AMLP ETF: I’m Buying Every Dip On This Near 8% Yielder

spooh

Alerian MLP ETF (NYSEARCA:AMLP) focuses on investing in energy infrastructure MLPs which includes: pipelines, processing plants and storage facilities. Investors love the yield that MLPs offer, and they are great options for income investors. However, I never buy MLPs directly because they often issue K1s, which are end-of-the-year tax forms.

My experience has been that these tax forms are often sent out late, complicate your tax filings, and are even amended/corrected later, which can make it necessary to file an amended tax return. All of this can cause issues when you try to file your taxes on a timely and correct basis, so that is why I specifically avoid this sector. However, there are some MLPs, such as AMLP, which do not issue K1s but instead file 1099-DIV forms, which are far more straightforward. I find that AMLP offers the best of both worlds, which is the high yields that MLPs provide, and yet without the hassles of K1 tax forms, so let’s take a closer look:

The Chart

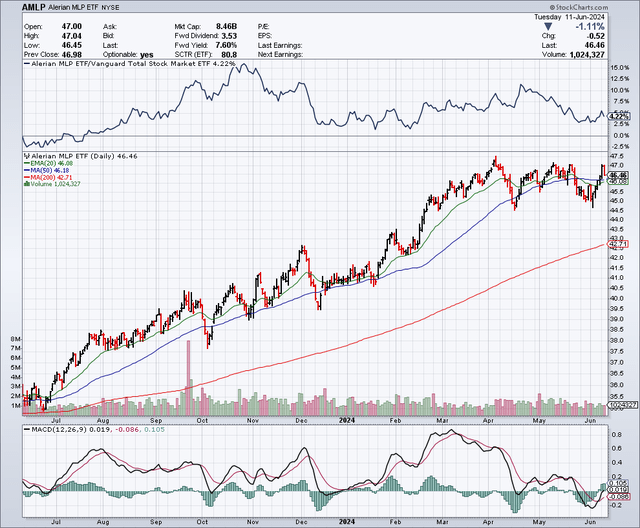

As the chart below shows, this stock has been in a strong uptrend for the past year. The 50-day moving average is $46.19 and the 200-day moving average is $42.67. Buying dips for the past year has been a strategy that has paid off, and I believe this will continue. I plan to buy pullbacks, especially at or below these key support levels, which are the 50 and 200-day moving averages.

StockCharts.com

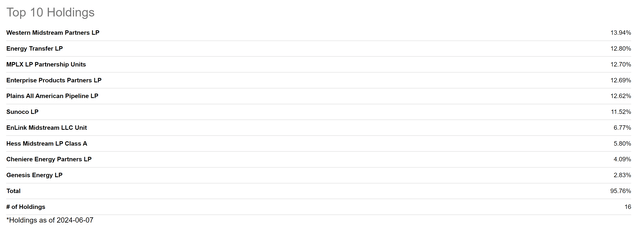

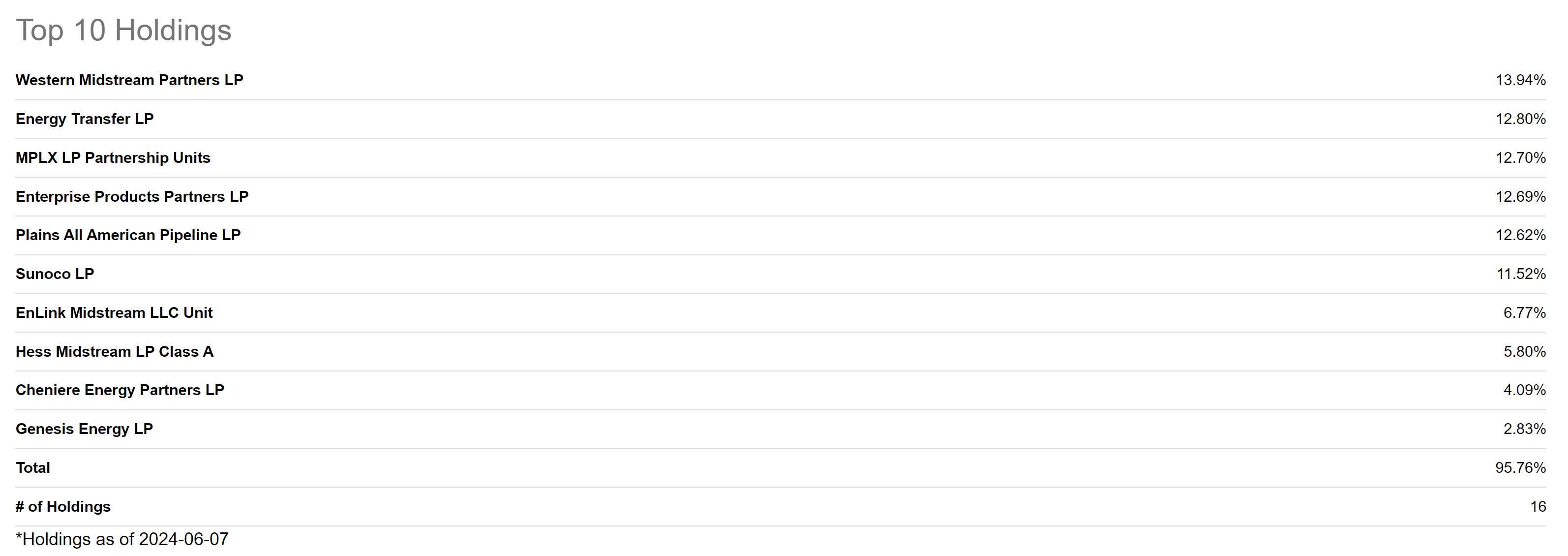

Top Ten Holdings

The top ten holdings for this fund include some of the most popular MLPs. Here is a listing of some of the holdings:

Seeking Alpha

Let’s take a closer look at the top 3 holdings:

Western Midstream Partners LP (WES) is a pipeline company which offers a yield of 8.9%. Bill Gross who co-founded PIMCO and is also known as the “bond king” recently called Western Midstream Partners as one of the best MLP pipeline companies. This stock is up for the year, but it still appears undervalued as it trades for just about 10 times earnings, which analysts expect to come in at around $4 per share for 2024. This MLP represents about 14% of the total assets held in AMLP.

Energy Transfer LP (ET) is one of the best-known and most popular pipeline companies. With a market capitalization of nearly $53 billion, it is also one of the largest and most liquid MLPs. This MLP offers a yield of about 8%, and it trades for just about 10 times earnings. Energy Transfer recently agreed to buy WTG Midstream Holdings for $3.25 billion. This deal shows that this industry is potentially undervalued and ripe for more consolidation. Energy Transfer is a significant holding for AMLP at nearly 13% of total assets.

MPLX LP (MPLX) is an energy infrastructure company with gathering, processing, and storage facilities. It offers a yield of about 8.25%, and it trades for just around 10 times earnings for 2024. MPLX is another major MLP, with a market capitalization of around $42 billion. MPLX represents almost 13% of AMLP’s total assets.

Why This ETF Could Continue Providing Upside

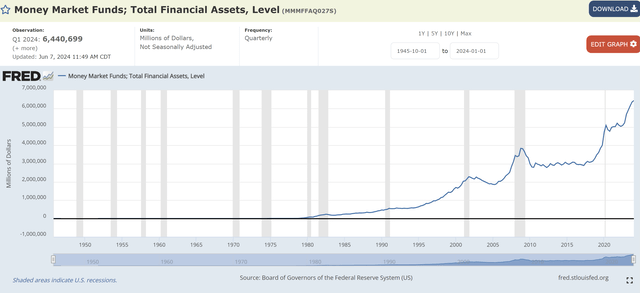

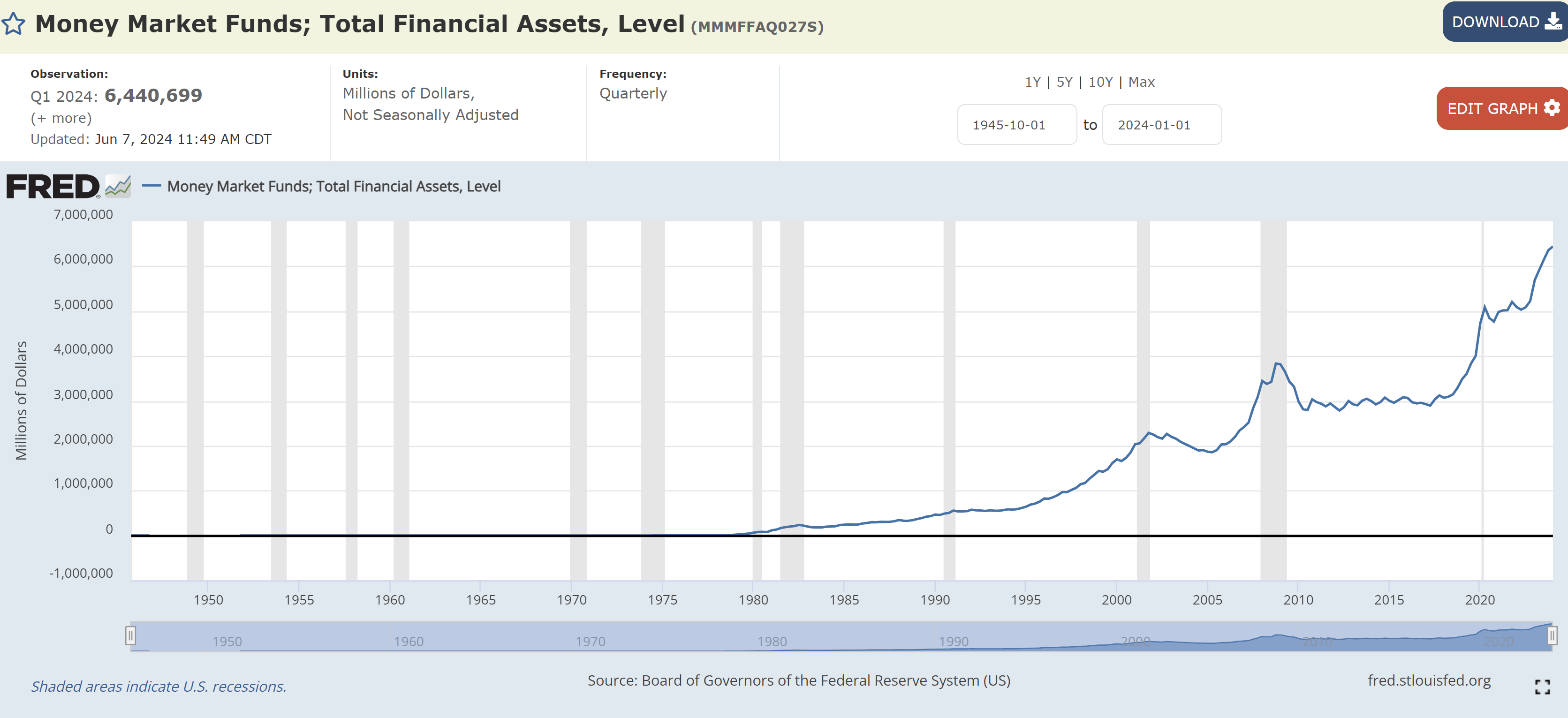

The Federal Reserve’s “Dot Plot” shows that it expects the Fed Funds rate to drop from about 5% today, to around 3% in 2026. That’s a drop of roughly 40%, and this means money market yields could also follow this same path and see yields drop from around 5% to just about 3%. If this happens, investors are likely to seek out and be willing to pay more for stocks that offer high yields. This could also be fueled on a massive scale, since money market funds have a record level of cash, which is now more than $6.4 trillion (as shown in the chart below).

If money market yields drop to around 3% in 2026, I believe yields from MLP stocks will also drop, and that means prices are going up. For this reason, I think it makes sense to lock in the high yield that AMLP offers now, before rates eventually decline. This could produce strong total returns for shareholders between the high current yield offered now and the potential for capital gains as rates drop.

Board of Governors of the Federal Reserve System (US)

More M&A Deals Could Be Coming And Boost Shareholder Returns

As noted above, Energy Transfer recently announced an acquisition, and it said it expects more M&A deals in the midstream sector. East Daley Analytics is also expecting the robust M&A activity to continue and views it as being driven by a few factors, as detailed in a report which states in part:

As the midstream sector transitions into a lower-growth environment with increasing regulations, we expect M&A to continue. Companies will use mergers to gain scale, better position themselves to take advantage of growing export markets, and optimize their existing assets in the ground.

Based on this, I would expect more deals to be announced. In particular, I believe Energy Transfer will continue to acquire smaller midstream assets which could be accretive to earnings through cost savings and scale. This should continue to be a positive tailwind for the sector, and I see this as another reason to continue a buy the dip strategy with AMLP.

The Dividend

In May 2024, Alerian MLP ETF raised the quarterly dividend by nearly 7%, which brings it to $0.94 per share. This provides a yield of around 8%.

Potential Downside Risks

Even though most MLPs have little to no direct exposure to oil prices, this sector tends to trade with the energy sector. Because of this, there could be potential downside risks from a big drop in oil prices and energy stocks. Regulations are another potential downside risk to consider, especially during an election year. Lawsuits from accidents, pipeline leaks and other environmental concerns are additional potential downside risks to consider.

In Summary

When looking at valuation, many of the MLP stocks are trading for just around 10 times earnings and also provide high yields. I think this leaves a lot of upside potential in terms of multiple expansion. Another factor that could drive multiple expansion for this sector is the potential for interest rates to drop over the next couple of years. When you combine a high yield with the potential for capital appreciation, the total returns could be very strong. I also like seeing some M&A activity in this sector, which could be a sign of undervaluation and also help to drive the upside. Since I think the uptrend in AMLP and this sector in general is poised to continue, I view AMLP as a strong buy, especially on pullbacks.

No guarantees or representations are made. Hawkinvest is not a registered investment advisor and does not provide specific investment advice. The information is for informational purposes only. You should always consult a financial advisor.

Source link