Grab 2Q24 Earnings: Robust Growth But Conservative Guidance (NASDAQ:GRAB)

gahsoon

Recap

In our latest article on Grab (NASDAQ:NASDAQ:GRAB), we wrote that Delivery Gross Merchandise Value (“GMV”) growth would be under pressure because of the pull-forward demand in the food delivery service. However, the positive sides were Mobility returning to pre-COVID levels, lower incentives as players pursue profitability over growth, and rapidly growing Fintech and high-margin Advertising businesses. Our fair value estimate of Grab was $3.6 per share, derived from the sum-of-the-parts (“SOTP”) valuation method. This implied a 14% upside potential. We reiterated a HOLD rating.

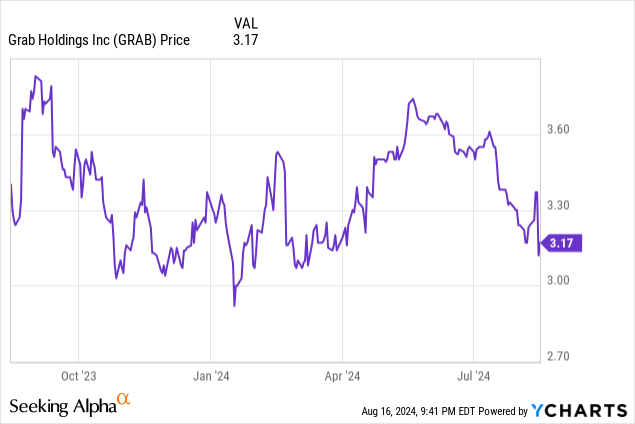

However, following the 2Q24 earnings release, the stock price dropped by over 7% to $3.1 per share before rising to $3.2 per share. Revenue came in below the consensus estimate.

This article will discuss the 2Q24 earnings results in more detail, and how our view has changed in these six months.

2Q24 Earnings Results

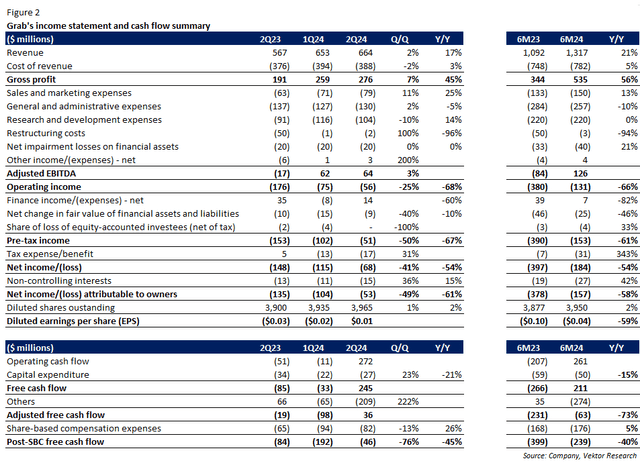

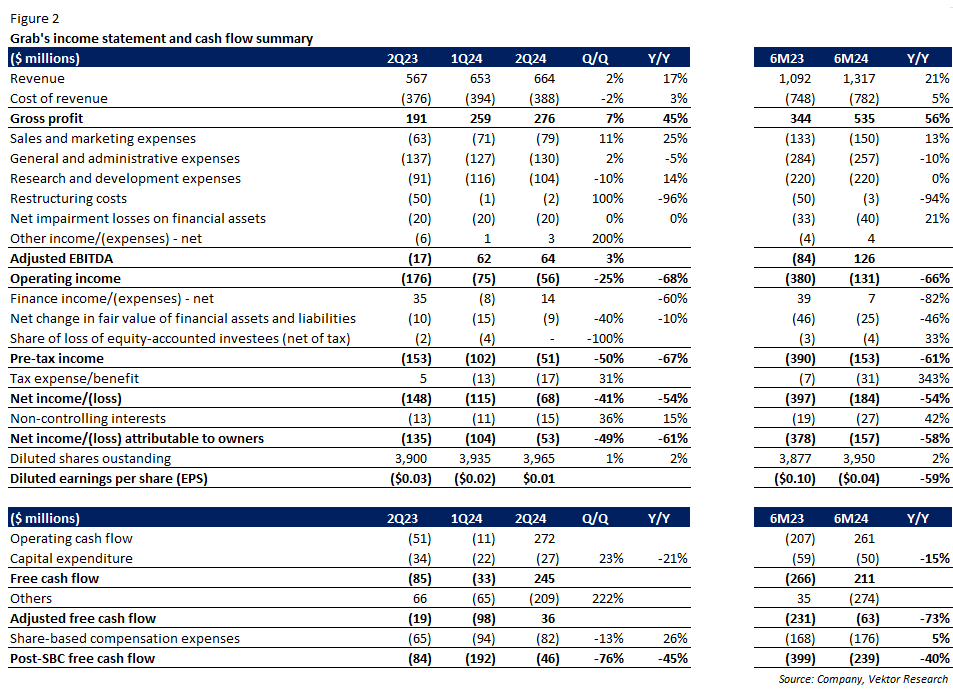

Please find the 2Q24 earnings summary below:

2Q24 earnings results summary (Company, Vektor Research)

Let us discuss each of the segment individually.

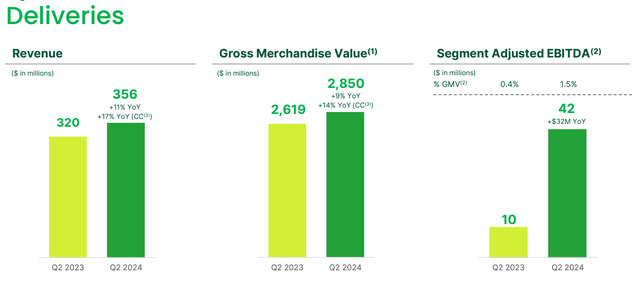

Deliveries

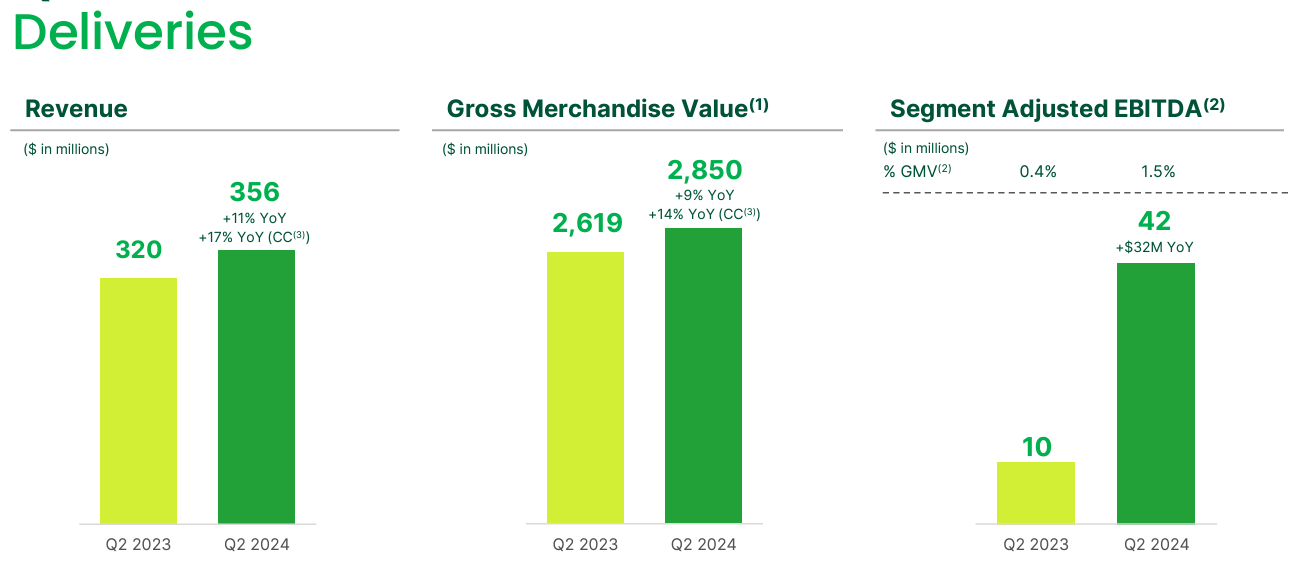

GMV grew 6% sequentially and 9% (Y/Y). However, on a constant-currency basis, the growth was 14% (Y/Y), driven by food delivery transactions that grew 11% year-on-year. The quarter-on-quarter GMV growth rate accelerated from a 1% decline in the previous quarter. We think the accelerating growth was propelled by higher MTU numbers thanks to Saver deliveries and the rapidly growing Advertising business, which took a greater portion of GMV vs. last quarter.

Grab did not disclose the on-demand MTU figure separately, but management said Saver deliveries accounted for 28% of Deliveries transactions compared with 10% a year ago. Besides Saver’s order frequency being twice as high as non-Saver users, Saver contributed 15% of new Deliveries monthly transacting users (“MTUs”).

In the Advertising business, monthly active advertisers grew 56% (Y/Y) to 168,000 during the quarter, up from 119,000 in 1Q24 (+41% Q/Q). Revenue from Ads is equal to 1.5% of Deliveries GMV, which was also driven by increasing average spending (+26% Y/Y).

Deliveries 2Q24 results (Company)

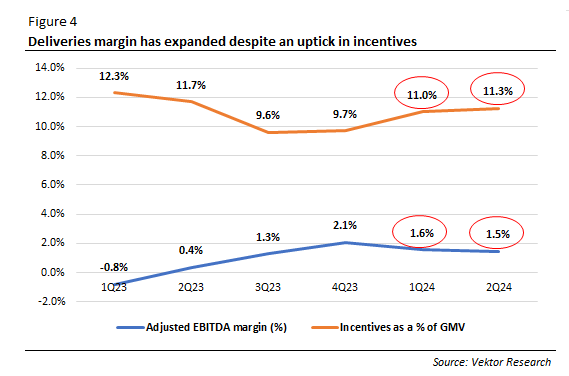

Revenue increased 2% (Q/Q) and 11% (Y/Y) or 17% (Y/Y) excluding foreign exchange impact, with the take rate (revenue and incentives as a percentage of GMV) declining by 20bps. Adjusted EBITDA margin was 1.5% in 2Q24, down from 1.6% in 2Q24. Additionally, total incentives as a percentage of GMV had a slight uptick to 11.3% from 11% in 1Q24.

We try to see how margins performed if we exclude the impact from changes in incentives and take rate. For example, although the adjusted EBITDA margin shrank by 10 bps vs. 1Q24, incentives as a percentage of GMV were up by 30 bps. In addition, the take rate declined by 20 bps. Thus, the margin would have been 50 bps higher if the incentive and take rate ratios were unchanged, all else being equal. We think higher contributions from the Ads business contributed to the margin expansion.

Deliveries margin vs. incentives (Vektor Research)

Mobility

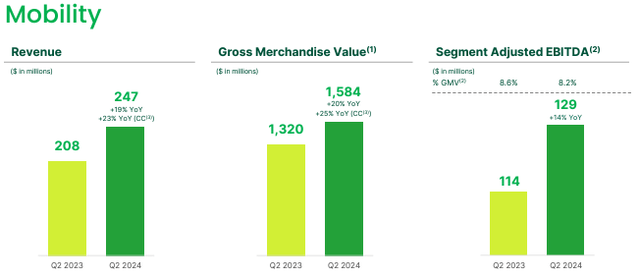

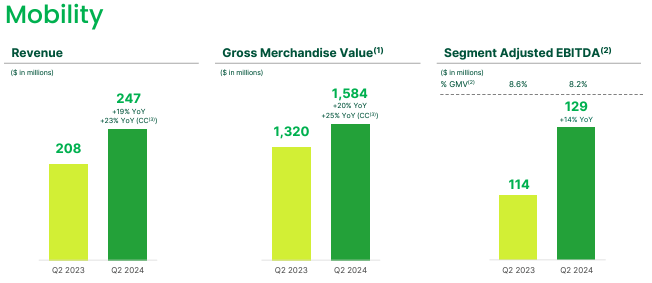

Moving on to the Mobility segment, GMV grew 20% (Y/Y) and 25% on a constant currency basis. But on a quarter-on-quarter basis, the GMV growth decelerated to 2% from 5-8% in the previous quarters as MTUs are nearly at pre-COVID levels.

According to management, Grab Premium generally yields revenue over two times more than do regular ones. But Saver largely contributed to new user acquisitions, as 14% of the Group’s MTUs joined through Saver Mobility. Further, 8% who transact via Saver options also bought food. This is important because, while Mobility sequential growth slowed down, it was able to “cross sell” to other services. Additionally, premium offerings, which were only recently launched, will start kicking in in the back half of the year.

Mobility 2Q24 results (Company)

These initiatives, especially the more affordable options, have expanded the Total Addressable Market (“TAM”):

Saver offers more affordable options alongside our established GrabCar or GrabBike products. And while these products may involve some trade-offs for passengers in the quality of the vehicles or the longer waiting times, they have enabled us to expand our addressable market, all while upholding our core value propositions of safety and reliability.

Revenue was flat quarter-on-quarter but grew 19% (Y/Y) and 23% (Y/Y) excluding foreign exchange impact. The flat sequential growth was primarily because total incentives as a percentage of GMV increased to 8.1% from 7.4% in the previous quarter. Adjusted EBITDA margin came in at 8.1%, down from 8.9% in 1Q24 and 8.6% in 2Q23.

However, this time is a different story. Indeed, incentives as a percentage of GMV advanced by 70 bps on a quarter-on-quarter basis. However, the take rate also increased by 30 bps. Thus, the margin would only have expanded by 40 bps if incentives and the take rate ratio were unchanged from the previous quarter. Management attributed the margin contraction to new product roll-out and product mix.

Mobility margin vs. incentives (Vektor Research)

Financial Service

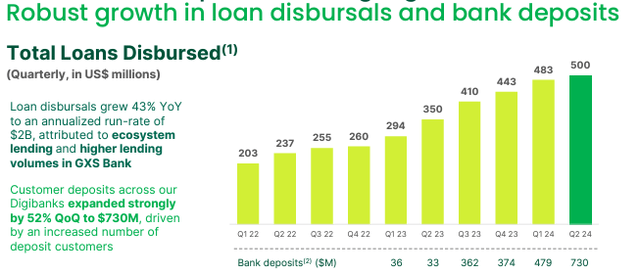

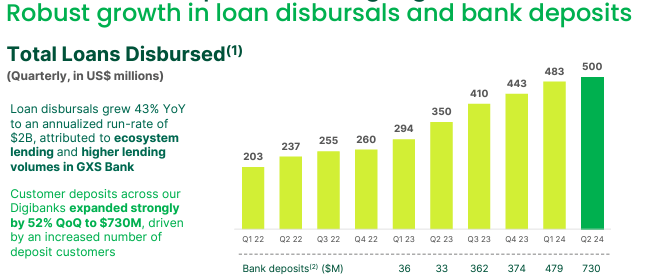

Lastly, total loans disbursed reached $500 million, growing nearly 4% sequentially. The loan portfolio, which represents total loan receivables net of expected credit loss allowance, stood at $397 million vs. $363 million in 1Q24 (+9% Q/Q). The 90-day non-performing loan ratio was stable at 2%.

Meanwhile, bank deposits were recorded at $730 million, increasing 52% (Q/Q) from $479 million in 1Q24. Management attributed the robust growth to increasing GXBank customers in Malaysia. We still expect the Financial Service segment to drive Grab’s growth. GXBank in Malaysia is yet to launch lending products, and GSX Bank in Singapore is also looking to roll out new investment products.

Total loan disbursed and deposits (Company)

Revenue grew 9% (Q/Q) and 54% (Y/Y) or 61% on a constant-currency basis. Adjusted EBITDA losses were $24 million, a sequential decrease of $4 million, consistent with management’s expectation that the peak loss was in 4Q23.

Overall, on-demand GMV grew 5% sequentially and 13% (Y/Y) or 18% excluding foreign exchange headwinds, driven by more affordable options that propelled transactions (+7% Q/Q; +22% Y/Y). But at the same time, higher transactions came at the expense of lower on-demand GMV per MTU, which declined by 2% (Q/Q) and 6% (Y/Y). On a constant-currency basis, the unit economics declined by 1% (Y/Y).

Adjusted EBITDA came in at $64 million, up from $62 million in 1Q24 thanks to reduced corporate costs. The impact of headcount reduction will be more prevalent in the back half of the year since restructuring was done in June last year. Additionally, we witnessed a huge improvement in adjusted free cash flow from a negative $98 million in 1Q24 to a positive $36 million in 2Q24. Yet, free cash flow was still negative when adjusted by share-based compensation.

During the quarter, Grab repurchased 9.6 million shares for $34.6 million. Since the $500 million repurchase program was announced, the company has bought back 40 million shares for $131 million.

In sum, besides Deliveries’ and Fintech’s strong sequential growth despite foreign exchange headwinds, we like Grab’s ability to generate free cash flow during the quarter. We are more positive about Deliveries, given the robust 2Q24 sequential growth. A 6% sequential growth is equal to about 24% year-on-year growth.

We initially believed that future growth would be tepid because people returned to dining onsite. However, Euromonitor suggests that online delivery service is here to stay, with restaurant dining at 60% of the food industry in Asia, significantly down from 79% in 2019.

Higher Incentives in the Near Term?

Let us look at management guidance for the year:

| No. | KPIs | Guidance | 1H24 Results | 2H24 Guidance |

| 1. | Revenue | $2.7-$2.75 million | $1.32 million | $1.38-$1.43 million |

| 2. | Adjusted EBITDA | $250-$270 million | $126 million | $124-$144 million |

| 3. | Adjusted free cash flow | Positive | -$62 million | Over $62 million |

Management’s guidance implied the 2H24 revenue at $1.41 million (mid-point), higher by 7% from 1H24 and 11% from 2H23. The full-year guidance assumes a 3.5% year-on-year foreign exchange headwinds. We think the guidance is slightly conservative and assumes incentives to stay at the current levels.

Why? One possible reason is that heightened competition is at play. While management said this on the 2Q24 earnings call when asked about an increase in incentive spending:

There’s a lot of new launch activity going on in this quarter, not just in Mobility, but also Deliveries, Peter was referring to the omni services that we’ve been launching, as well as Saver there. And then, we’ve got Saver and advanced booking in the Mobility space. So those incentives were largely associated with supporting those launches. The competitive activity is there, but it’s always been there, as I was saying earlier.

So we don’t see any particular intensification of competitive activity. The product mix is a factor.

ByteDance’s TikTok announced it was exploring the idea of “local services,” particularly in dining and tourism, in Indonesia and Thailand. In addition, GoTo is partnering with TikTok to integrate social media with its food delivery service. According to management, GoTo gained market share in its three main offerings: ride-hailing (two and four-wheels) and food delivery. An intensified competition will result in Grab offering more subsidies to protect its market share.

Alternatively, Grab has ramped up its incentives to drive the adoption of its affordable services, which has driven transactions. The importance of having scale is that these costs will be spread over higher transaction volumes, leading to more efficient operations and thus resulting in long-term margin expansions. On the other hand, struggling smaller players will exit the market completely or via consolidations, resulting in less competition.

Features like mapping, hyper batching and just-in-time allocation, they’re all unique to Grab’s and none of our competitors have that and we believe that makes us consistently more reliable as well as more affordable. As well as obviously attracting consumers because of the reliability with the group MTUs now at an all-time high. So it’s very difficult for any local competitors in our — in any of our markets to replicate that strategy because they simply don’t have that scale and the technology to show sustainable profitability in the same way as we are.

Either way, we still expect financial service and Ads businesses to drive Grab’s long-term growth, while affordable options such as Saver will drive on-demand MTUs. However, we think incentives will remain at the current level as Grab is rolling out its affordable services, and heightened competition is on the cards.

Valuation

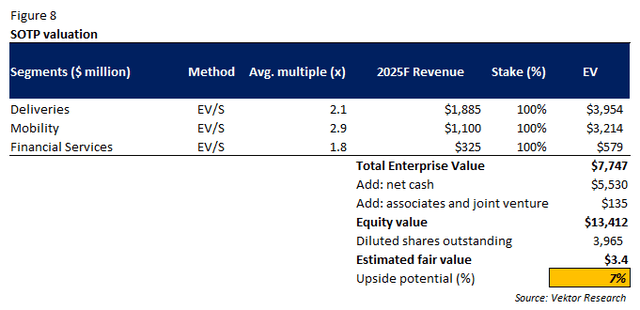

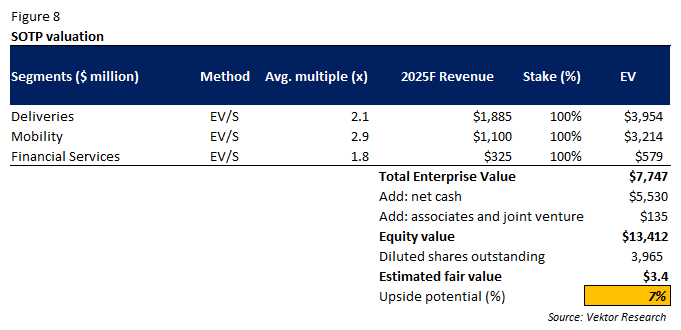

Our sum-of-the-parts valuation method suggests that Grab’s estimated fair value is $3.4 per share (7% upside), down from the previous estimated value of $3.6 per share. This implies a 2.3x 2025F forward EV/Sales.

Overall, we revised the 2025F revenue estimate upward by 4%, driven by a higher estimate of Deliveries GMV. On the contrary, we revised our 2025F revenue estimate for Mobility, as sequential growth appears to be running out of gas following MTUs returning to pre-COVID levels.

SOTP valuation (Vektor Research)

However, global peers’ multiple contractions in the last six months have significantly impacted our fair value estimate via the SOTP method.

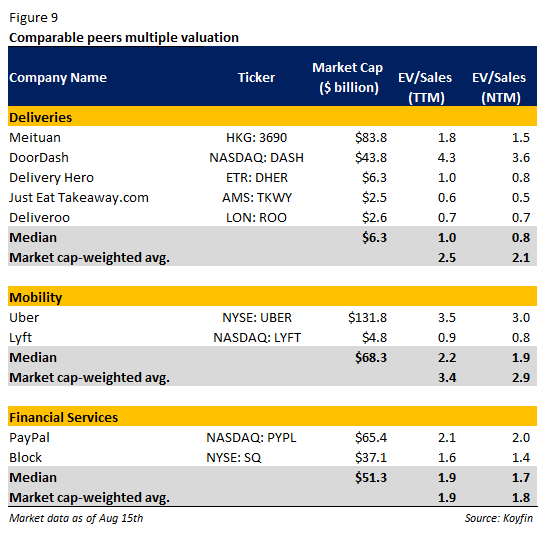

Comparable peers’ valuations (Koyfin, Vektor Research)

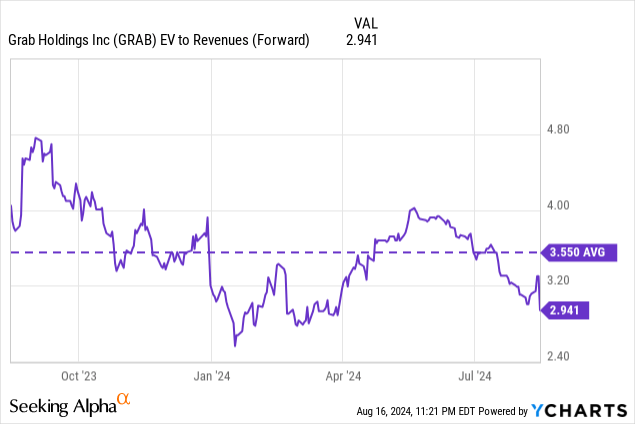

Another way to look is to examine the multiple the stock is currently trading at, and how much growth is baked into the stock. Grab is trading at nearly 3x forward EV/Sales, lower than the 1-year average of 3.6x. The consensus estimate is a 17% annual revenue growth in 2025, lower than our estimate of 19%, driven by robust Deliveries growth and foreign exchange headwinds winding down. Assuming the stock will trade at the same multiple next year, our estimated fair value is $3.9 per share (23% upside potential).

Conclusion

Foreign exchange severely impacted on-demand GMV growth (528 bps year-on-year headwind). Still, Deliveries GMV had robust sequential growth, supported by Saver deliveries and the high-margin Ads business. While Mobility GMV’s sequential growth appears to be running out of gas, Grab succeeded in cross-selling its offerings. Finally, the Financial Service segment demonstrated robust growth.

Our SOTP valuation suggests that Grab’s fair value stands at $3.4 per share (7% upside), down from $3.6 per share, largely driven by global peers’ multiple contractions. Another way to look at is through the current multiple and how much growth is baked into the stock. The stock is now trading at 2.9x forward EV/Sales, assuming a 17% revenue growth in 2025. We estimate revenue to grow by 19% in 2025, driven by Deliveries growth and foreign exchange headwind winding down. Assuming the stock will trade at that multiple, the estimated fair value is $3.9 per share (23% upside).

The recent pullback has provided the stock with a sufficient margin of safety, in our view. Catalysts are rapidly growing the Financial Service and the Ads businesses that will take a bigger proportion of revenue, margin expansions due to scale from affordable services, and foreign exchange headwinds winding down. Risks to our call are strengthening USD and heightened competition that prompted Grab to increase incentives. Upgrade from HOLD to BUY. If you have any questions, please do not hesitate to comment below.

Source link