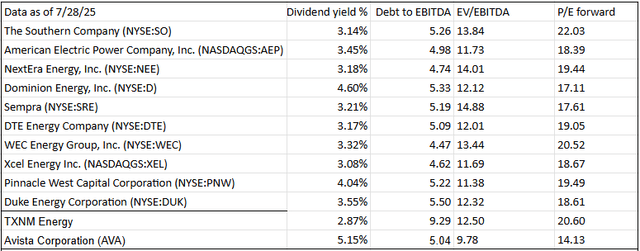

Stay On The Revenue Side Of AI

Companies of all stripes are trying to glom onto AI excitement. Even companies that are only tangentially involved will have the term AI appear 52 times in their conference calls.

AI is here and it‘s powerful, but how can investors differentiate between the businesses that truly benefit and those that are just clinging on to a trend?

I propose two simple and easy-to-follow rules that allow an investor to participate without getting swept up in the mania:

- Stay on the revenue side of AI

- Stick to a reasonable valuation

Lots of companies talk about how they are investing in their AI capabilities. That’s a cost-line item that hopefully will pan out someday. Or it could be another metaverse.

Recall that shortly after the pandemic, people correctly predicted that videoconferencing would be the future of business.

Zoom Communications (ZM) shot up hundreds of percent to around $600. But then it became clear that despite them having an excellent platform, monetization was always going to be difficult.

SA

I think many of the AI products will suffer a similar fate. Many companies will build useful and perhaps even broadly adopted tools, but monetization and margins are questionable.

I’m not suggesting that companies won’t be successful in selling AI, but rather that it’s a massive unknown. Many will fail, and a few will succeed.

A More Reliable Way to Invest in AI

Rather than trying to make something with AI and then sell it, other companies sell the foundational infrastructure that makes AI possible. I call this the revenue side of AI, because the revenues are already flowing,

I’m certainly not the first to notice this distinction, as the market has already bid up many or even most of the revenue-side stocks.

- Chips

- IPPs (independent power producers)

- Nuclear energy producers

NVDA and its chip peers have dominated the market.

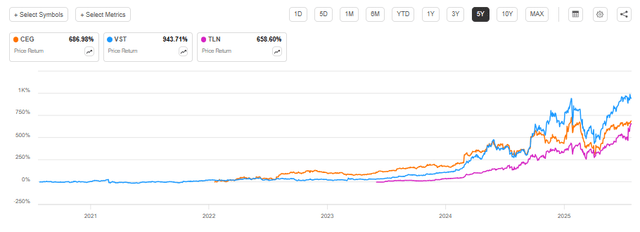

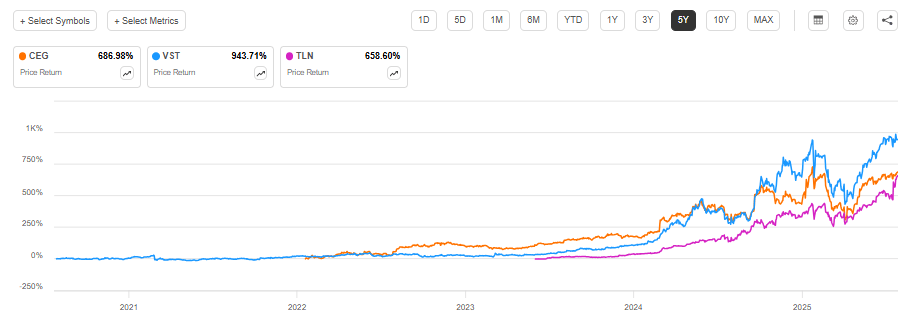

The independent power producers, Constellation (CEG), Vistra (VST), and Talen (TLN), shown below, are up 650% to 950%.

SA

Anything in the nuclear supply chain is soaring on hopes that it’s the reliable power to fuel AI.

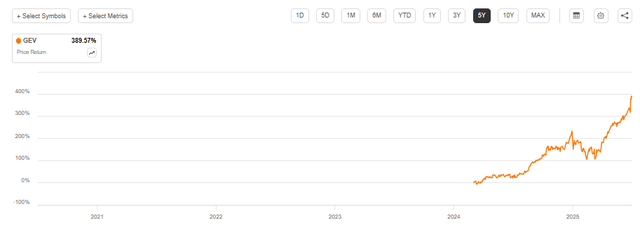

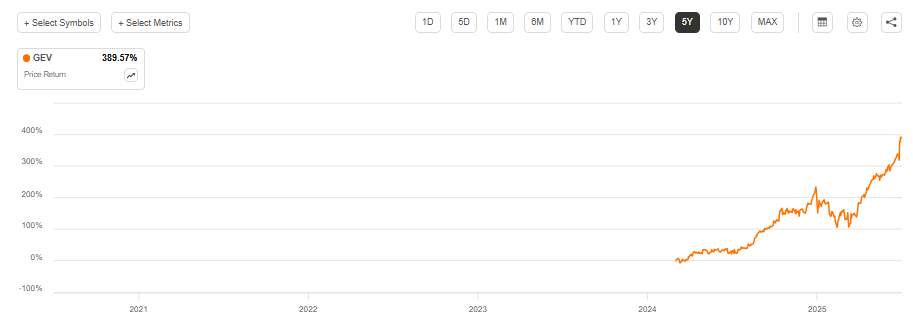

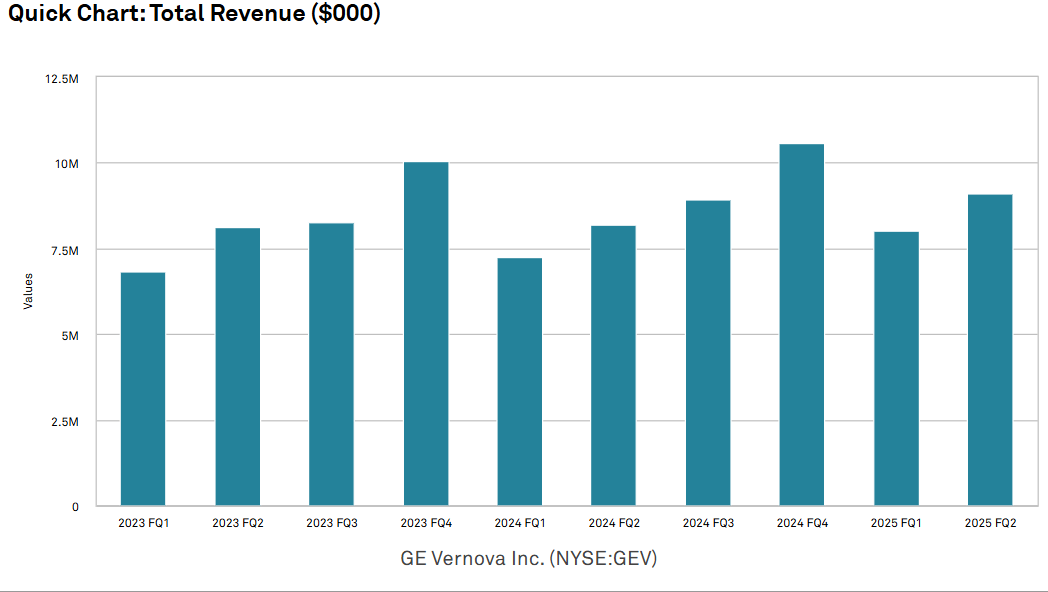

GE Vernova (GEV) is perhaps the poster child for the energy infrastructure boom.

SA

Each of these categories has had legitimate fundamental success.

The latest PJM auction shows significantly increased prices, which will further bolster the earnings of the independent power producers.

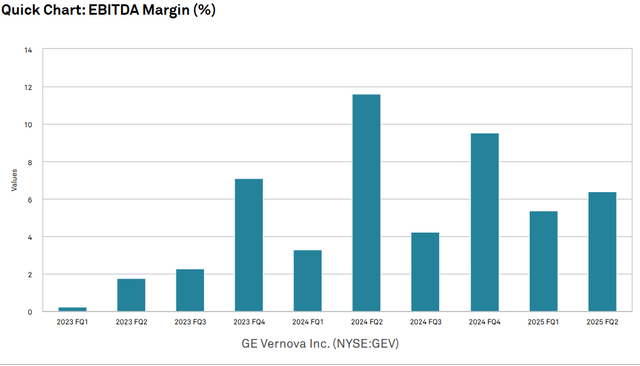

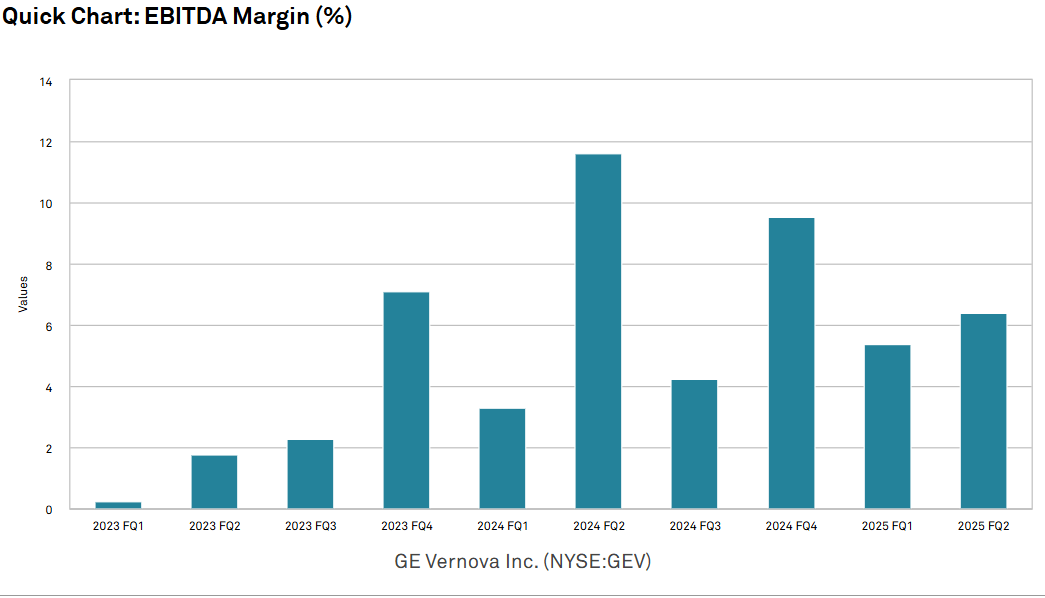

GEV’s margins have increased significantly, and there is speculation they will rise to the mid-teens.

S&P Global Market Intelligence

I wrote about and bought GEV shortly after its spin-off. It was a great position for me, but I sold too early and now have a healthy dose of seller’s remorse.

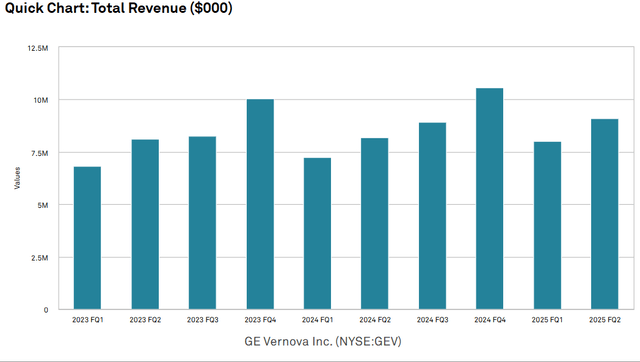

GEV’s revenues have increased steadily along with the margins.

S&P Global Market Intelligence

Revenue growth in tandem with margin expansion has a multiplicative impact on earnings. However, even strong earnings growth could not keep pace with the explosive market price.

GE Vernova now trades at 87X forward earnings. The rest of the really hot revenue-side AI stocks follow the same pattern—strong earnings growth that hasn’t kept pace with stock price.

This leaves them trading at lofty multiples:

- CEG – 35X forward

- VST – 28.6X forward

- TLN – 58.1X forward

- NVDA – 40.1X forward

These multiples may not seem that high compared to the S&P, but keep in mind that these stocks are in sectors that have historically been quite cyclical.

A cyclical stock should trade at its highest multiple at the trough of the cycle and its lowest multiple at the peak of the cycle. Thus, to justify multiples this high, one would have to believe that these companies are closer to the trough than the peak. Given the explosive earnings growth they have already experienced, I find that difficult to believe.

It’s possible the AI wave is so powerful that these industries are no longer cyclical and have been launched into secular growth. That‘s the sort of conviction one would need for investment at today’s prices to be justified.

Instead, I think there are more reliable gains to be had in the pockets of the revenue side of AI that have not yet been bid to the moon.

Value Plays on the Revenue Side of AI

We consider regulated utilities to be the best mix of value and growth for participating in AI. They’re not typically considered AI names, so allow me to elaborate on how they benefit by contrasting them with the IPPs discussed earlier.

The independent power producers participate in market prices of reliable extra electricity, so they directly and swiftly benefit from the spike in PJM auction prices.

The swiftness has made their earnings spike and, in my opinion, oversubscribed by stock market prices.

Regulated electric utilities experience a similar demand spike, but due to their heavily regulated nature, they’re much slower to respond.

These next few years will be an interesting time frame in which there is a tremendous imbalance in energy markets. The demand for electricity ramped up rapidly, while the production of additional electricity is a process that takes up to five years. Permitting, regulating, and physically building new plants all take a long time.

During this window of imbalance, the IPPs and suppliers like GEV are reaping the majority of benefits. However, as time goes on and supply catches up to demand, it will be the regulated utilities that enjoy long-term higher earnings.

Incremental demand for electricity has manifested in massive pipelines for just about all of the regulated electric utilities. They’re putting in place plans to substantially grow their production and transmission infrastructure base over the next decade. Most of their pipelines are between 50% and 200% of the market cap of each company.

As this infrastructure is built, the rate base of each utility increases, and its earnings increase proportionally with the rate base. Most of the utilities are now projecting long-term annual earnings growth in the 6%-9% range.

This might not sound like much, particularly as the S&P has recently been growing a bit more than that. However, there are two factors that I think are being overlooked by the market.

- 6%-9% growth is a lot more for companies that don’t really have negative growth periods

- Valuation

During growth phases, the S&P might grow at a double-digit pace, but it also has periods where it has substantial negative growth. Thus, a portion of its growth during the good times is just making up for previously lost growth.

Electric utilities are different because they have largely avoided recessions. Thus, each 6% to 9% growth they put up is against record high growth. The growth is fresh, incremental growth rather than a portion of it making up for previous losses.

So really, the S&P is only growing faster in nominal terms when looking at a period that happens to be during an upswing.

The 6%-9% annual growth rate utilities are positioned to enjoy over the next decade, in combination with their dividends, significantly outperforms the long-term returns of the S&P.

Valuation

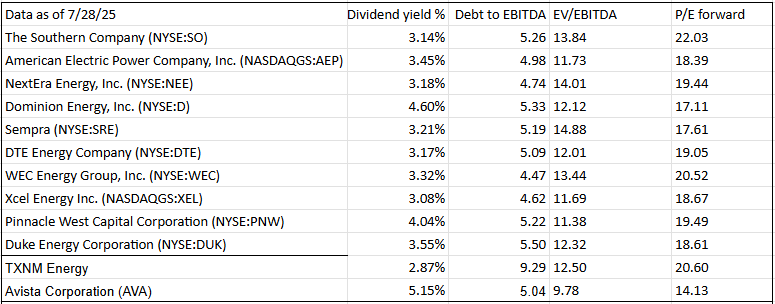

As electric utilities have not really been considered part of AI despite the massive spike in electricity demand that results, market prices have remained low. The entire sector is trading at a significant discount to the broader market.

2MC

Between discounted valuation and high sustainable growth, I think regulated electric utilities will outperform the market.

Source link