Helmerich & Payne: U.S. Shale’s Long Goodbye Drives KCA Deutag Merger (NYSE:HP)

Jose Luis Pelaez Inc/DigitalVision via Getty Images

Introduction

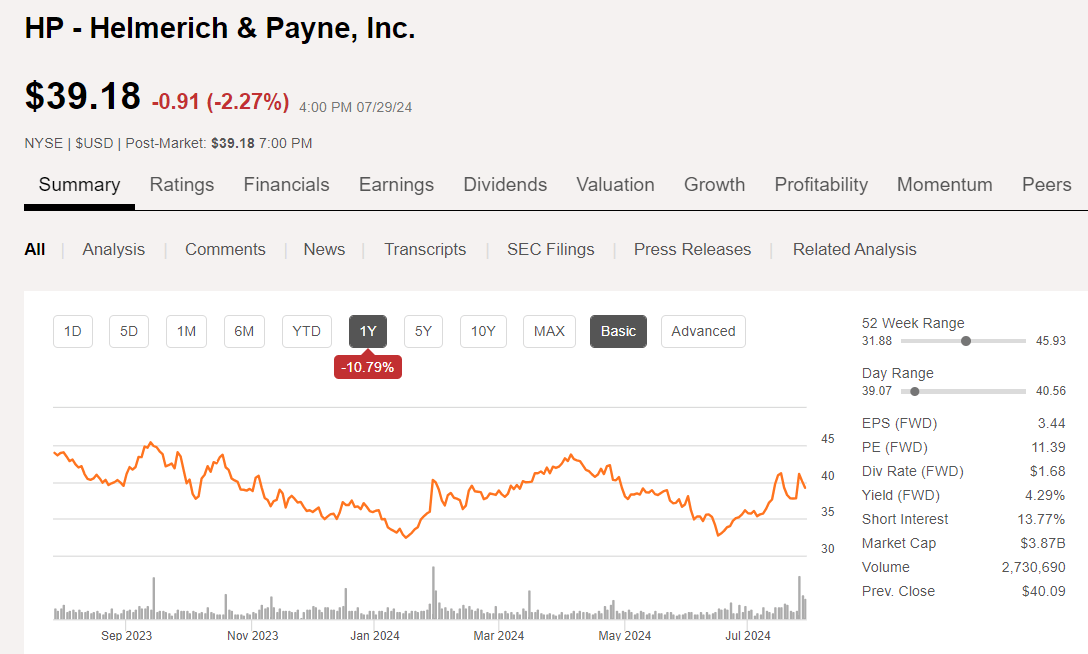

In our last article in January, we made a case for a second half rally in shares of Helmerich & Payne, Inc. (NYSE:HP). A rally that would be led by a resurgence in shale drilling to maintain output. That thesis hasn’t played out as longer laterals, increased completions intensity, and improved AI led understanding of subsurface rock properties, have enabled production to largely tread water. Shares of HP rallied strongly in Q-1 based on oil and gas prices, peaking in April in the low $40’s. Now as we head into the back half of the year, we see another rally beginning to fizzle as oil and gas prices turn spongy again, just as the company makes a major acquisition.

H&P price chart (Seeking Alpha)

Analyst expectations are modest at the present, with a hold rating and price targets ranging from $36-$50 and a median of $44. H&P beat EPS estimates for Q-3 by a wide margin, and forecasts for Q-4 are in the same range at $0.78 per share. Obviously, the merger isn’t reflected in this forecast. A similar beat for the coming quarter is a stretch on H&P results along, but if one comes, the stock could move higher.

In this article, we will review the recent quarter and hit the highlights of the merger with KCA-Deutag, and target an entry point for the stock for risk tolerant investors.

Fortunes of geology

You don’t have to read too many quarterly reports for service providers to figure out there is a geographic shift in the activity upon which they depend. The big service providers, Schlumberger, (SLB), Halliburton, (HAL), and Baker Hughes, (BKR), and most of the second tier providers agree on one thing. The Middle-East, African geomarkets will outperform North America for the foreseeable future.

The great shale basins of the U.S. have had a great run for the last 15 years. Often called a miracle, drillers have figured out how to efficiently drill and complete these wells. The state of play in shale is now a high art, as evidenced by the industry’s ability to contract drilling and completions activity by ~30%, and still maintain near-record production. Those days are coming to an end. Not that U.S. shale has finished its run-it has at least a couple of decades to go, but growth, in the absence of a massive increase in drilling, is in the rearview mirror.

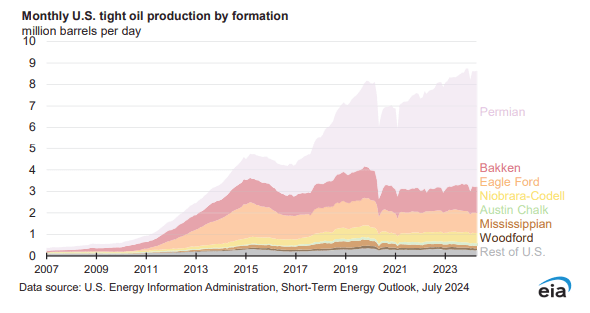

Monthly tight oil production (EIA STEO)

Note in the slide above, taken from the most recent EIA-STEO, that the only basin with any significant increase in production since 2019, is the Permian. And, that period came to an end in early 2023.

There are several reasons for this outcome, and we will list-in no particular order, but not dwell on them in this report. Capital Restraint, Tier I inventory exhaustion, M&A activity siphoning off drilling capex, and in the case of gas drilling, low prices that made it uneconomic to drill. There are half a dozen other reasons for the state of play in which we find ourselves, but the ones I’ve listed are probably in everyone’s top five.

I hesitate to use the term “seismic” in relation to oil production, but there is underway a seismic-caliber shift eastward geographically in oilfield activity. I’ll let H&P management set the scene for this view of oilfield growth. John Lindsay, CEO, comments on the transaction-

This is the right transaction at the right time for H&P. Shortly after the advent of the super-spec rig in the U.S. market and our U.S. customers becoming more capital disciplined in their businesses, we realized the market in the U.S. was evolving and that growth opportunities here would likely be more measured than they were in the past. As a result, we developed a more concerted strategy to expand internationally. In recent years, KCA has streamlined its portfolio of assets geographically, strengthened its financial position by significantly reducing debt, and enhanced its leadership in the Middle East by acquiring Saipem’s onshore operations. The U.S. and Middle East are the two most prominent oil and gas-producing regions in the world. We have often said, if you want to be big in the U.S., you have to be in the Permian. And if you want to be big globally, you have to be in the Middle East. This transaction gives H&P immediate scale in core Middle East markets in a way that would be challenging to replicate organically, making H&P one of the larger rig providers in the Middle East.

I’ll close by emphasizing there are decades of productive drilling remaining in North America, and business will improve from current levels. But the “Miracle” has run its course. You don’t have to look any harder than that for the rationale for H&P’s merger with KCA Deutag.

The thesis for H&P

Helmerich and Payne is a storied land and offshore platform drilling contractor from the earliest days of the oil business. The company does one thing-make holes in the ground, and does it well. They are known for fielding experienced, competent crews on top tier, high technology equipment. This reputation has made it the leader in U.S. drilling. KCA has a similar operating philosophy, and as John Lindsay noted in the call-

KCA Deutag shares our cultural values focused on safety and the well-being of employees, sustainability, and a customer-centric approach. These will remain priorities and will support a seamless integration.

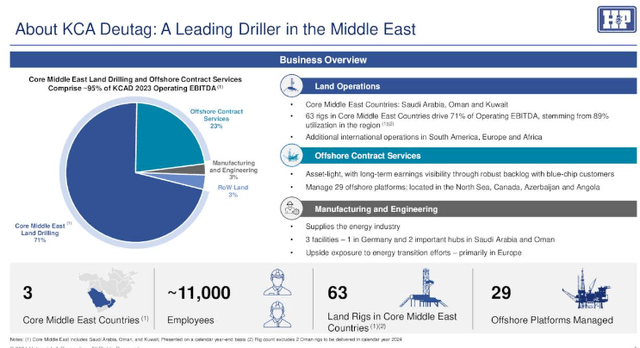

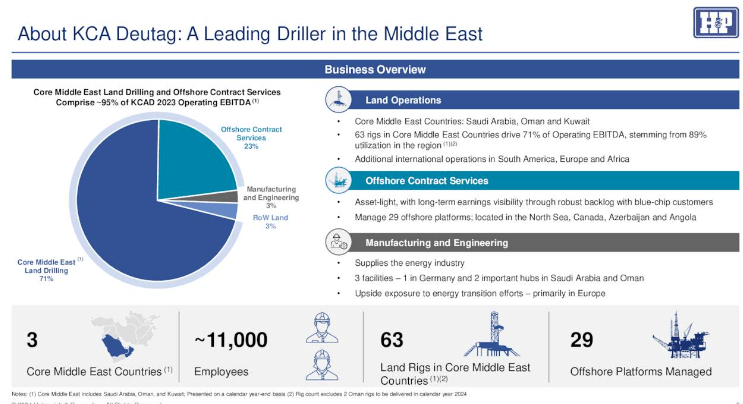

KCA Deutag details (H&P)

The slide above gives an idea of KCA’s core geographic footprint, manpower, and service distribution between land rigs and offshore platform rigs. KCA also brings local, in-theater, manufacturing capabilities that will help set apart H&P from other companies.

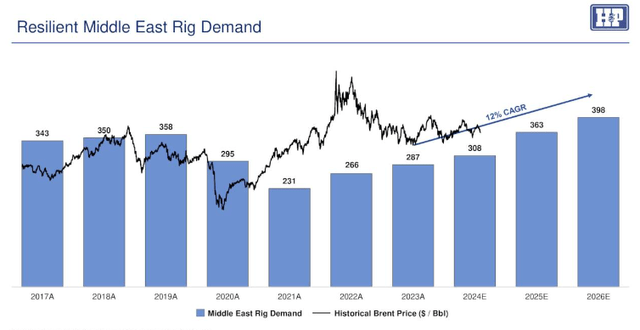

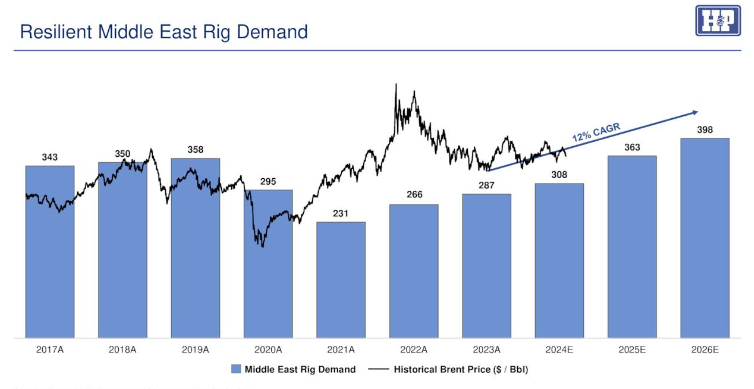

The Middle East market is forecast to grow at a 12% CAGR through 2026, and I expect when this slide is updated for future presentations, this trend will continue. Conversely, while I expect the U.S. rig count will rebound, the days of an 800+ rig market are behind us. The logic behind the KCA/H&P merger becomes crystal clear in this context.

Middle East Rig demand (H&P)

Q-3, 2024 and outlook

The Company reported fiscal third quarter net income of $89 million, or $0.88 per diluted share; on revenue of $695 mm, a slight increase from Q-2’s $685 mm. Net cash provided by operating activities was $197 million for the third quarter of fiscal year 2024 compared to net cash provided by operating activities of $144 million for the second quarter of fiscal year 2024.

Capital expenditures for the full fiscal year 2024 are still expected to be at the top end of the original range, around $500 million. Total international expansion CapEx this fiscal 2024 is approximately $175 million, which is 35% of the fiscal 2024 total expected CapEx.

H&P had cash and short-term investments of approximately $290 million at June 30, 2024, versus an equivalent $277 million at March 31. They repurchased a limited number of shares in fiscal Q2, but did not buy back any shares in fiscal Q3, even though per share values were below the trailing 18 months average buyback levels at times within the quarter. Instead, seeking to preserve cash on hand for the contemplated KCA Deutag transaction.

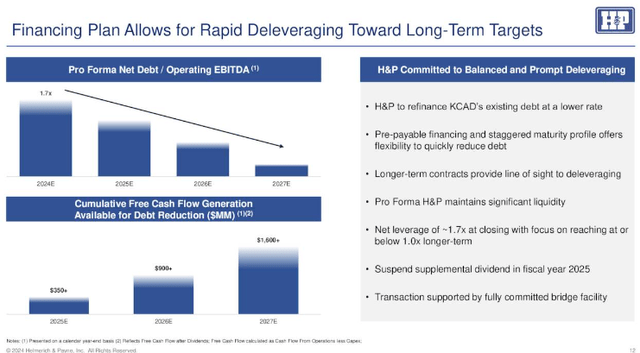

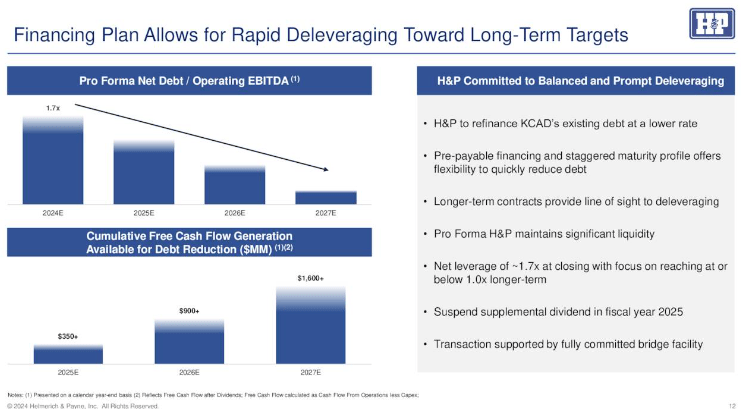

For the KCA Deutag acquisition, H&P is willing to temporarily increase their leverage to take advantage of a meaningful international growth opportunity. They expect to maintain their investment grade rating. Debt reduction will be a capital priority for one to two years post-close. The slide below gives a forecast for carrying out deleveraging.

KCA financing plan (H&P)

The Company declared a quarterly base cash dividend of $0.25 per share and a supplemental cash dividend of $0.17 per share; both dividends are payable on August 30, 2024, to stockholders of record at the close of business on August 16, 2024.

Segment results

The North America Solutions (“NAS”) segment exited the third quarter of fiscal year 2024 with 146 active rigs and recognized revenue per day of $39,800/day with associated direct margins per day of $20,300/day during the quarter. Quarterly NAS operating income increased $16 million sequentially; while direct margins increased by $6 million to $277 million, as revenues increased by $6 million to $620 million and expenses remained relatively flat at $343 million.

H&P’s NAS segment anticipates exiting the fourth quarter of fiscal year 2024 between 147-153 active rigs.

International

This segment had an operating loss of $4.8 million, compared to operating income of $3.6 million during the previous quarter. The decrease in operating income was mainly due to recommissioning expenses for rigs that will be exported to Saudi Arabia and related start-up costs. Direct margin during the third fiscal quarter was $0.4 million, compared to $8.4 million during the previous quarter. Current quarter results included a $2.1 million foreign currency loss, compared to a $0.5 million foreign currency loss in the previous quarter.

Offshore Gulf of Mexico:

This segment had operating income of $5.0 million compared to operating income of $0.1 million during the previous quarter. Direct margin for the quarter was $7.6 million compared to $2.9 million in the previous quarter. The increase in operating income was primarily attributable to rigs moving to full operating rates earlier than planned.

Outlook for full year 2024

Based on this quarter’s results and their projections for the final quarter of the fiscal year, H&P is generating ample cash flow to cover this year’s extended capital expenditures, the base dividend, this fiscal 2024 supplemental dividend plan, and the share repurchases to date.

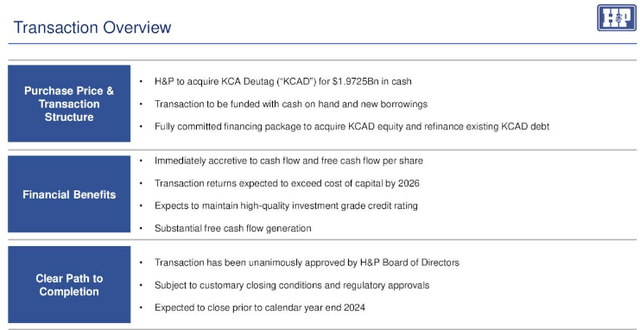

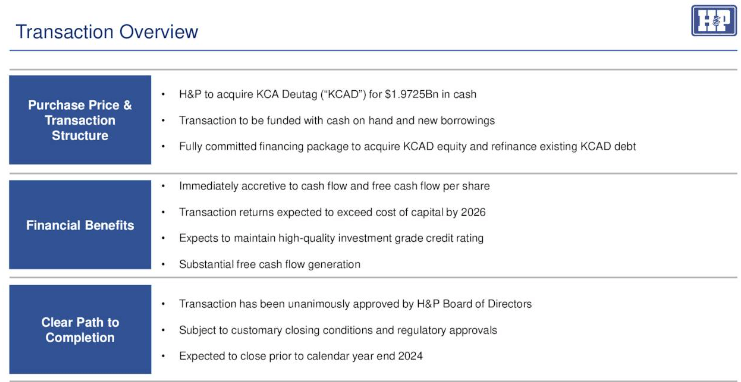

Details of the deal

On a combined basis, the combined company would have delivered operating EBITDA of approximately $1.2 billion over the past 12 months, an increase of more than 30% from H&P on a standalone basis.

KCA Transaction overview (H&P)

This transaction will grow their international land operations from approximately 1% on a standalone basis to approximately 19% on a pro forma basis on calendar year 2023 operating EBITDA. And offshore operations are expected to grow from approximately 3% on a standalone basis to approximately 7% on a pro forma basis.

On a pro forma basis, about 1/4 of the combined company’s operating EBITDA will come from international and offshore operations, creating a diversification from our legacy U.S. onshore business. As a result, H&P will have better geographical balance in earnings and cash flow streams.

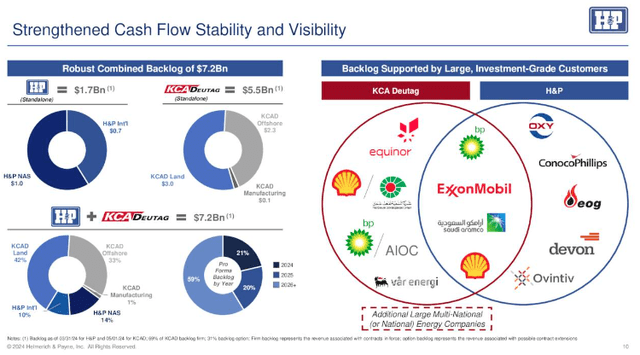

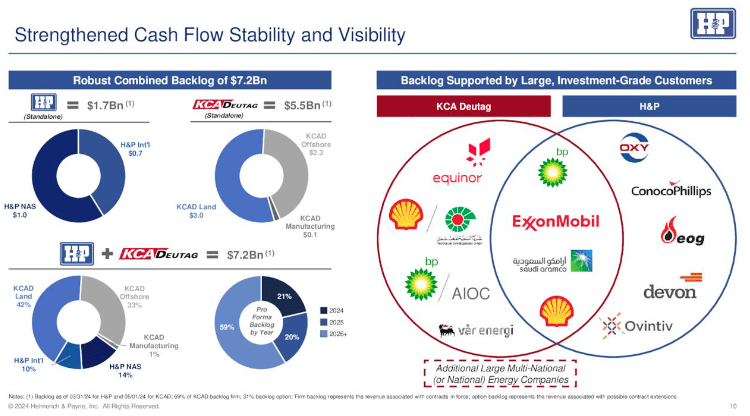

KCA Deutag adds approximately $5.5 billion of contract backlog to H&P’s $1.7 billion, approximately $3.8 billion of which is firm and approximately $1.7 billion of which is optioned. This includes work for large, well-known customers of KCA Deutag including BP, ExxonMobil and Shell, as well as NOCs in key international markets.

H&P projected cash flow (H&P)

The transaction is accretive to all key financial metrics. It is immediately accretive to cash flow and free cash flow per share and increasingly accretive thereafter, with double-digit free cash flow accretion expected as soon as 2025. Furthermore, the returns from this transaction are expected to exceed cost of capital by 2026.

H&P is acquiring KCA Deutag at a transaction multiple of approximately 5.4x. This is much lower than the trading multiples of other Middle East public peer companies.

Risks

H&P is trading near the top of its recent range of $32-42, and just below support at $38.41, and just at its 200-day SMA. While we see the KCA deal as a big plus for H&P, the market is in no mood to reward any long-term thinking with the current softness in oil and gas prices. In short, without a strong catalyst for commodities, better prices may be obtained as we move through the quarter.

Your takeaway

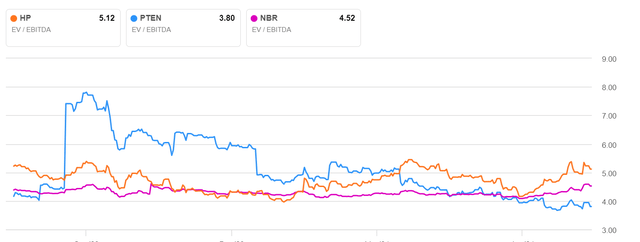

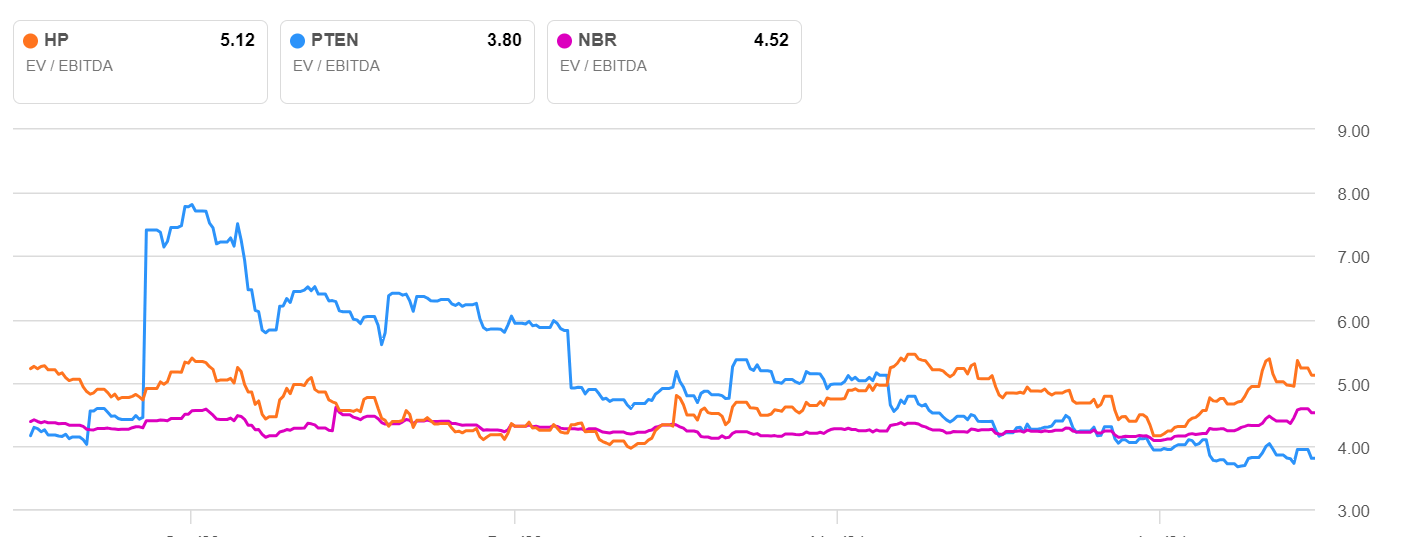

As a standalone, H&P is trading at 5.12X EV/EBITDA, at the top of its recent range and well ahead of competitors-none of whom have H&P’s standing in the industry or its international exposure.

EV/EBITDA driller cohort (Seeking Alpha)

Assuming the transaction goes through, and we don’t see anything to prevent it, when KCA financials are consolidated to the H&P balance sheet, the multiple should adjust to 5.25X, so no big boost coming in the short term.

I think patience is warranted here for investors wanting to add H&P to their portfolios. The recent run-up in share prices has taken the stock to near one-year highs. I think the market may deliver better pricing, and plan to monitor for an entry point closer to recent lows in the $32’s.

Source link