Don’t Let Kinder Morgan’s Upswing Turn You Away (NYSE:KMI)

Daniel Wright/iStock Editorial via Getty Images

Kinder Morgan (NYSE:KMI) is a massive infrastructure company with a market capitalization of almost $50 billion. The company has been hitting some of its strongest share prices since the 2020 crash. At the same time, the company has continued to pay out a dividend of almost 6% and generate strong shareholder returns.

As we’ll see throughout this article, the company is a strong investment.

Kinder Morgan 2Q 2024 Results

Kinder Morgan reported its 2Q 2024 results with $0.26 / share in EPS (P/E of 20 annualized) and DCF per share, putting the company at a 10% yield.

Kinder Morgan Investor Relations

The company generated a massive $1.1 billion in DCF ($4.4 billion annualized). The company’s size along with its continued 10% DCF yield will enable long-term shareholder returns. The company’s DCF covers its dividend yield of almost 5.6% while still leaving the company with roughly $2.4 billion annualized it can utilize for growth.

Those are strong results for the company.

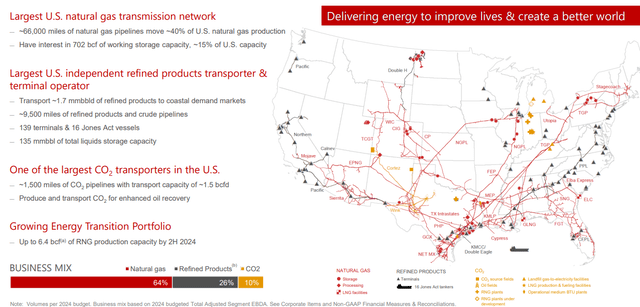

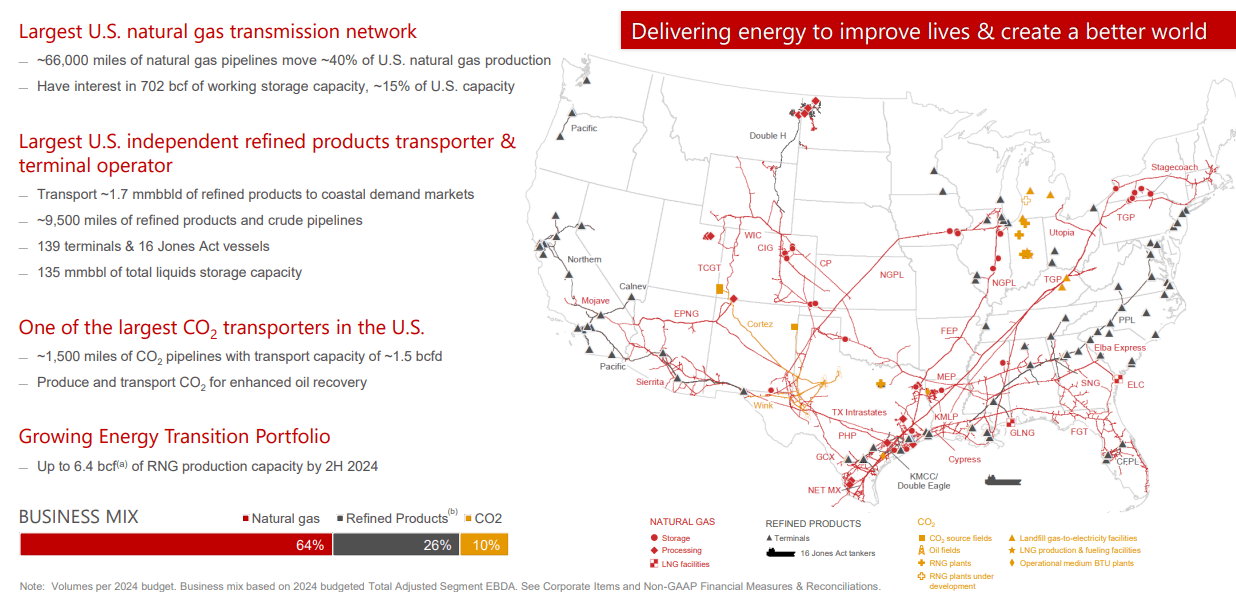

Kinder Morgan Infrastructure Portfolio

The company maintains one of the largest infrastructure portfolios in the country, focused on natural gas.

Kinder Morgan Investor Relations

That’s important because natural gas has much more staying power than oil for the company. The company’s business is a massive 64% natural gas. The company has ~66 thousand miles of natural gas pipelines, moving ~40% of U.S. natural gas production. The company also has a ~15% interest in U.S. storage capacity, showing its strong integration to the market.

The company is also the largest U.S. independent refined product transporter and one of the largest CO2 transporters. The company has numerous terminals and Jones Act vessels along with storage capacity. All of this will enable continued reliable cash flow for the company’s infrastructure.

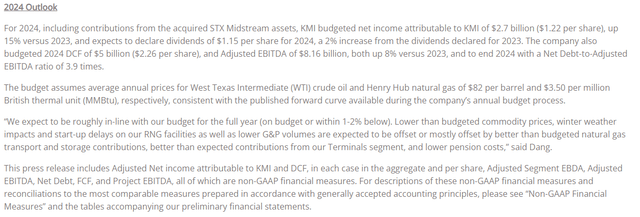

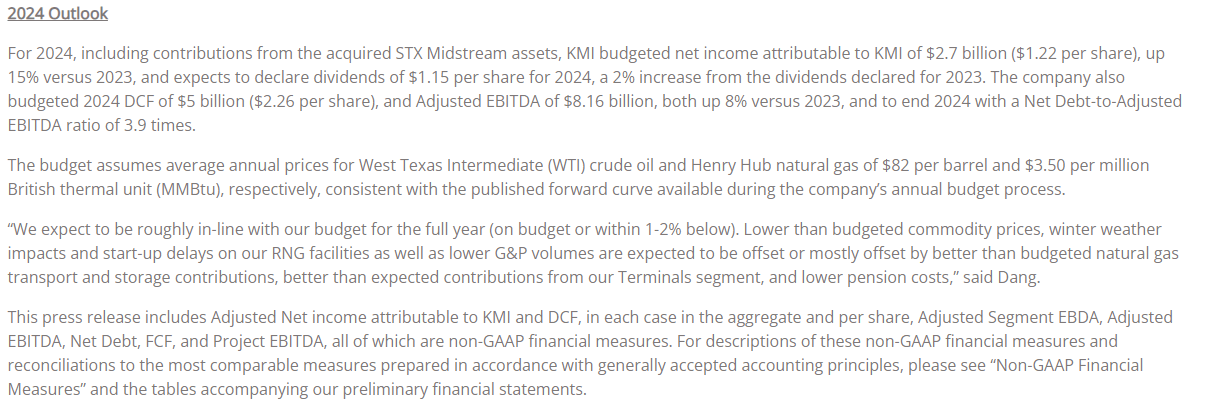

Kinder Morgan 2024 Outlook

Kinder Morgan has a 2024 outlook focused on long-term shareholder returns.

Kinder Morgan Investor Relations

The company acquired STX Midstream for almost $2 billion, providing it with strong assets that integrate well into the remainder of its asset portfolio. The company has increased its dividend by 2% and is budgeting $5 billion in DCF. That’s enough for the company to continue generating double-digit shareholder returns off of its DCF.

The company has an incredibly manageable net-debt-to-adjusted EBITDA of roughly $32 billion, with a ratio of 3.9x. That’s not the lowest ratio in the industry, but even in a higher interest rate environment, it’s a ratio that the company can comfortably manage. The ~$1.5 billion in annual interest is something the company can comfortably afford.

The company’s 2024 outlook shows how it can continue generating strong long-term shareholder returns.

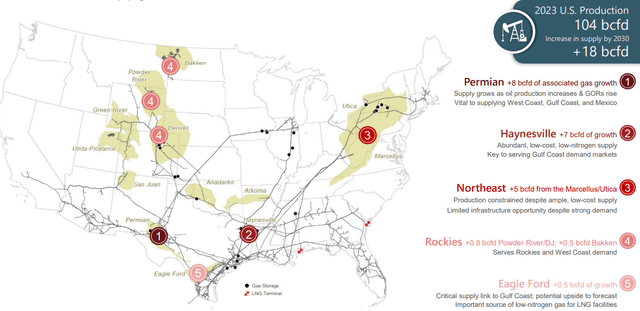

Market Demand Growth

The company has the ability to continue to benefit from a strong market, especially for natural gas.

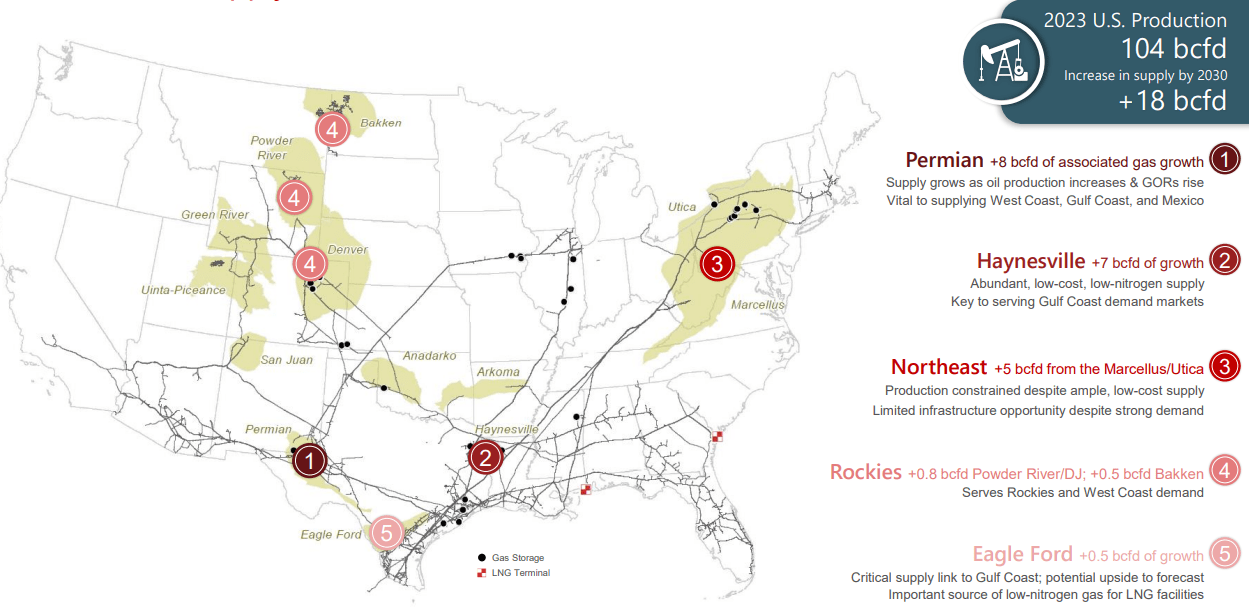

Kinder Morgan Investor Relations

Overall 2023 U.S. production was a massive 104 billion cubic feet / day and supply is expected to expand by 18 billion cubic feet / day by 2030. That’s almost 20% growth over the next 6 years. That growth will come from a variety of basins, but a common theme for all of these basins is the largest distance between them and LNG exports or population centers.

That continued market demand means strong long-term demand for Kinder Morgan’s assets, along with additional growth potential.

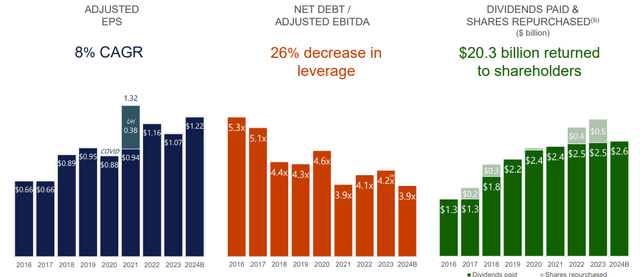

Kinder Morgan Shareholder Returns

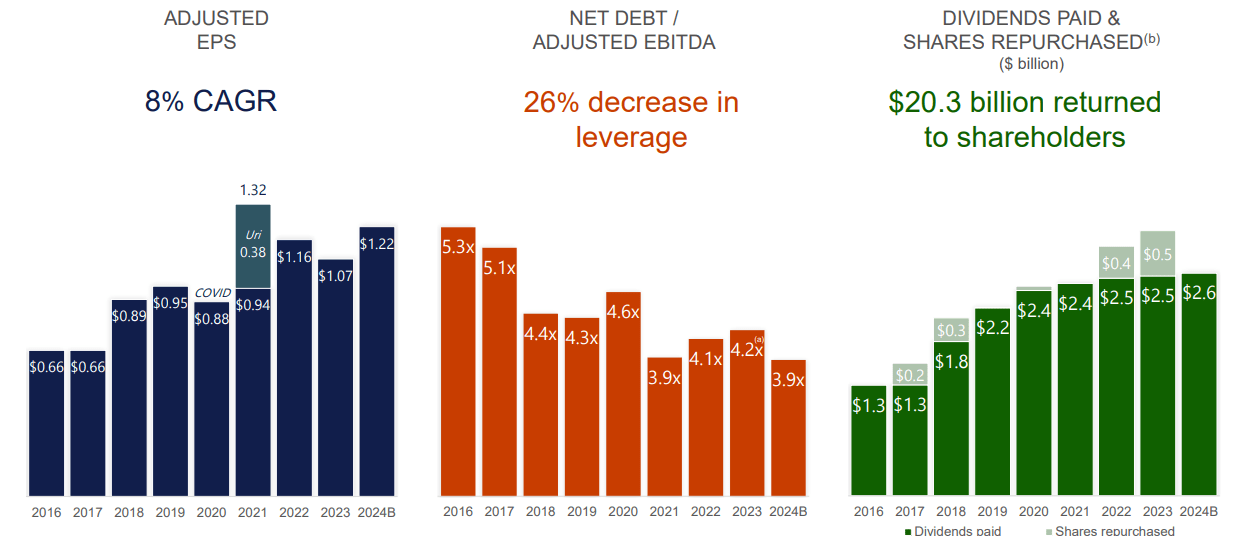

Kinder Morgan has a long history of generating shareholder returns using its DCF intelligently.

Kinder Morgan Investor Relations

The company continues to pay the majority of its DCF to its incredibly strong dividend yield of almost 6%. The company has repurchased shares in prior years, but right now, it’s more focused on capital spending. It has a $3.3 billion capital program expected to come in service in 2024-2025 primarily (85%) which will provide roughly $600 million in additional annual EBITDA.

This growth in EBITDA has been the primary source of the company’s decreased leverage. The company has seen 8% annualized EPS growth, and we expect that growth to continue. The company’s ability to provide an almost 6% dividend along with growth highlights how it’s such a good investment. The company’s willingness to use share repurchases is also exciting.

The company’s continued intelligent usage of its cash flow makes it a valuable investment.

Thesis Risk

The largest risk to our thesis is that Kinder Morgan is dependent on long-term demand and changing secular trends. Demand for oil is expected to decline over the long-term, and demand for natural gas is growing for now but isn’t expected to grow forever. That could hurt the company’s ability to generate long-term shareholder returns.

Conclusion

Kinder Morgan’s earnings highlight its continued success on its path to earn $5 billion in DCF in 2024, a double-digit DCF yield on the company’s strong portfolio of assets. The company is able to use this to pay a dividend yield of almost 6% along with continued massive capital investments with the company’s backlog of more than $3 billion.

The company’s EBITDA ratio on these new assets is expected to add more than $500 million in annualized EBITDA. That will add even more DCF and enable growing dividends. We’d like to see the company repurchase some shares if possible; however, regardless of how the company uses its DCF, it’s a valuable long-term investment.

Source link