Consumer Behavior Driving Costco’s Results: Worth Half Its Current Value (NASDAQ:COST)

artran/iStock Editorial via Getty Images

Investment Thesis

Costco Wholesale Corporation (NASDAQ:COST) is an operator of discount stores known as membership wholesale clubs. I became interested in Costco for the first time after Charlie Munger showed interest in the company and spoke very highly about their operations. He was the second-largest individual shareholder after former CEO, Craig Jelinek. Even with the incredible moat and growth of COST, I thought Charlie paid a very high multiple for COST. Over the past 18 years, the company has been able to grow at a rather impressive rate, but I think this will come to an end, and the multiple is not justifiable. A company with the size of COST can grow at those rates up to a point – and that point has already arrived.

COST is quite an expensive company. Sell-side analysts expect the company to make a little over $16 a share in EPS this year and trades for over $800 per share – that’s 50x this year’s earnings. The company has always had an immense PE multiple, even Charlie paid a rather expensive multiple, but it has worked very well for him so far. However, as per all my valuation models below, COST should not be trading in the $800 range. I don’t think paying a high multiple is justifiable when the company has not been able to grow its operating income in a long time.

COST operates in an industry characterized by low single-digit margins. They do not make money in the price, they make money in the quantity, if we look at it from an economic perspective. The company has been able to operate in the 3%-4% EBIT margins for a long time but has not been able to increase it very much to the 6% territory, and I don’t think they will any time soon, unless they start increasing the prices of its products and services. This might prompt a decline in customers, as it will be more costly to shop at Costco.

The company recently announced that it will increase its yearly membership fees for the first time in 7 years. Although this would bring additional cash into the top line, this would not have any major impact in growth as membership fees only account for 2% of the total revenue. In my opinion, management is anticipating a potential slowdown in shopping, so they have increased membership fees in an effort to generate additional revenue.

COST – FY23

The Consumer

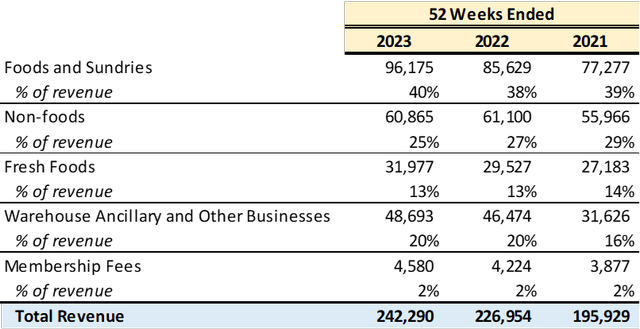

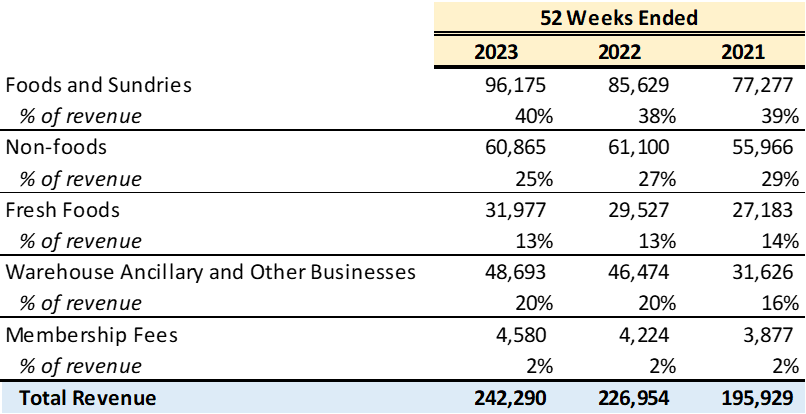

Costco customers are becoming more and more “value-conscious,” which has resulted in a slowdown in sales of expensive items (where demand is very elastic) like high-end televisions, computers, etc. As per the above revenue breakdown, non-food item sales have slowed down since 2021, and I expect these to keep declining as a percentage of total revenue. It is very true that COST has loyal customers all over the US and Canada (that account for more than 80% of its revenues), however, there are better options to shop out there, and consumers are looking to get more value out of the products they buy.

Not to mention, COST is not well positioned in online shopping (e-commerce represented approximately 6% of total net sales in 2023), whereas competitors such as Walmart and Amazon are dominating the online shopping market and offer great alternative prices. In the next couple of years, we will see a slowdown in traditional shopping that will affect Costco stores.

Ali Hortaçsu and Chad Syverson put together a research paper called ‘The Ongoing Evolution of US Retail: A Format Tug-of-War‘ that basically highlights the changes in the way shopping is conducted over the past 15 years and how that looks into the future. Given the slowdown in traditional shopping (as per the graph in page 99), the multiple of COST is not justifiable. I think the company is a SELL and worth about half its current value, around $450 per share.

Valuation

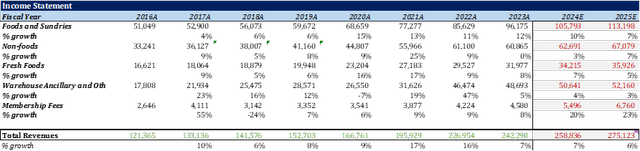

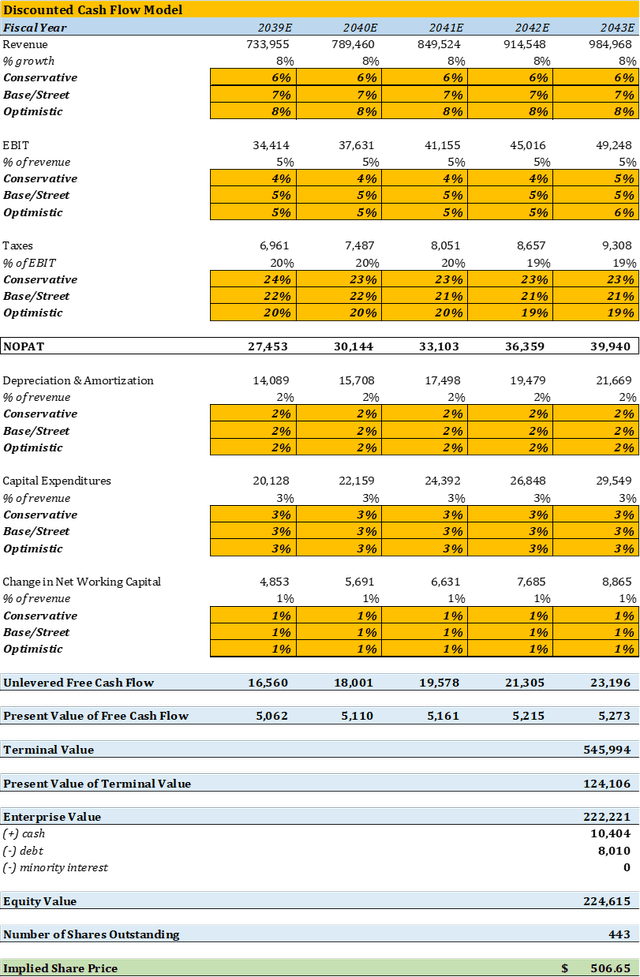

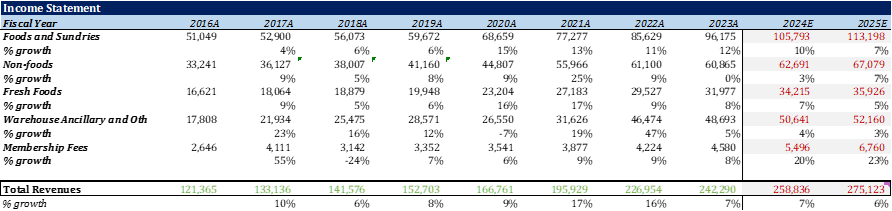

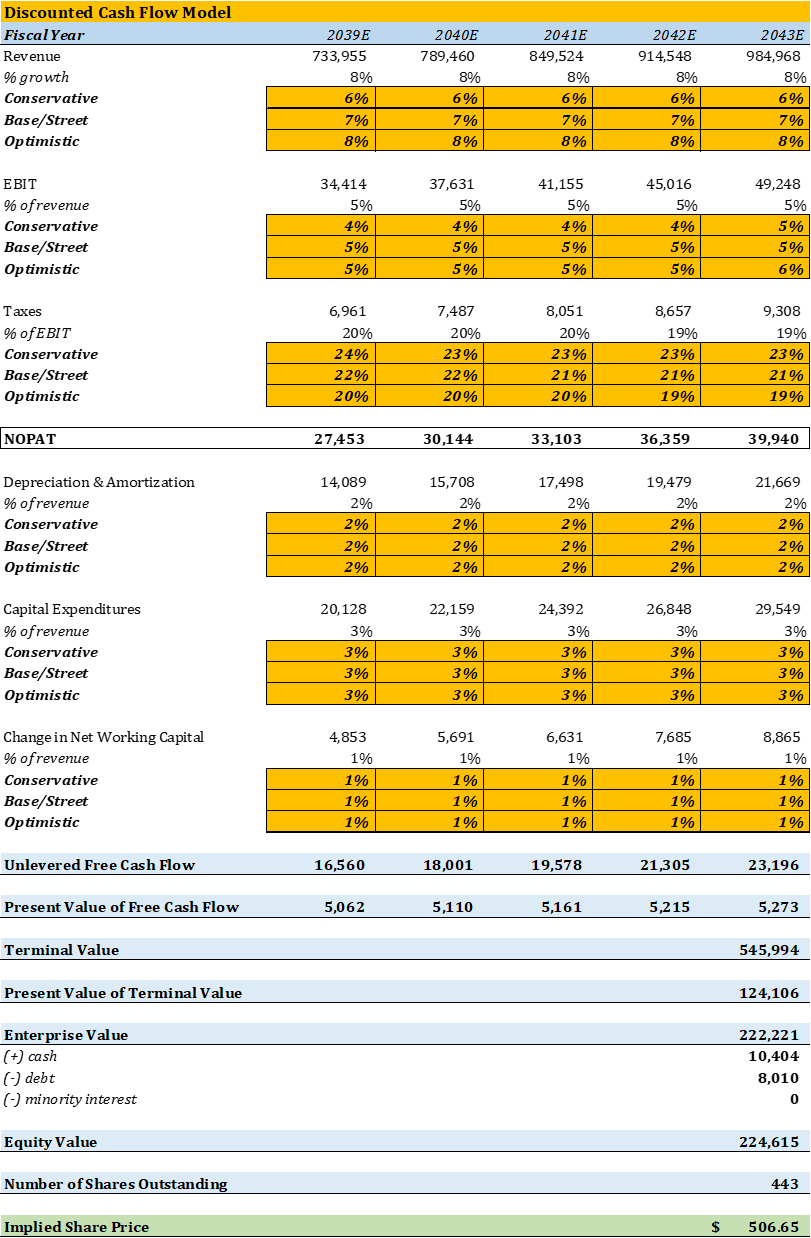

My 20-year DCF model discounts COST’s future cash flows to come up with a company valuation. Using the below assumptions for 2024 onwards, I expect the company to increase its revenues to almost a trillion dollars by 2043 (if the company grows its revenues 7% every year). COST is a company with low single-digit EBIT margins. I expect the company to achieve a plateau margin of 5% by the end of 2043. Taxes were kept at 21% over time, as per the US corporate tax rate. COST has a current market capitalization of $368.3B ($830.74/share), trading at a premium to my DCF model’s implied equity value of $224.6B, or $506.65/share.

Analyst Assumptions, Giacomo Bocanegra Analyst Assumptions, Giacomo Bocanegra

Moreover, COST trades at a premium to its peers – Walmart (WMT), Target (TGT), Kroger (KR), Dollar General (DG), Albertsons (ACI). As per my trading comparable analysis, COST should be trading in the $400 neighborhood at the current revenue multiple and between $250 and $350 at EBIT and net income levels. As noted before, the company operates in an industry characterized by very low and consistent margins. COST does not have the growth and operating margins of a technology company, so it should not be trading at a tech multiple.

Analyst Assumptions, Giacomo Bocanegra

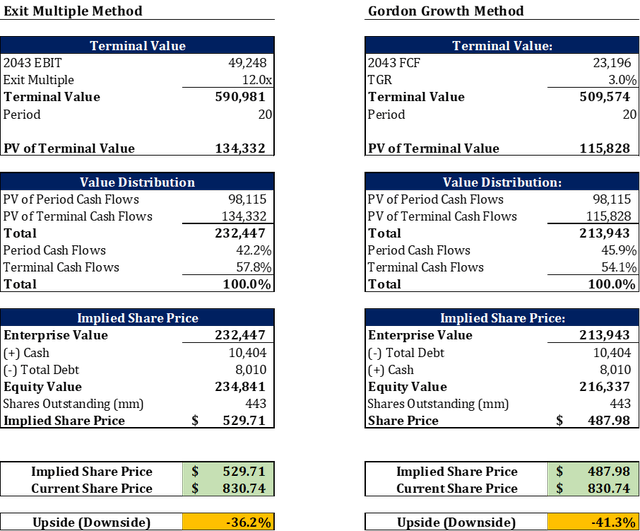

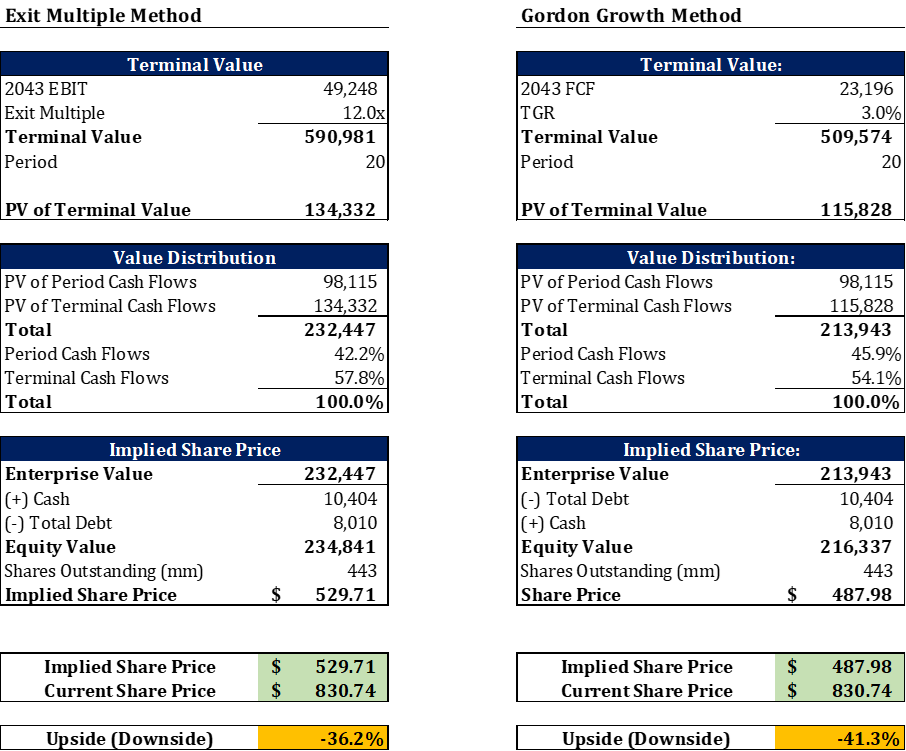

My Exit Multiple Method and Gordon Growth Method, also show downsides to the stock. Using a 12x exit multiple assumption (which is the industry average), we see an equity value of $234.8B, or $529.71/share, 36.2% lower than $830.74. The implied share price will show even a wider downside if a lower exit multiple is exercised. The Gordon Growth Model, on the other hand, shows an equity value of $216.3B or $487.98/share, implying a downside of 41.3% from current levels.

Analyst Assumptions, Giacomo Bocanegra

Potential Risks

The short interest for COST stock is 1.6%, which shows strength for a feeling towards the bull side. There could be a potential risk as investors are leaning more towards the bull side and won’t be willing to sell. Most of the shares outstanding are held by huge passive asset managers (Fidelity, Northern Trust, Wells Fargo); therefore, there will be less interest in selling a large portion of the stock and this could not drive down the price of COST to my price target of $450 per share.

From an economics perspective, there should be a decrease in membership subscribers as yearly fees increase. The same happens for demand-elastic products that Costco sells. However, the economics theory might not always be the right case.

Conclusion

Costco was one of the best consumer staples distribution and retail performers; it has tripled in price since 2019 and did very well during COVID. However, I believe this will come to an end, and the current PE ratio of 50x cannot be justified, especially considering the company’s long-standing inability to increase operating income. COST has EBIT margins that range from 3% to 4% and has not been able to significantly increase them to the 6% range. Unless they start charging more for their products and services, I don’t think they will ever do so. This could provoke a decrease in customers, as it will be more expensive to shop at Costco.

E-commerce represented 6% of total net sales in 2023; it does not have a well-developed online business. Most of their revenues come from traditional shopping. The company is poorly positioned in online shopping, whereas Walmart and Amazon, which offer great alternatives at competitive prices, dominate the market. Costco stores will be impacted by a slowdown in traditional shopping over the next few years. The slowdown in traditional shopping was made clear in the paper by Hortaçsu and Syverson.

Buyers are becoming more “value-conscious,” which has slowed sales of expensive items like high-end televisions, computers, and other products where demand is highly elastic. Non-food item sales have decreased since 2021, and I expect these to keep declining as a percentage of total revenue. While it is true that COST has a moat and a loyal customer base across the United States and Canada, consumers are seeking greater value from their purchases, and there are better alternatives available somewhere else. I believe the company is worth about half its current value.

Source link