Invesco Small Cap Growth Fund Q2 2024 Review

Vertigo3d

Key takeaways

- The fund outperformed its benchmark.

- The fund held up better than its benchmark as both declined for the quarter. Stock selection in health care, consumer discretionary, technology and financials contributed to the fund’s outperformance of its index. Selection in industrials and consumer staples detracted.

- Small cap stocks underperformed large-cap stocks.

- The US small-cap universe declined in the second quarter, trailing US large-cap as investors appeared to consider the potential negative effects if interest rates stay higher for longer.

- We remain cautious with a balance of defensive stable growth and offensive cyclical growth.

- While the market seems in our view ready for a shift to lower interest rates, we remain cautious and continue to monitor the weight of the evidence for possible changes in interest rates and the economy.

Manager perspective and outlook

Large-cap US equities advanced during the second quarter as investors appeared to continue to process the possibility of a Fed pivot to easier monetary policy in 2024 and a select group of mega-cap technology stocks rallied on headlines about artificial intelligence.

The US small-cap universe declined during the second quarter, trailing US large-caps, as investors appeared to consider the potential negative effects if the Fed keeps interest rates higher for a longer period.

Since 2022, interest rate increases have slowed the US economy and dampened inflation, although the US labor market has remained healthy. While markets seem in our view ready for a shift to lower interest rates, we remain cautious and continue to monitor data in order to weigh the evidence for or against changes in interest rates and the economy. We scaled back some defensive positioning and introduced more cyclicality to the fund. However, we are aware of potential risks, so we seek to maintain balanced positioning. We see artificial intelligence as a significant technology trend with wide-ranging implications for technology investment, employment and productivity enhancements moving forward.

Portfolio positioning

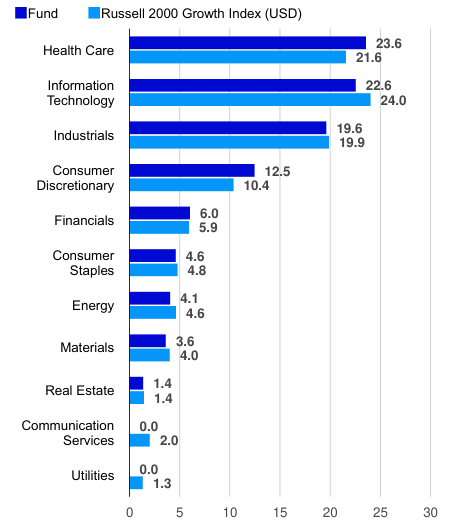

At the end of the second quarter, the fund’s largest absolute weights were in the health care, technology, industrials and consumer discretionary sectors. Relative to the Russell 2000 Growth Index, the fund was overweight in consumer discretionary and health care and underweight in communication services, technology and utilities. During the quarter, we added to the fund’s positions in health care and materials and reduced exposure in the technology, industrials and consumer discretionary sectors. In technology, we added Rambus (RMBS), Impinj (PI), SiTime (SITM), Nova and Itron (ITRI) and sold DoubleVerify (DV), Manhattan Associates (MANH), Blackline (BL), Freshworks (FRSH), Lattice Semiconductor (LSCC), Credo Technology (CRDO), Gitlab (GTLB) and Globant (GLOB). In health care, we added Vericel (VCEL), ADMA Biologics (ADMA), Integer (ITGR), Inspire Medical Systems (INSP), Encompass Health (EHC) and BioLife Solutions (BLFS) and sold Cytokinetics (CYTK), Shockwave Medical (SWAV) and Acadia Healthcare (ACHC). In industrials, we added FTAI Aviation (FTAI). In consumer discretionary, we added SharkNinja (SN) and sold On Holding (ONON). In consumer staples, we sold Grocery Outlet (GO). In energy, we sold ChampionX (CHX). In materials, we added ATI (ATI).

Second quarter additions to the fund:

Rambus makes memory semiconductor chips.

Impinj makes radio-frequency identification (RFID) devices and software.

SiTime makes miniaturized electro-mechanical circuitry and systems for advanced precision timing devices.

Nova makes dimensional, material and chemical metrology solutions for semiconductor manufacturing.

Itron provides systems for utilities and municipalities to manage energy, water and infrastructure.

Vericel makes a biological human cellular product used in orthopedic surgical treatments.

ADMA Biologics makes immuno-technology plasma-derived therapeutics to treat infectious diseases and manage immunocompromised patients.

Integer provides outsource manufacturing to medical device equipment manufacturers.

Inspire Medical Systems provides implanted devices used to treat obstructive sleep apnea.

Encompass Health operates rehabilitation hospitals.

BioLife Solutions provides cryogenic cell processing consumables and storage services.

FTAI Aviation provides aircraft leasing, aircraft engine leasing and engine repair parts and services.

SharkNinja makes Shark and Ninja brand household products, including vacuums, steam mops, hair dryers, countertop appliances and more.

ATI makes high-performance metals, alloys and components for aerospace, defense, energy, auto, electronics, medical and mining.

Top issuers (% of total net assets)

Fund | Index | |

Natera Inc (NTRA) | 1.69 | 0.00 |

Glaukos Corp (GKOS) | 1.69 | 0.44 |

Onto Innovation Inc (ONTO) | 1.55 | 0.71 |

Wingstop Inc (WING) | 1.52 | 0.00 |

TransMedics Group Inc (TMDX) | 1.38 | 0.37 |

Tenet Healthcare Corp (THC) | 1.36 | 0.00 |

Guidewire Software Inc (GWRE) | 1.35 | 0.00 |

Clean Harbors Inc (CLH) | 1.35 | 0.00 |

TMX Group Ltd (OTCPK:TMXXF) | 1.31 | 0.00 |

Element Solutions Inc (ESI) | 1.24 | 0.00 |

As of 06/30/24. Holdings are subject to change and are not buy/sell recommendations. | ||

Sector breakdown (% of total net assets)

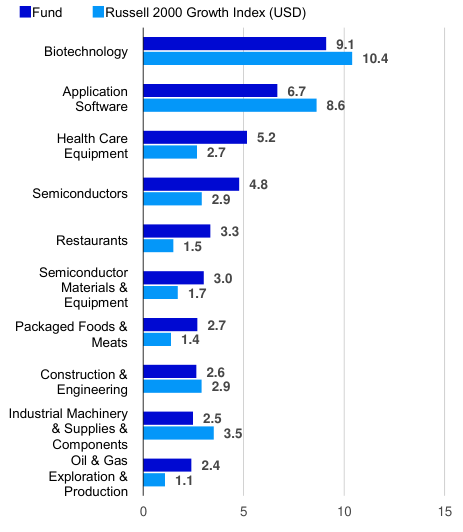

Top industries (% of total net assets)

Performance highlights

The fund outperformed its benchmark during the second quarter. Though both the fund and index declined, the fund held up better. Stock selection in the health care, consumer discretionary, technology and financials sectors contributed to the fund’s outperformance of the index. Stock selection in industrials and consumer staples detracted.

Contributors to performance:

TransMedics provides technology and services to transport organs in a warm living state for transplant surgery. The company has expanded its aircraft fleet with the goal of capacity, volume and margins.

Twist Bioscience (TWST) makes synthetic DNA used in biopharma research and development. The company reported better-than-expected revenue and raised guidance while continuing to build manufacturing capacity with the goal of meeting growing demand.

Glaukos makes treatments and diagnostics for glaucoma and other eye disorders. The company reported better-than-expected revenue and raised guidance due to momentum in its treatment for intraocular pressure.

Tenet Healthcare operates hospitals, imaging centers, ambulatory surgery centers and other health facilities. The company has benefited from improving hospital utilization trends, a favorable shift in its procedure mix, and use of proceeds from hospital sales to reduce its debt.

Natera makes genetic diagnostics and monitoring tests for oncology, organ health and pre-natal testing. The company has benefited from momentum in its cancer diagnostic business and effective execution in its pre-natal testing business.

Detractors from performance:

DoubleVerify provides systems to monitor and analyze the effectiveness of digital advertising and ecommerce. The company has experienced headwinds from lower advertisement spending by several major customers.

Inspire Medical Systems provides implanted devices to treat obstructive sleep apnea. Despite reporting double-digit sales growth, the stock declined on lower-than-expected US sales. The deceleration in sales growth and competitive threat from GLP-1 obesity drugs appear to have weakened investor sentiment. We have observed evidence that mitigates the competitive threat.

Kinsale Capital (KNSL) is a property and casualty insurer specializing in excess and surplus lines of insurance. The stock declined on a deceleration in revenue growth due to difficult year-over-year comparisons.

Repligen (RGEN) provides instruments, software, consumables and services used in bioprocessing and biopharma research and development. The stock declined during the quarter due to the longtime CEO’s transition to Executive Chairman and a continued slow recovery in its bioprocessing end market.

SiteOne Landscape Supply (SITE) distributes landscape supplies for residential and commercial landscape professionals. The stock declined during the quarter on falling commodity prices and slower end market demand across product categories and geographies.

Top contributors (%)

Issuer | Return | Contrib. to return |

TransMedics Group, Inc. | 103.71 | 0.71 |

Twist Bioscience Corporation | 43.63 | 0.39 |

Glaukos Corporation | 25.52 | 0.35 |

Tenet Healthcare Corporation | 26.56 | 0.29 |

Natera, Inc. | 18.40 | 0.28 |

Top detractors (%)

Issuer | Return | Contrib. to return |

DoubleVerify Holdings, Inc. | -45.14 | -0.41 |

Inspire Medical Systems, Inc. | -44.29 | -0.37 |

Kinsale Capital Group, Inc. | -26.55 | -0.32 |

Repligen Corporation | -31.46 | -0.30 |

SiteOne Landscape Supply, Inc. | -30.44 | -0.27 |

Standardized performance (%) as of June 30, 2024

Quarter | YTD | 1 Year | 3 Years | 5 Years | 10 Years | Since inception | ||

Class A shares (MUTF:GTSAX) inception: 10/18/95 | NAV | -2.14 | 7.86 | 10.42 | -8.29 | 6.41 | 7.67 | 9.91 |

Max. Load 5.5% | -7.51 | 1.93 | 4.33 | -10.01 | 5.22 | 7.06 | 9.70 | |

Class R6 shares (MUTF:GTSFX) inception: 09/24/12 | NAV | -2.06 | 8.08 | 10.86 | -7.91 | 6.87 | 8.16 | 10.66 |

Class Y shares (MUTF:GTSYX) inception: 10/03/08 | NAV | -2.07 | 8.01 | 10.69 | -8.06 | 6.68 | 7.94 | 10.96 |

Russell 2000 Growth Index (‘USD’) | -2.92 | 4.44 | 9.14 | -4.86 | 6.17 | 7.39 | – | |

Total return ranking vs. Morningstar Small Growth category (Class A shares at NAV) | – | – | 37% (211 of 578) | 78% (422 of 550) | 64% (298 of 519) | 65% (258 of 403) | – |

| Expense ratios per the current prospectus: Class A: Net: 1.17%, Total: 1.17%; Class R6: Net: 0.75%, Total: 0.75%; Class Y: Net: 0.92%, Total: 0.92%. Performance quoted is past performance and cannot guarantee comparable future results; current performance may be lower or higher. Visit Country Splash for the most recent month-end performance. Performance figures reflect reinvested distributions and changes in net asset value (NAV). Investment return and principal value will vary so that you may have a gain or a loss when you sell shares. Returns less than one year are cumulative; all others are annualized. Index source: RIMES Technologies Corp. Please keep in mind that high, double-digit returns are highly unusual and cannot be sustained. Had fees not been waived and/or expenses reimbursed in the past, returns would have been lower. Performance shown at NAV does not include the applicable front-end sales charge, which would have reduced the performance. Class Y and R6 shares have no sales charge; therefore performance is at NAV. Class Y shares are available only to certain investors. Class R6 shares are closed to most investors. Please see the prospectus for more details. For more information, including prospectus and factsheet, please visit Invesco.com/GTSAX Not a Deposit Not FDIC Insured Not Guaranteed by the Bank May Lose Value Not Insured by any Federal Government Agency |

Source link