DiamondRock Hospitality: Preferred Dividend Coverage Appears Stable (DRH)

jewhyte/iStock via Getty Images

Introduction

I like preferred shares as a subdivision of my income portfolio, and my main focus is obviously on the issuer’s ability to pay the preferred dividends while the balance sheet strength also plays an important role. The REIT’s management team also calls value creation its ‘magnetic north’, and that definitely is an attitude I like to see.

I have been keeping an eye on DiamondRock Hospitality’s (NYSE:DRH) preferred shares and I used to have a long position which I sold when the preferred shares were trading above par. The preferred shares are still trading above par, so in this article I will have a closer look to check if it would make sense to re-establish a long position.

The performance of the hotel REIT remains solid

In the REIT sector, the net profit is less important than the FFO and AFFO result of a REIT. Also keep in mind the seasonality plays an important role in some hotel REITs and that is definitely the case at DiamondRock where the Q1 AFFO was less than 20% of the anticipated full-year AFFO (I will discuss the full-year guidance later in this article).

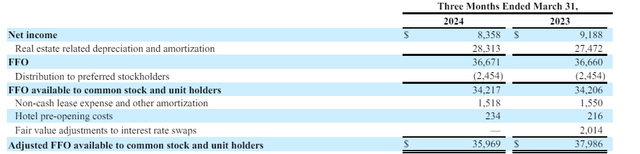

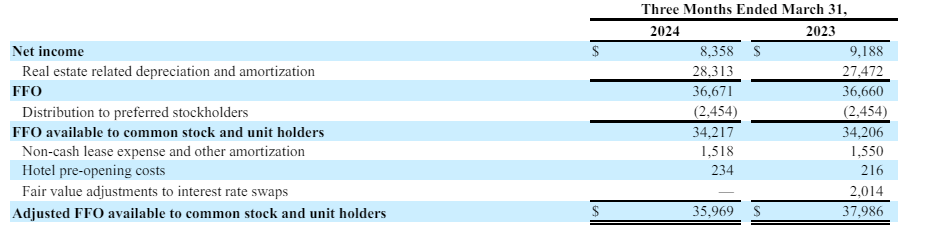

Looking at the Q1 results, the starting point of the FFO and AFFO calculation is the $8.4M net profit. As you can see below, the depreciation and amortization expenses are added back to the equation while the preferred dividend payments are deducted. This results in an FFO of $34.2.M.

DRH Investor Relations

After adding back some non-recurring items like the pre-opening costs related to some of the hotels and other non-cash expenses, the AFFO was almost $36M. Keep in mind this includes the $2.5M in preferred dividend payments which means the REIT needed just over 6% of its pre-preferred dividend AFFO to cover the dividends.

Also keep in mind DiamondRock Hospitality spent almost $19M on capital expenditures which means the post-capex and pre-preferred dividend AFFO was approximately $19.5M. That means the payout ratio was a little bit over 10%.

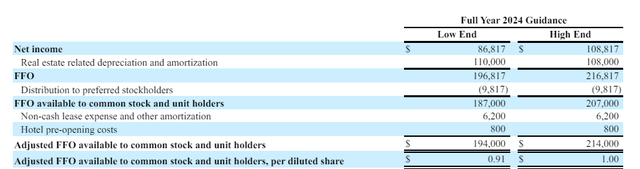

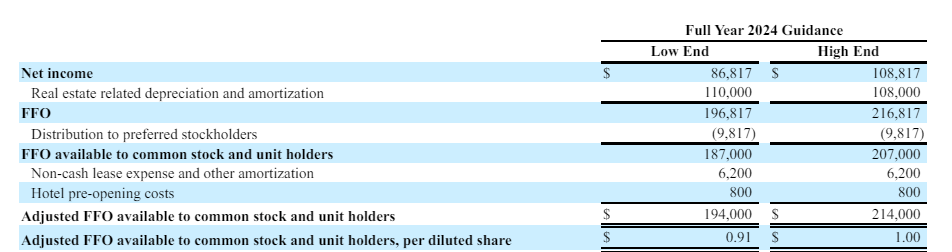

Keep in mind the first quarter is traditionally weak, and the REIT’s full-year guidance reflects that. As shown below, the full-year AFFO will come in between $194M and $214M and the midpoint of that equation is $204M. Adding back the preferred dividend payments results in $214M, of which $100M will be spent on capex. This means the full-year AFFO post capex will be approximately $114M before taking the preferred dividend payments into consideration.

DRH Investor Relations

As the preferred dividend payments will remain unchanged at just under $10M, the payout ratio will be just under 9%. So from a preferred dividend coverage perspective, I am certainly satisfied the REIT will continue to honor its payment commitments.

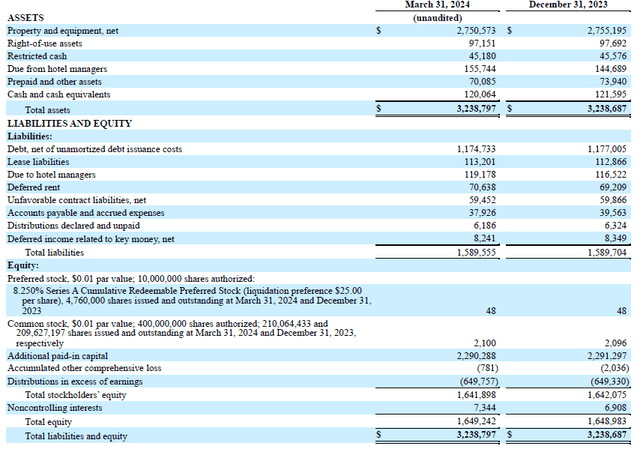

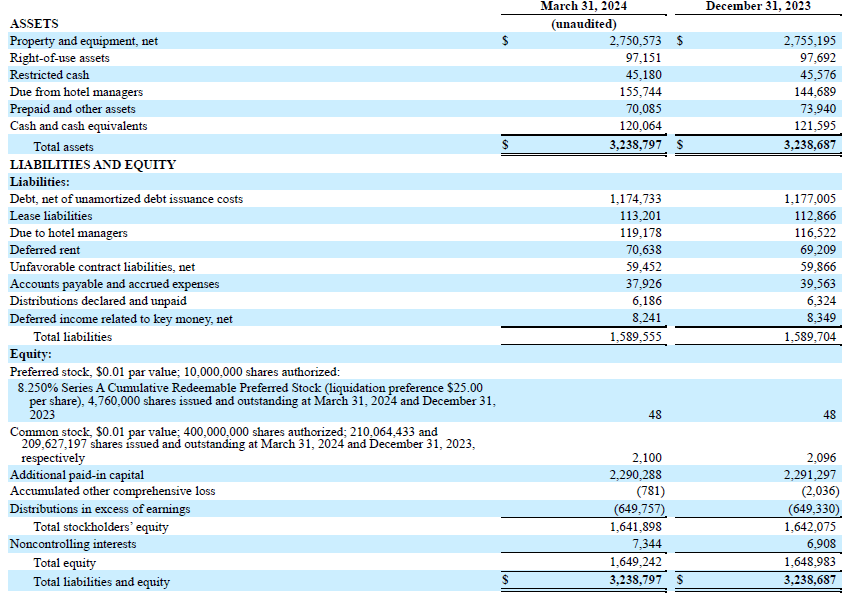

And as the REIT remains profitable (despite the depreciation expenses), the balance sheet also remains quite robust. As you can see below, the balance sheet contains $3.24B in assets with just $1.17B in gross debt. After deducting the $120M in cash, the net debt is just $1.05B.

DRH Investor Relations

Compared to the $2.75B asset value, this represents an LTV ratio of just 38%. There’s $1.64B in equity on the balance sheet and as the preferred stock represents just $119M of that amount, the common equity, which ranks junior to the preferred equity, stands at $1.52B. In other words, the first $1.52B in losses will be absorbed by the common equity.

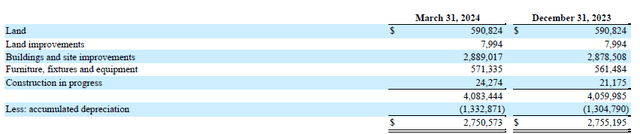

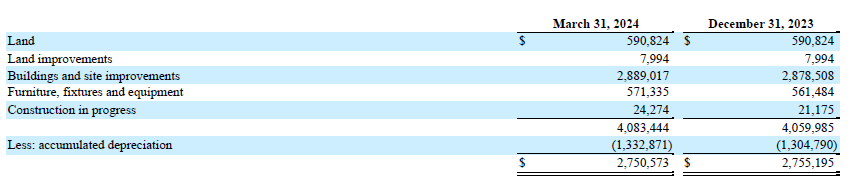

But there’s more. The $2.75B asset value already includes $1.33B in accumulated depreciation. The total acquisition cost was $4.08B and even if you would exclude the $571M in furniture and equipment, the acquisition cost of the land and buildings was still $3.5B. I think the fair value of the assets will be closer to the acquisition cost than to the book value.

DRH Investor Relations

Not only does this potentially add an additional layer of safety, it would also indicate the pro forma LTV ratio is just around 30% if you’d use the gross book value (minus furniture and equipment) instead of the net book value.

The preferred stock is still attractive

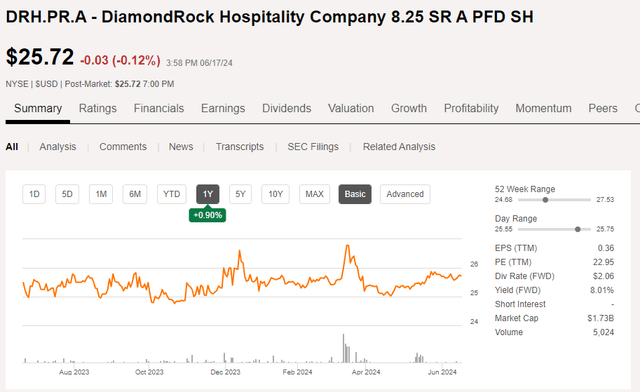

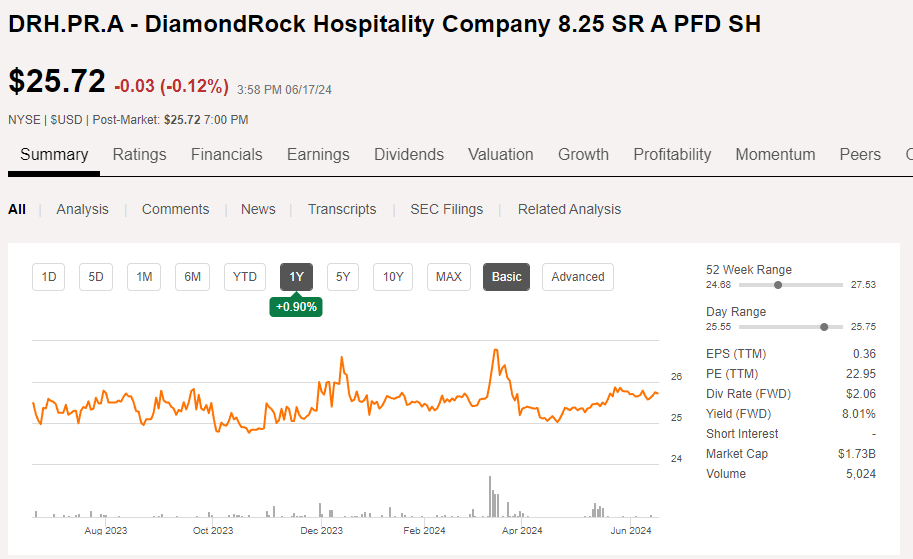

DiamondRock REIT has only one issue of preferred shares outstanding. The series A preferred shares (NYSE:DRH.PR.A) are a cumulative issue, offering an annual preferred dividend of $2.0625 per preferred share paid in four quarterly installments. The securities can be called from Aug. 31, 2025 on. I am expecting the interest rates on the financial markets to decrease between now and the summer of 2025, so seeing the securities being called appears to be pretty likely given the relatively high preferred dividend rate and the relatively small issue size.

Seeking Alpha

On Monday, the preferred shares closed at $25.72 which means that if the securities get called, investors will generate a 3% capital loss. That being said, one would still receive five quarterly preferred dividends so the total return would be approximately $27.58 for a total return of 7.2%, which is roughly 6.2% annualized.

That’s still not bad, but it also depends on the tax treatment of capital losses and preferred dividends. So while an investment in DiamondRock could still make sense for some investors, it may not be the best idea for other (foreign) investors with a different tax implication.

As the securities are trading above par, it goes without saying that the longer the securities remain outstanding beyond August 2025, the higher the return will be.

Investment thesis

I currently have no position in DiamondRock Hospitality, but as I think it is increasingly likely the securities will get called in 2025, I should perhaps look at the preferred shares as a 14 month ‘term deposit’ (it of course still is an investment in an equity security and not a deposit. And while I am trying to add some duration to my portfolio, the annualized 6.2% yield for a 14 month investment isn’t too shabby either.

While the common shares of DiamondRock Hospitality are relatively attractively priced based on the gross book value of the assets (the acquisition cost of land + buildings + the value of assets under construction) represents approximately $10.85/share. The stock is trading at just 9 times the AFFO, but keep in mind 2024 will be another capex-heavy year as the refurbishment of some hotels is still ongoing.

Source link