Clean Harbors: Continued Reinvestment Runway To Redeploy Freely Available Cash (NYSE:CLH)

Matteo Colombo

Investment update

Following my last publication on Clean Harbors, Inc. (NYSE:CLH) the stock is +36% to the upside and there’s been several notable developments to the investment debate. Winding back to the original thesis, I was attracted to CLH for several reasons, namely:

- Top-down strategic allocation indicative of allocation to industrials given the attractive risk/reward fundamentals of the sector (it was poised to deliver ~16% of the coming 12 months’ S&P 500 earnings growth, but held just 8% notional value at the time).

- Management has an insatiable focus on producing freely available cash flow by persistently exhibiting reinvestment growth on incremental capital.

- It has methodically rotated earnings into FCF growth over the past 1,3 and 5 years respectively at ~18%.

These trends are in full situ following CLH’s Q2 FY’24 numbers and my conviction on this name remains equally in situ. This report will provide the latest updates for investors’ own reasoning. Net-net, continue to rate buy.

Q2 FY’24 earnings breakdown

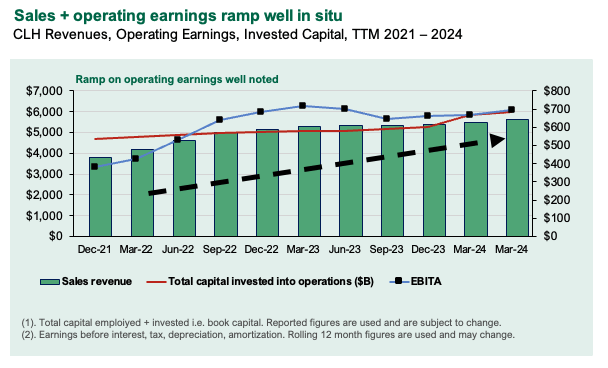

CLH put up Q2 revenues of $1.5Bn (+10.7% YoY) on adjusted EBITDA of $328mm – up from $287mm the year prior. This continues the longer-term ramp in sales + earnings (Figure 1).

Figure 1.

Company filings

The divisional breakdown on this is as follows:

The environmental services segment grew 12% YoY thanks to the first contributions from its HEPACO acquisition – Management said that this acquisition accounted for ~50% of the entire growth in revenues for this segment. The remainder was driven by volume and pricing. It said that incinerator utilization was 400bps higher compared to last year at 88%, with a +300bps increase in average realised prices. This was backed by a 400bps increase in landfill tonnage. Meanwhile, the technical services business grew 14% YoY, as it collected a record number of drum volumes.

The Safety-Kleen division grew 11% YoY due to higher volumes. Growth was underscored by demand for container waste removal. This could be a tailwind for the segment moving forward, but in my view, it is the environmental services business that deserves the most attention at this point in the cycle.

Regarding the potential deal with Castrol management discussed on the call last quarter, it had this to say on the Q2 call:

Last quarter, we discussed our multiyear partnership with Castrol and its more circular program. Castrol officially launched the program in late May at a key transportation industry trade show.

They have been employing considerable marketing efforts since the program was announced with two dozen media [indiscernible] and key publications. While we can’t share specifics about their sales progress, we can confirm that they have been building a pipeline of interest across many large fleet operators.

Our multiyear agreement with Castrol as a sustainability partner is a strong validation of our high-quality rerefined base oil.

As a talking point, management says that it is in a great position to execute on its Vision 2027 program. This is a good sign and the fact that it is focused on the combination of organic growth, acquisitions, servicing debt and buying back stock all “driven by ROIC” shouldn’t be overlooked in my opinion.

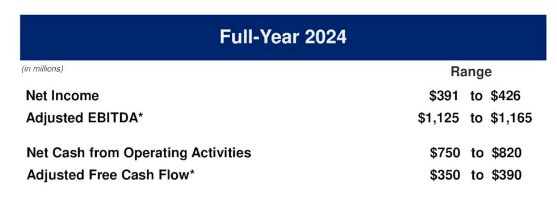

Given the reasonably strong result during the quarter, management revised guidance to the upside and now calls for $1.16Bn in pre-tax income at the upper end of range. It looks to produce $426mm of earnings on this, both of which are double-digit increases on previous guidance. The major upside driver is the HEPACO acquisition which management forecasts will contribute $35mm in pre-tax earnings this year.

It looks to throw off ~$350mm-$400mm of free cash flow which is tremendously attractive in my opinion as 1) it translates to roughly 30% of pre-tax earnings and 2) provides an excellent facility to re-deploy cash to meet its capital allocation objectives. In my view, it was a strong quarter that continued a lengthy process of management redeploying funds back in the business at high marginal rates of return. It is telling me that the New investments are more profitable than the legacy assets, which is highly conducive for a long runway of growth ahead in my opinion.

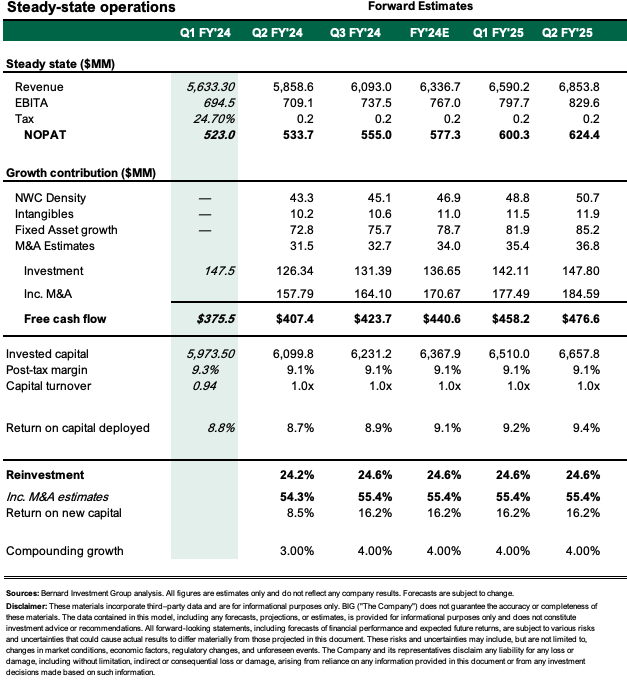

Figure 2.

CLH Investor Presentation

Valuations supportive of future upsides

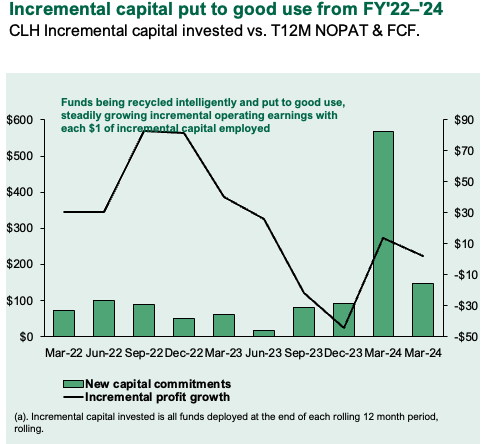

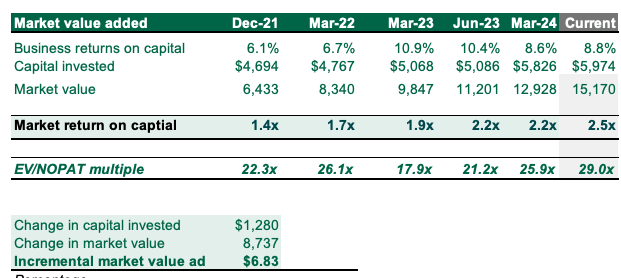

One of the standout features of this debate is management’s propensity to roll back the majority of cash earnings into the business to grow earnings power. We can see in Figure 3 this trend since 2021 and the corresponding rate of incremental earnings growth (note, the black line shows the earnings growth not the actual cumulative or printed earnings for the period, where earnings is net operating profit after tax). Point is, CLH is compounding capital at high marginal rates of return.

Figure 3.

Company filings

Valuation insights

- The market is certainly respecting this aspect and has lifted the valuation multiple on this business from 1.4x to 2.5x at the time of writing. Every dollar that management has retained and recycled back into the business by growing the capital base has been valued at $6.80 in market. Consequently, management has plowed back ~$1.3Bn to grow the business, this has produced more than $8.7Bn in incremental market value.

Figure 4.

Author

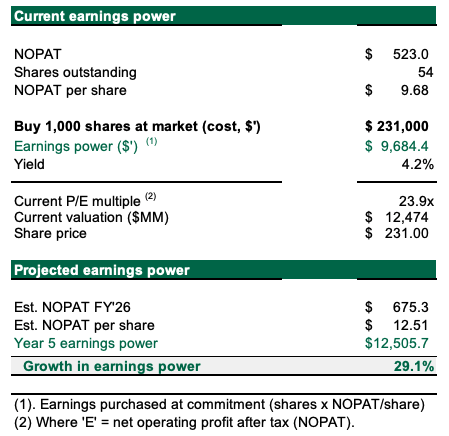

- The question is whether these trends continue, and will this valuation multiple hold. To get there, the business has had to produce high marginal rates of return on its incremental investments – in other words, it has had to reinvest in new projects that produce plenty of incremental earnings growth. My revised assumptions (see: Appendix 1) call for a 29% growth in earnings power by FY‘26E which could result in a market valuation of $245 per share.

Figure 5.

Author

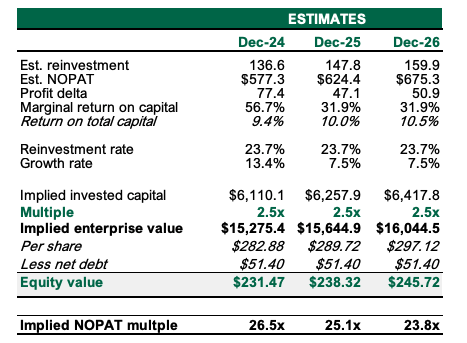

- This assumes management will reinvest about 20% of cash earnings each year, and produce up to 32% marginal return on these investments. This is a high hurdle, and the embedded expectations are equally as high at these current valuations. Therefore the risk is this management do not conform to these high expectations which could result in investors paying a lower dollar amount per dollar of invested capital in this business, or the propensity for the stock to carry higher prices be less given this fact.

- Subsequently my opinion is that CLH is well positioned to continue redeploying freely available cash back into its core operations and/or acquire accretive businesses to grow earnings power at statistically meaningful rates over the coming 2-3 years.

Figure 6.

Author

Risks to thesis

Downside risks to the thesis include 1) management, not redeploying funds into the business at all instead choosing to return all capital to shareholders as this reduces the valuation, 2) Rates in revenues and growth fading below 5% for the same reasons as above, 3) regulatory changes that impose a symmetrical burden onto the industry or the company, and 4) the broader of macroeconomic risks that must be considered right now, mainly the inflation/rates axis, and the spite of geopolitical risks that could potentially spill over into broad equity markets.

Investors must recognize these risks in full before proceeding any further.

In short

CLH remains a buy in my view given 1) lengthy reinvestment runway management has to redeploy surplus funds at an advantage, 2) it’s hard to replicate business advantages that ensure it has less frictional growth ahead of itself, and 3) business economics that warrant it to carry higher prices at current valuation multiples. Reiterate buy, aiming for $245 per share as the price objective.

Appendix 1.

Author

Source link