MSCI: Already A Good Company, Now ESG Makes It Even Better (NYSE:MSCI)

Ca-ssis/iStock via Getty Images

Investment thesis

MSCI (NYSE: NYSE:MSCI) has always been one of the go-to financial services provider that most of the world’s largest money managers rely on to make investment decisions. It provides informed decisions from offering research and advisory services that enable clients to understand and analyze drivers of risk in various markets while building portfolios. By the year’s end, MSCI had a clientele of approximately 7,000 clients across ninety-five countries.

MSCI

Due to the vastness of its investment holdings, BlackRock, a major hedge fund, is among MSCI’s top clients, representing about 9.8% of the company’s total income. However, MSCI has a varied income stream. It earns 95.4% of its income from management fees for its ETFs and ETFs indices.

With its market-dominating status and its “all weather” business nature, which means that it earns its revenue regardless of the market situation, our rating to the company is a Buy.

A quick look on its business segments

The company generates its revenues from four key business segments.

Indices

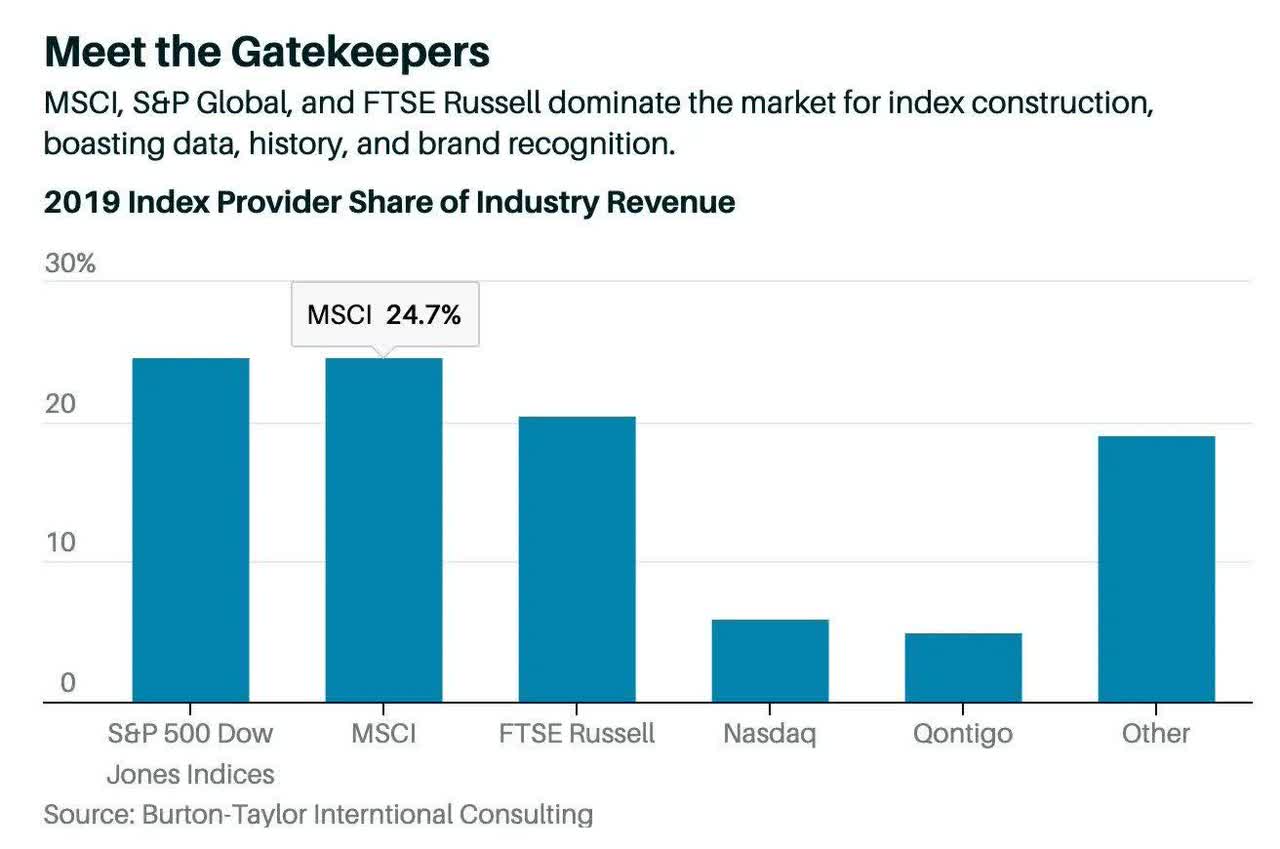

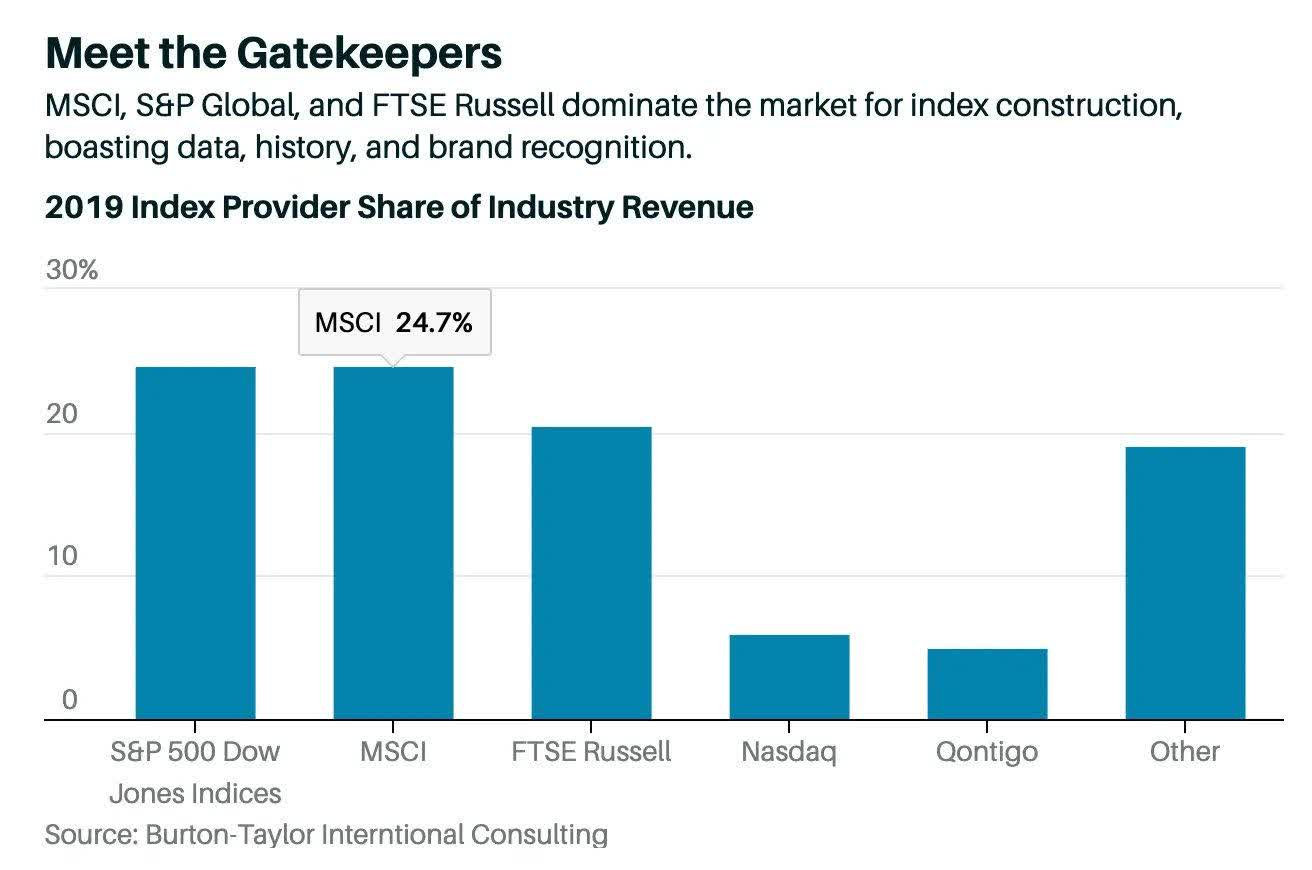

It is arguably the biggest segment under the MSCI portfolio tasked with developing indexed financial products such as ETFs, mutual funds, and annuities that investment managers track. The fact that MSCI calculates over 290,000 indices daily and 16,000 in real time underscores why it is one of the biggest players with a 25% market share.

Burton-Taylor International Consulting

MSCI offers indices tailored to specific product offerings, geography, investment factors, and volatility. Investment managers track these indices while building investment portfolios and paying annual and recurring subscriptions.

MSCI generates significant revenues from the indices by charging 0.02% to 0.04% fees on assets managed according to its research services. Consequently, the indices segments account for about 38% of its total revenues.

Analytics

Analytics is another major segment that accounted for about 24% of the company’s revenues in 2023. The segment offers portfolio management performance and risk management content. Clients tap into these resources at a fee to better analyze the various assets’ market and climate risk. Some tools offered under the segment include single security analytics and pricing models, stress tests, and liquidity risk analytics.

ESG & Climate

ESG & Climate is arguably one of the fastest growing segments under the MSCI portfolio owing to the growing demand and interest in investment opportunities tailored towards sustainability. Under this segment, MSCI provides tools and solutions that allow its clients to understand better how sustainability issues around the environment and social and governance issues could affect long-term risk exposure and return characteristics. The portfolio accounted for about 11.3% of the company’s revenues in 2023

Private Asset

The private assets segment offers data and analytics for private assets that clients use to understand fundamental information measures and compare the performance of various opportunities. The tools can also be used to manage risk in the investment world and conduct robust analyses. Some tools offered under the unit include Robust Capital Analytics, Portfolio Performance and Insights, and Private Capital Portfolio Management Platform.

MSCI

A growing business is a good, a high-margin business is even better

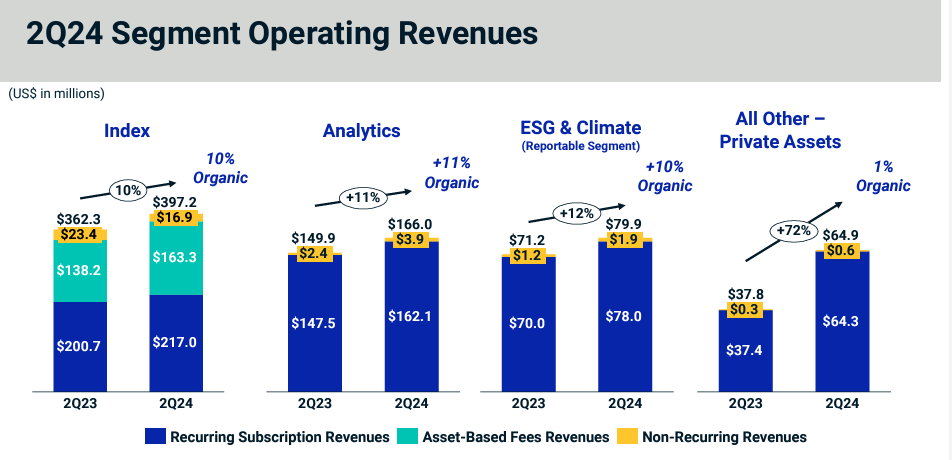

Based on the solid second-quarter financial results, the financial services company has been firing on all angles across its four segments. The results demonstrated the strength of all the franchises and their blue-chip client base.

The Indices segment posted a 9.6% revenue increase to $397.2 million, attributed to higher asset-based fees and recurring subscription revenues. Asset-based revenues increased, driven by ETFs linked to MSCI equity indexes.

Additionally, MSCI continues to benefit from growth in its market cap-weighted indexes. The adjusted EBITDA margin improved to 77.3% from 76.5% a year ago, benefiting from revenue growth.

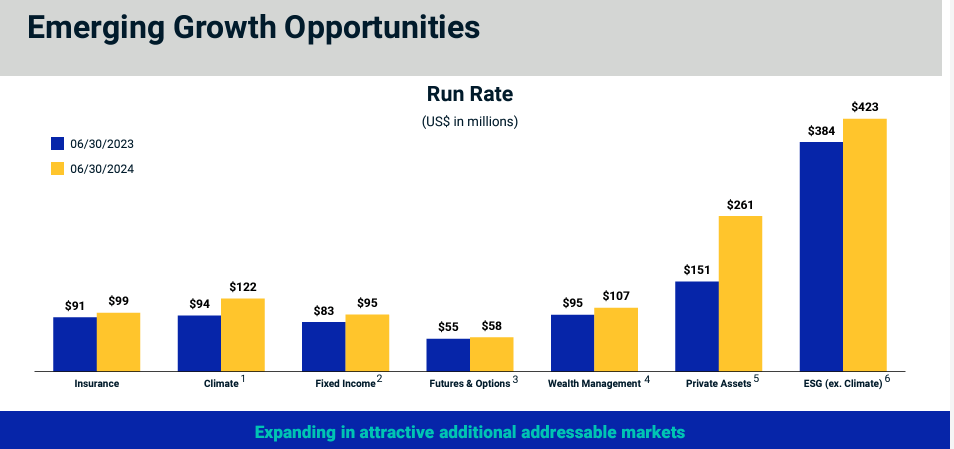

On the other hand, the ESG and Client Segment is once again proving why it could be a key driver of value in the years to come, having posted a 12.1% increase in revenues in the second quarter to $79.86 million. In the segment, MSCI benefited from growth in recurring subscriptions related to climate screening and product ratings. MSCI is staring at tremendous growth opportunities within its ESG segment, with the run rate increasing by 14.4% in the second quarter.

MSCI

Now, it comes to the core of our thesis – ESG is going to be a powerhouse to the business.

ESG rating is as important as other ratings

Firstly, ESG investing is the trend

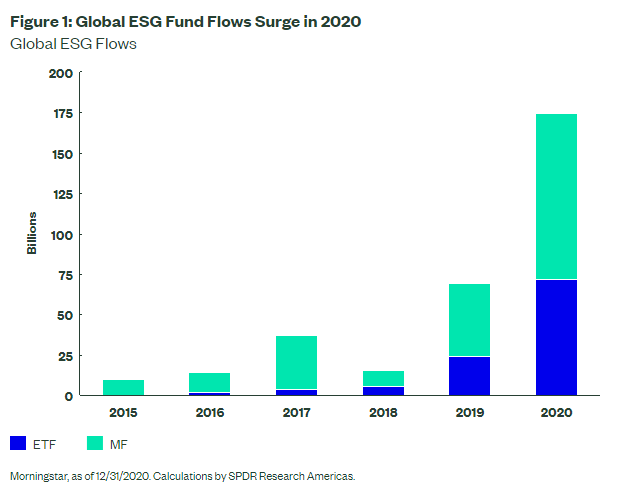

Climate change and other environmental and sustainability issues has become more and more important in investors’ decisions, because of the apparent intensifying extreme weather and surging regulatory requirements in ESG. ESG, or sustainable, investing is inevitably the next “credit rating” which every investor and manager has to comply and consider in their funds, which is shown in below graph.

ETF Trends

According to PwC, ESG fund will grow at a nearly 13% CAGR in the next 5 years and will constitute more than 20% of the global AUM. In another word, there will be a huge market for it.

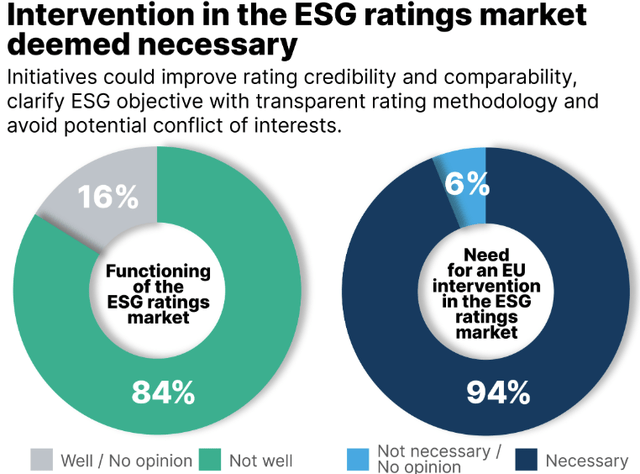

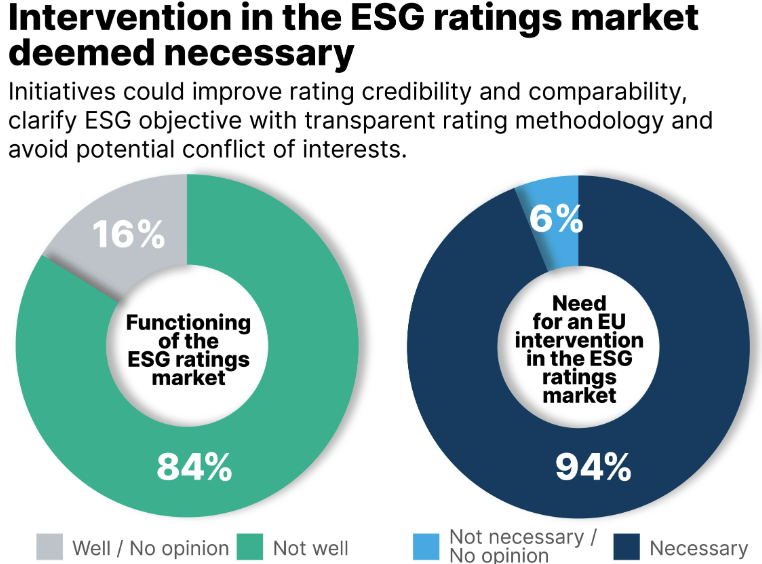

Secondly, there is little trustable source of data and rating for ESG

However, currently there is a huge gap in credit rating providers as there is little to no reliable data and ratings. In a consultation conducted by the European Commission, over 80% of the respondents said that the ESG rating market is now insufficient and performing not well.

IEEFA

This stands as a huge opportunity for MSCI who is a premium service provider that fund managers use and trust for a long time.

Lastly, ESG rating is a good business

MSCI has set itself a long-term target for the ESG business at mid to high 20% annual growth, which is the highest among other business segments. At the same time, ESG rating is one of the highest-margin business segments in the company. This begs the question – what is ESG rating?

MSCI

In a simple rating from AAA to CCC, there are numerous of issues taken into account, such as carbon emissions and board diversity. While some of these issues are quantitative data extracted from not-too-exclusive source such as ESG reports, most of these environmental and social issues are not quantifiable. As such, the business involves mainly data collection and establishing a mechanism – which can be leveraged and updated in subsequent year.

Therefore, this makes ESG rating a good business because once the mechanism and “quantifying” formula are set, it can be monetized for the future.

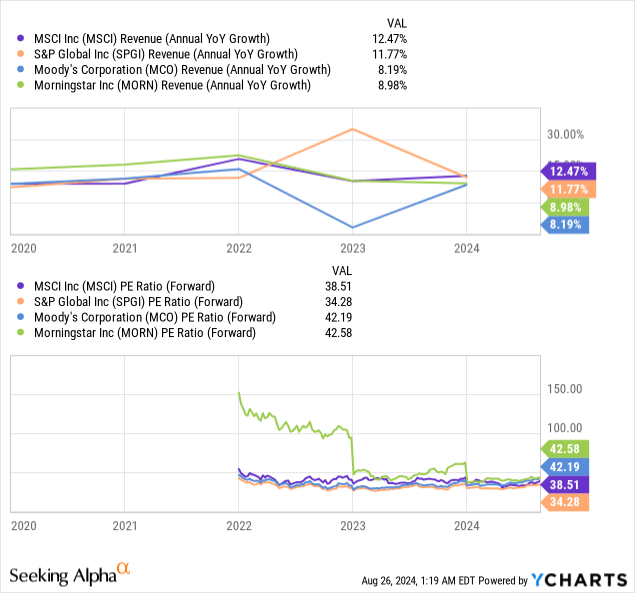

Target price: Solid financials and growing profitability

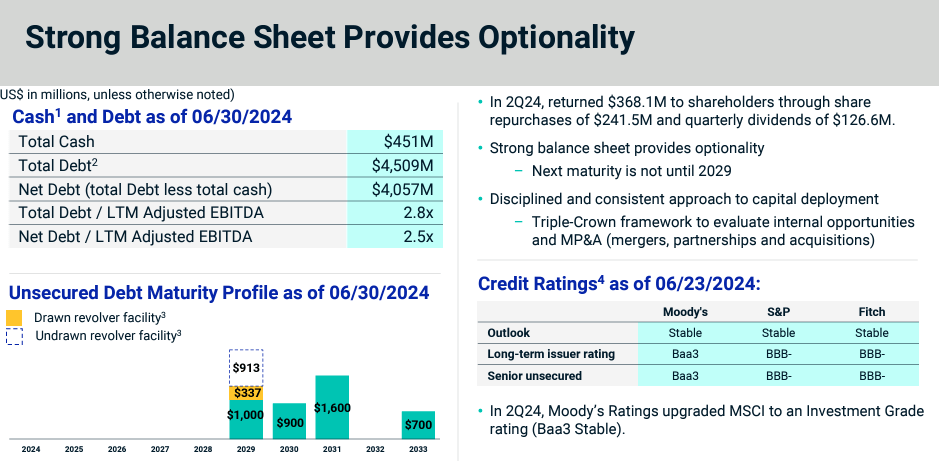

Amid robust growth, MSCI remains in a solid financial standing, concluding the second quarter with $451.4 million in cash. The company’s consistent effort to keep cash reserves between $225 million and $275 million for daily operations highlights its strong financial health.

MSCI

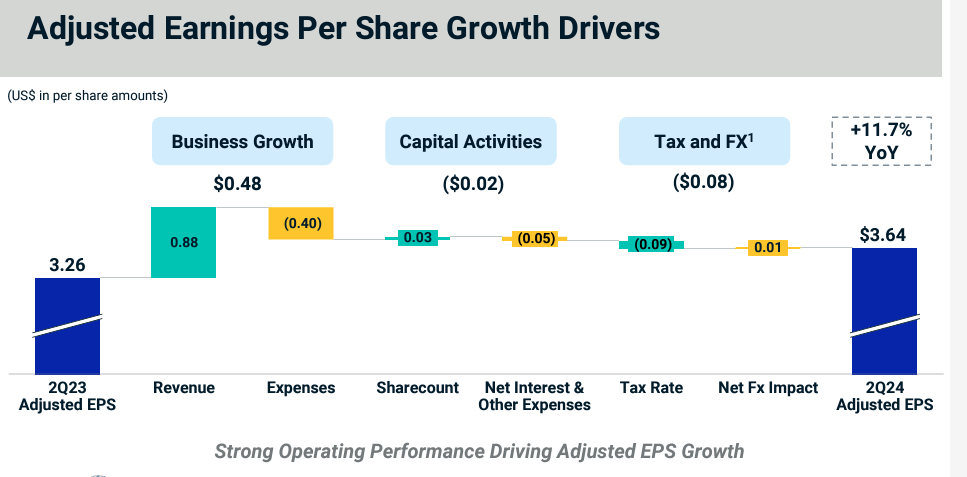

The company saw a rise in its cash flow due to an 8.1% growth in its net income for the quarter, which amounted to $266.8 million. Adjusted EBITDA climbed 14% to $430 million; adjusted EBITDA margin came at 60.7%. It exited the quarter with an adjusted earnings per share of 3.64 in the quarter, marking an 11% increase compared to the previous year.

MSCI

With its quality business operations and growing focus on emerging segment as discussed, it is estimated that the company’s earnings per share will continue to grow at a double-digit rate in the next 3 years, reaching around $15 earnings per share in 2024.

Meanwhile, the company is now having the lowest forward P/E ratio despite having the highest YOY growth in annual revenue because of its good execution of business strategy and profitability. Therefore, we think that the company will be re-valued to around 40x – 42x P/E ratio based on its growth and outlook.

With that, the 2024 target price for us is at around $600 – $630, which is a 10% upside based on a more conservative estimates. Therefore, it is a Buy for us.

Investment risks

Concentration risks: MSCI’s largest customers constitute a high proportion of its income, with BlackRock having 9.8% of its total income. If any of these customers decided to pull back, it will severely impact the company’s revenue and profits

Regulatory shift: We discussed that ESG will be an important driver for the company’s growth. But after all, ESG investing is a matter of compliance and regulatory requirements. Any new requirements or changes will affect the company and requires extra investment

Market volatility: Despite its “all weather” nature of having different kinds of indices and ETFs, changing market environment or downturn will lead to less AUM and services provision, affecting the business performance

Source link

{kind=link}