Much Data to Digest… U.S. Stock Futures in the Red Ahead of PPI and Many Other U.S. Reports – Currency Thoughts

Much Data to Digest… U.S. Stock Futures in the Red Ahead of PPI and Many Other U.S. Reports

May 15, 2025

The dollar, U.S. stock futures and 10-year Treasury yield lost ground overnight, reacting in part to greater-than-anticipated U.S. oil inventories last week and OPEC downwardly projected energy supplies.

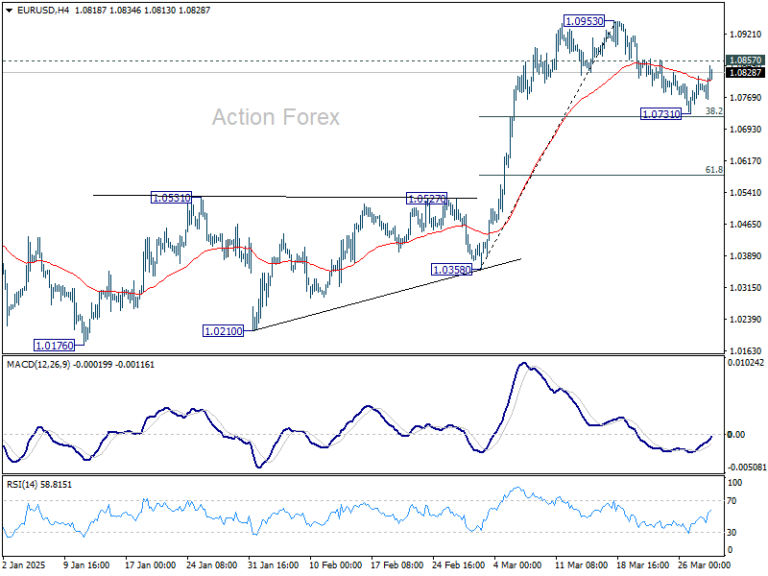

The dollar fell 0.5% below Wednesday closing levels against the yen and Swiss franc. The greenback is also down 0.3% against the Mexican peso, 0.8% versus the Korean won and 0.1% relative to the euro and sterling.

Around 08:00 EDT, U.S. stock futures were trading about a half percent lower. West Texas Intermediate oil had lost 3.4% in value, and Bitcoin was down by 1.1%. Stock markets this Thursday fell 1.0% in Japan, 0.8% in Hong Kong, and 0.7% in China but advanced 1.5% in India following Trump’s disclosure that India was offering to cut its tariffs to zero percent. There’s been comparatively little net movement so far today in European stock markets.

Amid fresh concerns about future growth, ten-year sovereign debt yields are down by four basis points in France and Germany, three bps in Italy and Spain, two basis points in the United States and U.K., but up a basis point in Japan. The price of gold weakened 0.3%.

Some of today’s already-reported data have shown resilience. Industrial production in the euro area leaped 2.6% in March, their largest advance in 52 months. Production was 3.6% greater than in March 2024. Real GDP growth in the joint currency area last quarter got revised downward marginally to 0.3% on quarter, but the year-on-year comparison matched the early estimate of 1.2% as well as on-year growth in the final quarter of 2024. Within Euroland, quarterly GDP rose fractionally in Germany, France and Italy and fell by 0.5% in Portugal. But growth in Ireland and Cyprus accelerated to 3.2% and 1.3%. Employment in the euro area advanced 0.3% on quarter, beating expectations of a 0.1% uptick, and were 0.8% greater than a year earlier.

From today’s menu of British data releases, investors learned that GDP rose by a greater-than-forecast 0.7% last quarter and 1.3% in year-on-year terms. The quarterly figure was the most in a year and led by business investment. British industrial production fell back 0.7% in March after a 1.7% increase in February, and such also posted a 0.7% year-on-year decrease. Construction output in March climbed 0.5% on month and 1.4% on year. British labor productivity grew more slowly (0.2%) last quarter than in the prior quarterly period and was also 0.2% below its year-earlier level.The U.K. goods and services trade deficit narrowed to a 2-month low of GBP 3.65 billion in March was more than five times larger than the deficit of GBP 683 million in March 2024. Among just goods trade, the deficit remained substantial at 19.87 billion pounds.

Like consumer prices reported Tuesday, U.S. producer price inflation in April was lower than forecast. The overall PPI sank 0.5% on month, its greatest drop in 60 months and yielding a 7-month low 12-month increase of 2.4% after 3.4% posted in March. Producer price inflation excluding food and energy slowed from 4.0% in March to 3.1% last month, and the index when trade was also excluded dropped 0.6 percentage points to a year-on-year pace of 2.9%. None of these cases were below the cyclical lows in 2023 of 0.3% overall, 1.8% excluding food and energy, or 2.5% excluding food, energy and trade, but each was below analyst expectations.

Separately, the U.S. Commerce Dept report on April retail sales confirmed a tariffobic drag. Retail sales, which had risen 1.7% in March, went up just 0.1% last month. Sales growth in the latest three months amounted to 0.9% relative to the average in Nov-Jan. New jobless insurance claims last week stayed at the prior week’s level of 229 thousand and down from the 29-week high of 241k in the last full week of April.

ShareThis

ShareThisYou can leave a response, or trackback from your own site.