BILL Holdings: Stock Looks Unattractive In The Near-Term (NYSE:BILL)

Jennifer Miranda

Investment action

I recommended a hold rating for Bill.com (NYSE:BILL) when I wrote about it in May, as I was not convinced that the business is turning around, despite the very early positive signs. Based on my current outlook and analysis, I recommend a hold rating. My key update to my thesis is that BILL’s near-term outlook (both revenue and adj EBITDA margin) remains poor and uncertain. Until BILL shows evidence that its investments are working, with tangible improvement in various key metrics, I don’t think the stock is attractive.

Review

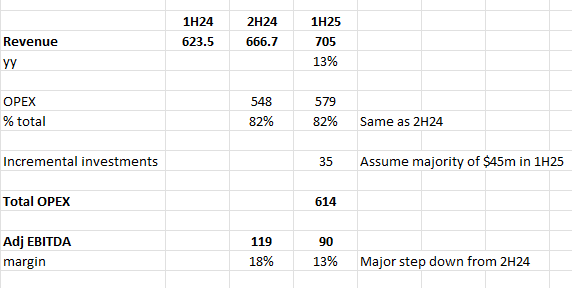

BILL reported 4Q24 earnings earlier this week, with revenue seeing a total of $344 million, beating consensus estimates of $329 million, implying a y/y growth of 16%. Both core revenue and interest on funds held for customers grew by 16%. Gross margin compressed by ~170 bps y/y, resulting in gross profit growth slower than the top line (14%). However, the leaner cost structure led to an adj. EBITDA margin expansion of 310bps y/y to 17.4%.

Based on my review, BILL 4Q24 results were pretty mixed, with positives and negatives. On the positive end, BILL showed further signs of stabilization in its core operating metrics. To highlight a few:

- BILL managed to significantly improve customer net adds for its core module, adding 11.3k customers in 4Q24 vs. 4.9k churn in 3Q24 and 3.1k adds in 4Q23.

- Core BILL offering TPV grew 9% in the quarter, the same as 3Q24;

- Core organic take rate saw 14.8 bps vs. 15 bps in 3Q24;

- All the above led to core revenue-sustaining high-teens revenue growth (16% in 4Q24 vs. 17% in 3Q24).

This is really good if we consider the weak macro environment that is still putting a lot of pressure on SMEs. Based on management first-hand data, they also called out stabilization in the macro environment and, notably, strong momentum with the recent product initiatives and go-to-market changes. With this optimism, management guided FY25 core revenue growth of 13–16% y/y growth and >20% growth in FY26.

However, I don’t think investors should celebrate early. One main assumption that management made was that the core take rate would accelerate in 2H25, which is expected to continue into FY26. In my opinion, this is hard to underwrite because management is also guiding rates to sequentially decline in the near term. This basically becomes a macro bet (hoping it will get better), and given how the macro situation is (weak labor market, rates still high, and both consumer and small business indexes still weak), I think it is going to be hard for any investors to take a convicted view today. Another major uncertain event that could be a major headline risk is how the V and MA-related litigation settlements will play out. As of the latest update, it seems like the proposed settlement will get rejected, and if it does get rejected or prolonged further, it would further taper investors expectations of a take rate acceleration (as interchange fees are not lowered).

I’d say that first of all getting to the 20% growth that we talked about, that’s obviously going to be a progression, right. We’re going to make progress in the second half of ’25 and we’ll continue that through FY26. We are assuming better expansion of monetization in ’26 than in ’25. But that’s not the sole driver of our belief that 20% is in range for ’26. We obviously have much higher both volume and revenue growth on our Spend and Expense product. We talked about the proliferation of card payments starting to happen within the BILL ecosystem that will provide incremental growth as well. 4Q24 call

Author’s work

The other development that made investing in BILL unattractive was the heavy step-up in investments, which is going to weigh on 1H24 adj EBITDA margins. Management was guided to invest an incremental $45 million (mostly in 1H25), primarily in R&D and go-to-market. By my math, this could easily suggest a ~500bps sequential stepdown from 2H24, which will be a major headline risk to the stock as some investors will be concerned that BILL has pivoted back to gross-focused vs. profitable-growth-focused.

Moreover, the four main investment areas highlighted are not easy “fixes.” To recap, the four investment areas include: (1) enhancing the value proposition of existing solutions; (2) expanding go-to-market strategies for suppliers; (3) deepening accounting partner relationships; and (4) expanding BILL’s ecosystem. All of these are major strategic focuses that may take more time than expected. And if you look at each of them, the key “enabler” is to have boots on the ground to meet and talk to each counterparty—to gather information, understand existing problems, and negotiate terms (which is time-consuming). If BILL cannot find the right talents to do so, the plans may get delayed, and this will impact the timing of growth acceleration (and perhaps require more investments that further weigh on margins).

This is a long quote from the 4Q24 call, but I think readers will have a better understanding of the underlying requirements for these 4 investment areas (and how much time needed):

We’re going to expand card uses across the platform. We’re going to give folks more opportunities to leverage the card. And then the next thing, the second thing I would say is that we’re going to augment the experience and go to market for suppliers. What we started doing again halfway through the year was having dedicated teams that talk to suppliers that have significant volume on the platform. We’ve learned a ton. There’s a lot of opportunity for us to create more value for them, better reconciliation, more automation, even leveraging AI across the experience that they have. And that’s what we’re hearing and that’s what we’re developing and that’s where we want to invest. And then on the third thing that we’re going to invest in, it’s going to be deepening our accounting relationships. We have defined an entirely new line of business for accountants. We’ve worked with CPA.com and AICPA to create client advisory services, cast practices, and you heard a quote from Aprio and Ambra. They’re talking about how they started 14 years ago with no customers on the BILL platform and now have over 500. But when you have 500 customers, how you manage and support those customers becomes a lot more challenging. And so we have an opportunity to actually provide cash flow insights and strategic advisory services through the platform we have. We have an opportunity to create efficiency for the accounts and how they manage their clients. And we have an opportunity to create better customer experiences around multi-entities since many of their clients have that. And so we’re investing behind that. And the fourth and final area of investment is driving expansion of our ecosystem. 4Q24 call

Valuation

Author’s work

Hence, given the poor near-term core take rate outlook (and uncertainty in 2H25 acceleration), the higher levels of investments, and, most importantly, the uncertain macro backdrop, I think BILL is an unattractive investment in the near term. I don’t see the stock working (going upwards) until it shows investors that they are seeing the benefits of these investments: inflection in the take rate; acceleration in customer adds; and an improved TPV growth trend.

Given this outlook, I think BILL will at best continue to trade at this valuation of 3x forward revenue, in line with where other payment peers are trading. If you look at the peer table above, you will notice that BILL’s 1-year forward growth is much lower than peers, and despite this, it trades in line with peers. The reason is because BILL’s T+2 growth is in line with peers, which means if BILL does not show evidence that all its investments are working, valuation may get further pressured in the near term.

Final thoughts

My recommendation is a hold rating. The 4Q24 earnings report presented a mixed picture. While core revenue growth remained stable and management expressed optimism for future growth, I am concerned about the near-term performance. In particular, core take rate and EBITDA margins are going to be under pressure, and the investments may take longer to yield results. Hence, my view is that the stock is unlikely to move upwards until tangible results can be seen.

Source link