Patience Needed In The AI Buildout

D-Keine

Transcript

Markets are questioning whether top tech and cloud firms can deliver on their artificial intelligence investment.

1) Markets questioning AI

Capital spending by these firms has surged as they race to build out AI.

Some recent research from the investment community questions if revenues from AI alone will catch up with this capex.

We think it will take some time for big tech company revenues to reflect their AI capital spending. The AI buildout will take years – not quarters – to complete.

2) Broad-based AI demand

It’s important to distinguish between some of the companies spending big on AI – and the overall macro investment likely going into the AI theme. That has room to ramp up over time.

Nvidia’s Q2 revenues doubling from last year due to demand for its chips shows that AI capex is sizable and ongoing.

We will monitor revenue growth of top AI companies and adoption trends to gauge whether AI capex is paying off.

3) Our roadmap

Our three-phase roadmap helps us assess the potential economic and market impacts of AI.

We see the first phase unfolding now as large tech firms race to invest in data centers.

Early AI winners include big spenders and chip producers. Beyond that, we see opportunities in firms supplying key inputs like energy, utilities, materials and real estate.

We stay overweight the AI theme but eye signposts to alter our view.

Investors are debating whether future revenues for top tech and cloud computing firms could justify billions of dollars of capital spending being poured into artificial intelligence (AI). We think it’s key to distinguish between the individual companies and the broader economy when gauging the impact. We’re overweight the AI theme and see winners along the AI supply chain. Yet, we eye signposts for changing our view, including stalling revenue growth or sluggish AI adoption.

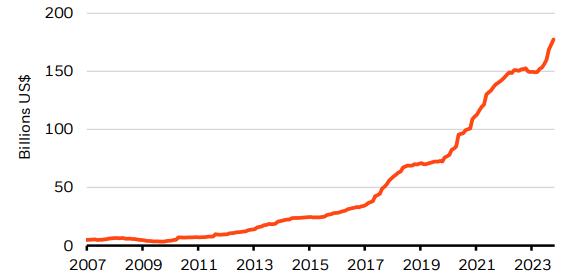

Big spending

Major tech and cloud company capital spending, 2007-2024

Past performance is not a reliable indicator of current or future results. Source: BlackRock Investment Institute, with data from LSEG Datastream, August 2024. Notes: The chart shows the combined 12-month trailing capital spending for Microsoft, Amazon, Meta and Alphabet.

In recent months, market buzz over the benefits of AI has flipped to worries that the companies investing big in it may not see the benefits so quickly. We assessed this sudden shift in sentiment with our portfolio managers. Overall capital spending by top tech and cloud players has surged in recent years, especially in energy-hungry data centers, as they race to build out AI. See the chart. Past investment ultimately led to a boost in revenue, helping deliver a return on investment, data from LSEG show. Yet, some recent research has questioned if the revenues from AI alone will eventually justify this wave of capital spending on it. When assessing AI capex by individual companies, investors must consider if they are making the best use of their balance sheets and capital. But for the economy overall, we judge AI investment by the major revenue that AI could generate across sectors.

Investment in AI could compare to capital spending on past tech innovations, like cloud computing. Yet, it’s possible that shareholders may not see further AI investment as the best use of corporate balance sheets. We see a disconnect between the short-term lens of some investors and the long-term visions of tech and cloud service providers. That divergence has spurred jitters among investors – but we think patience is needed. Some big spenders on AI have earmarked capex for building new data centers and exponentially multiplying processing power for AI. Such plans take years – not quarters – to complete. So it may take some time for revenues to fully realize AI capital spending. Some tech companies are already reporting increasing revenues from the roll out of AI-related products.

Broad-based AI demand

We see room for overall AI capex to spur some of the waves of transformation driven by mega forces, or structural forces shaping returns. Nvidia’s Q2 revenues doubled from a year ago, showing that AI capex is sizable and ongoing. Nvidia’s (NVDA, NVDA:CA) results highlight how the AI buildout is broadening: more than half its AI revenues came from non-tech sectors. We track a few signposts to assess our upbeat view on the AI theme. First, we look for signs of stalling revenue growth at top AI companies, adding to the importance of each earnings season. Second, we gauge changes in still-low AI adoption beyond the tech sector. Third, we eye any U.S. growth downturn that could spur big tech companies to curb spending.

We use our three-phase roadmap to track the economic and market impact of AI. The first phase – the buildout – is unfolding now as large tech companies race to invest in data centers. Early winners in this phase include those big spenders and chip producers. We also see opportunities in firms supplying key inputs like energy, utilities and real estate. In the second phase, we think AI adoption will expand to sectors beyond tech, such as healthcare and financials. This could result in a third phase of broad productivity gains, but the size and impact is uncertain. Our coming research will explore this in more detail.

Our bottom line

Investors are debating the implications of the AI capex boom. Some investors have cut positions in tech in recent months, implying room to rebuild holdings. We stay overweight the AI theme, but eye signposts to change our view.

Market backdrop

U.S. stocks have climbed back near all-time highs. The AI trade regained its footing after the volatility in July and early August, even as Nvidia’s shares stumbled on profit taking after its Q2 earnings beat expectations. Broadening Q2 corporate earnings growth, coupled with last week’s upbeat jobless claims and GDP data, show U.S. economic growth is holding up – a positive for risk assets. We think the Federal Reserve is unlikely to cut rates as sharply as markets are pricing in.

U.S. payrolls for August are in focus this week. At the Jackson Hole symposium, Federal Reserve Chair Jerome Powell noted the central bank is now focused more on any softening in the labor market. A further rise in the unemployment rate helped stoke recession fears last month. Yet, this was caused by an immigration surge increasing labor supply, not layoffs. We expect this week’s data to show signs of job growth holding up, alleviating lingering growth concerns.

Source link