Manchester United: Get Ready For A Period Of Uncertainty (NYSE:MANU)

Tom McAtee

Manchester United plc (MANU) is an English Football club subject to much speculation, given its recent transfer of ownership. Moreover, the club’s domestic and cup leagues have concluded for the 2023/24 season, meaning a potential inflection point has emerged.

We last covered Manchester United’s stock in June 2023, when we downgraded it to a Hold rating. At the time, we argued that Manchester United’s takeover prospects were uncertain, and its stock was overvalued.

Our Previous MANU Rating (Seeking Alpha)

Manchester United’s stock has slumped by more than 30% since our latest coverage. We revised the asset in recent weeks and decided to maintain our hold rating.

Despite maintaining our hold rating, we have identified alternative risk factors and value drivers since our latest coverage that we want to communicate.

Herewith are our latest findings on Manchester United’s stock.

What We Like

A New Corporate Strategy

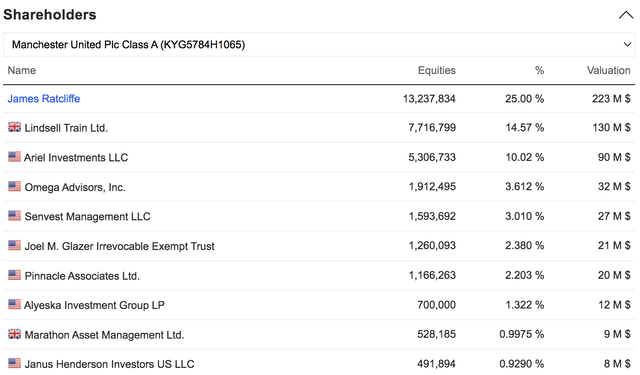

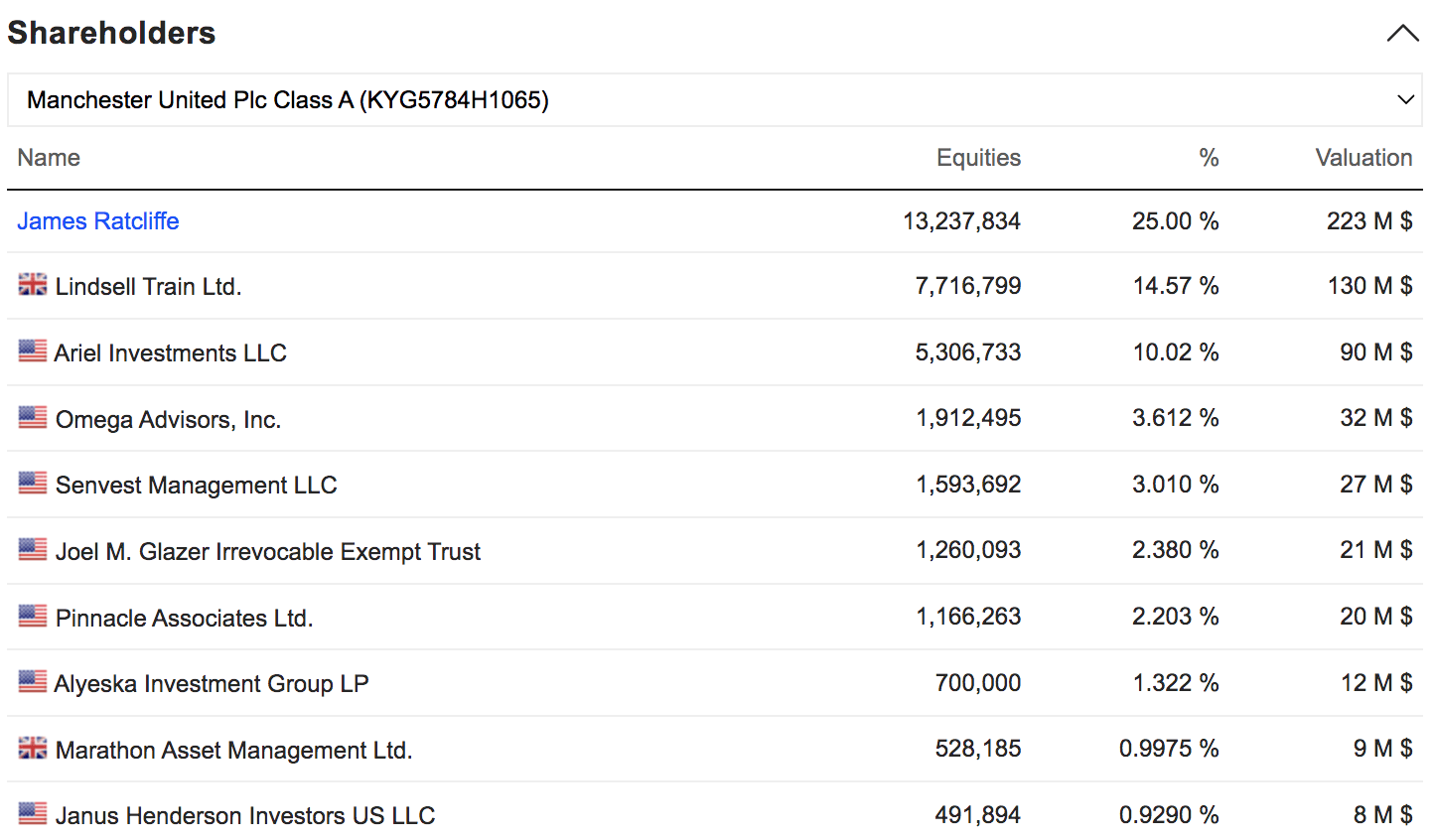

Sir Jim Ratcliffe recently acquired a significant chunk of Manchester United, making him the club’s largest shareholder. Although Ratcliffe remains a minority shareholder, he has considerable voting authority, as shown by recent changes at the club; a discussion follows the diagram below.

MANU Largest Shareholders (Market Screener)

Manchester United has made significant alterations to its C-Suite since Ratcliffe’s involvement. Firstly, it announced an array of interim CEOs. However, Omar Berrada is set to take over on a permanent basis from July 13th. Additionally, Roger Bell is set to step in as CFO at the start of the new season.

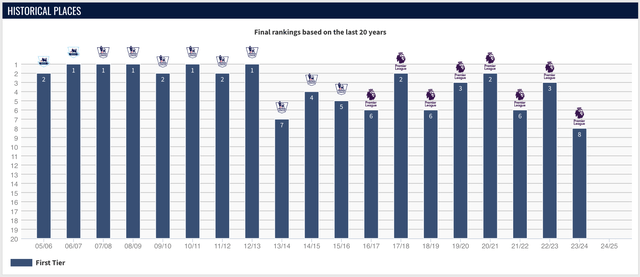

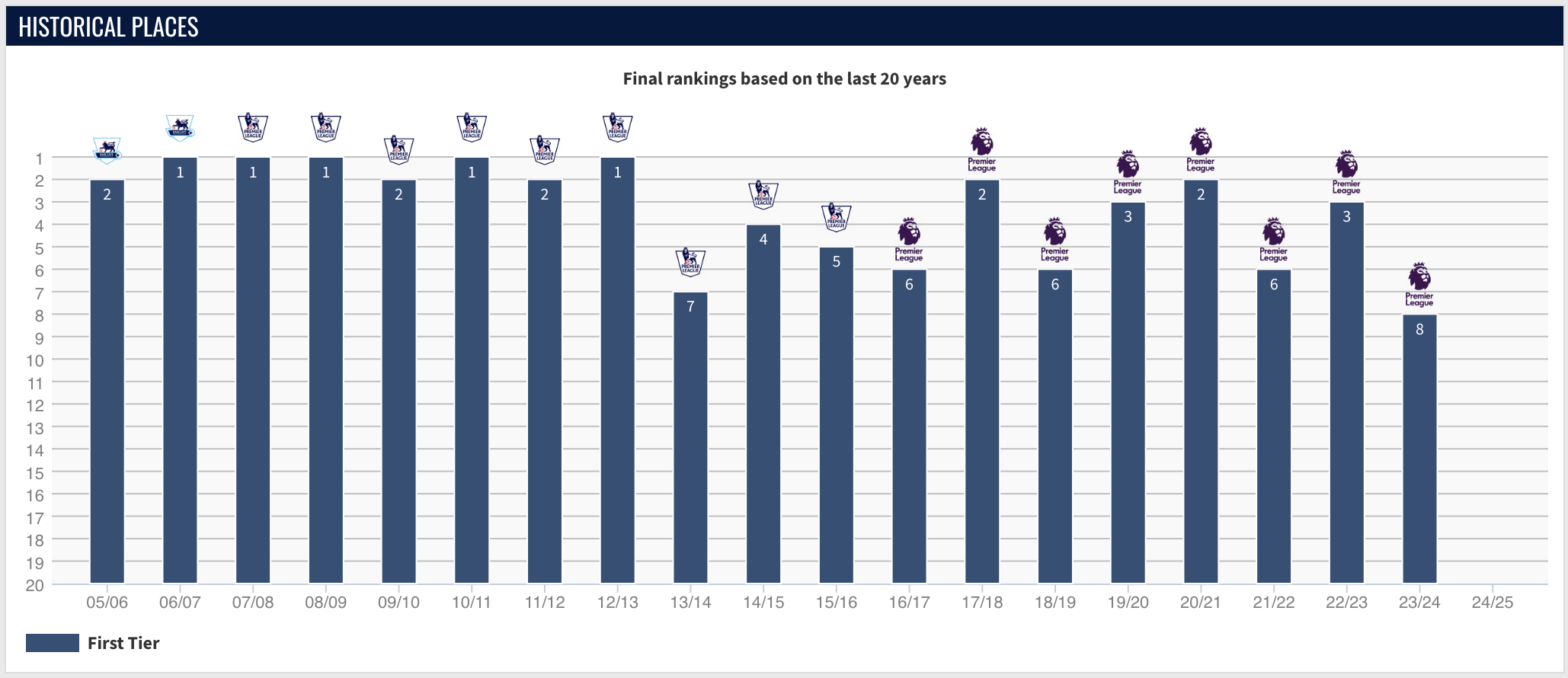

The important thing here is that Manchester United is shaping a formal C-Suite. The former majority owners, “the Glazers,” entrusted their then vice-chairman Ed Woodward, an ex-JPMorgan (JPM) investment banker, to run the club’s commercial expansion. However, Woodward’s tenure was unsuccessful after numerous high-profile player and managerial signings failed to sparkle.

Woodward departed a few seasons before Ratcliffe’s minority control bid. Therefore, it is unfair to say that he was solely at fault for the club’s recent inconsistency. However, the years following his exit didn’t introduce substantial changes in approach, leading to a period of additional uncertainty.

MANU League Position By Year (Transfermrkt.co.za)

Interestingly, Joel Glazer remains chairman at Manchester United, sharing much of the oversight responsibilities with Sir Jim Ratcliffe and numerous technical directors. However, we believe a renewed corporate strategy will formalize in the coming years, allowing Manchester United to head into a new director after a topsy-turvy decade of football.

Recent Earnings & Outlook

The big elephant in the room is Manchester United’s European Champions League exit, which could influence its 2024/25 earnings. However, I wanted to run through a few positives before delving into the Champions League debacle.

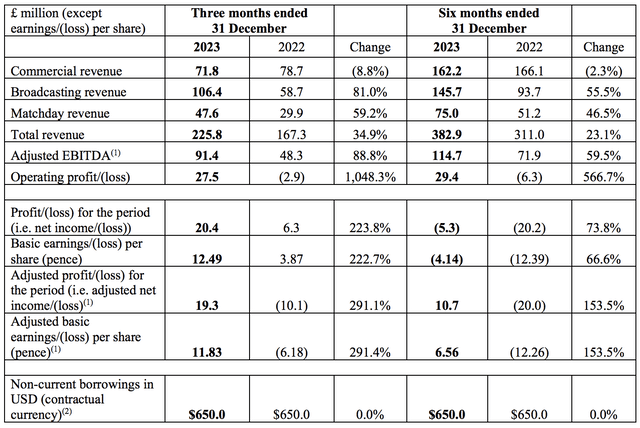

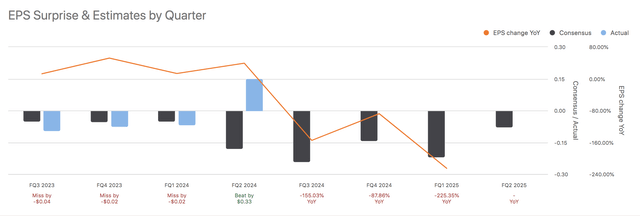

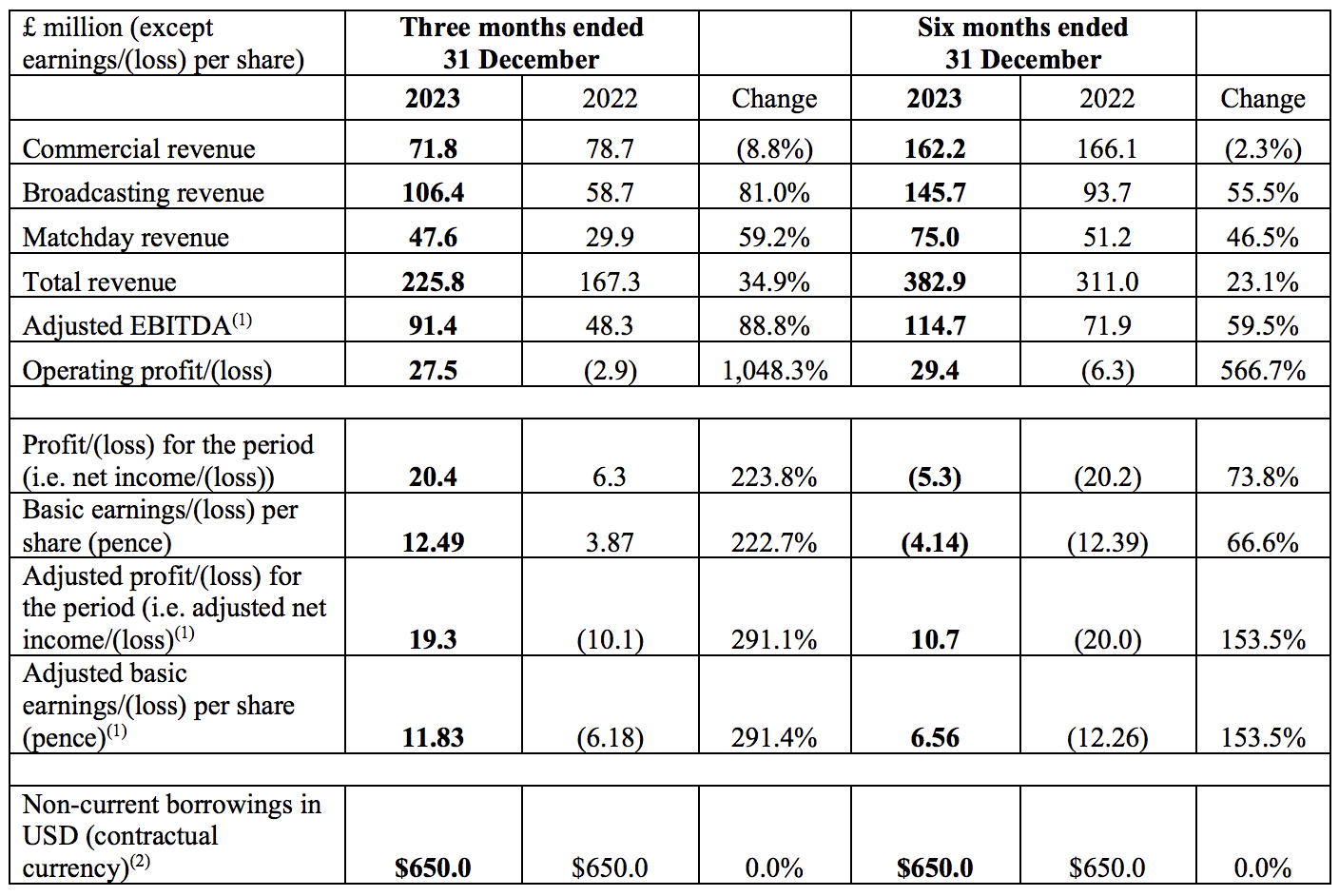

Manchester United released its second-quarter earnings in March and is set to deliver its third-quarter report on June 21st. The following diagram communicates key information about United’s second-quarter results; a discussion follows.

Q2 Earnings (Manchester United)

Retrospective

Manchester United showed staggering revenue growth in its second quarter, surpassing analysts’ revenue estimates by $69.38 million (FX-adjusted). Moreover, the firm’s FX-adjusted earnings-per-share settled 33 cents above target, showing that the street underestimated Manchester United’s bottom-line potential for the quarter.

The company’s broadcasting revenue surged by 81% as the club represented itself in the European Champions League. Moreover, by the end of its second quarter, Manchester United had already made a strong showing in its domestic cup competitions, allowing it access to additional broadcasting revenue.

Furthermore, Manchester United’s second-quarter match day revenue increased by 59.7% year-over-year, mainly due to its return to Champions League football and more home games. Remember that Manchester United is a growing brand, and, therefore, seeing its match day revenue increase year-over-year shouldn’t be surprising.

Manchester United’s commercial revenue declined by 8.8% year-over-year. The company claims the drop was due to a £28 million (approximately $35.58 million) drop in quarter-over-quarter sponsorship revenue. The club received a sponsorship credit in its previous quarter, which didn’t reoccur in Q2. As such, we think the drop is a non-core event and likely immaterial in the long term. If lower sponsorship demand were the reason for the decline in earnings, we would’ve concluded differently.

Lastly, a noteworthy mention is Manchester United’s cost base.

Although Manchester United hosted more matches and traveled for more games, its operating costs failed to dent its Q2 revenue surge. In fact, the club’s operating income surged by about 10.05x to £27.5 million (approximately $34.94 million).

Most of the increased operating expenses were linked to a £77.3 million (approximately $90.2 million) year-over-year increase in employee benefits due to participation in the Champions League. Additionally, the club’s amortization increased by £5.5 million (approximately $6.98 million) due to a higher player investment base, which we don’t deem problematic.

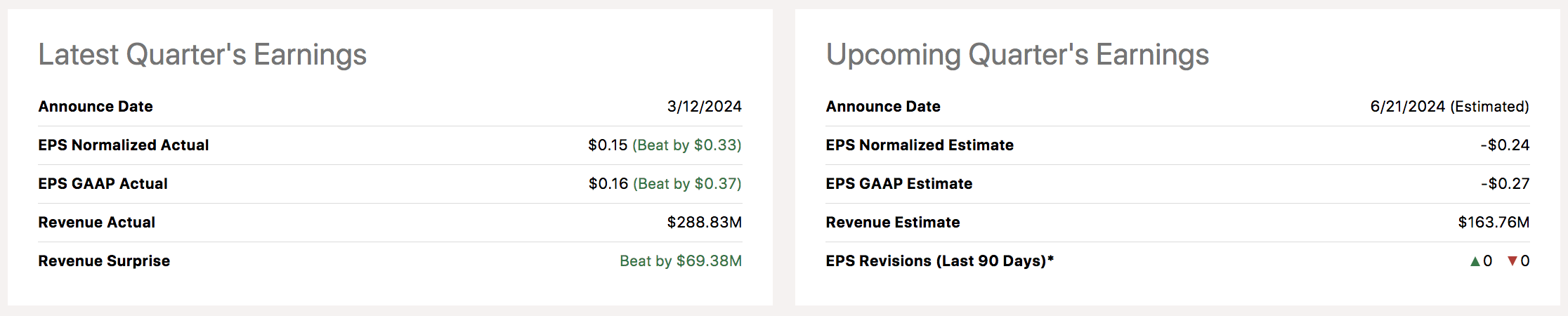

What Could Happen on June 21st?

As shown below, analysts anticipate Manchester United’s third-quarter revenue to reach $163.76 million and its earnings-per-share to settle at -$0.27.

MANU Earnings Estimate (Seeking Alpha)

The first factor to note regarding Manchester United’s third quarter is that the company recently entered the off-season. Therefore, seasonality will likely dent part of its fiscal period.

Furthermore, Manchester United crashed out of the Champions League group stages; thus, it likely didn’t realize the same broadcasting benefits as in Q2. Although the club participated in the Europa League thereafter, we believe traction would’ve been lower.

On the plus side, Manchester United secured the FA Cup trophy since reporting its Q2 earnings. The semi-finals and finals were played at neutral grounds, meaning Manchester United’s match day revenue probably wouldn’t have benefitted. However, the FA Cup victory likely contributed to broadcasting revenue.

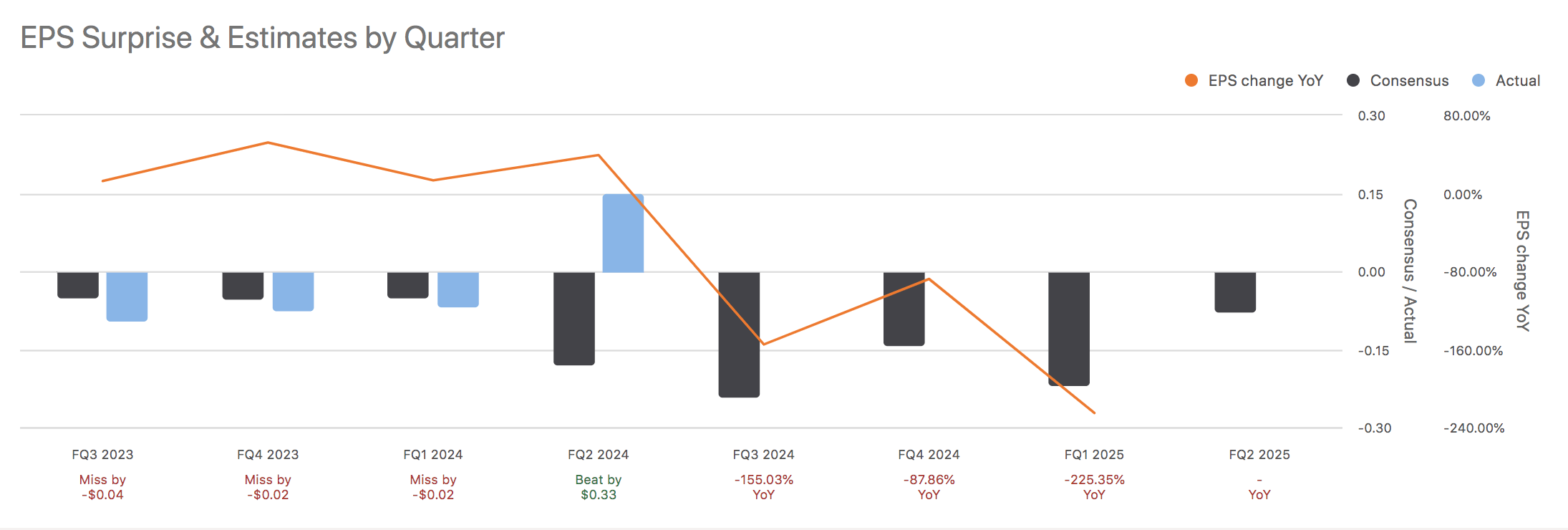

That’s as much as we can say for Manchester United’s earnings outlook. However, to end the section, I embedded a chart of the club’s recent quarterly earnings hits and misses. Believe it or not, the club’s lack of earnings momentum can stun its stock’s performance; therefore, we flag this as a risk going into June 21st’s results.

Seeking Alpha

What We Don’t Like

No European Champions League Football

Manchester United qualified for the Europa League via its FA Cup win. However, the Europa League is considered the B-League Vs. the Champions League.

Considering the aforementioned financial statements, the failure to participate in the Champions League will likely rebase Manchester United’s revenue back to where it was in 2022. Moreover, it might prevent Manchester United from signing big-name players this summer to avoid financial fair market implications. Thus, we see this as quite the conundrum for the club, especially as its new ownership structure will likely want to change course but might have their hands tied.

In essence, we expect lower revenue across all segments this year, purely due to Manchester United’s Champions League exit. Although we might be wrong in our outlook, we think the evidence from previous years’ financial results backs this up.

Transfer Market Activity

As conveyed in some of our previous Seeking Alpha articles, we have been very negative about Manchester United’s transfer activity in recent years.

We last stated that Harry Kane would be a good target, as we think the team is light up top. Moreover, Kane could’ve attracted additional commercial, broadcasting, and match-day revenue due to his stature in the game. However, the transfer didn’t happen last summer, and Manchester United instead opted for Mason Mount, Højlund, and Onana.

transfermarkt.co.za

We don’t think Mount was a great spend as he is a carbon copy of Bruno Fernandes, the current club captain. Although we think that Onana (goalkeeper) was a good capture, we also dislike the Hojlund signing. Sure, Hojlund, who plays striker, has potential, but he is merely 21 years old, which is extremely young for someone leading the line at a big club like Manchester United. Again, as mentioned before, we believe Harry Kane would’ve been a better fit as Manchester United needs instant success to get itself back on track.

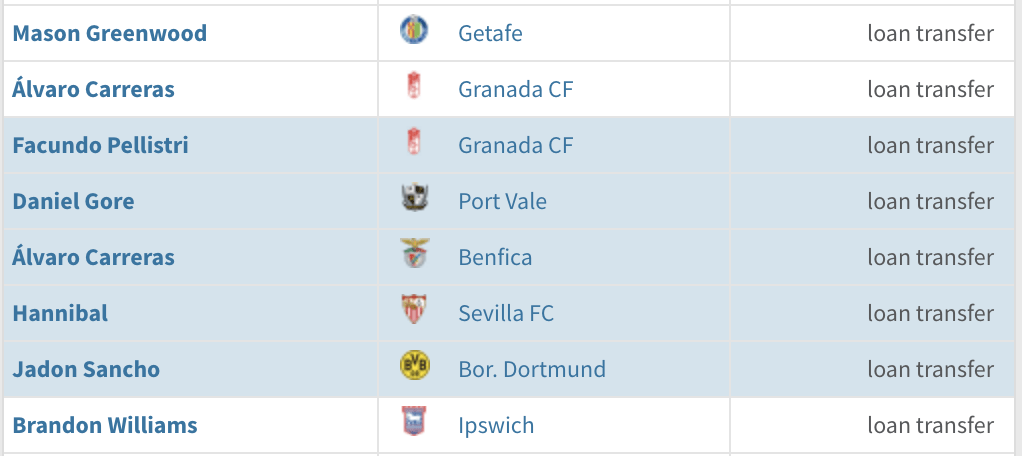

Fast track to today, and there has been little going on in the transfer market for Manchester United. The club will see various loanees returning to base. Additionally, rumors have emerged of Manchester United’s interest in young defensive players such as Marc Guéhi and Jarrad Branthwaite. However, we think Manchester United needs to sign impact signings to get itself back on course, instead of relying on loan returnees and young defensive signings.

MAN UTD Loan List For 23/24 (transfermarkt.co.za)

Valuation

Relative

Manchester United has a unique business model for a publicly traded company, making peer comparison difficult. However, instead of relying on peer-based comparisons, a time-series relative analysis can be relied upon by comparing the same stock’s past valuation multiples with its current.

Herewith are a few of Manchester United’s key price multiples; a discussion follows.

| Metric | Value | 5Y AVG |

| Forward EV/EBITDA | 21.44x | 20.73x |

| Forward P/CF | 22.07x | 31.27x (trailing) |

| Forward P/S | 3.28x | 3.73x |

Source: Seeking Alpha

As shown above, Manchester United’s salient price multiples are in line with its five-year averages. The multiples are all on a forward basis and, therefore, probably factor in the club’s lower expected earnings (from its Champions League exit). Nevertheless, we still feel they underappreciated the ferocity of a Champions League exit, given the contingent financial fair play effects.

Manchester United’s price multiples are difficult to place. However, we think the probability of its stock being relatively undervalued is slim.

Technical

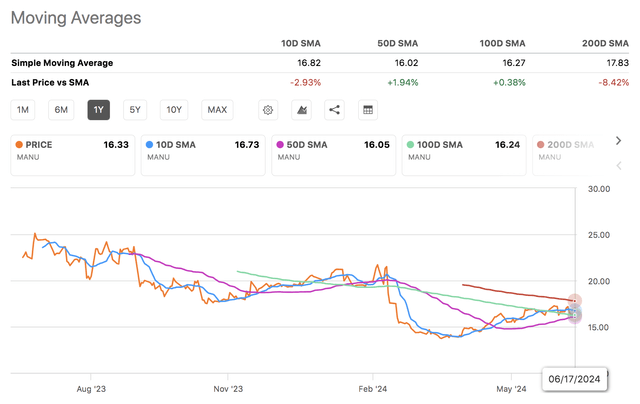

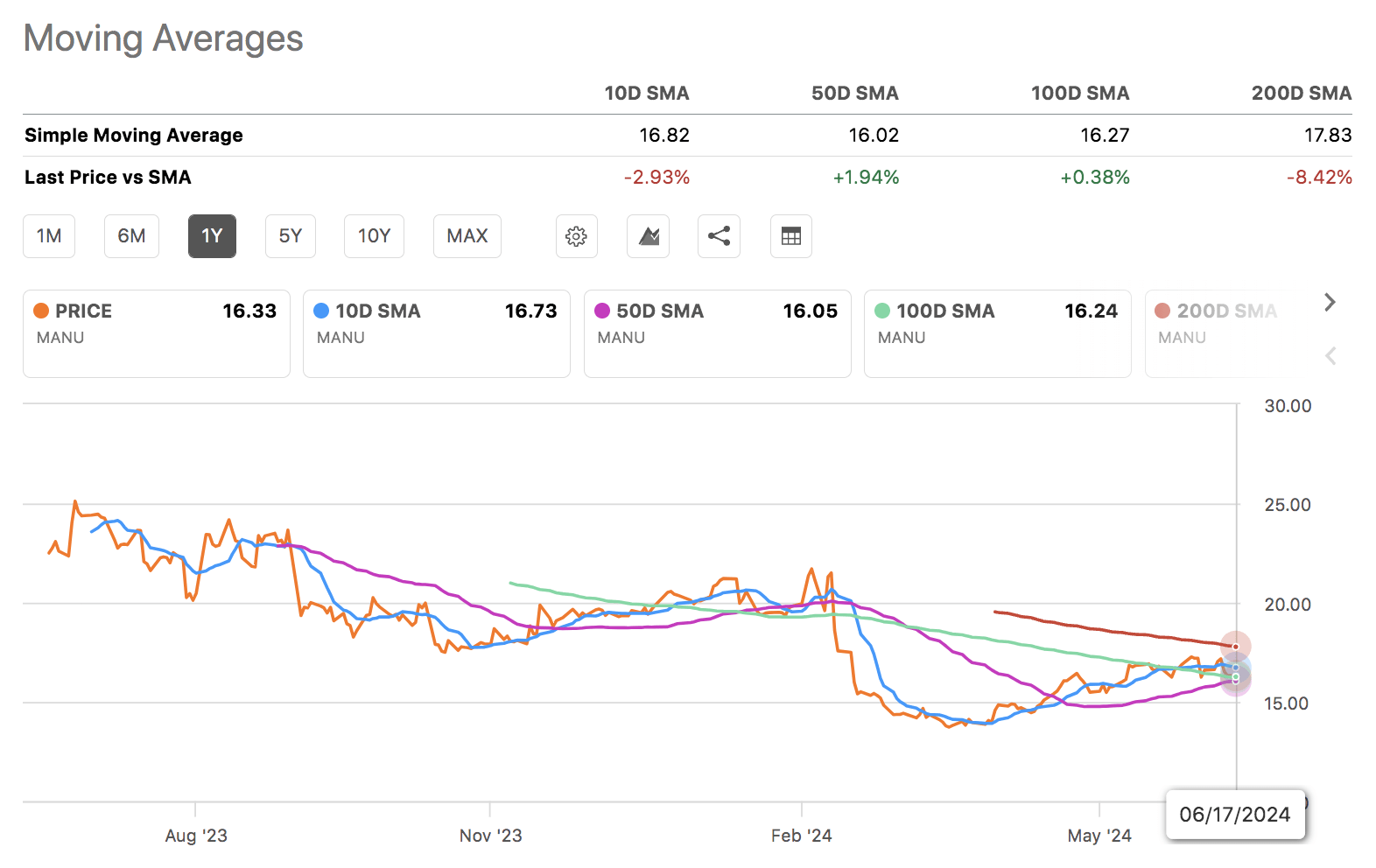

A look at Manchester United’s stock’s technical features shows that it is trading above its 50- and 100-day moving averages but below its 10- and 200-day moving averages. Moreover, the stock’s RSI of 47.3x is near its midpoint, suggesting little conviction exists from either buyers or sellers.

Moving Averages (Seeking Alpha)

Both metrics used in this section can be countercyclical. However, a fundamental push has to emerge for that to occur. Similar to our fundamental valuation assessment, Manchester United’s technical features illustrate little sign that the stock might be undervalued. However, we also don’t have a reasonable enough basis to deem the stock overvalued.

Final Word

Manchester United’s salient variables suggest its stock remains a Hold.

Although its Champions League exit might result in receding financial performance, Manchester United’s stock has lost more than 15% of its value in the past six months, suggesting that investors have already priced in much of its Champions League exit story.

However, on the other end of the spectrum, we cannot justify a buying opportunity as we disagree with Manchester United’s transfer market activity and fear potential Champions League-related financial fair play restrictions. Moreover, given our take on its relative price multiples and technical indicators, we believe Manchester United’s stock is in fair value territory.

We hereby maintain our Hold rating on Manchester United’s stock.

Source link

![[Weekly Roundup] The Secret to Beating Buffett - shareandstocks.com](https://dcgreferral.com/wp-content/uploads/2024/09/1727135485_Weekly-Roundup-The-Secret-to-Beating-Buffett-shareandstockscom-768x432.jpeg)