RLI Corp.: A Reliable Dividend Champion (NYSE:RLI)

baona/iStock via Getty Images

Executive Summary

RLI Corp. (NYSE:RLI) is a member of the esteemed “Dividend Insurance Champion” club, alongside Aflac (AFL), Chubb (CB), Cincinnati Financial (CINF), and Old Republic (ORI). Having recently revisited Old Republic’s business model, profitability, and valuation, I decided to review RLI Corp. as well, since my last article on this insurance carrier was one year ago.

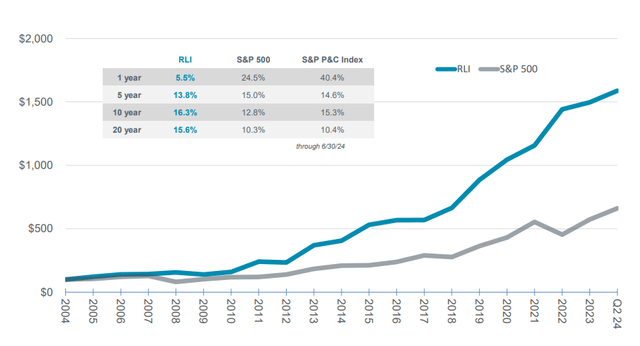

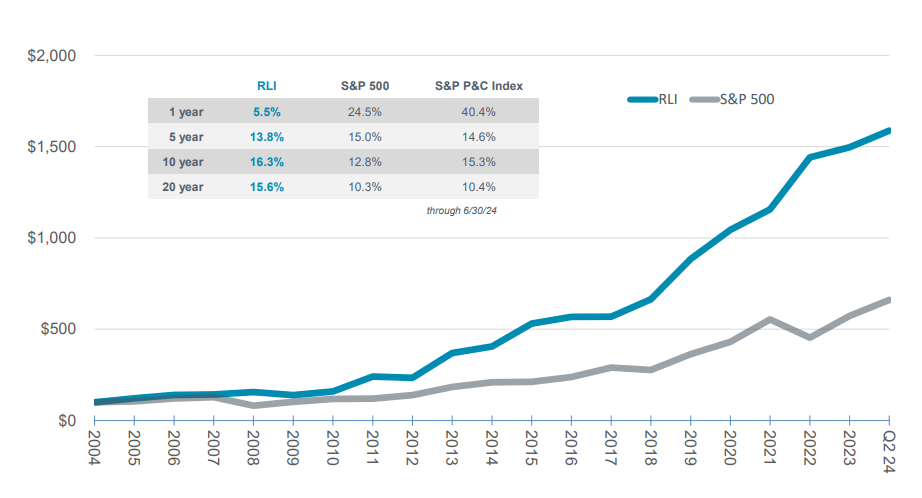

Despite its low dividend yield (below 1% excluding the special dividend distribution), RLI is highly regarded by investors for its consistent dividend increases over the past 49 years. Additionally, the stock has outperformed the S&P 500 in total return over the last two decades.

Q2 2024 Presentation – RLI Corp.

The shareholder returns validate the RLI story, which focuses on several pillars: prioritizing underwriting margin over premium growth at any cost, maintaining a steady investment portfolio with a highly rated bond component, and complementing it with active and passive equities, resulting in prudent but consistent gradual dividend increases.

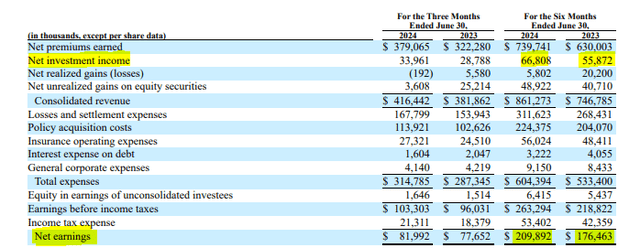

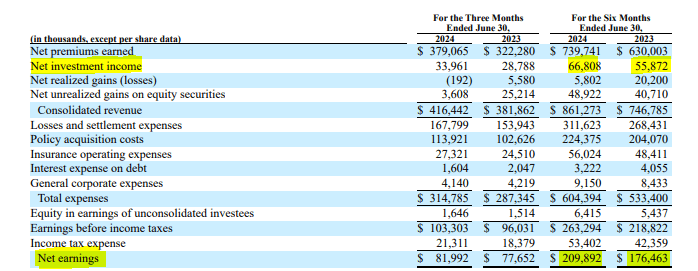

The recently released quarterly results once again showcased the company’s strong position in the U.S. property and casualty market. Year-to-date income increased by approximately $33 million compared to the previous year, benefiting from higher investment income coupled with steady underwriting income.

Q2 2024 Report – RLI Corp.

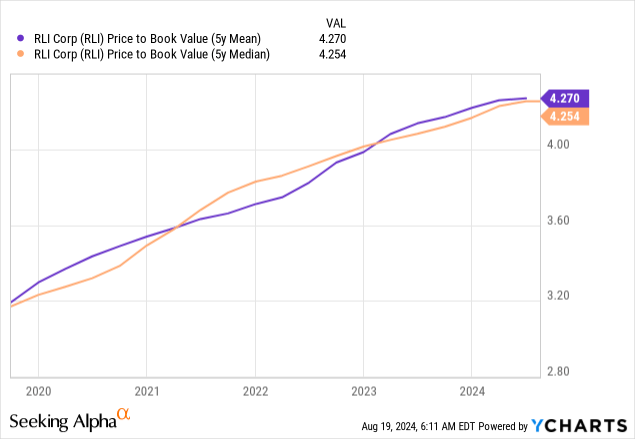

Despite the resilience of underwriting margins over the cycle and the growth in investment income driven by increased investment yield, the current valuation of 4.3 times book value suggests that the stock is priced with no safety margin.

Steady Underwriting Results

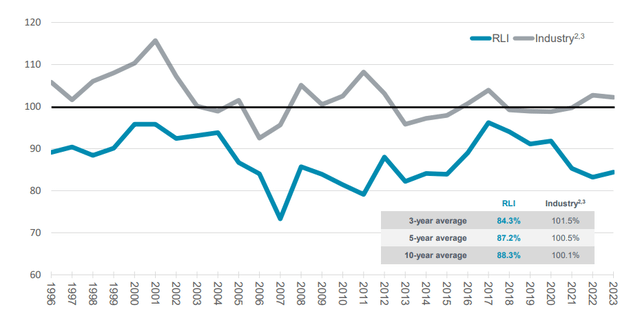

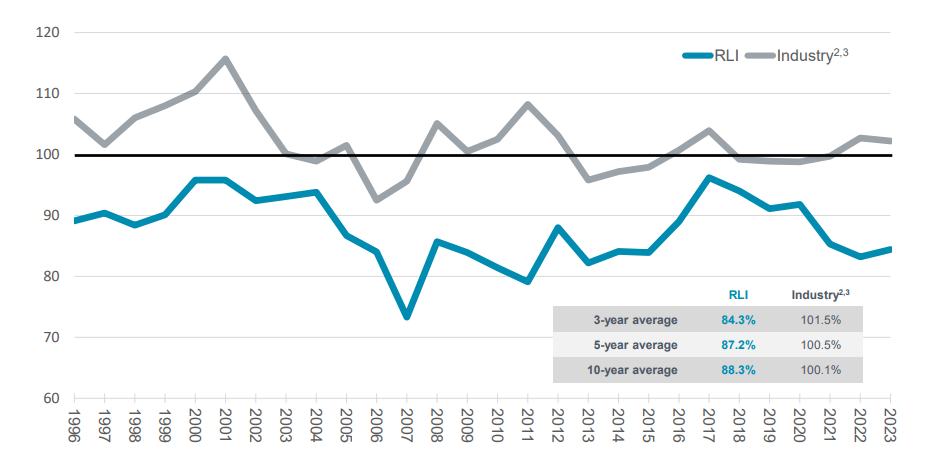

RLI has proven to be a resilient and outperforming insurer, offering property, casualty, and surety insurance coverages. Over the last 29 years, RLI has maintained a combined ratio below 100, surpassing the industry average by an average of 12 points over the past decade.

Q2 2024 Presentation – RLI Corp.

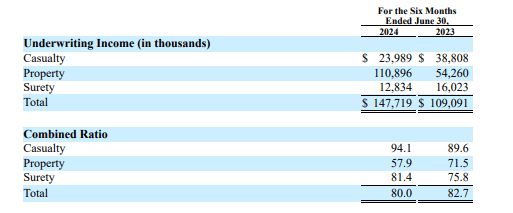

During the first six months of the year, RLI recorded an underwriting income of $147.7 million, resulting in a combined ratio of 80%, marking a year-over-year improvement of 2.7 points.

Q2 2024 Report – RLI Corp.

The three lines of business contributed to the underwriting income, all delivering a combined ratio below 100%. The largest earnings contributor was the property segment, which delivered an impressive 57.9% combined ratio on a year-to-date basis, generating $110.9 million in underwriting income.

The higher underwriting gain from the property insurance segment resulted from larger releases on prior years’ loss reserves, and low attritional non-catastrophe losses, which more than offset the impact of higher storm losses. Furthermore, the segment’s expense ratio decreased to 29.8% in 2024 from 36.0% in the prior year, as the growth in the earned premium base exceeded the growth in expenses. Additionally, the expense ratio benefited from an increase in the expense override the company earns for writing business on behalf of other carriers.

The gross written premium of the property segment grew by 6% in the second quarter, led by the marine insurance division, which grew by 20%, including a 5% rate increase. At the net level, premiums grew by 32% during the second quarter. On a year-to-date basis, the net of reinsurance topline of the property segment increased by 38%, driven by rate increases, new opportunities in the marine insurance business, and reduced competitors’ appetite for Hawaii homeowner coverages, allowing the other property insurance business to grow by 4%.

The casualty insurance segment combined a 12% year-to-date net premium increase with a year-to-date combined ratio of 94.1%, resulting in an underwriting income of approximately $24 million, a reduction of around $14.8 million from the same period last year. Lower levels of reserve releases on prior accident years contributed to the higher loss ratio in 2024, while the expense ratio remained almost flat at 37.4%, with a 0.1-point increase from the same period last year.

The surety insurance business also experienced reduced underwriting income due to a higher combined ratio. The combined ratio for the surety segment totaled 81.4% for the first six months of 2024, compared to 75.8% for the same period in 2023. The segment’s loss ratio was 9.2% in 2024, up from 9.0% in 2023. The expense ratio was 72.2%, up from 66.8% in the prior year. The impact of the reinsurance reinstatement premium on the earned premium base increased the loss ratio by 0.3 points and the expense ratio by 2.0 points. Additionally, the increase in the expense ratio resulted from continued investments in technology and personnel to support growth and improve customer experiences.

Despite reduced underwriting margins in the surety and casualty insurance segments, RLI Corp. is well-positioned to achieve steady underwriting results for 2024, as its insurance product portfolio remains healthy, benefiting from rate increases and underwriting expertise.

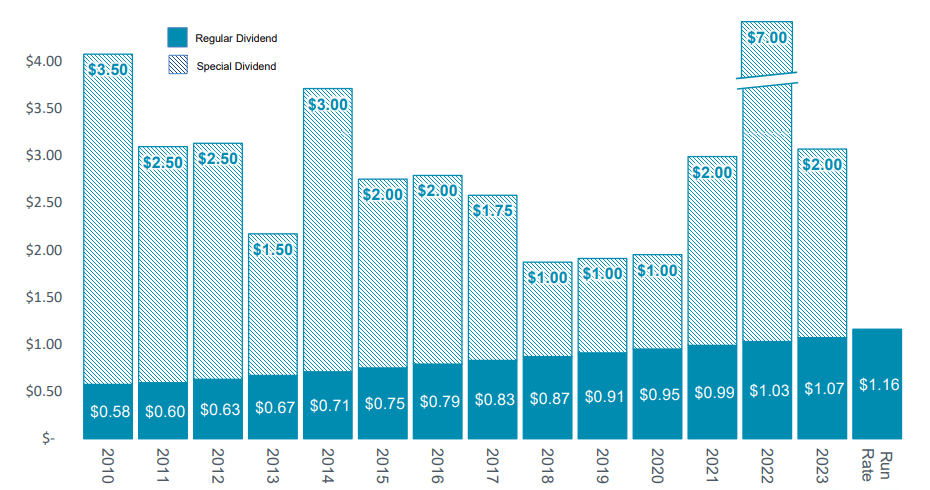

Consistent Cash Dividends Paired With Annual Special Dividends

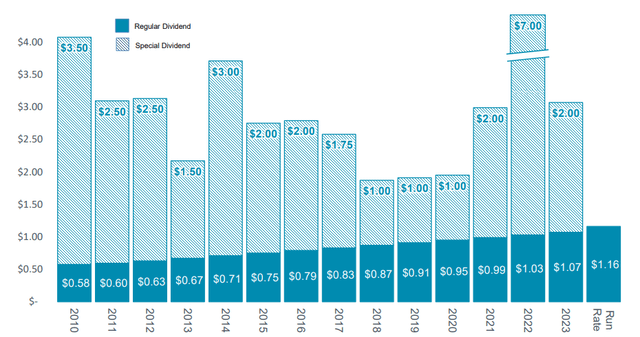

The company is recognized as one of the dividend aristocrats due to its long track record of dividend increases, and it also declares annual special dividends to redistribute excess capital to shareholders.

In 2022, the company distributed a special dividend of $7.0 per share, made possible by the sale of its minority interest in Maui Jim. In 2023, the special dividend returned to its pre-2022 level, with the company declaring a $2 per share special dividend.

Q2 2024 Presentation – RLI Corp.

RLI has a distinguished track record of sharing success with shareholders: 49 straight years of dividend increases, a 5% growth rate over the last 10 years, and 14 years of special dividends. To put it simply, the company serves its loyal shareholders well.

Valuation

RLI’s shareholder equity amounts to $1.58 billion, compared to a market capitalization of approximately $6.85 billion. This results in a P/B ratio of around 4.3, close to its 5-year mean and median price-to-book value of about 4.2 to 4.3.

In other words, RLI Corp. appears to be fairly valued compared to its 5-year average. However, peers typically trade at multiples ranging from 1.5 to 2.5. This high valuation is driven by several factors:

- A best-in-class combined ratio within the property and casualty insurance industry. Over the past decade, the combined ratio has consistently remained below 96.4%, with a 10-year average of 88.3%.

- Consistent dividend increases for 49 consecutive years.

- A positive perception of the company among investors, viewing RLI as a SWAN (Sleep Well At Night) stock.

Despite its impressive financial performance and underwriting expertise, which results in steady underwriting gains coupled with gradually higher investment income, I consider RLI to be valued at a fair price, with no safety margin.

Final Thoughts

Although RLI is a highly profitable and well-managed insurance company, the current valuation appears too high (or at least too high without a safety margin) to start investing in the company. However, current shareholders, whether they are dividend seekers or not, who acquired RLI’s stocks at a lower price may continue enjoying the gradual dividend increases coupled with special dividend distributions.

Source link