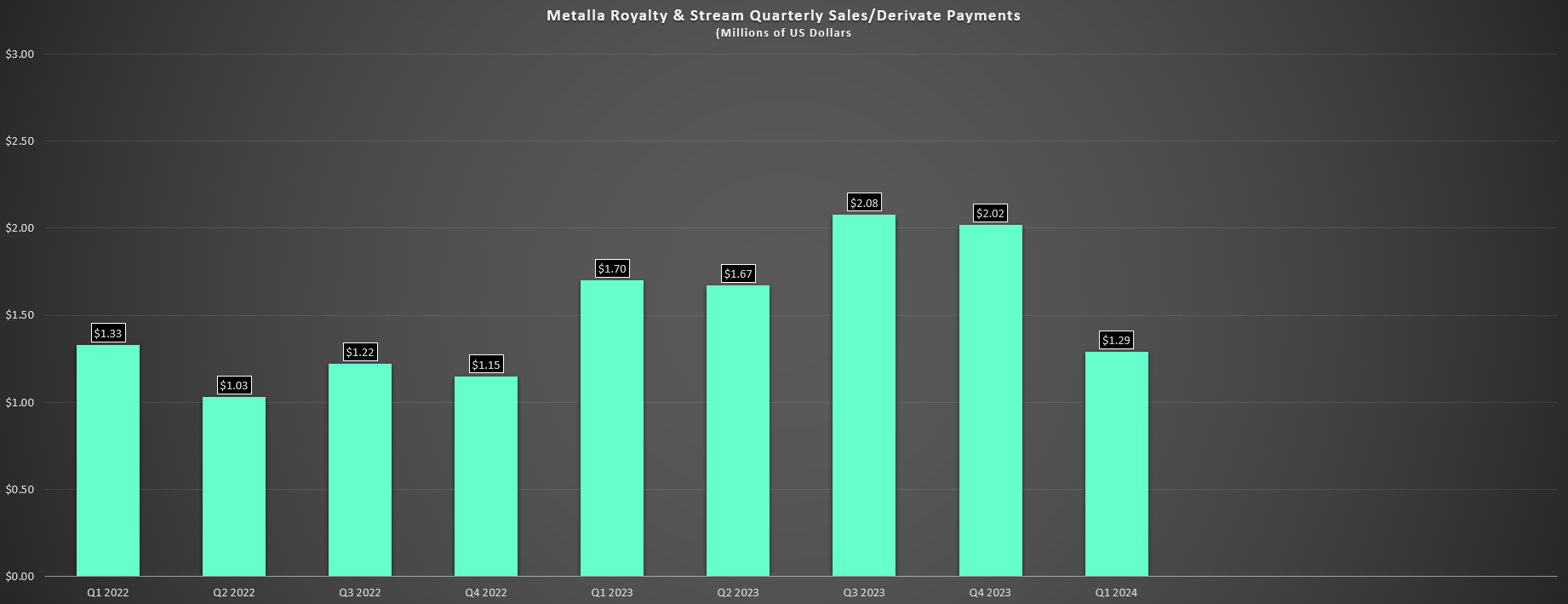

As for the financial results, Metalla reported royalty/stream revenue of ~$1.3 million on 624 GEOs and a cash margin of $2,061/oz from its five producing assets. This was an improvement from the year-ago period. Fortunately, the company will have easy comparisons in Q2 2024 as well, with Q2 2023 revenue of just ~$960,000. On a positive note, Metalla has suspended its At-The-Market equity agreement [ATM] and will benefit from much higher gold prices in Q2 and 2024. So, while production will be lower year-over-year, the company should still generate close to ~$7.0 million in revenue this year.

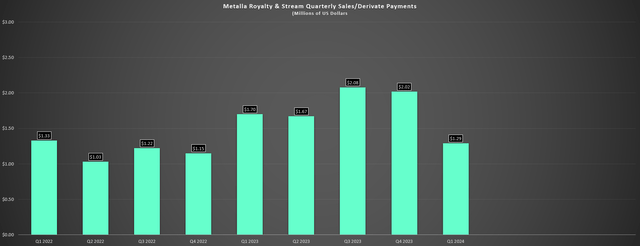

Metalla Quarterly Revenue – Company Filings, Author’s Chart

Finally, Metalla ended the quarter with ~$11.0 million in cash and cash equivalents, offset by ~$12.5 million on its Beedie convertible loan facility. This facility was recently amended and restated, with the maximum available increasing to C$50.0 million, and the conversion price adjusted to C$6.00 per share with maturity of May 10, 2027. Metalla currently has C$30.9 million available under the amended facility, and cash declined slightly at the beginning of Q2 with a payment of $0.7 million to settle its Castle Mountain loan. While the continued net losses are disappointing, more important to the company is where the portfolio is going and how its royalty portfolio looks, which we’ll dig into below:

Recent Developments

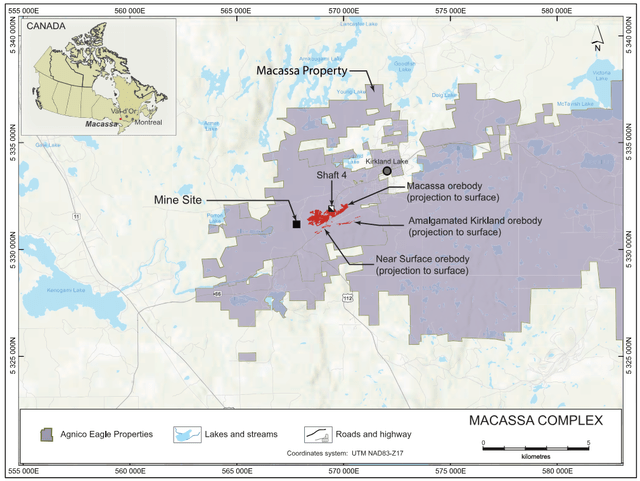

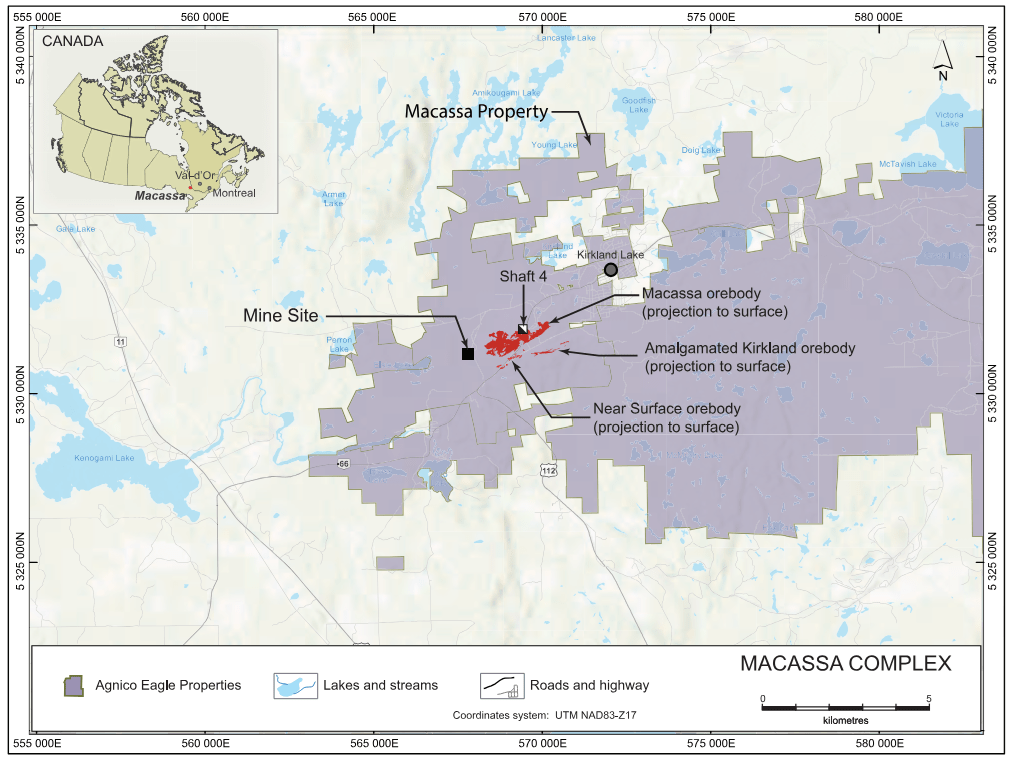

Digging into recent developments and starting with Metalla’s royalty assets owned by Agnico Eagle, developments have been mixed. Starting with Amalagamated Kirkland, it’s positive to see Agnico Eagle providing an initial date for the start of production at Amalgamated Kirkland (“AK”) of Q4 2024, with it sounding like this asset could contribute up to 30,000 GEOs per annum between 2025 and 2028, with ore to be trucked east to the company’s LZ5 processing facility (LaRonde). This will give Metalla another producing asset, but with just a 0.45% NSR, it doesn’t look like we’ll see much over 130 GEOs per annum or ~$300,000 in contribution to Metalla from this asset.

Kirkland Lake Camp/Macassa Complex – Agnico Eagle Mines

As for Wasamac, this is certainly a solid asset with a lot of potential longer-term, and it certainly looks like this could become an important source of feed for the hungry Malartic Mill post-2027. Assuming mining/haulage rates of ~5,000 tonnes per day, an average grade of 2.50 G/T of gold and ~95% recoveries, this would translate to annual production of ~140,000 ounces per annum. And while this would be a very meaningful contribution for a company of Metalla’s size (1.5% NSR, but likely 1.0% NSR with ~$5.2 million buyback option on 0.5%), the more conservative production date looks to be H2 2028 or later, a downgrade from Yamana’s plans, with it targeting 2026 production and a 2024 construction start.

Obviously, keeping the ounces in the ground for a few more years isn’t a huge issue to Metalla as it will still likely benefit from all these ounces. However, Wasamac would have significantly improved Metalla’s medium-term cash flow profile and will not under the current schedule, given that it’s now schedule to come online at the same time as other major assets closer to the end of the decade.

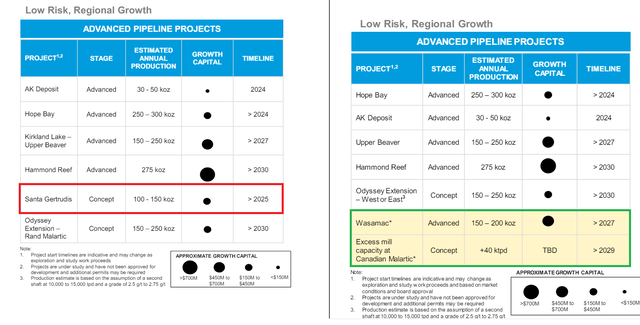

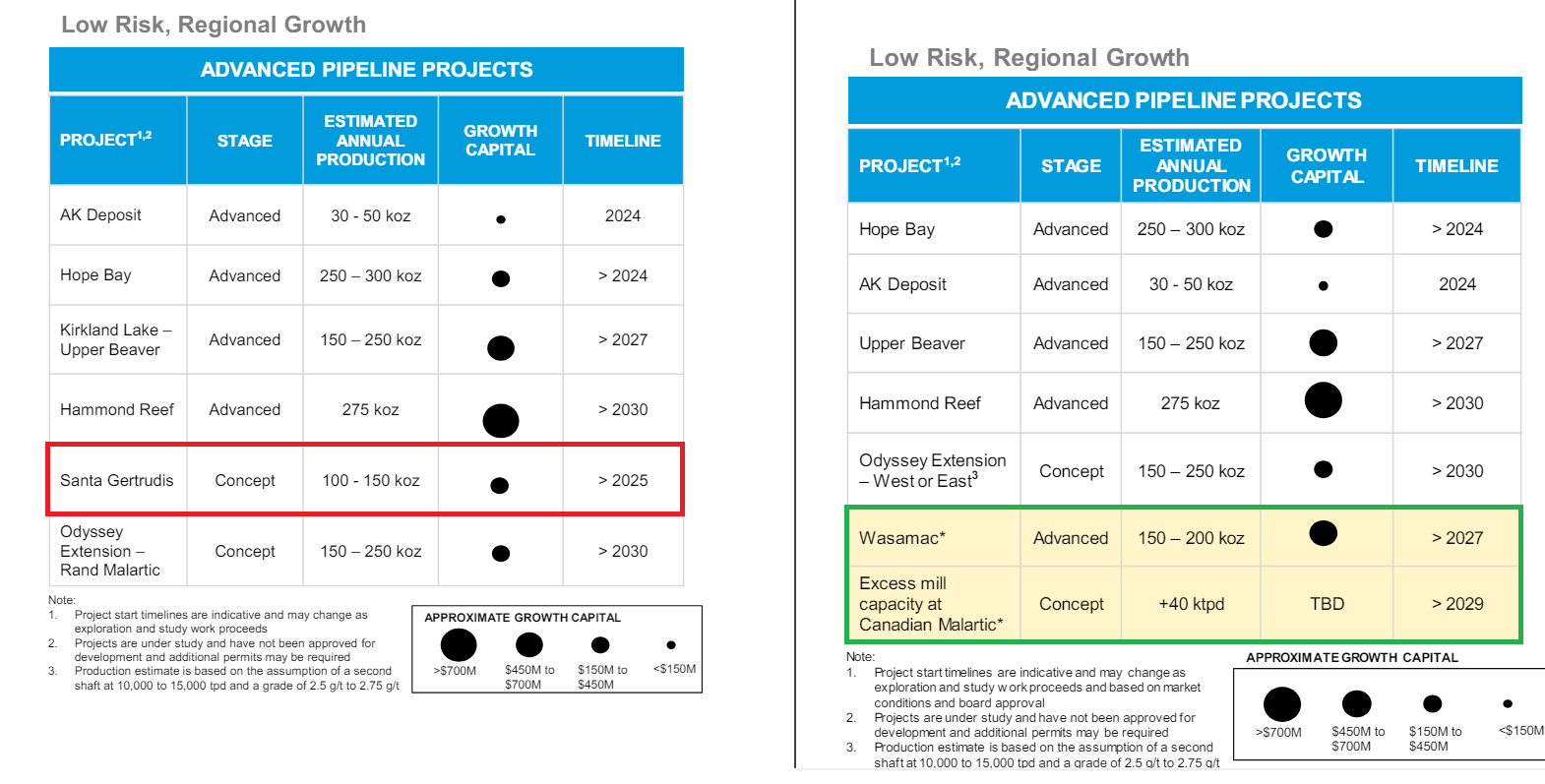

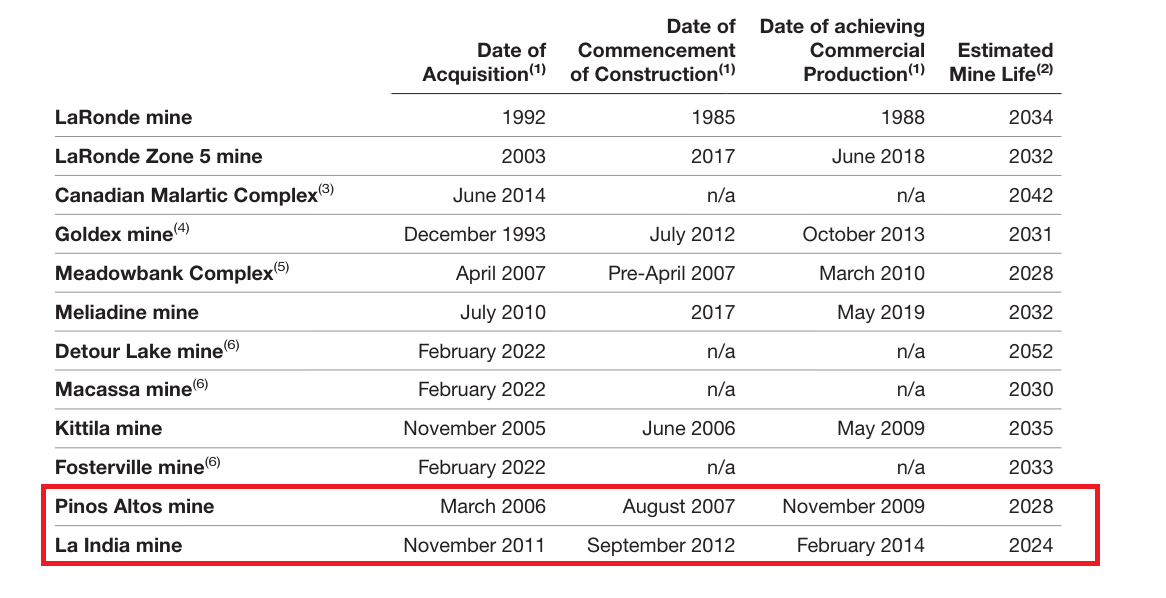

As for the negatives, the new contribution in 2025 from AK will be massively offset by the ~1,000 fewer GEOs from El Realito (2023) and ~500 GEOs this year (2024), with Agnico’s La India Mine (El Realito) set to move offline by 2025 with residual leaching now underway. Meanwhile, exploration expenses declined materially last year in Latin American (primarily Santa Gertrudis), with spending down from ~$24.1 million to ~$13.6 million. Simultaneously, Santa Gertrudis is missing from Agnico’s “low-risk regional growth” slides, with the 2022 and 2023 presentations side by side below. This isn’t surprising given that Agnico is looking for bigger assets than 100,000 to 150,000 ounce mines, with San Nicolas looking like the higher priority where it will transition its Mexican workforce, with short mine lives at La India and Pinos Altos.

Agnico Eagle Low-Risk Regional Growth Opportunities – Company Presentations (2023 vs. 2022) – Agnico Website Agnico Eagle Estimated Mine Lives – Company Filings

Obviously, a less clear future in regard to the development of this Mexican gold-silver asset (Santa Gertrudis [*]) is not the end of the world. However, Metalla was initially calling for production from this asset by 2026, and it made up a chunk of the company’s NAV given that its 2.0% NSR would have translated to up to 3,000 GEOs per annum. As it stands, I don’t see a clear path forward for Santa Gertrudis this decade, and I’m not sure that Agnico will develop it at all given that it has high return opportunities with organic growth potential at Detour Lake, Canadian Malartic, and hub & spoke opportunities at Upper Beaver and Wasamac. So, similar to Wasamac, this is a downgrade to the previous medium-term cash flow profile, but worse in this case as Wasamac is likely to be developed, and Santa Gertrudis may not meet the size requirements for Agnico given its larger scale at 3.5-4.0 million ounces [*].

[*] Santa Gertrudis has resources of ~2.0 million ounces of gold and ~38 million ounces of silver. Generally, producers of Agnico’s scale are looking for 200,000 ounces per annum assets minimum (Santa Gertrudis: 100,000 to 150,000 ounces), unless it can develop mines like Wasamac/Upper Beaver/AK that provide feed for existing processing facilities that have excess capacity like the Malartic Mill and LZ5. [*]

Moving to other assets where we’ve seen positive developments, Tocantinzinho is progressing well, with total project progress 93% complete and construction 95% complete. Metalla owns a 0.75% GVR on Tocantinzinho and this will become its most significant contributor to annual GEOs behind Wharf and Aranzazu when it comes online later this year. Based on the current schedule, commercial production is expected to start by Q4 2024, and Tocantinzinho should contribute close to 1,000 GEOs for Metalla in 2025 and average ~1,500 GEOs in Year 2 through 5 or upwards of $3.0 million of annual contribution to Metalla.

Tocantinzinho Production Profile – G Mining Presentation

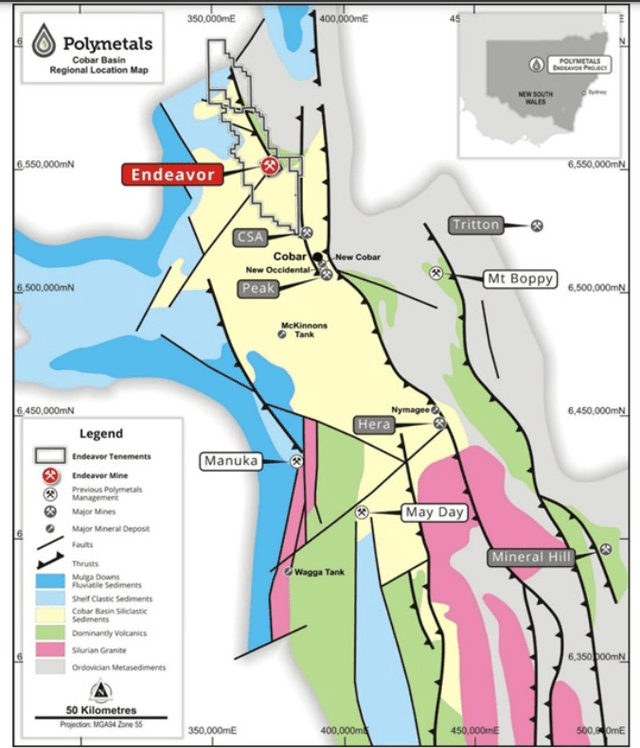

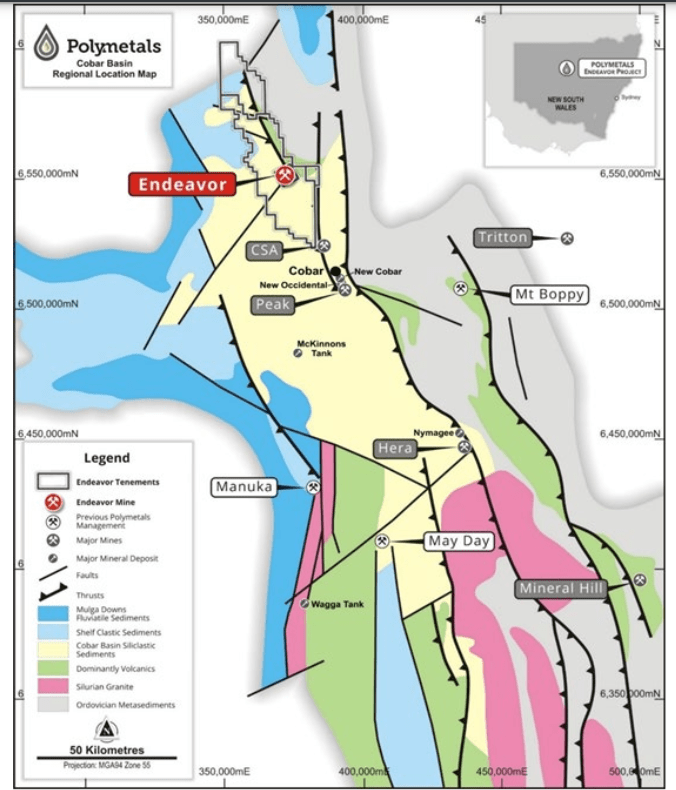

Elsewhere in Australia, the restart of the Endeavor polymetallic mine (silver, lead, zinc) is looking more likely, with this asset expected to generate over upwards of $130 million in revenue per annum with a triple-digit IRR at higher metals. Previously, it wasn’t clear whether Polymetals would be able to restart the mine even with its modest pre-production capex (~$16 million) given that it’s a relatively small company and it wasn’t getting much help from silver or zinc prices at the time of its 2023 restart study. However, the project’s IRR is looking far better with silver near $30.00/oz near $23.00/oz in the 2023 study, and the surge in zinc prices doesn’t hurt either. Plus, Polymetals now has a strategic alliance with Metals Acquisition (MTAL) with it planning to invest up to ~$3.5 million.

As for the benefits to Metals Acquisition [MAC], the past-producing Endeavor Mine sits just 30 kilometers north of MAC’s CSA Mine and there is the potential for MAC to treat high-grade ore from CSA at Polymetals’ facilities. In addition, Polymetals has agreed to provide excess water offtake to MAC, which could allow MAC to increase throughput at CSA. Overall, this looks like a win-win for both parties, and Metalla certainly benefits as well, given that the Endeavor Mine could contribute upwards ~2,000 GEOs per annum if restarted over a 10-year mine life, with the potential for production to move back online by H2 2025. MAC had the following to say about the deal:

Endeavor Mine Location & CSA Mine (Cobar Region) – Polymetals Presentation

By investing in POL, we are creating a partnership to achieve better outcomes for both companies. We have known the POL management team for over 20 years, they bring a wealth of experience to the area and have the ability to operate mines very efficiently and we are very supportive of their efforts to reopen the Endeavor mine as well as exploring their immediate mine environment which like the CSA Copper Mine is very underexplored for all base metals including copper.”

– MAC CEO, Mick McMullen

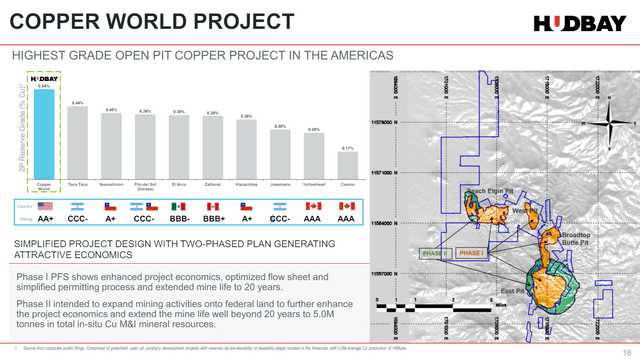

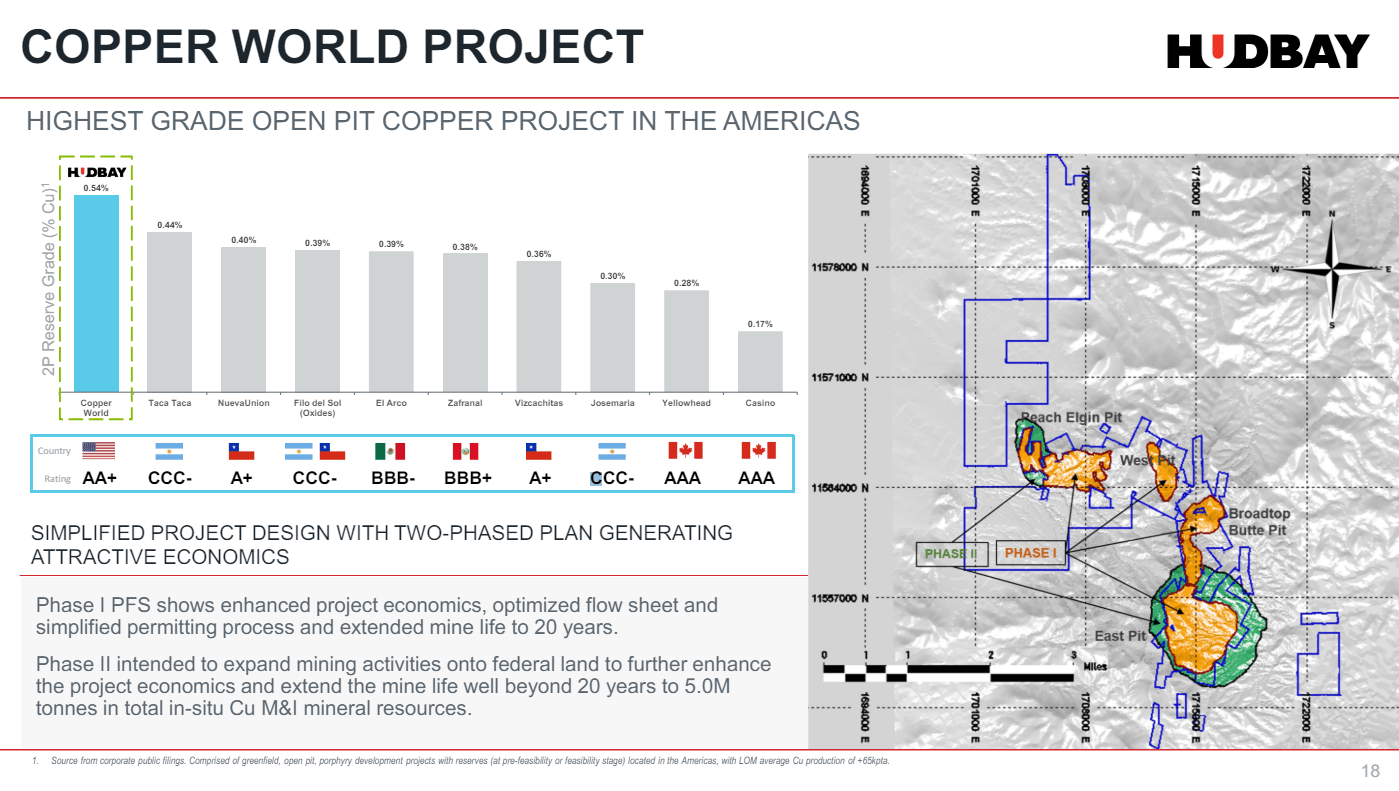

Finally, looking at other developments, Hudbay (HBM) has reiterated that it expects to receive its remaining two state permits at Copper World this year, and that it has seen strong interest from potential joint-venture partners. While it’s not clear on a start date, this asset could start production by 2026 and be in production before 2029 and be producing ~90,000 tonnes per annum of copper in the first ten years. This would translate to nearly 1,500 GEOs per annum to Metalla, another decent boost to its annual GEOs. As highlighted below, Copper World in Arizona is a phenomenal asset, with some of the highest grades among other open-pit copper projects in the Americas.

Copper World Grades vs. Other Open-Pit Projects – Hudbay Presentation

Last but not least, IAMGOLD (IAG) continues to build on its resources at the Gosselin Project, which sits directly next to its newly producing Cote Gold Mine. In fact, Gosselin resources increased to ~4.4 million ounces in the indicated category at 0.85 G/T of gold, with an additional ~3.0 million ounces at 0.75 G/T of gold in the inferred category. This is a monster deposit being uncovered that’s consistently reporting some of the thickest intercepts of gold mineralization in North America, and it should help to smooth out the Cote Gold mine plan.

The only minor negative for Gosselin (*) is that while it may be significant in scale and looks like it could contain up to 5.0 million ounces of reserves, there is no significant rush to put it into production unless IAMGOLD is looking to undergo a major throughput expansion. This is because Cote Gold (current mining area) has the higher reserve grade (~1.0 G/T of gold) vs. Gosselin. Hence, I see Gosselin as more likely to come in during 2030 to help smooth out the production profile and also add onto the back of the mine life vs. displacing Cote Gold ore which is higher-grade. This is not to suggest that this is not an extremely valuable asset for Metalla given that it has a 1.35% NSR on what could be upwards of 5.0 million ounces of gold reserves, but the value is not as significant vs. having a royalty on Cote like Royal Gold (RGLD), which will benefit from these ounces now vs. at the end of this decade or later when discounting out this cash flow.

(*) Metalla has a 1.35% covering all of the Gosselin Project, but its royalty on Cote (which just announced its first gold pour) covers less than 10% of reserves. (*)

In total, the positives have certainly outweighed the negatives at Metalla’s royalty assets and while an unclear future for Santa Gertrudis (lower priority) and timelines being pushed significantly at Wasamac and Castle Mountain P2 vs. previously provided estimates are negative, these developments aren’t the end of the world. Plus, the resource growth at Gosselin has given Metalla another cornerstone asset in its portfolio. Let’s take a closer look at Metalla’s growth profile below:

Growth Profile

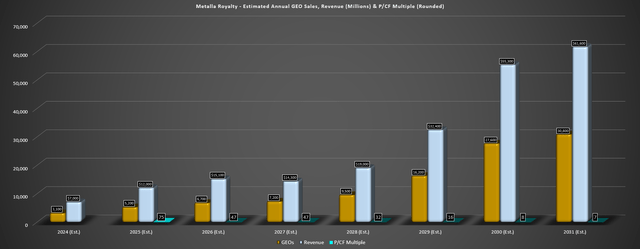

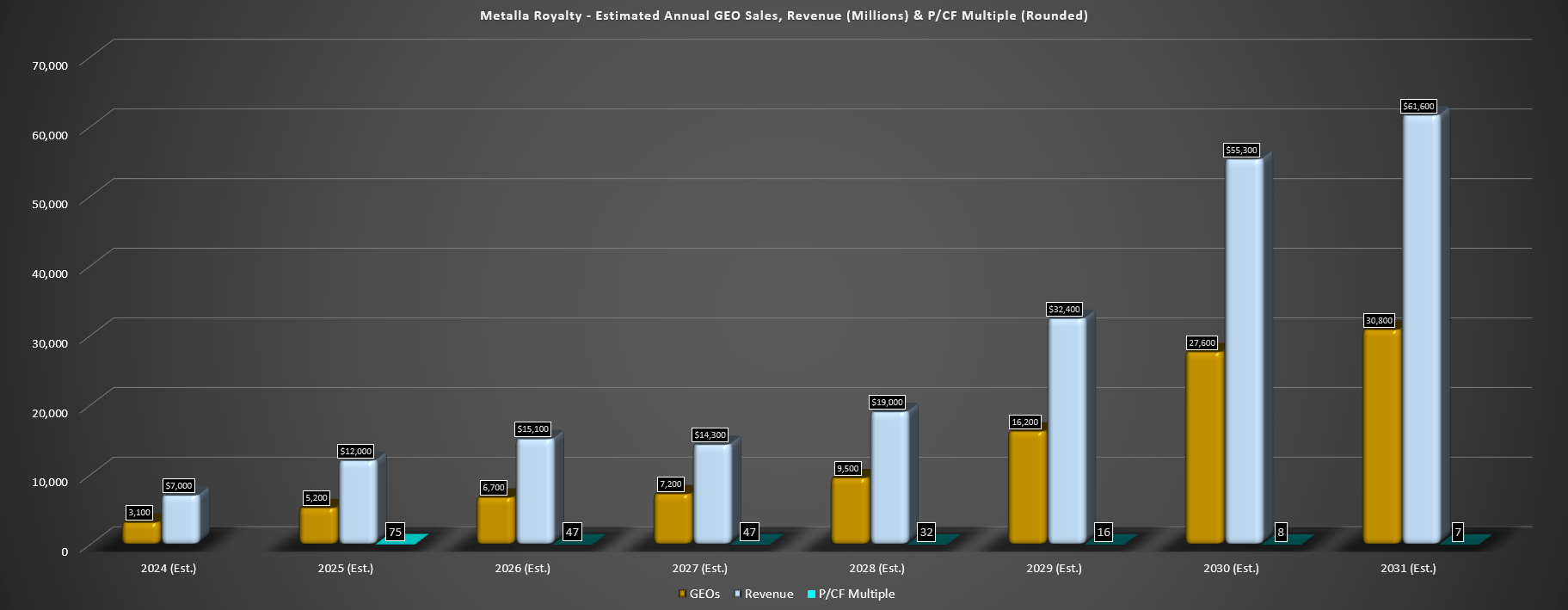

Although Metalla may not be generating much revenue today, it has assembled a portfolio with significant growth potential. This includes expected contributions from gold assets like Wasamac and Castle Mountain Phase 2 and Gosselin (Cote Mine), as well as copper assets like Copper World, Taca Taca, Vizcachitas, Josemaria, and West Wall. However, several of these are mega projects that are longer-dated with longer construction timelines and permitting still to be completed, and while the company could see growth towards sales of 5,000 GEOs next year, it won’t see a significant ramp-up in attributable GEO sales until 2028. That said, if all of its advanced and semi-advanced royalty assets come online as planned, Metalla could see sales of up to 30,000 GEOs in 2031 or ~$62 million in revenue at a conservative $2,000/oz gold price.

Metalla Royalty Estimated Annual Gold-Equivalent Ounce Sales, Revenue (Millions) & P/CF Multiple – Company Filings, Author’s Chart & Estimates

This significant royalty portfolio with superior depth relative to peers gives Metalla an advantage vs. others like Elemental that will have to build up their portfolio in a competitive environment and have yet to add many long life assets, never mind having a portfolio built around much smaller operators. However, some of this growth looks priced into Metalla’s stock today. In fact, Metalla is trading at over 75x FY2025 cash flow estimates and over 25x FY2028 cash flow estimates, comparing very unfavorably to names that also have solid pipelines and larger scale yet trade at barely 16x FY2025 cash flow estimates today like Royal Gold.

Valuation

Based on ~97 million fully diluted shares and a share price of US$3.25, Metalla trades at a market cap of ~$315 million, which compares quite favorably to its estimated net asset value [NAV] of ~$540 million (5% discount rate, $2,250/oz gold price 2024-2026, $2,000/oz long-term gold price). However, unlike some of its junior royalty/streaming peers that are generating significant cash flow already, the bulk of Metalla’s NAV is tied to its development stage assets and its attributable production growth is heavily weighted to the back end of this decade, relying on mega-capex assets coming online like Copper World, Taca Taca, Castle Mountain Phase II, and Vizcachitas.

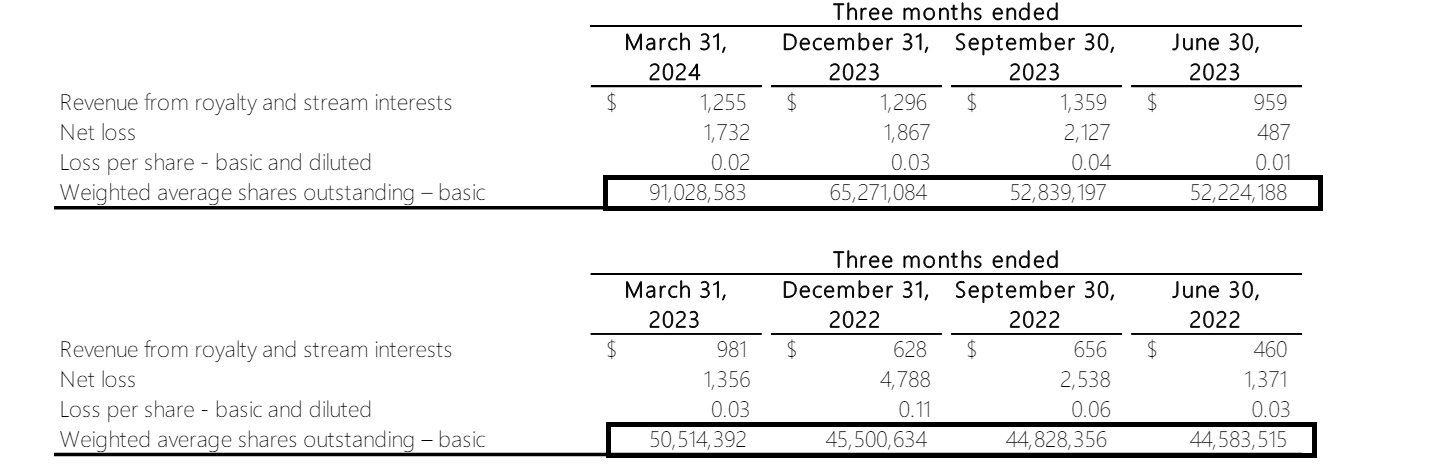

So, while companies like Vox and EMX have active buyback programs and can add new royalties over the next two years while maintaining or reducing their share counts (suggesting higher growth in NAV per share), Metalla is not in similar shape near-term with limited cash flow generation. In fact, since Q1 2023 alone, Metalla issued ~33.9 million shares for its Nova Royalty acquisition, ~310,000 shares to Trinity Advisors and PI Financial in shares for services agreements (Nova acquisition), ~1.4 million shares for other royalty acquisitions, ~665,000 shares under its ATM, 2.8 million shares in a private placement with Beedie Capital, and an additional ~430,000 shares at ~US$2.55 for accrued and unpaid interest as part of its convertible loan (~$13.0 million outstanding). The result is that its fully diluted share count increased nearly 90% year-over-year (Q1 2023 to current) with its FD shares up from ~55 million to ~97 million.

Metalla Quarterly Revenue, Net Losses & Weighted Average Shares – Company Filings

Plus, while Metalla prides itself on consistently completing royalty transactions at a significant discount to NAV, it’s tough to argue for significant value creation in these deals when it’s been buying assets at a discount while issuing shares at a similar discount to NAV in some of these instances. And while most junior royalty companies have little choice but to issue shares to grow their portfolio in their infancy, I think it makes sense to be more judicious regarding new acquisitions if it’s going to come at the cost of significant share dilution and their shares are trading at a significant discount to NAV.

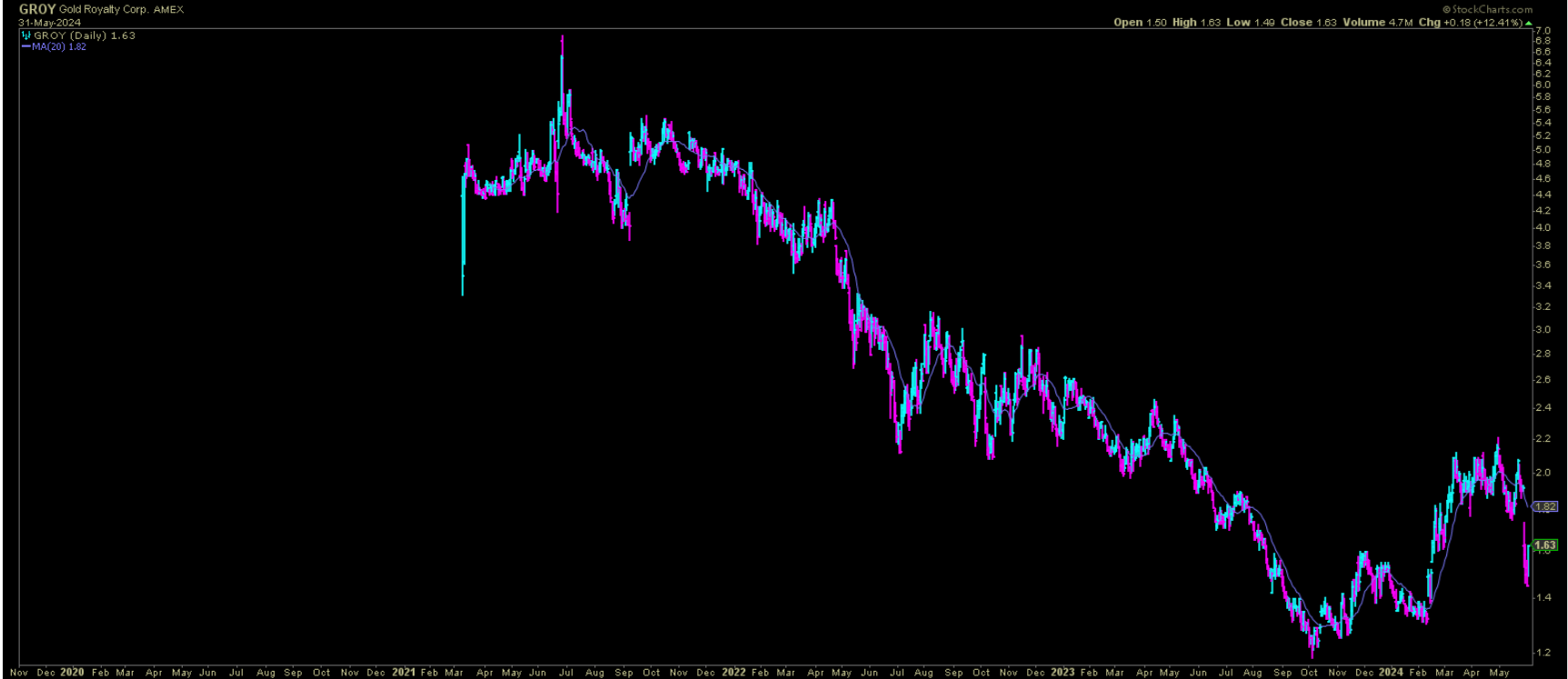

Another example is Gold Royalty’s (GROY) acquisition of a copper stream on the Vares Mine (a high-grade polymetallic project) which resulted in significant dilution, overshadowing what was otherwise a decent deal (~20 million shares issued at US$1.72, with full warrants for 3 years at US$2.25, or issuing up to 40 million shares). However, at least with Gold Royalty, the stock was heavily overvalued for its first year of trading, so its acquisition spree made sense if it could go out and use expensive currency to bulk up and broaden its portfolio.

GROY Chart Since IPO Debut – StockCharts

So, what’s a fair value for Metalla?

Using what I believe to be fair multiples of 0.90x P/NAV and 16.0x FY2025 cash flow estimates and a 75/25 weighting to P/NAV vs. P/CF, I see a fair value for Metalla of US$4.15. This points to a ~28% upside from current levels, but I am looking for a minimum 30% discount to fair value to justify entering new positions in junior royalty companies, and ideally closer to a 35% discount to fair value. And while it’s certainly possible that Metalla could continue higher from here with one of the better royalty portfolios among its peer group, I don’t see enough of a margin of safety just yet. Hence, I would need a deeper pullback in Metalla minimum to become more interested in the stock, and I continue to focus on other junior royalty companies like one I recently added to my portfolio and discussed here that trades at much lower multiples with what I believe to be significantly more upside to fair value.

Summary

Metalla has seen several positive developments in its legacy portfolio over the past year, with Gosselin continuing to grow, Copper World finally looking like it might be closer to full approval, and a restart at the polymetallic Endeavor Mine looking more likely. That said, the stock just came off a year of nearly 90% share dilution which has put a dent in its valuation and with lower near-term cash flow generation than peers and seemingly no hesitation to issue shares at depressed levels to continue tacking on growth, I remain more neutral on the stock here relative to peers which look like superior bets. That said, if we were to see a deeper pullback in the stock or a new low-risk technical setup, I might consider starting a new position in MTA, but I see far better value elsewhere for now.

Source link