After Surging, Mayville Engineering Company Deserves More Upside (NYSE:MEC)

Monty Rakusen

It’s always great when an investment opportunity significantly exceeds your expectations over a short window of time. A great example of this can be seen by looking at Mayville Engineering Company (NYSE:MEC), a company that is engaged in the production and sale of components catering to certain end markets like the power sports market, the agricultural industry, the construction space, and both the heavy and medium duty commercial vehicle market. To many, this might not seem like all that exciting a space to play in. However, I find that some of the most ‘boring’ companies on the planet tend to be the most intriguing.

They also, from my experience, offer some of the best upside if you can get in when the time is right. As an example, back in early May of this year, I upgraded Mayville Engineering Company from a ‘buy’ to a ‘strong buy’. This came after shares fell 10.2% from the prior time I had written about the company in February of 2023 through that present moment. But the fact of the matter is that shares have gotten very cheap and revenue continued to grow. Sure, the company did experience some weakness from a profit and cash flow perspective. But this was not enough to offset the positives that I was looking at.

Since upgrading the stock, things have gone exceptionally well. Shares are up a remarkable 37.5% at a time when the S&P 500 is up by only 5.7%. You might think that this would cause me to finally downgrade the stock to a ‘buy’ again. After all, shares can only justify so much upside. And truly, that was my initial thought looking at the numbers again. But when you consider how cheap shares remain and the trajectory that management has the company on, I do think that keeping it rated a ‘strong buy’ is perfectly logical.

Optimism is still justified

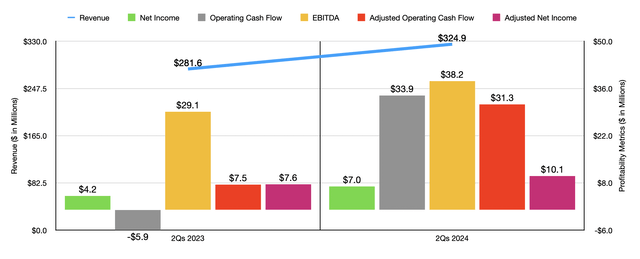

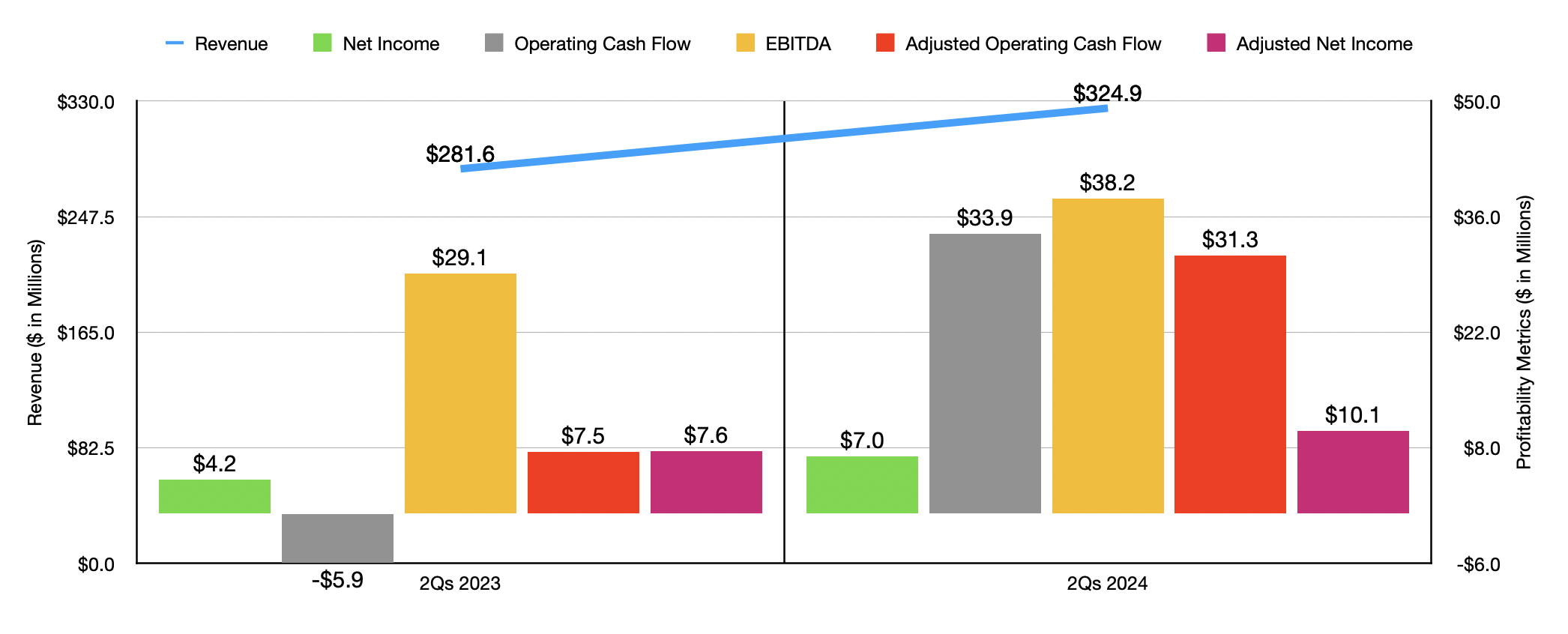

When I last wrote about Mayville Engineering Company a few months ago, we only had data covering through the end of the 2023 fiscal year. In fact, at that time, we were on the cusp of the business announcing results for the first quarter of its 2024 fiscal year. Today, data now extends through the second quarter of 2024. And during this time, things have gone incredibly well. Revenue for the first half of 2024 totaled $324.9 million. That’s an increase of 15.4% over the $281.6 million generated one year earlier. To be clear, some of this growth was driven by organic sales volumes within the commercial vehicle, construction and access, and power sports end markets. But according to management, a lot of this increase was attributable to the company’s acquisition of MSA in the third quarter of the 2023 fiscal year.

Author – SEC EDGAR Data

Regardless of the cause, the increase in revenue brought with it higher profits and cash flows. Net income nearly doubled from $4.2 million to $7 million. On an adjusted basis, net profits expanded from $7.6 million to $10.1 million. In addition to benefiting from higher sales volumes, the aforementioned acquisition, and commercial pricing actions, the company also benefited from cost cutting initiatives that management had put into place. As a result, other profitability metrics moved higher as well. Operating cash flow in the first half of 20/23 was negative to the tune of $5.9 million. This year, it was positive by $33.9 million. On an adjusted basis, the metric grew from $7.5 million to $31.3 million. Even EBITDA was pushed higher, rising from $29.1 million to $38.2 million.

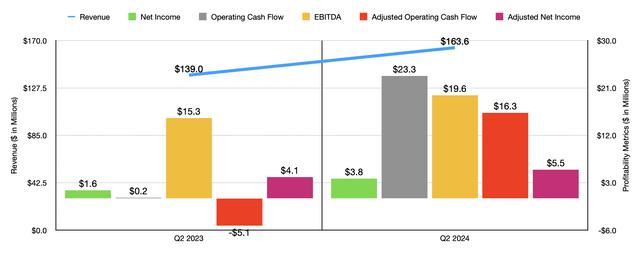

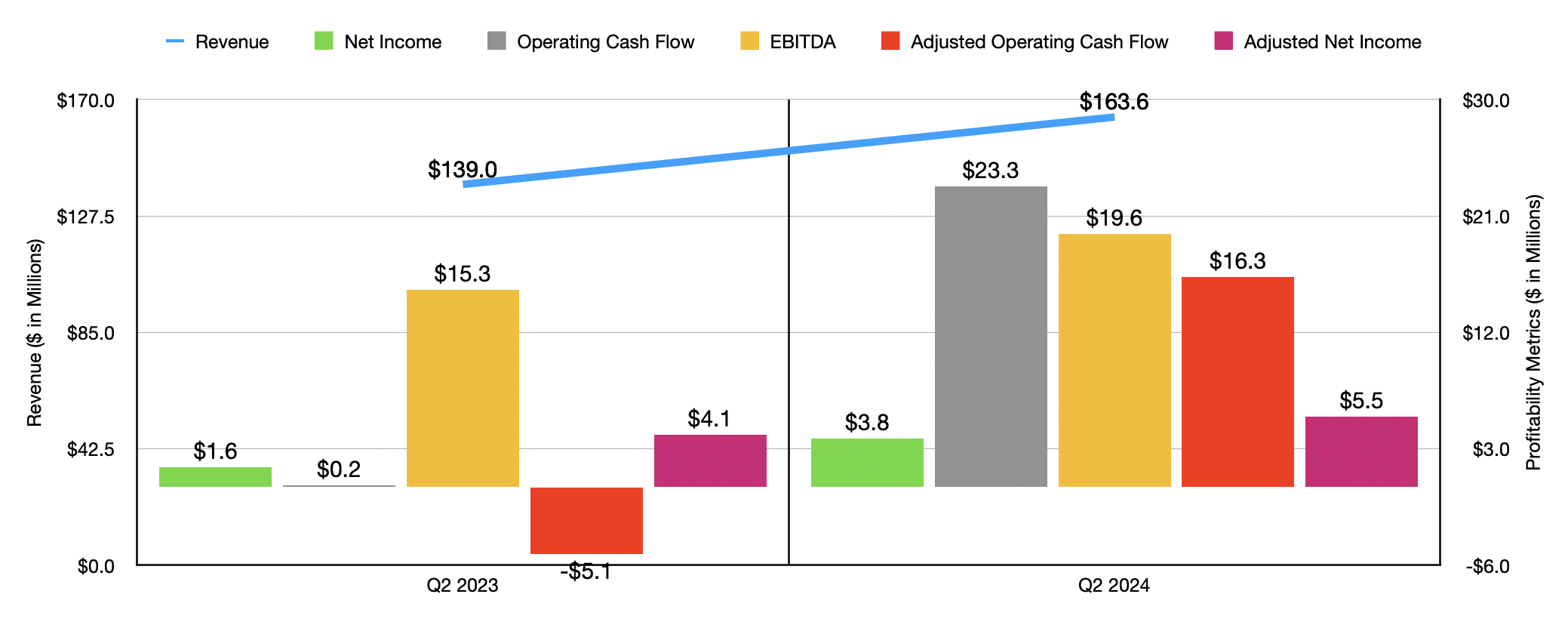

When it comes to the second quarter of 2024 on its own, the picture was particularly pleasant. Revenue was 17.7% higher year over year at $163.6 million compared to the $139 million reported one year earlier. The same factors that contributed to growth for the first half of this year relative to the same time last year were responsible in the second quarter for the company. And when it came to profitability, every metric improved without exception. Net income grew from $1.6 million to $3.8 million. On an adjusted basis, it expanded from $4.1 million to $5.5 million. Operating cash flow soared from $0.2 million to $23.3 million. And if we adjust for changes in working capital, we get an improvement from negative $5.1 million to positive $16.3 million. And lastly, EBITDA for the company expanded from $15.3 million to $19.6 million.

Author – SEC EDGAR Data

To be honest with you, there’s nothing really substantive to complain about here. Now when it comes to the 2024 fiscal year in its entirety, management expects revenue of between $620 million and $640 million. At the midpoint, that would be 7.1% greater than what the company achieved in 2023. The firm also anticipates EBITDA of between $72 million and $76 million. If we assume that the midpoint here is indicative of the growth that adjusted operating cash flow will receive on a year-over-year basis, then we should anticipate a reading for it for this year of $38.5 million.

Author – SEC EDGAR Data

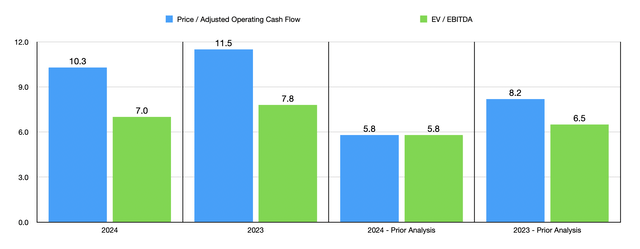

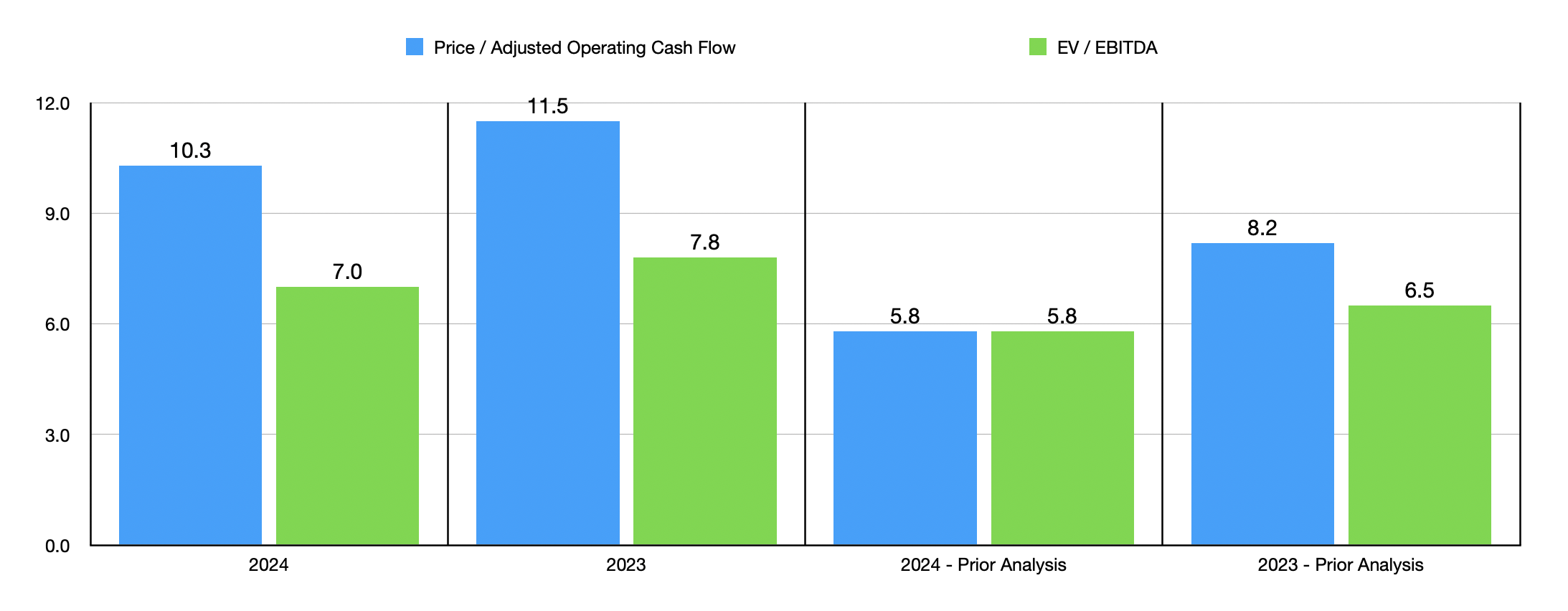

With these figures, you can see how shares are valued on a forward basis for this year in the chart above and how they are valued using historical figures from 2023. For context, the chart also shows how shares were valued for both of those years when I last wrote about the company earlier this year. Clearly, this is a significant increase. On a relative basis, the stock is also attractively priced. If we use the 2024 estimates, then, compared to five similar firms shown in the table below, Mayville Engineering Company ended up being cheaper than any of these five firms on both a price to operating cash flow basis and on an EV to EBITDA basis.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Mayville Engineering Company | 10.3 | 7.0 |

| Mueller Industries (MLI) | 11.1 | 8.2 |

| Crane Company (CR) | 38.3 | 22.9 |

| Parker-Hannifin (PH) | 22.1 | 16.5 |

| Enpro (NPO) | 17.8 | 16.1 |

| Standex International (SXI) | 21.6 | 15.4 |

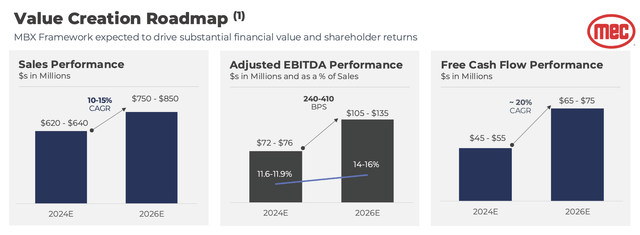

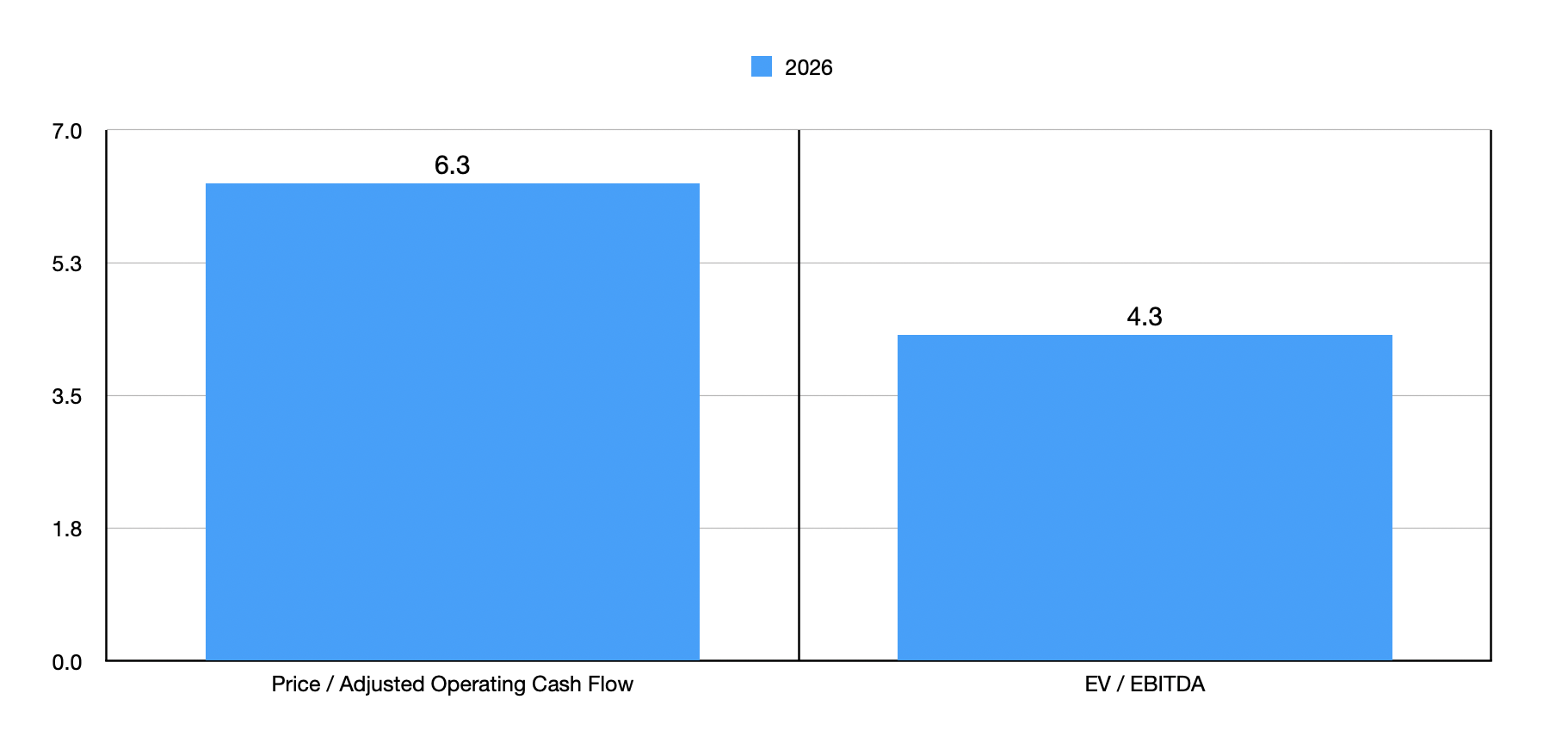

This is great to see. And I see no reason why shares should not be rated at least a ‘buy’ based on valuation. But the real reason why I’ve decided to keep it rated a ‘strong buy’ relates to management’s forecasts for the future. In the image below, you can see that management is forecasting annualized revenue of between $750 million and $850 million for the 2026 fiscal year. They also expect EBITDA of between $105 million and $135 million for a midpoint of $120 million. Using that midpoint, we should anticipate adjusted operating cash flow of about $62.4 million.

Mayville Engineering Company

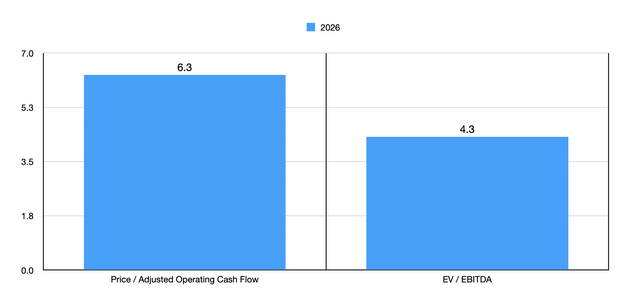

In the chart below, you can see just how cheap shares are on a forward basis for the 2026 fiscal year. But that’s not the only step that we need to take here to see what kind of upside is justified. If we make the assumption that the stock should trade at the same multiples it’s currently trading at for the 2024 fiscal year, then we should anticipate a market capitalization, using the price to adjusted operating cash flow approach, of $642.7 million. Over the span of approximately two-and-a-half years, that gets us an annualized return for shareholders of 21.4%. It’s a bit trickier when we use the EV to EBITDA approach. I say this because we don’t know how much leverage management will take on in order to achieve its growth. But if we assume that net debt remains unchanged, the EV to EBITDA multiple today would translate to a future enterprise value for the company of $840 million. Stripping out net debt of $121.7 million, we get an annualized increase over the next two-and-a-half years of 26.9%. In both of these cases, we end up with hypothetical upside that is drastically higher than the 10% to 12% that the market historically averages.

Author – SEC EDGAR Data

Takeaway

To be perfectly honest with you, the recent financial performance achieved by Mayville Engineering Company was surprising even to me. Although I rated the company a ‘strong buy’ when I last wrote about it earlier this year, I didn’t think that we would see such rapid and significant appreciation in its share price. I came into this expecting to find some reason to downgrade the stock. But the more that I looked at the numbers, the more I realized that further material upside is probably on the market. Given these factors, I have no problem keeping the company rated a ‘strong buy’ for now.

Source link