Carvana Stock: Navigating Long-Term Sustainability After PIK Deferral Ends (NYSE:CVNA)

Lu Zhang/iStock Editorial via Getty Images

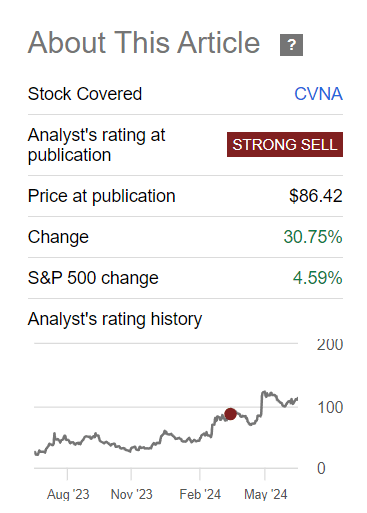

Last March, I initiated my coverage on Carvana Co. (NYSE:CVNA), rating it as a strong sell due to weakness in the auto loan market, fueled by high delinquency rates and its unsustainable earnings, in my opinion. Although the stock has climbed by nearly 31% since then, I remain bearish on Carvana due to the headwinds facing used car prices, which could see used car prices fall by as much as 24%.

Seeking Alpha

In addition, I still believe the company’s financial performance is unsustainable, due to the company sharing that it plans to commence cash interest payments on its restructured debt in 2025. With the last PIK interest payment on the 2028 and 2030 notes scheduled for next August, I expect the market to re-rate Carvana, as its mountain of debt will once again become the forefront of the stock’s investment thesis, due to the high interest payments that the company will have to pay in cash.

In fact, I expect the cash interest scheduled for 2025 will act as a major headwind to Carvana’s free cash flow generation, since the PIK interest payments were the main reason for the free cash flow it generated in Q1. In light of this, I’m reiterating my strong sell rating on Carvana, with a price target of $18.2, implying 84% downside from current levels.

Industry Headwinds

The mid-June Manheim Used Vehicle Value Index fell 8.5% from June 2023 and 0.3% from May 2024 to 196.8. The seasonal adjustment reduced the impact for the first half of June, as the non adjusted price change declined 1.6% from May and 9.5% YoY. Cox Automotive’s Senior Director of Economics and Insights, Jeremy Robb, commented on these results, saying “May ended with stronger than normal price declines in the last few weeks, and that’s continued into early June.” As a result, the average used car listing price was $25,670 in early June, down 6% YoY.

The force driving this continuous decline in used car prices is new car prices. New car prices surged 20% from 2021 to 2023 after stagnating from the mid-90s until the pandemic. This sudden spike, post the pandemic, was fueled by automakers suspending production, supply chain constraints, and a shortage in semiconductors.

But at the moment, the supply chain has tightened and semiconductors are no longer at shortage levels, leading to an improvement in auto production. Meanwhile, economic conditions have dampened consumer demand for vehicles. Therefore, new car inventory has been building up.

According to Cox Automotive, the US supply of available unsold new vehicles was at 2.89 million units at the beginning of June, 55% higher than a year ago, despite dealers reducing the previous model year’s supply by 2%. However, this decline was offset by the arrival of 2025 models, which increased by more than 3%.

Numbers from Ford (F) highlight the significance of the inventory build up. The giant has 100 days’ supply of cars, leading CFO John Lawler to share his concern about that rising figure. Data from Cox Automotive shows that the average inventory level in the US is 74 days. The current high inventory levels of new cars come at a time when new car prices are stabilizing. According to Cox Automotive, the average listing price for a new vehicle at the start of June was $47,390, lower by $107 compared to the prior year.

However, during the Memorial Day holiday, one of the stronger selling periods in the calendar year, the report states that there were higher incentives and discounts at 6.7% of average transaction price, the highest level since May 2021. But with new model year vehicles starting to fill up dealer lots, Cox Automotive expects the incentives and discounts to remain and potentially increase to reduce inventory of older model year vehicles.

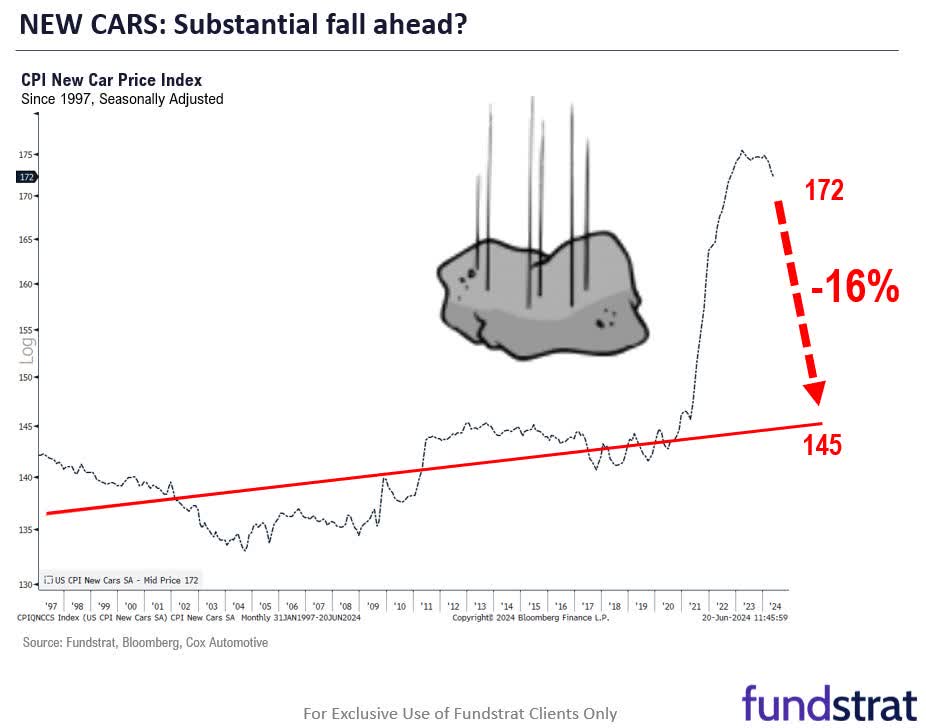

In my opinion, the high inventory levels, along with increasing discounts and incentives, give credence to data from Fundstrat, that see new car prices potentially declining by 16% if they fall back to their 50 year trend.

Fundstrat

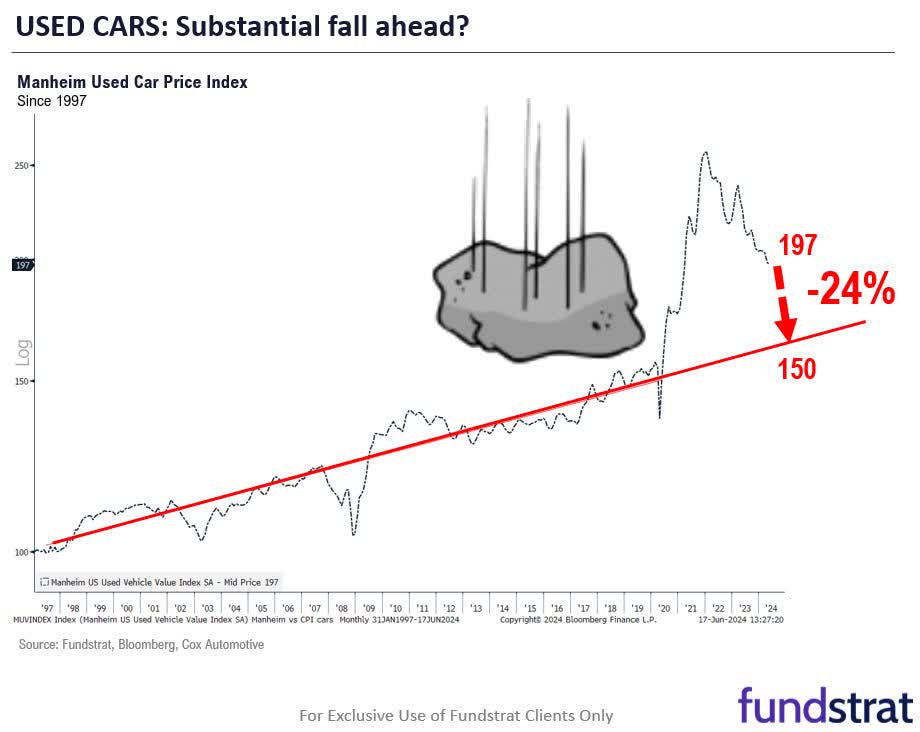

In the same vein, Fundstrat sees used car prices potentially falling 24% to fall back to their 50 year trend.

Fundstrat

Unsustainable Earnings

In my opinion, the pricing headwinds and forecasts of further price declines in new and used cars are concerning for Carvana’s future prospects, in light of its financial performance in Q1. During that period, Carvana reported record net income of $49 million, record adjusted EBITDA of $235 million, operating cash flow of $101 million, and free cash flow of $82 million.

OCF | $101,000,000 |

CapEx | $19,000,000 |

FCF | $82,000,000 |

At first glance, Carvana’s figures show that the company is on the right track to grow profitability and cash flow, which are crucial to deal with its $5 billion debt mountain. However, as is the case with its 2023 earnings, the figures aren’t as impressive after digging deeper.

In terms of net income, Carvana benefitted from an unrealized gain on Root (ROOT) warrants of $75 million, as mentioned in the 10-Q filing. Without this unrealized gain, the company would have reported a net loss of $26 million, showing that Carvana is still unable to operate profitably, even after slashing costs substantially.

Net Income | $49,000,000 |

Unrealized Gain on Root Warrants | $75,000,000 |

Adj. Net Loss | -$26,000,000 |

This issue could show in the coming earnings report as the Root warrants must have lost value as Root’s share price at the end of Q1 was $61.08, and at the moment, its share price is $45.03, 26.3% lower. In this way, Carvana’s unrealized gain on these warrants at the moment could be estimated to be around $55.3 million, if it didn’t exercise these warrants. As such, for Carvana to show that its business is profitable indeed, it should generate more than $55.3 million in net income in Q2.

In terms of record adjusted EBITDA, Carvana doesn’t recognize a real cost its operations incur, which is depreciation. The company has a vehicle inventory of $1.16 billion, and depreciation definitely impacts the value of this inventory when Carvana sells these vehicles. During that period, Carvana reported $82 million in depreciation, representing 7% of its total vehicle inventory.

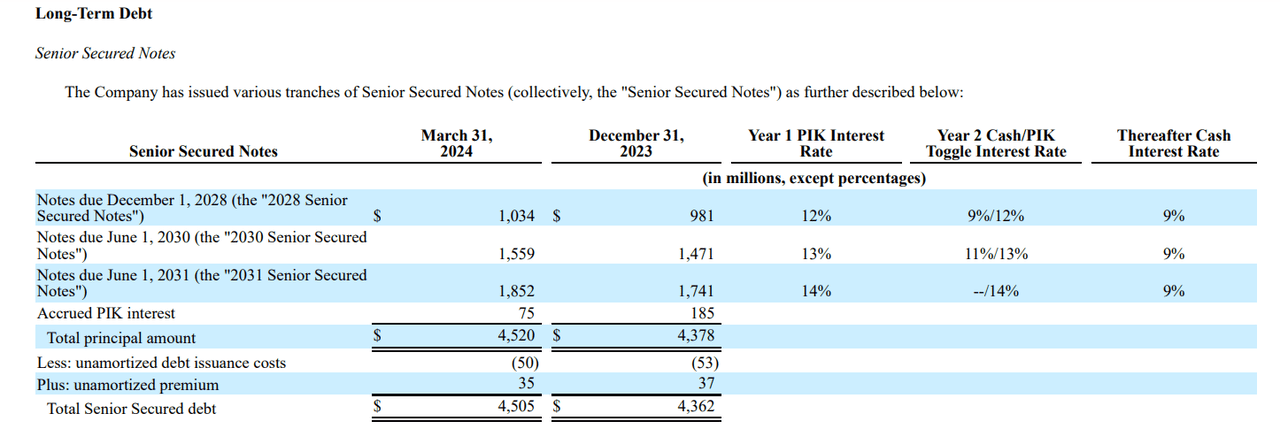

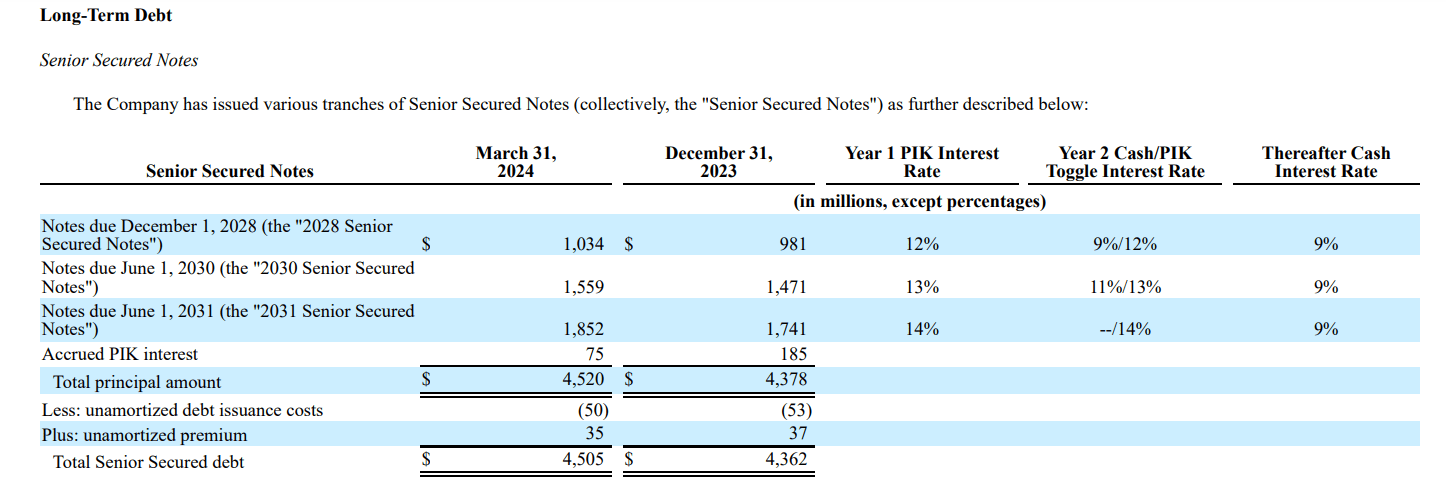

In addition, adjusted EBITDA doesn’t take into account interest expenses, which is crucial considering that Carvana’s debt load of more than $5.5 billion has a high interest rate as shown in the following 2 tables.

Secured Debt | Balance | PIK Interest | Cash Interest |

2028 Notes | $1,034,000,000 | 12% | 9% |

2030 Notes | $1,471,000,000 | 13% | 9% |

2031 Notes | $1,741,000,000 | 14% | 9% |

*Compiled from Carvana’s latest 10-Q filing.

Unsecured Debt | Balance | Cash Interest |

2025 Notes | $98,000,000 | 5.625% |

2027 Notes | $32,000,000 | 5.50% |

2028 Notes | $22,000,000 | 5.875% |

2029 Notes | $26,000,000 | 4.875% |

2030 Notes | $27,000,000 | 10.25% |

*Compiled from Carvana’s latest 10-Q filing.

With that in mind, Caravana reported $173 million in interest expenses, of which $142 million were paid-in-kind. As such, the reported operating cash inflow of $101 million benefitted from these PIK payments, and in turn, it was able to generate free cash flow of $82 million. As is, without this factor, Carvana would have reported operating cash outflow of $42 million and free cash outflow of $60 million.

OCF | -$41,000,000 |

CapEx | $19,000,000 |

FCF | -$60,000,000 |

Carvana’s dependence on the PIK payments to generate cash flow is concerning, with the company stating in the Q1 shareholder letter that it plans to pay cash interest semi-annually on the 2028 and 2030 secured notes in 2025. According to Carvana’s Q1 report, it pays interest on the secured notes semi-annually on February 15 and August 15. In Q1, the company paid interest in kind of $53 million on the 2028 notes, $88 million on the 2030 notes, and $111 million on the 2031 notes. Accordingly, the notes’ balance increased by the end of the quarter.

10-Q Filing

During Q2, Carvana raised $350 million from the sale of 3.05 million shares at an average price of $114.85 per share, and used $259 million of the proceeds to repurchase $250 million, or 24%, of the 2028 secured notes. Based on this, the balances of Carvana’s outstanding secured notes can be estimated as follows.

Secured Debt | Balance at End of Q1 | Redemptions | Current Balance |

2028 Notes | $1,034,000,000 | $250,000,000 | $784,000,000 |

2030 Notes | $1,471,000,000 | $0 | $1,471,000,000 |

2031 Notes | $1,741,000,000 | $0 | $1,741,000,000 |

Using these figures, it is easy to estimate the closing balances of these notes by the end of the year, as well as the cash interest that Carvana will incur next year. Since there’s 1 more PIK payment remaining this year of 12% on the 2028 notes, 13% on the 2030 notes, and 14% on the 2031 notes, I expect these notes’ balances at the end of 2024 to be $831 million, $1.56 billion, and $1.86 billion, respectively. Considering the cash interest rate of 9% for these notes, I expect Carvana to incur $215.8 million in cash interest on the secured notes alone in 2025.

Secured Debt | Current Balance | Remaining PIK | Balance at EoY | 2025 Cash Interest |

2028 Notes | $784,000,000 | $47,040,000 | $831,040,000 | $74,793,600 |

2030 Notes | $1,471,000,000 | $95,615,000 | $1,566,615,000 | $140,995,350 |

2031 Notes | $1,741,000,000 | $121,870,000 | $1,862,870,000 | $0 |

Carvana will also have to pay cash interest on its unsecured debt, which I forecast to be as follows.

Unsecured Debt | Balance | Interest | Interest Expense |

2025 Notes | $98,000,000 | 5.625% | $5,512,500 |

2027 Notes | $32,000,000 | 5.50% | $1,760,000 |

2028 Notes | $22,000,000 | 5.875% | $1,292,500 |

2029 Notes | $26,000,000 | 4.875% | $1,267,500 |

2030 Notes | $27,000,000 | 10.25% | $2,767,500 |

Accordingly, I’m forecasting Carvana’s interest expense on the unsecured debt in 2025 to be around $12.6 million. This means that the company’s total cash interest expense in 2025 could be around $228.4 million. This forecast doesn’t take into consideration the 14% PIK interest on the 2031 secured notes, which would bring the total balance of these notes to $2.1 billion by the end of 2025, per my estimates.

Moreover, Carvana has to deal with the $98 million unsecured notes that mature in 2025. As such, I see 3 scenarios for the company to deal with this debt maturity. The first scenario would be Carvana utilizing its existing liquidity to repay this debt. According to its latest 10-Q filing, Carvana has total liquidity resources of $3.2 billion, including $252 million in cash and equivalents, $1.4 billion available under short-term revolving facilities, and $1.2 billion in super senior debt capacity.

10-Q Filling

The downside of this scenario to Carvana, in my opinion, is that it might have to tap into its available debt resources in light of the potential cash flow generation headwinds that could occur, once it starts paying cash interest on the secured notes. This would see Carvana taking on debt to repay the maturing debt, which isn’t sustainable in my opinion.

The second scenario, and the most likely in my opinion, would be Carvana tapping into its ATM offering to raise the funds required to repay the debt. At the current share price of $112.99, raising this amount means the sale of around 867 thousand shares. In both scenarios, Carvana’s total cash payments towards servicing its debt in 2025 would be around $326.4 million.

Total 2025 Cash Interest | $228,388,950 |

2025 Maturity | $98,000,000 |

Debt Payments | $326,388,950 |

The third scenario would be Carvana refinancing this debt, which would come at the expense of a higher interest rate. This would further add pressure to Carvana’s ability to generate free cash flow, which is crucial to deal with its secured notes.

Valuation

Given the headwinds facing used car prices as well as Carvana’s lackluster financial performance, I believe the stock is extremely overvalued at current levels. At its current share price of $112.99, Carvana’s enterprise value is more than $29 billion, after considering the recent $250 million debt redemption and the $350 million capital raise.

Cash | $343,000,000 |

Debt | $6,178,000,000 |

Net Debt | $5,835,000,000 |

EV | $29,067,345,317 |

Assuming Carvana generates $1 billion in adjusted EBITDA this year, its annualized rate, as management shared in the Q1 shareholder letter, which in my opinion would be the absolute best case scenario, it would be trading at a forward EV/Adjusted EBITDA multiple of 29.07, compared to a sector median of 9.58. Meanwhile, other used car equities such as CarMax (KMX), AutoNation (AN), Sonic Automotive (SAH), and Group 1 Automotive (GPI) are trading at the following multiples.

Company | EV/EBITDA |

KMX | 29.90 |

AN | 8.56 |

SAH | 9.62 |

GPI | 8.87 |

Average | 14.24 |

Since CarMax’s high valuation skews the average upwards, I’m using the sector median to reach my price target, thanks to Carvana’s debt load, elevated cash interest payments starting next year, and the headwinds facing used car prices, the company’s core business. Accordingly, my price target for Carvana is $18.2 per share, representing 84% downside from its current valuation.

EV | $29,067,345,317 |

Adj. EBITDA | $1,000,000,000 |

EV/Adj. EBITDA | 29.07 |

Target Multiple | 9.58 |

Implied EV | $9,580,000,000 |

Net Debt | $5,835,000,000 |

Equity Value | $3,745,000,000 |

OS | 205,614,172 |

Price Target | $18.21 |

Share Price | $112.99 |

Downside | -84% |

Risks

As is the case with my prior coverage on Carvana, the main risk to my thesis is a short squeeze occurring. Currently, Carvana’s short interest rate is high at 23%, per Fintel data, and any positive news could send the stock on another run similar to the one it had following its Q1 earnings. Such a run could take place when Carvana posts its Q2 earnings, especially if it shows improving performance in terms of profitability and cash flow generation. Another catalyst that could trigger a short squeeze, would be Carvana buying back more debt, since it would help relieve its balance sheet.

Conclusion

With car prices, new and old, falling, Carvana’s business model is under pressure. New vehicle inventories are extremely high, and automakers and dealers are resorting to deep discounts and incentives to stimulate demand. In this way, used car prices could continue their downward trajectory, which could see them drop by as much as 24%. This pricing headwind is especially concerning for Carvana since it is on track to commence cash interest payments on its 2028 and 2030 secured notes in 2025, and has $98 million in debt maturing in 2025 that it has to deal with.

Given that the company’s cash flow generation has been mainly due to the PIK payments on its secured debt, these cash payments could result in Carvana generating negative cash flows, unless it drastically improves its operational efficiencies. That said, I don’t see Carvana further reducing its costs from their current levels. As such, I expect the market to rerate Carvana’s shares in the coming months, especially after the next PIK payment in August. For these reasons, I’m reiterating my strong sell rating for Carvana, with a price target of $18.2, implying 84% downside from current levels.

Source link