Broadleaf Partners Growth Equity Portfolio Q1 2025 Review

Torsten Asmus/iStock via Getty Images

Performance Commentary

Annualized | |||||||

Q1 2025 | 1 Year | 3 Years | 5 Years | 10 Years | 15 Years | Since Inception | |

Broadleaf | -11.6% | 0.2% | 7.1% | 17.6% | 15.2% | 14.9% | 12.3% |

-4.3% | 8.3% | 9.1% | 18.6% | 12.5% | 13.2% | 10.2% |

| Fund Inception 8/18/05. Portfolio performance reflects Broadleaf’s Growth Equity Composite, described more fully under the caption “Performance Disclosures.” You are urged to read that information in its entirety in connection with any evaluation of Broadleaf’s performance statistics. All figures are shown net of actual fees. Any assumed fees have been calculated on a pro forma basis, reflecting the highest fee levels that Broadleaf would charge clients per our disclosures in Part II of our Form ADV. |

Growth stocks had a tough relative quarter, as the market punished many of the big winners of the past few years. This “momentum” unwind resulted in a tough quarter for the BGEP.

Market Review & Outlook

We have written more than usual this quarter, given the volatility of the market and the flip- flopping developments in the economy. The rapid change in daily news flow has us on our toes, however, we feel that it makes sense to be more gradual with portfolio changes to the BGEP, as we discern what is true and what is narrative. The market is best described as moody, and we get a new mood each day. We believe it is important to listen to what the market is saying, but when it is hard to get a clear signal, it doesn’t always pay to obsess over every movement.

Our goal for this update will be to report facts on the economy, as we have recently given our opinions on the current tech and political environment. We will try our best to avoid AI or politics but feel obliged to mention that we are more constructive than the polarizing news flow. While at risk of being boring, sometimes a more sober approach is warranted.

Note: In the last couple of days we have spent preparing these thoughts, multiple highly respected market strategists have increased their odds of a recession, showing just how fragile the current environment is. We would note that most of these recession-call probabilities still reside below 50%, but the pace at which they are ticking up is notable. In addition, 4/2/2025 has been marked, “Liberation Day” by President Trump, which might represent yet another drastic shift in market conditions.

Earnings

Q4 2024 Earnings were rather strong, as earnings were up 13% in aggregate for large caps. Earnings also beat expectations rather handily, outpacing analyst expectations by about 7%, despite weakness in more cyclically oriented sectors such as energy and industrials. However, as we know, the market doesn’t care about the past – but cares about what is next.

The first look at annual guidance for 2025 was solid, but perhaps a bit conservative, as company management teams warned about the uncertainty in the business outlook, primarily due to tariffs. It is very common for management teams to guide conservatively in the first quarter of each year, and then set their sights on beating these conservative expectations.

There’s no doubt that given the volatile environment, management teams may find extra prudence to be wise, and this has been reflected as full-year earnings estimates have come down a hair since the beginning of the year.

If we drill down into the quarterly earnings expectations for 2025, the 1 st quarter has taken the largest hit as investors expect that the volatility of the current environment will bleed through in the upcoming quarter. However, a strong back half of the year is still expected, suggesting that analysts and market strategists are still expecting the current situation to improve as the year progresses.

Summary: Strong, resilient expectations in 2025.

Employment

The key cog for the economy is typically employment. Federal layoffs have thus far been absorbed relatively well, as weekly jobless claims have remained relatively low. If companies begin to suspect that economic uncertainty will not be resolved quickly, they will likely begin more significant layoffs to defend earnings.

Most management teams know that it is hard to make long-term strategic decisions in a whiplash kind of environment. Given this, companies are not hiring at the rapid pace they once were, nor are they shedding many employees. Many companies are simply maintaining the status quo, and as such, employees are more content to stay at their current jobs. As we saw a few years ago in 2022, we are not likely to have a recession unless further cracks emerge in employment.

Summary: Stable

The Consumer

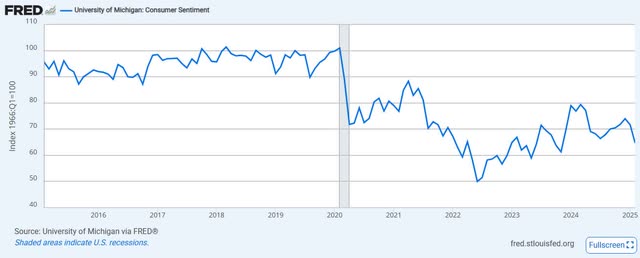

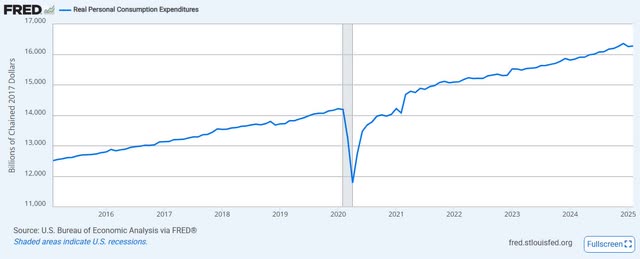

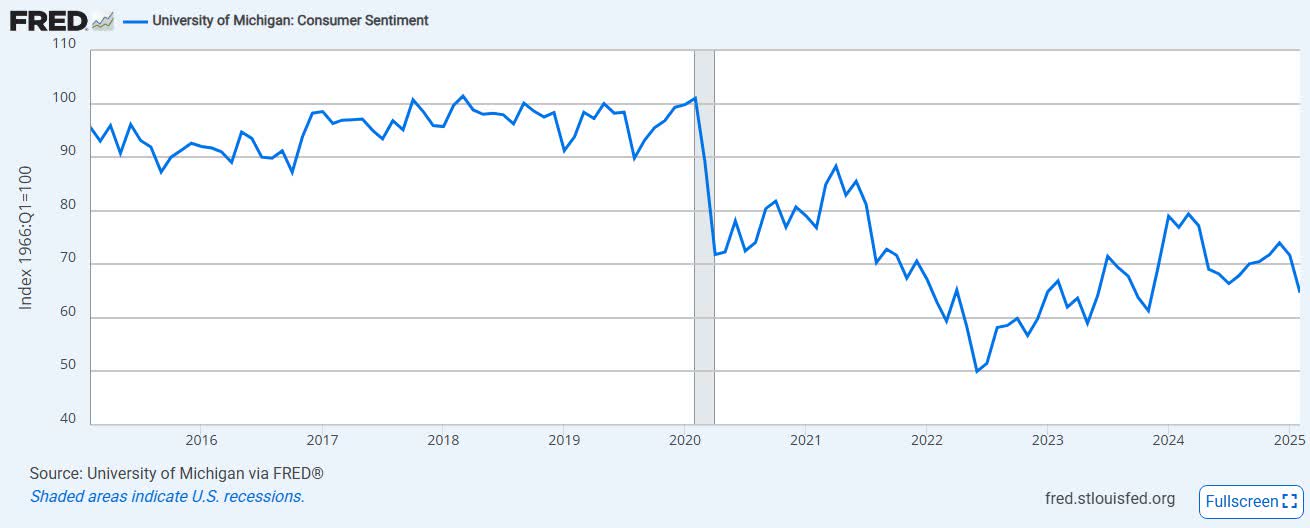

Consumer sentiment surveys hit the lowest levels since 2022, as consumers expect inflation to pick up again for a multitude of reasons. Many management teams affirmed that reinflation fears may be justified, with the prices paid for goods beginning to trickle up. These management teams also indicated that the consumer is selective, but they are still active. Who doesn’t love a good deal? The most recent economic data from last Friday, March 28th seemed to affirm these observations, with inflation trickling up month over month, and with actual consumer spending less depressed than how consumers are feeling.

Note: Consumer sentiment remains well below pre-pandemic levels. Consumers HATE inflation.

Note: Actual spending is as steady as it gets, save for the 2020 craziness.

One of our favorite economists, Ed Yardeni, likes to point out that consumers love to spend, especially when they are depressed, so long as they remain employed. While surveys have value, it is important to watch what consumers do, not just listen to what they say.

Consumers have remained relatively depressed ever since the COVID pandemic, with actual consumer spending looking rather resilient. The latest data suggests a slight bump in the road, but no major trend change at this point. It is important to listen to how consumers feel, as it can indicate future weakness, but this has not been a very reliable signal over the past few years.

Summary: Watch What I Do, Not What I Say.

GDP

The Atlanta Fed puts out a forecast on real GDP growth expectations for the current quarter. This forecast has a pretty strong reputation as being a reliable predictor of GDP growth for the current quarter. The most recent quarterly Real GDP forecast is expected to shrink by 1.8%, which is certainly not a good sign. However, a deeper dive into the components of this figure shows that net exports are solely responsible for the decline. Put in plain English, the economy is still growing, but companies are importing cars, electronics, and a whole host of goods before tariff day, which is leading to negative Q1 growth estimates. Companies will not likely import at such a rapid rate once tariffs are in place, making a Q2 bounce possible, but hard to predict.

If you are in the market for a new car, it might not make sense to wait much longer.

Summary: Declining. Tariff pull-forward clouds data.

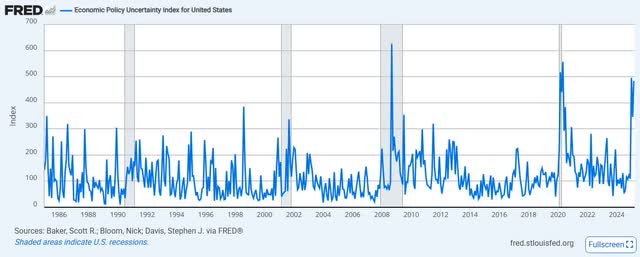

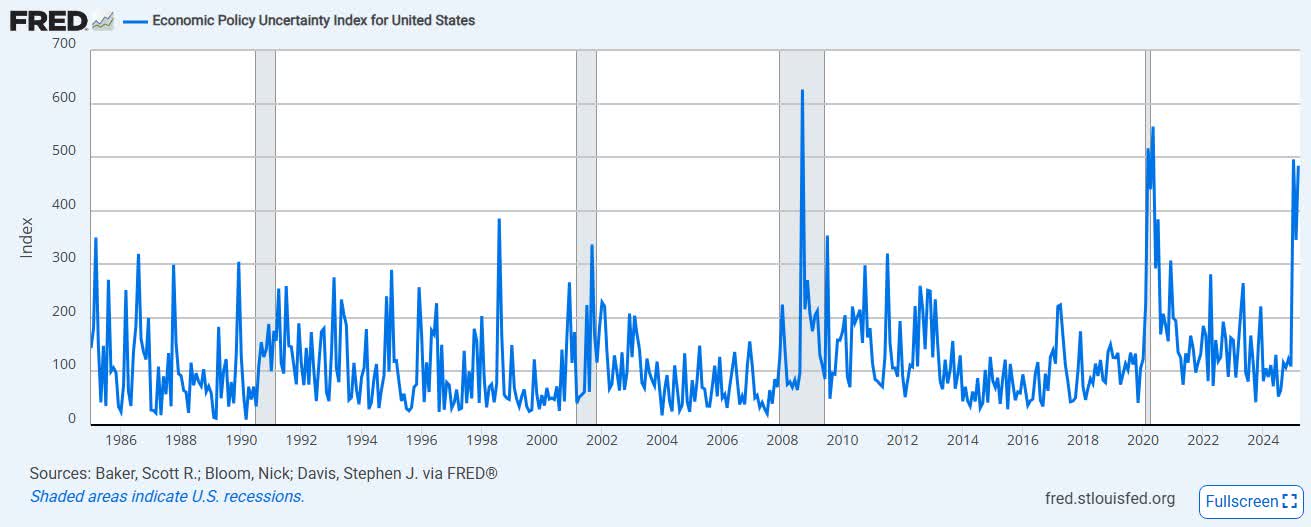

Uncertainty:

Economic policy uncertainty is near levels seen during COVID and during the Great Recession. This is surprising, as economic panic felt more palpable out on Main Street during those two prior peaks. While the current environment has raised a few eyebrows, we think that the uncertainty brought upon by tariffs and DOGE can be resolved rather quickly, for better or worse. We have no illusions that tariffs are good for consumers, but we do hope for more straightforward messaging and policy in due time.

It definitely seems like the business environment is on high alert right now, as M&A has slowed considerably. One of our favorite investing parables is, “Risk is where uncertainty is growing.” We won’t discount this one, but also think that self-inflicted dramas are more easily placated. In the meantime, risk is certainly elevated.

Summary: There’s a lot of fear out there.

Recently I have noticed in personal conversations and on social media that a debate has sparked on the wisdom of buying this dip. Many are happily buying it, throwing their hard-earned cash in potential harm’s way while other investors take risk off the table, fearing the worst is yet to come. This debate gets testy at times, as some investors question whether we can get yet another “V-shaped bounce.

Our crystal ball is as good as anyone else’s – and they are all pretty poor -, but we believe that both of these investors could be right. Being in the business of predicting recessions is tough and usually quite unprofitable work. We would remind folks that not long ago, it seemed like all of the smartest economists were calling for a recession that never came. Bear markets and volatility are a certainty of life, and they are the price we pay for the good times that will also no doubt, one day come.

A chart in my office shows the history of the US Economy. It serves as a reminder that we made it through a Civil War, the worst recession in US history (so bad it was called a Depression), two World Wars, a Cold War, the brink of nuclear catastrophe, endless panics, inflationary and deflationary regimes, and countless other periods of high uncertainty, just like we have today. I can also tell you that investors with a long-time horizon are happy with the forward returns from each of these uncertainty “peaks”. There is not much of a reason to think that this time will be different.

The real answer to the buy the dip question may be more of an emotional one. We feel that this could just be One Of Those Times, not inherently from a good or bad economy, but policy-induced anxiety. The solution to anxiety during these kinds of periods is usually altering one’s asset allocation – or buckling up for the ride.

We are coming off a long-term winning streak, and investors who began this run with us may find themselves today in a completely different financial situation than when it started. All the facts and charts in the world probably won’t change how you feel about your money, but we are still here to help. Our financial advisory team is one of the best in the business at managing the less quantitative, but more emotional intersection of behavioral investing and portfolio construction. Please do not hesitate to reach out to them if you have questions, or to me if you want to talk about some more epic charts and data!

Source link