Super Micro Computer Gets A Reality Check (NASDAQ:SMCI)

J Studios

Super Micro Computer (NASDAQ:SMCI) was hit with a reality check in q4’24 as the firm experienced exceptionally strong growth at the risk of marginally disappointing operational performance. Much of this was the result of the firm managing their supply chain risk in order to capture market share for their direct liquid cooling server racks as the AI infrastructure investment frenzy continues. Despite the substantial top-line performance, I believe analysts are growing concerned about SMCI’s attempt to grow too fast; as the firm continues to leverage their balance sheet to raise capital in the debt and equity capital markets to finance their hypergrowth state. Though I anticipate this growth to be sustainable through eFY26, I believe the firm may be trading off operational excellence for market capture, posing a risk to overall performance during a time of unclear economic growth. Given the operational challenges afoot, I am downgrading my recommendation to a SELL rating with a price target of $450/share at 8.15x eFY26 EV/aEBITDA.

FinChat

Operations & Risks

Super Micro Computer is finding itself in a similar place as Intel (INTC) in which the firm is ramping up production to catch up with demand. Though the two firms are day and night different, they’re both playing catch-up to take full advantage of this AI infrastructure buildout while risking operational efficiencies. In SMCI’s case, the catch-up is expediting materials for their DLC liquid-cooling racks. In Intel’s case, the firm is outsourcing A20 production in order to manufacture more AI PCs while demand is ramping up. In both cases, margins are severely compressed, resulting in lackluster operational performance that was reflected in each respective stock’s performance following their earnings releases.

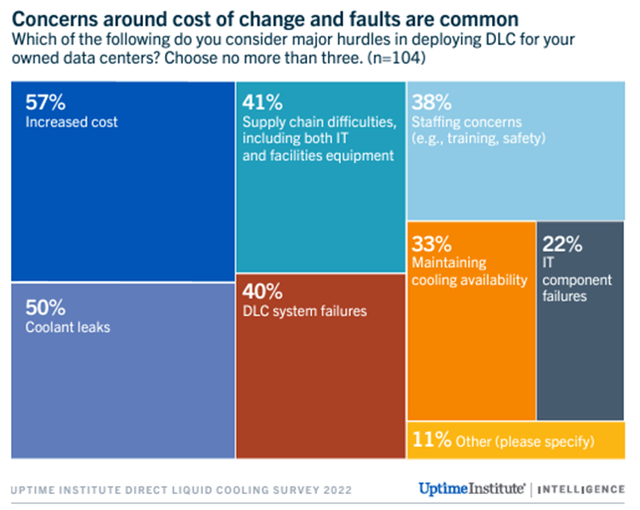

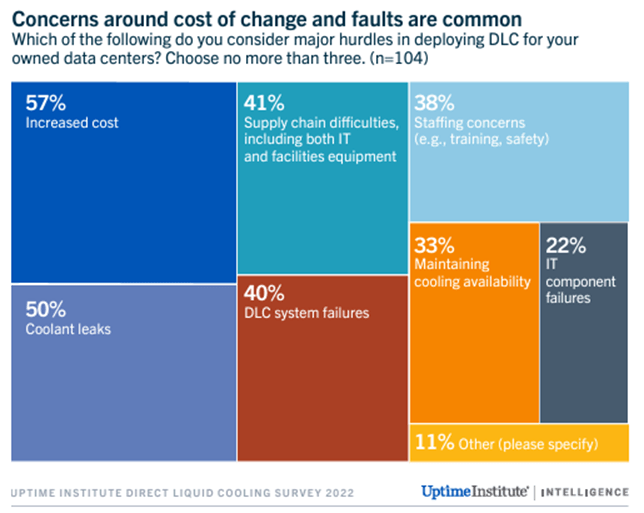

There were some peculiar questions asked by analysts that were left unanswered on the call. Mr. Nehal Chokshi asked about DLC failure rates, as he had heard rumors that the technology may have higher rates when compared to direct air cooling. Given that I don’t have direct exposure to data center operations, I cannot attest to any information pertaining to challenges with DLC; however, a quick search for DLC failures provides information relating to the subject. Accordingly, the top issues include increased costs, coolant leakage, system failures, and supply chain difficulties.

Uptime Institute

Though a heightened failure rate for DLC may be concerning, I do not believe this will materially impact sales to the downside, as DLC is said to be 30-40% more power-efficient than direct air cooling. This feature is exceptionally appealing given that hyperscalers will likely be partnering with utilities, midstream operators, and upstream gas producers in order to source adequate power for these massive facilities. Depending on the contractual agreements, this could either drive up services revenue or impact margins through a warranty feature if failure is expected within the limitations of the agreement. According to SMCI’s 10-k, the firm does offer 1-3 year and extended warranties that include servicing of the equipment. One additional factor that may impact this is the cost of the coolants. Depending on the type of coolant used within the DLC rack, the price for coolants may be increasing in the coming years as more stringent regulations are placed for production of virgin HFCs.

In terms of this infochart, SMCI faced challenges relating to supply chain constraints in sourcing materials, leading to the firm expediting materials in order to fulfill orders. This was one of the leading challenges that resulted in the 10.54% adjusted gross margin in q4’24. For reference, this fell significantly below the firm’s recent range of 15-19% adjusted gross margin.

The other side to the decline in the gross margin was the customer mix, which was more heavily weighted to hyperscalers as opposed to enterprises, which pose tighter margins. Though I believe AI/LLM models will inevitably be located in private data centers given the high costs associated with running models in cloud environments, I do not anticipate this transition to occur until enterprises begin bringing their applications into the production environment. In the instance of an economic contraction or recession, I believe enterprises will push out further investments into their private data centers as they pertain to AI/LLM applications and will require significant capital investments and operational expenses in order to source and manage the infrastructure. If these two cases play out, hyperscalers may remain a heavier weight of SMCI’s customer mix.

One question raised on the q4’24 earnings call was whether the delay in the production ramp of Nvidia’s (NVDA) Blackwell GPUs would impact sales targets for SMCI. This question was also asked during Arista Networks’ (ANET) q1’24 earnings call, as sourcing GPUs was more challenging at the time. I do not believe that enterprises and hyperscalers would necessarily choose a different cooling system or push out cooling rack infrastructure as a result of delays in their next generation GPUs, given that IT-related investments are made for future scale as opposed to the current demand. I believe that there are bigger constraints at play that could result in delayed purchases: construction of the facilities and power sourcing. Power transmission may be a major bottleneck worth considering, given that transformers are in short supply. According to the July ISM-PMI Services print, construction contractors & subcontractors and electrical components & electrical equipment are in short supply. CleanSpark (CLSK), a bitcoin mining company, has been facing delays in bringing one of their data centers online as a result of the transformer shortage. These factors could result in slower sales growth for SMCI if the supply constraints persist.

Super Micro Computer Financials

Corporate Reports

Taking into consideration management’s guidance, I anticipate SMCI to run on tight margins throughout eFY25 with incremental improvements quarter-by-quarter. I anticipate eFY26 to experience more normalized margins but still remain below their FY23 level of 18% gross.

I anticipate enterprises to moderate IT investments throughout the duration of eCY24 and eCY25 as a result of the persistent economic challenges as they pertain to inflationary pressures and challenged margins. The automotive OEMs have suggested challenges in moving inventory, which I believe to be an early sign of further economic woes to come. Consumer demand appears to be moderating, if not declining, across different nodes, which may result in tighter budgetary constraints for enterprises in the coming quarters. This may result in tighter capital investments for new IT infrastructure in the near-term as enterprises grapple with tighter margins paired with lower revenue growth.

Given that hyperscalers are dependent on providing the best user experience gives me reason to believe that capital investments will not slow, regardless of the economic climate. My rationale behind this is that AI training is dependent on low latency, high speeds, and cost moderation in order to be successful. This suggests that hyperscalers will do everything within their power to invest in the latest GPUs, cooling systems, networking equipment, and power transmission in order to maintain their competitive quality of service.

Investment Risks For Super Micro Computer

Bull Case

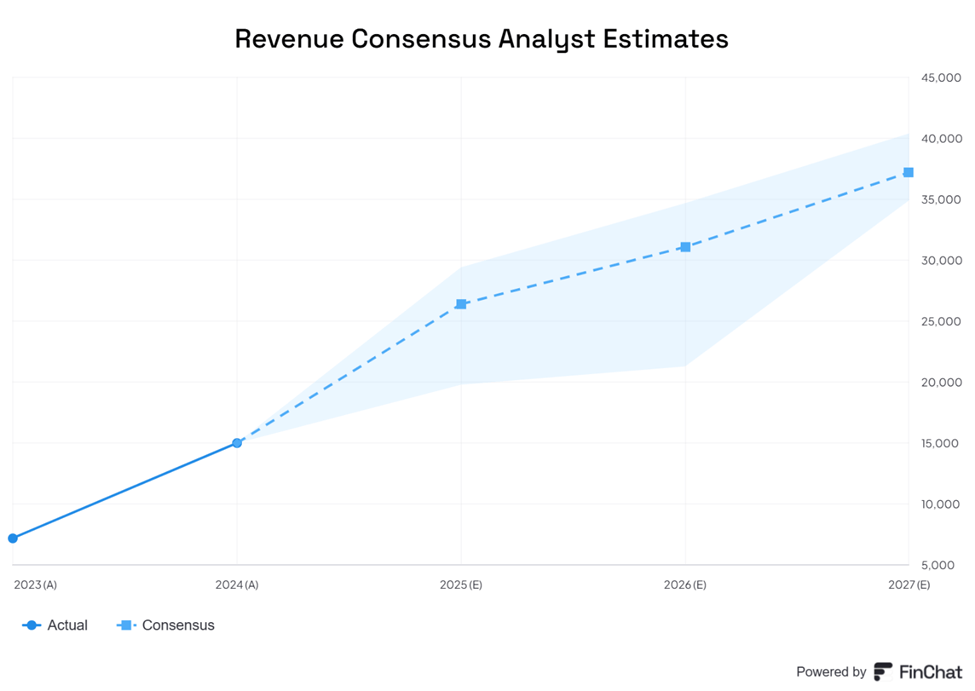

The bull case for SMCI is that the firm is scaling their operations in order to cater to the heightened demand for their plug-and-play server rack technology. Management suggested that the firm will have the capacity to ship 3,000 server racks per month by November, up from 1,000 seen in q4’24. This can be a major revenue growth catalyst for the firm, allowing for the firm to reach guidance of $26-30b in eFY25. Through scaled operations, gross margins should migrate back to more normalized ranges between 15-19%, a major improvement from q4’24’s adjusted gross margin of 10.54%. Management also remains focused on enhancing their go-to-market strategy for building up their enterprise sales pipeline, which will likely attribute to margin expansion.

The increasing demand for AI infrastructure leads me to believe that investments within the AI space will persist for the time being. Dell Technologies (DELL) and Hewlett Packard Enterprise (HPE) each show growing backlogs for AI infrastructure that may persist as the next generation of GPUs are released between Nvidia and Advanced Micro Devices (AMD).

Bear Case For SMCI

SMCI is raising capital as if they’re in a hypergrowth state. The ultimate question is, will all these investments pay off, or will the rug be pulled out from under them? Though I do not anticipate any shortage of investments at the hyperscaler-level any time soon, adoption of AI/LLM applications in the cloud may determine the capital outlay in the coming quarters. Microsoft (MSFT) and Oracle Corp. (ORCL) continue to make major investments in infrastructure to build out their AI factories. What I’m getting at here concerns whether this level of spending will persist if their customer base pulls back on their AI/LLM journey if found less viable than initially expected during the hype mania? If this does occur, SMCI could be caught flat-footed in the process as the firm undergoes a major round of capital investments, catering to consistently growing capital investments towards AI factories and leaving equity investors tied up in a company with growing debt and equity dilution.

Valuation & Shareholder Value

Corporate Reports

SMCI shares experienced a significant decline post-q4’24 earnings that resulted in a decline of -15% to the share price. Shares have continued to remain at this level as investors digest the lackluster margin performance despite the significant growth outlay. Taking into consideration SMCI’s historical valuation, the shares appear to be undervalued based on my eFY26 forecast for adjusted EBITDA.

Corporate Reports

From a company comps perspective, SMCI appears to be relatively overvalued. Given the recent operational challenges SMCI was exposed to in q4’24, I believe that we may be in the early stages of the stock’s valuation coming back down to earth and more in line with its peers.

Seeking Alpha

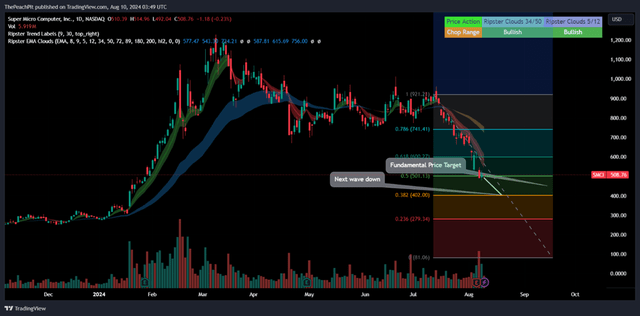

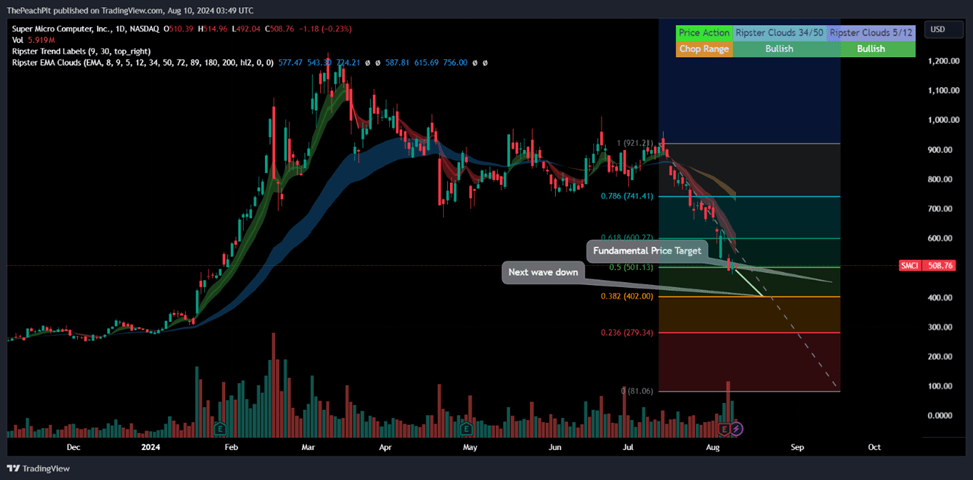

From a tactical perspective, shares may continue their downward trend as the stock began its wave retracement in March 2024. Given the stock’s trajectory, I have reason to believe the stock could land at ~$400/share to complete its c-wave. Net of market dynamics, I believe that eq1’25 will determine whether SMCI will experience an upward retracement once the c-wave is completed, or an extended downward retracement.

TradingView

Given the economic headwinds paired with the need for operational improvements, I recommend SMCI shares with a SELL rating with a price target of $450/share at 8.15x eFY26 EV/aEBITDA. This valuation will place SMCI more in line with its IT infrastructure peers at 1.93x TTM price/sales, just over the market cap-weighted peer price/sales average of 1.83x.

Source link