Delek US Holdings: Refining Troubles And Rising Debt Spell Ratings Downgrade (NYSE:DK)

Monty Rakusen

Thesis

On August 10, 2023, I started covering Delek US Holdings, Inc. (DK) and broke down their Q2 2023 performance. I called out both the wins and the challenges they faced. Delek had a total throughput of 295,000 barrels per day and an adjusted EBITDA of $201 million, which showed some optimism, especially with rising demand and easing recession fears. But, I didn’t go all-in on a bullish outlook. Delek was lagging the S&P 500 (SP500), had an adjusted operating earnings growth rate of -5.84%, and there were some red flags like inconsistent dividends and shaky valuation numbers.

Since my call, DK moved sideways with some small gains into 2024 but started to edge down significantly in early April. The stock dropped for three reasons, despite oil and gas demand being solid. To begin with, rising crude oil prices hurt refiners like Delek. They buy crude to make gas, so higher oil means higher costs. If they can’t also raise gas prices enough to cover that, their profits decline. Moreover, as crude prices rise, the spread between what refiners spend on oil and what they can earn from selling gas shrinks. Tight refining margins are less attractive to investors. Lastly, even strong gas demand will be dented if gas prices rise so much that consumers cut back.

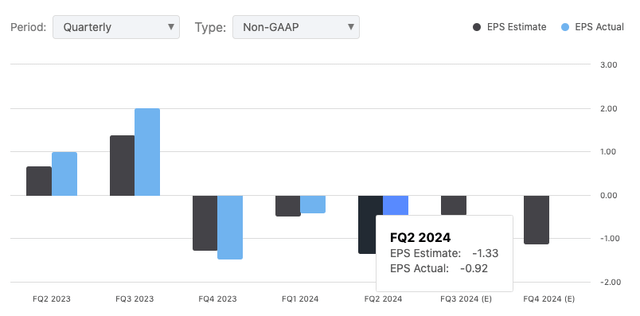

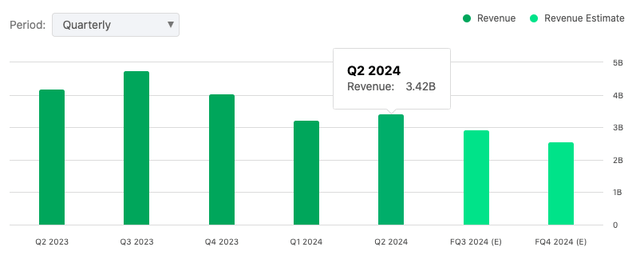

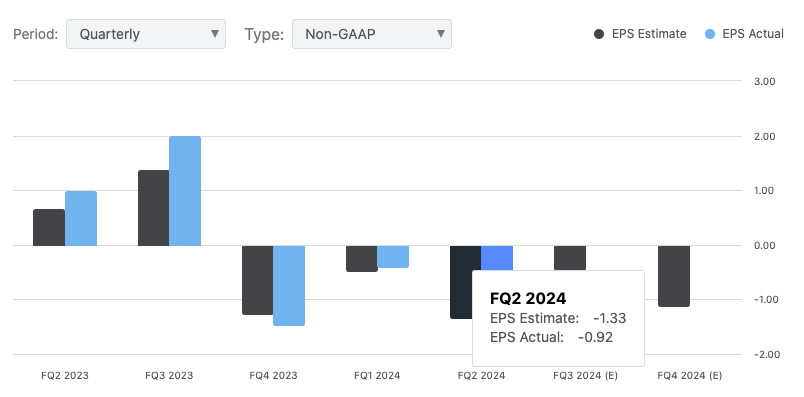

Today, I’m taking another look at Delek. Even though they reported a Non-GAAP EPS of -$0.92, beating expectations by $0.41…

Seeking Alpha

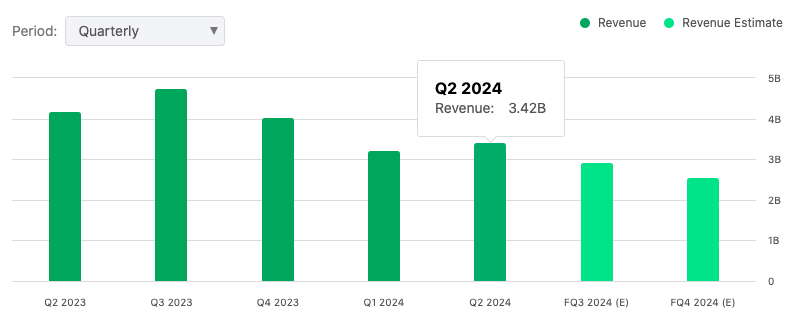

…and revenue of $3.42 billion, which is $110 million above estimates, they’re still up against some serious challenges.

Seeking Alpha

Operational improvements and strategic moves are nice, but they’re still underperforming compared to the S&P 500. With a hefty debt load and liquidity problems, I see a very bearish outlook for investors.

About Delek US Holdings

Established in 2001, Delek US Holdings, Inc. is headquartered in Brentwood, Tennessee, and engages in petroleum refining, logistics, retail, asphalt, and renewable fuels. Delek operates refineries in Texas, Arkansas, and Louisiana, and biodiesel production facilities in Arkansas, Texas, and Mississippi.

It has three main segments: refining, logistics, and retail (note: significant updates on “retail” below). Its refineries produce gasoline, diesel, jet fuel, and asphalt. The logistics side of the company gathers, stores, and transports crude oil and refined products. Its convenience stores, under the brand DK or Alon, are run under the retail segment, selling fuel and goods through locations in West Texas and New Mexico.

Delek has also been building its portfolio through acquisitions, such as its purchase of Alon USA Energy in 2017 (after previously holding a 47% stake in the company), which increased its holdings in refining and retail. As of 2024, Avigal Soreq serves as the CEO, leading Delek’s 3,500+ employees.

Delek US Holdings Performance

Fast Graphs

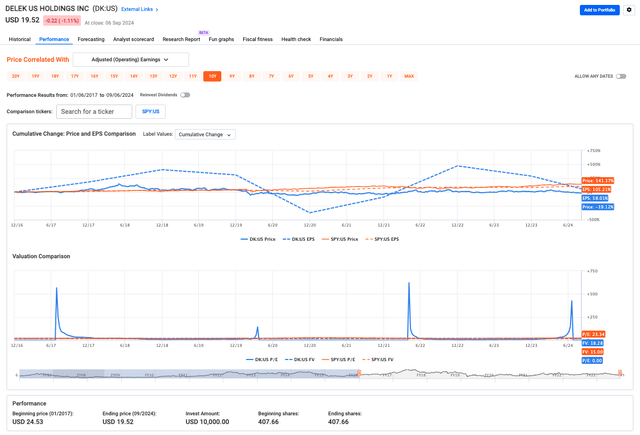

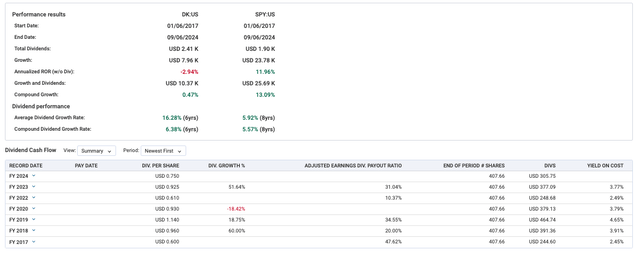

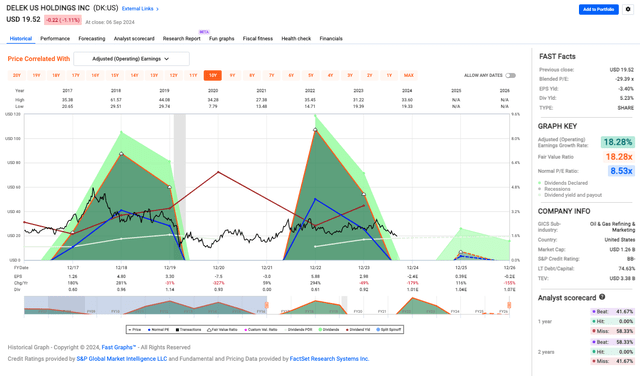

From 2017 to 2024, DK has underperformed, especially when you stack it up against the S&P 500. Since January 2017, Delek’s share price has dropped, giving an annual return of -2.94% (not counting dividends). Meanwhile, the S&P 500 has returned 11.96% annually.

Fast Graphs

Dividends have been the one bright spot, with DK’s average dividend growth of 16.28% over six years being solid, especially for the volatile energy sector. On the surface, income-focused investors might still find some value here, with a 6.38% compound growth rate in dividends. However, the bigger issue is Delek’s weak capital appreciation: a $10k investment in DK only grew to $7.96k, compared to $23.78k with the S&P 500. Bottom line: Investors would’ve been better off in an index fund. Simply looking at these comps, without better performance, higher margins, or favorable market conditions, DK risks staying a high-yield trap, not a growth play.

Delek US Holdings Growth

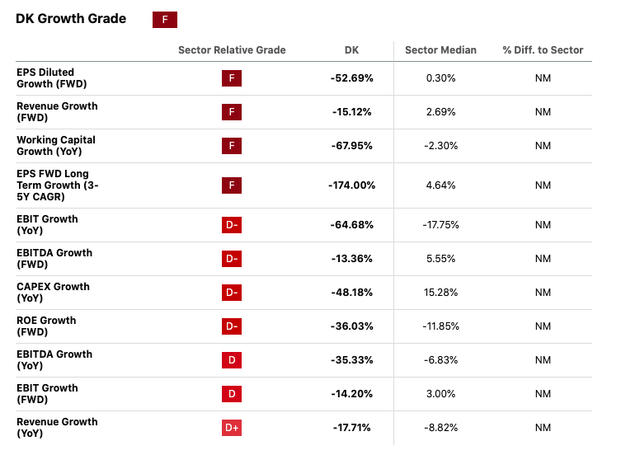

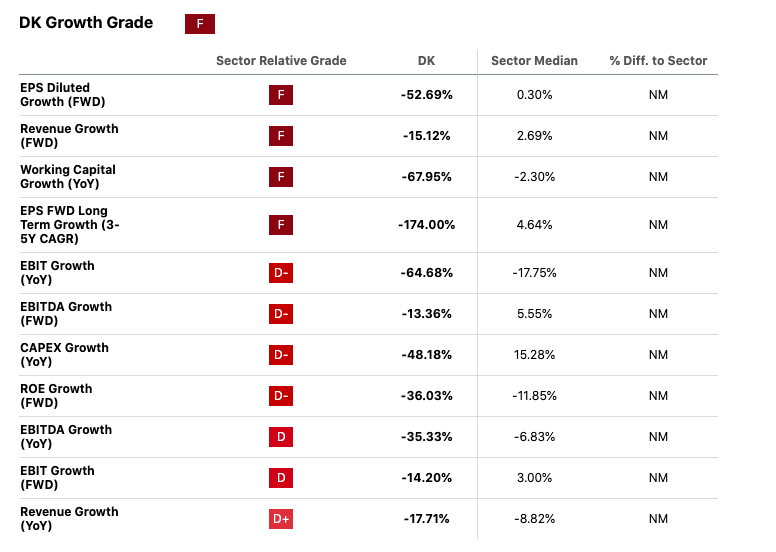

Since we’re on the topic of growth, DK’s has been tanking, and its momentum is slowing down compared to other Energy companies. That’s why it got slapped with Seeking Alpha’s “Sell” rating from the Quant system.

Seeking Alpha

Stocks with this rating have a history of performing way worse than the S&P 500. DK’s earnings per share are expected to decline by 174%, while the sector is seeing growth around 4.64%. The company’s financials, like revenue, working capital, and EBIT, are all down compared to others. Moreover, its stock price fell 27.76% in the past three months, much worse than the sector’s drop of 0.85%. These factors combined have led to the conclusion that Delek is likely to continue underperforming.

Delek US Holdings’ Q2 2024 Earnings Highlights

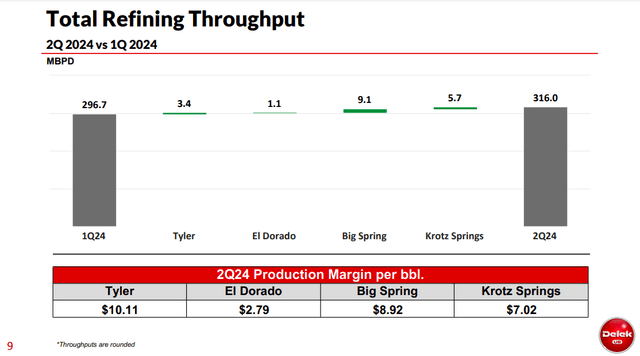

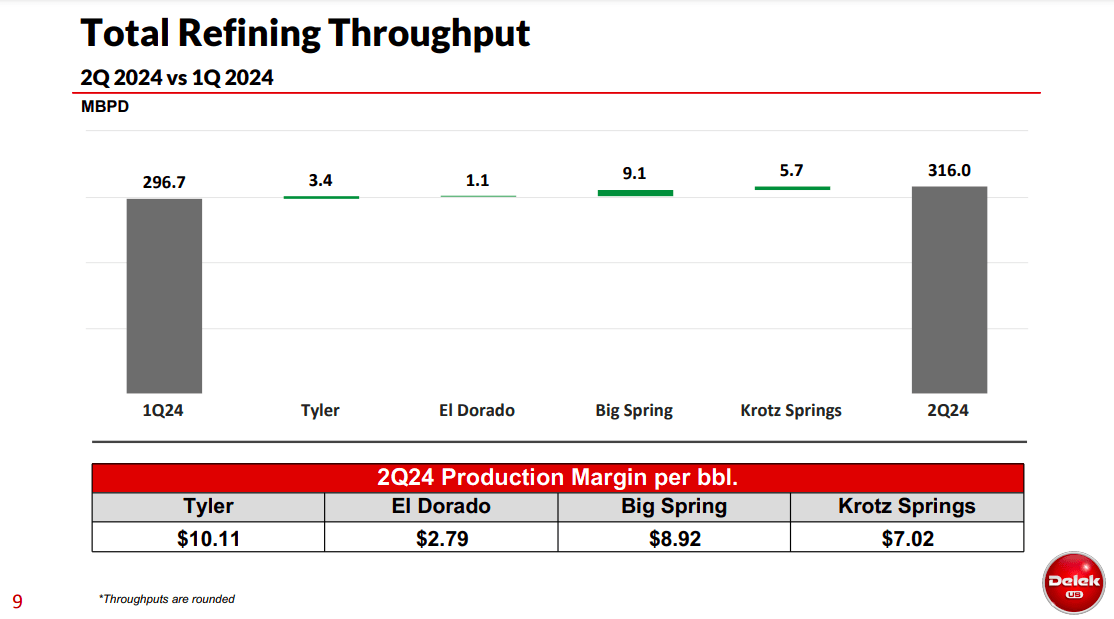

Delek US Holdings had a mixed quarter but made certain strides operationally. It set a quarterly throughput (the amount of crude oil that a refinery processes in a given period, usually measured in barrels per day) record of 316,000 barrels a day, a solid indication of refinery performance. The Big Spring refinery is also seeing signs of major improvement and now appears to be on a path to achieving the throughput and cost targets it set for itself.

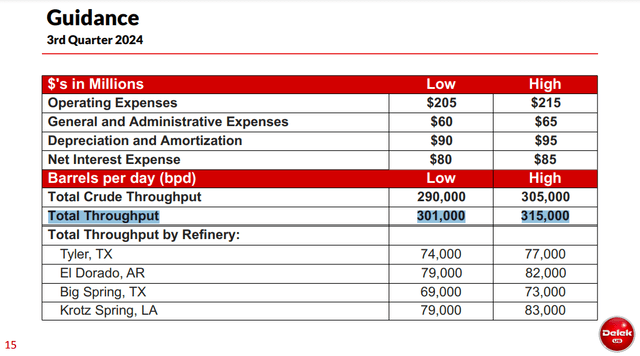

At the Big Spring refinery, they finished a project to handle benzene (a harmful chemical in wastewater) meeting legal requirements. For the next quarter, they expect to process between 69,000 and 73,000 barrels of oil per day.

DK 2Q24 Earnings Slides

In Krotz Springs, they processed around 82,000 barrels per day, making a profit of $7.02 for every barrel (see slide above), while spending $4.95 per barrel to run the refinery. They plan to process between 79,000 and 83,000 barrels per day next quarter. They’re also getting ready for scheduled maintenance in the fourth quarter.

DK 2Q24 Earnings Slides

Overall, they aim to process between 301,000 and 315,000 barrels per day (see above) across their whole system in the next quarter.

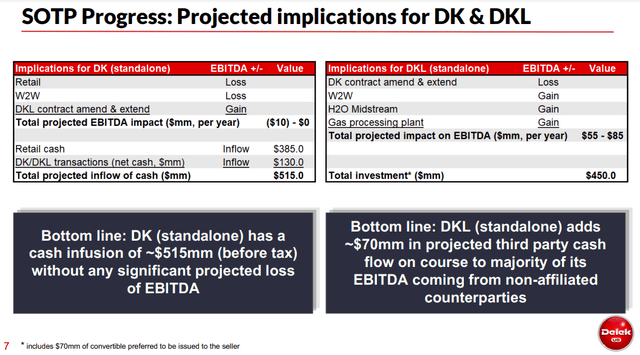

Meanwhile, on August 1, they announced the sale of Delek’s retail arm for around $385 million. This could make sense, given it will improve their balance sheet and put cash back into the hands of investors (via dividends), thus relieving some pressure on the company’s financial condition.

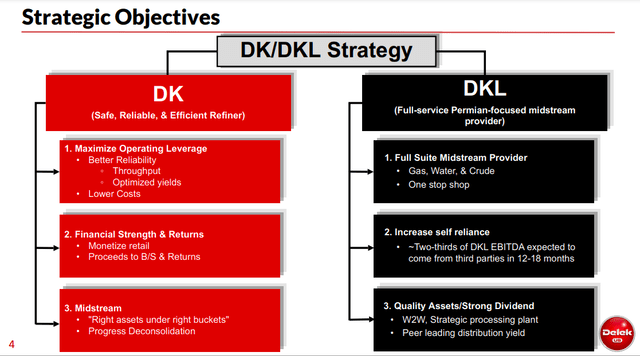

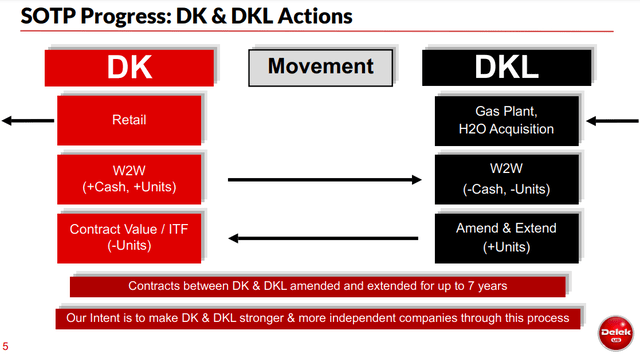

Regarding the recent announcements about Delek’s retail segment and other incremental progress and strategic developments, CEO Avigal Soreq highlighted the company’s strides in advancing its ‘sum-of-the-parts’ strategy. He noted that Delek has been making substantial progress in reorganizing its assets more effectively, with a particular focus on reducing the interdependence between Delek and Delek Logistics Partners, LP (DKL).

DK 2Q24 Earnings Slides

Note for new investors: DK mainly handles refining and retail (recently selling retail assets to simplify things). DKL, on the other hand, runs logistics, dealing with pipelines and fuel transport.

This includes the recent Wink to Webster project (processing and transport capacity), an expansion of gas processing capacity in Delaware, and the acquisition of H2O Midstream. All of this third-party business is a step toward making DKL more standalone – and ready for deconsolidation when a well-timed opportunity arrives. Additionally, the company recently initiated Phase 2 of its cost-reduction program, having met the initial target of $100 million in cost-cutting. Details of the next phase of cost-cutting remain under wraps for now, although management is still actively deploying teams to improve other parts of the business and will provide more details shortly.

DK 2Q24 Earnings Slides

All in all, DKL’s deal with Delek amounts to over $500 million in cash (see above) while keeping EBITDA steady, and it’s expected to deliver over 20% cash-on-cash return when it starts up in early 2025. And DKL’s acquisition of H2O Midstream will immediately boost EBITDA and free cash flow.

DK 2Q24 Earnings Slides

Meanwhile, the group’s logistics division delivered EBITDA of $101 million and DKL’s EBITDA increased on the back of higher third-party income and an extension of a contract by seven years (see above slide).

Seeking Alpha

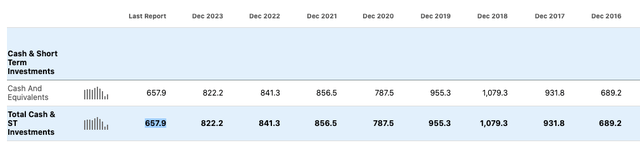

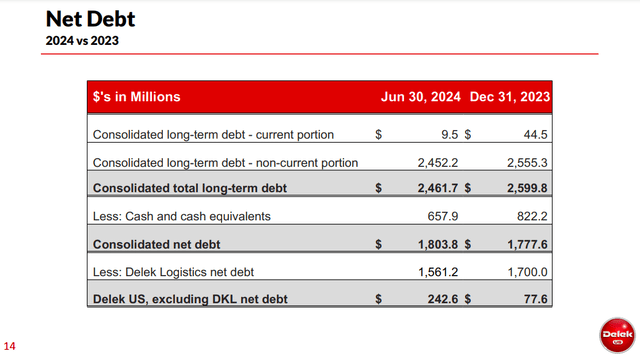

Finally, the balance sheet has cash of $658 million and $243 million in net debt.

DK 2Q24 Earnings Slides

Delek US Holdings’ Valuation

DK’s got a negative blended P/E ratio of -29.39x, which means it’s losing money, not making it. The EPS yield is also in the negatives at -3.40%.

Fast Graphs

While the (yield-trap) dividend is 5.23%, if the company keeps struggling to make a profit, they might have to cut that sometime down the road. Currently, the company is pouring lots of its cash back to shareholders and its stock with its recent $400M bump in its share repurchase authorization, bringing the total amount for repurchases to approximately $562M. It’s a bold move that aims to signal confidence as well as take advantage of lower-priced shares.

Adjusted operating earnings growth is 18.28%, but, in my opinion, with the company’s financial issues, that seems more hopeful than real. Delek’s loaded with debt, too, with a debt-to-capital ratio of 74.63%. That much debt, plus poor earnings, spells trouble if the economy or oil prices go south.

Then there’s the total enterprise value of $3.38 billion versus a market cap of $1.26 billion — that high enterprise value is mostly from big debt, showing Delek is leaning a lot on borrowed money. This can really tie their hands when it comes to investing in growth or getting through tough times with low earnings.

Delek US Holdings’ Risks & Headwinds

Overall, this was not a good quarter for Delek. They posted a net loss of $37 million, that’s negative $0.58 per share. The adjusted net loss hit harder at $59 million, or negative $0.92 per share. Refining EBITDA took a $64 million hit from weak margins, landing at an adjusted EBITDA of $108 million. Plus, they saw a negative cash flow of $48 million from operations, thanks to working capital outflows and net losses, signifying real liquidity problems.

The El Dorado Refinery took a hit, earning just $2.79 per barrel due to rough market conditions and higher costs. Delek’s Supply and Marketing also put red ink on the books, with wholesale marketing and asphalt divisions losing $17 million and $5 million, respectively, as early season bad weather weakened the asphalt market.

Finally, operating costs are likely to rise again next quarter, into the $205 million to $215 million range, not to mention another $65 million in admin costs. Meanwhile, Delek still hasn’t cracked the tough refining costs at its Big Spring and Tyler refineries, pushing margins even tighter.

Delek US Holdings’ Rating

I’m downgrading DK to a “Sell” since the company’s been consistently underperforming, it’s loaded with debt, its earnings are in the red and refining margins are slipping. Sure, there are some operational improvements and strategic sales, but the ongoing liquidity issues and the prospects of potentially necessary dividend cuts down the road mean investors might want to search for better opportunities.

Source link