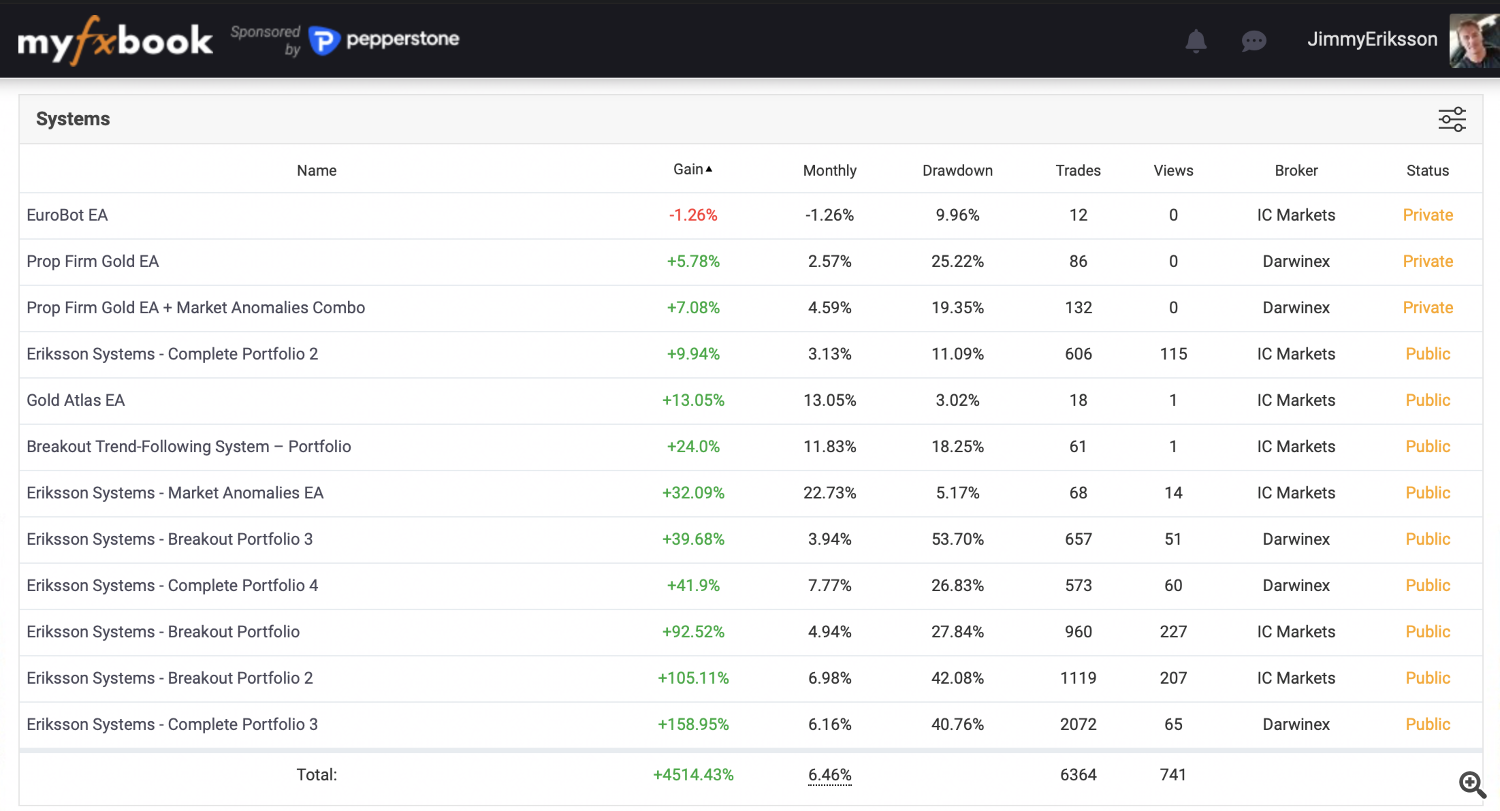

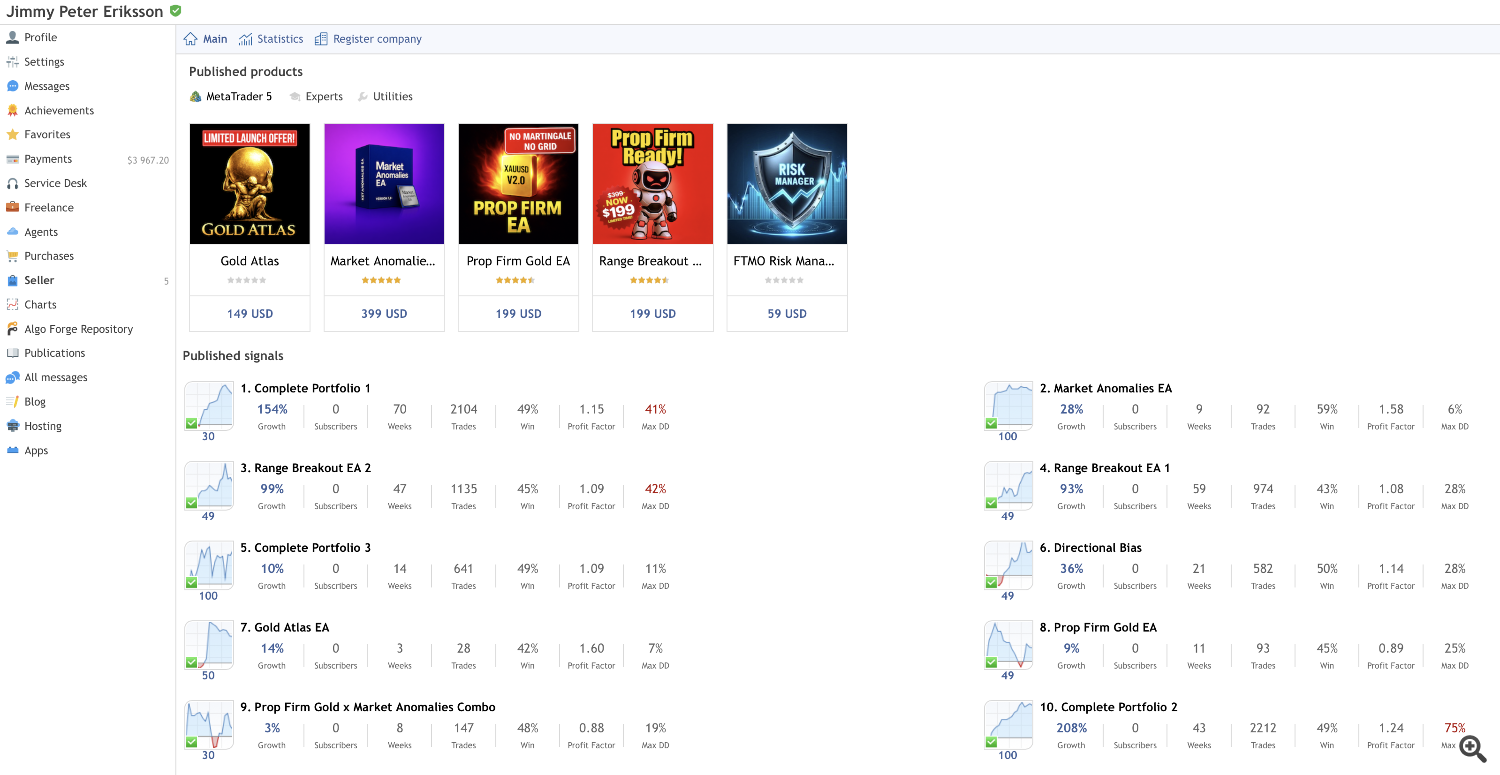

Why Most Multi-Strategy Portfolios Are Improperly Weighted

How I Calculate Risk per Strategy to Achieve Equal Portfolio Weighting

When running multiple expert advisors or trading strategies in the same portfolio, equal risk per trade does not mean equal exposure. In fact, using a fixed risk per trade across different strategies almost always leads to imbalanced performance, where some strategies dominate the portfolio while others dilute returns.

The goal of my risk model is simple:

Every strategy should contribute roughly the same expected annual return to the portfolio.

To achieve this, risk must be adjusted based on:

Why Fixed Risk per Trade Does Not Work

Let’s look at common mistakes:

1. Different trade frequency

If both use the same risk per trade, Strategy B will naturally have much higher exposure, even if it performs worse.

2. Different holding times

Even with the same number of trades per week, the strategy with longer holding time has:

Because of this, you cannot equalize risk by:

-

Using the same percentage risk

-

Dividing risk by trades per week

-

Ignoring holding time and volatility

Step 1: Risk Must Be Based on Volatility (ATR)

I base all risk on volatility, not stop-loss size or fixed percentages.

Specifically:

-

Risk is calculated using 1 ATR (Average True Range)

-

Usually a daily ATR, as it represents the market’s average daily movement

This approach:

-

Automatically adapts to different instruments (Forex, Gold, Indices, Crypto)

-

Adjusts for changing market conditions over time

-

Avoids problems where price levels change but volatility increases

A 1% move today is not the same as a 1% move 20 years ago — volatility-based risk solves this.

Step 2: Define the Portfolio Target

Example portfolio:

This means:

Step 3: Backtest Each Strategy at 1% ATR Risk

For each strategy:

Profit Factor is crucial because:

Step 4: Use a Realistic Profit Factor Baseline

Backtests often exaggerate performance.

I assume a realistic long-term profit factor of 1.2.

This is:

Step 5: Scale Risk Based on Profit Factor Degradation

Example 1: Strong Backtest, Needs Higher Risk

But:

Target is 5% per year, so:

Example 2: Weak Backtest, Needs Lower Risk

If PF improved from 1.1 → 1.2:

Target is only 5%, so:

Final Result

After adjusting risk this way:

-

Every strategy is normalized to the same expected annual contribution

-

High-frequency strategies no longer overpower low-frequency ones

-

Long-holding strategies are properly weighted

-

Portfolio behavior becomes smoother and more predictable

If all strategies end up with the same real-world profit factor, they will also produce the same annual return.

This is the foundation of a properly balanced multi-strategy portfolio.

Source link