Market Snapshot February 3rd 2026 – The Concept Trading

Volatility incoming…

Data:

1) Global Rates / Yields — Key Benchmarks

- United States: Treasury yields firm; 2‑yr ~3.60–3.65%, 10‑yr ~4.25–4.30%, 30‑yr ~4.85–4.95% on mixed economic data and policy uncertainty.

- United Kingdom: 10‑yr Gilt ~4.50–4.55% as markets look past recent BoE rate hold signals and inflation remains elevated.

- Australia: 10‑yr ACGB ~4.80–4.90%, elevated amid inflation outlook uncertainties.

- Canada: 10‑yr GoC ~3.40–3.50%, broadly tracking U.S. moves amid commodity price pressure and weaker CAD.

- Euro Area: 10‑yr Bund ~2.90–2.95%, France OAT ~3.55–3.60%, Italy BTP ~3.50–3.55% with spreads contained.

- Japan: 10‑yr JGB ~2.30–2.33%, near multi‑year highs and underpinning global yields.

- Emerging markets: Mixed yield performance with some curve steepening amid risk appetite shifts.

2) Equity Index Moves

United States

- S&P 500 ~6,976 (+0.5%), Dow Jones ~49,407 (+1.1%), Nasdaq ~23,592 (+0.6%) — broad rebound after recent volatility.

Europe

- Euro Stoxx 50 ~5,975–6,000 (+0.4–0.7%), DAX ~25,000 (~+0.5%), CAC 40 ~8,180–8,200 (~+0.6%) — supported by defensive and financial stock gains.

- UK FTSE 100 reached record highs (~10,341, +~1.1%) on sector rotation despite commodity weakness.

Asia

- Nikkei 225 ~52,800–53,100 (flat to –0.3%), pressured by FX and rates; broader Asian indices mixed with EM outperformance flows.

3) Prior‑Day Macro / “Red News”

- S. inflation data: Core PCE — Fed’s preferred measure — remains elevated with a brisk monthly gain, reinforcing a “higher for longer” view on U.S. policy.

- BoE signal: Bank of England expected to hold rates at 3.75% amid persistent UK inflation, with market chop around potential timing of cuts.

- Commodities rout: Sharp sell‑offs in gold, silver and oil weighed on risk assets and commodity‑linked FX.

- Emerging markets: Strong January inflows highlighted robust EM equity demand, contrasting developed markets’ cautious sentiment.

4) High‑Impact Market Headlines

- S. stocks rebound: Major U.S. indexes climbed on Monday, erasing part of recent losses and nearing record levels, led by cyclicals and small caps.

- $ Warsh Fed impact: Continued volatility after President Trump’s nomination of Kevin Warsh for Fed Chair, affecting yield curves and risk pricing.

- BoE moderation: Bank of England’s hold expectation tempered Gilt yields but kept focus on inflation/wage dynamics and March cut odds.

- Commodity selloff: Precious metals and oil plunged amid easing geopolitical tensions and rising yields, prompting defensive equity positioning.

- Currency moves: CAD weakened on commodity downturn; USD index broadly firmer, influencing global liquidity conditions.

- EM equity resilience: Emerging markets sustained strong inflows through January, signaling persistent global risk appetite outside DM.

- Tech/Ops dispersion: Divergent earnings reactions (e.g., Meta outperformed, others lagged) underscored differentiated sector trends in risk assets.

Companies.

+) Alphabet traded lower as investors reacted to earnings commentary highlighting slower near-term advertising growth, despite continued progress in AI-driven search and cloud monetization.

+) Amazon remained under pressure following results, with the market focused on AWS margin normalization and disciplined capex, even as retail efficiency continued to improve.

+) Nvidia declined as investors extended profit-taking in AI leaders, reflecting valuation sensitivity rather than any deterioration in demand fundamentals.

+) Advanced Micro Devices traded weaker in sympathy with the broader semiconductor complex, as markets reassessed AI accelerator competition and pricing dynamics.

+) Microsoft held relatively firm, supported by confidence in enterprise software resilience and sustained AI-driven cloud demand.

+) Tesla remained volatile, with ongoing debate around global pricing pressure, margins, and intensifying EV competition.

+) Lockheed Martin and Northrop Grumman outperformed modestly, underpinned by defense spending expectations and geopolitical risk.

+) UnitedHealth and Humana remained subdued, as Medicare reimbursement uncertainty continued to cap upside in managed-care stocks.

+) Pfizer traded narrowly after earnings, with investors focusing on cost discipline and pipeline execution amid declining COVID-related revenues.

+) Exxon Mobil and Chevron moved little, supported by capital-return commitments and stable crude prices.

+) Procter & Gamble and Coca-Cola saw mild inflows as investors rotated toward defensive, cash-generative names early in the month.

+) Netflix consolidated recent gains, with the market reassessing advertising-tier growth versus content spending discipline.

** Winners/ Losers: (in 28Jan)

| Ticker | Company | Move | Key Driver |

| LMT | Lockheed Martin | +1–2% | Defense spending expectations |

| UNH | UnitedHealth | +1% | Technical rebound |

| PG | Procter & Gamble | +1% | Defensive inflows |

| JNJ | Johnson & Johnson | +1% | Healthcare stabilization |

| DUK | Duke Energy | +1% | Utility demand |

| Ticker | Company | Move | Key Driver |

| NVDA | Nvidia | -2–3% | Profit-taking |

| AMD | Advanced Micro Devices | -2% | Semi consolidation |

| META | Meta Platforms | -1–2% | Valuation pause |

| TSLA | Tesla | -1–2% | Margin debate |

| ROKU | Roku | -2% | High-multiple pressure |

General

Currency Overview: FX markets remain disciplined as investors reassess early-February macro risks

G10 FX traded with subdued volatility as markets transitioned into February, with positioning anchored to relative monetary-policy paths rather than directional risk appetite. Liquidity conditions were normal, but conviction remained limited as investors balanced easing inflation trends against uneven global growth signals.

EUR: Euro softens modestly as weak Eurozone momentum continues to weigh

The euro edged lower as fragile activity data and subdued credit demand reinforced concerns about the Eurozone growth outlook. While ECB policy expectations remained broadly stable, the lack of positive catalysts limited EUR inflows, keeping price action driven by rate differentials rather than cyclical optimism.

GBP: Sterling trades defensively amid persistent UK growth and fiscal constraints

Sterling underperformed slightly as investors revisited concerns over weak domestic growth and fiscal sensitivity. Support from global rate dynamics proved insufficient to offset local headwinds, leaving GBP lagging peers.

USD: Dollar firms marginally on liquidity preference and cautious sentiment

The U.S. dollar found incremental support as investors favored liquidity and balance-sheet strength at the start of the month. Although expectations for gradual Fed easing remained intact, relative U.S. growth resilience continued to underpin the greenback.

JPY: Yen remains pressured as carry dynamics dominate low-volatility conditions

The yen stayed weak as stable global yields and compressed volatility encouraged continued carry positioning. In the absence of fresh policy signals from Japanese authorities, JPY remained driven by external rate differentials rather than safe-haven demand.

Precious Metals: Gold and silver consolidate as hedge demand persists

Gold and silver traded in narrow ranges, supported by contained real yields and ongoing portfolio-hedging demand. However, calmer risk sentiment and a firmer dollar limited momentum-driven inflows into precious metals.

Energy: Oil prices trade cautiously as demand uncertainty regains focus

Brent and WTI moved sideways to slightly lower as markets refocused on uncertain global demand prospects. Supply discipline and geopolitical risks remained background supports, but insufficient to drive a sustained rebound.

Equity Flow: Investors favor defensives and earnings visibility

Equity flows reflected continued late-cycle discipline, with investors favoring large-cap quality, defensives, and sectors offering clearer earnings visibility. Broader risk appetite remained selective rather than expansionary.

Geopolitics: Strategic tensions persist without triggering market stress

Major geopolitical themes—including U.S.–China strategic competition and ongoing regional conflicts—remained unchanged during the session. These risks continued to weigh on medium-term sentiment without provoking abrupt market repricing.

Upcoming News

Markets move into Tuesday with a data-reactive, positioning-sensitive tone, as investors build exposure around U.S. labour- and services-sector signals early in the month. Overall market sense is cautiously constructive, supported by easing inflation expectations, but conviction remains selective as participants look for confirmation that growth momentum is stabilising rather than rolling over. FX and rates volatility is expected to cluster around U.S. labour data and services activity, while equities remain focused on demand durability.

In the United States, attention centers on Job Openings (JOLTS) and Factory Orders, which together provide a timely read on labour-market tightness and manufacturing demand after January’s inflation and PCE signals. Markets will assess whether labour demand continues to cool in an orderly fashion—consistent with the Fed’s desired trajectory—or shows renewed tightness that could delay easing expectations. A softer JOLTS print would likely weigh on the USD and support front-end Treasuries, while resilience could cap rate declines into the mid-week data flow.

Across Europe, the focus remains on inflation and labour-market spillovers, with EUR trading primarily off U.S. yield differentials rather than fresh domestic catalysts. In the Asia–Pacific region, Australia’s retail sales provide insight into household demand and RBA expectations, while China remains largely headline-driven following the Caixin PMI. Corporate catalysts remain limited, leaving macro confirmation and positioning dynamics as the dominant drivers.

| Time (GMT+7) | Category | Country / Region | Event | Market Relevance |

| 08:30 | 🔴 Red News | Australia | Retail Sales (m/m) | Household demand; AUD and rates sensitivity |

| 16:55 | 🔴 Red News | Germany | Unemployment Change | Labour-market slack; EUR sentiment |

| 20:30 | 🔴 Red News | United States | Factory Orders (m/m) | Manufacturing demand; USD & rates impact |

| 22:00 | 🔴 Red News | United States | JOLTS Job Openings | Labour-market tightness; Fed path implications |

| All day | 🔶 Stress / Headlines | Global | Labour-market repricing / policy headlines | Can amplify FX and rates moves |

Snapshot

FX

- DXY rebounded to 60 (+0.47%), extending a technical recovery after recent sharp losses.

- EUR/USD eased to 1798 (+0.06%), consolidating near multi-week highs.

- GBP/USD edged higher to 3672 (+0.07%), maintaining a firm short-term bias.

- USD/JPY slipped to 42 (-0.12%), as yen strength resurfaced modestly.

- USD/CHF declined to 7790 (-0.08%), tracking the softer Swiss franc dynamics.

- USD/CAD edged lower to 3674 (-0.06%), despite stabilizing oil prices.

- AUD/USD advanced to 6955 (+0.10%), while NZD/USD rose to 0.6096 (+0.17%), outperforming among G10 FX.

Crypto

- Bitcoin rebounded to $78,689 (+2.3%), recovering part of the prior selloff.

- Ethereum climbed to $2,345 (+3.4%), supported by broader risk recovery.

- Solana advanced to $104.47 (+3.8%).

- Optimism (OP) rose to $0.230 (+1.3%), stabilizing after heavy losses.

Commodities

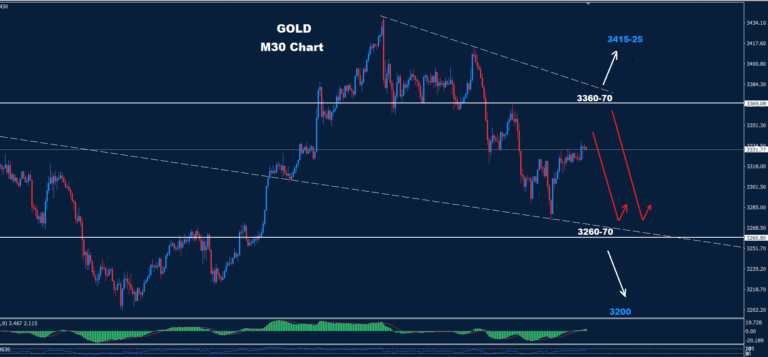

- Gold surged to $4,767/oz (+2.3%), rebounding sharply after the prior session’s selloff as risk sentiment stabilized.

- Silver jumped to $82.50/oz (+4.1%), continuing its higher beta response to gold’s rebound.

- Copper rose to $5.93/lb (+0.9%), supported by short-covering and improved risk appetite.

Equities / Indices

- S&P 500 climbed to 6,996 (+0.21%), recovering modestly after recent weakness.

- Euro Stoxx 50 rose to 6,033 (+0.19%), tracking the U.S. rebound.

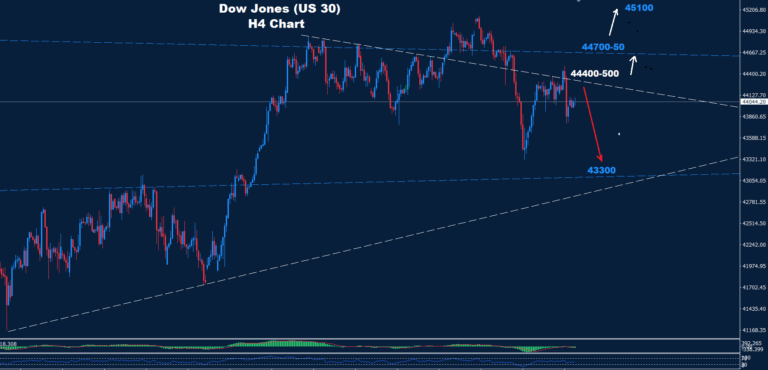

- Dow Jones gained to 49,457 (+0.12%), supported by cyclical stocks.

- Nasdaq 100 outperformed at 25,739 (+0.73%), led by tech rebound flows.

- CAC 40 advanced to 8,181 (+0.67%), showing relative strength.

- VIX slipped to 07 (-0.84%), signaling easing near-term market stress.

P/s: Weekly Snapshot will be incoming. Stay tuned.

This report is provided to The Concept Trading from Van Hung Nguyen