Options Slippage And Exit Problems: How To Avoid Getting Trapped

Sometimes you can enter a trade when the market is calm – even in a slightly illiquid stock.

But when there is panic in the market, and prices are moving fast, and people need to exit their trades, liquidity may become an issue.

Some orders may become difficult to get filled.

With options, it becomes even more complex.

Because options liquidity depends not just on buyers and sellers, but also on:

- market makers quoting the bid/ask

- open interest

- volume

- Whether the order contains multiple leg option structures

Contents

In general, the width of the bid/ask spread is a good indication of liquidity.

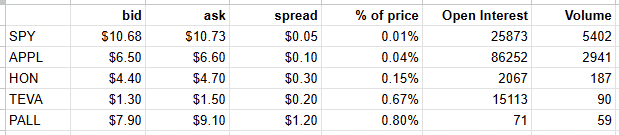

The S&P 500 ETF (ticker symbol SPY) is one of the most liquid underlyings.

As an example, an at-the-money call option with 30 days to expiration might cost anywhere from $10.68 to $10.73 per share.

That would be $1068 to $1073 to buy one contract (since one contract represents 100 shares).

Since prices are quoted on a per-share basis, we say that $10.68 is the bid price and $10.73 is the ask price.

The mid-price is $10.70.

The bid price is the price buyers are willing to pay.

The ask price is the price that sellers want to sell at.

This bid/ask spread is 5 cents wide.

This is a tight bid/ask spread indicating superior liquidity.

Apple (AAPL) is also very liquid.

An at-the-money call option with 30 days to expiration has a bid spread of $0.10 from a bid of $6.50 to an ask of $6.60.

Honeywell (HON) is less liquid, with a bid-ask spread of $0.30 from $4.40 to $4.70.

Palladium (PALL) has a spread of $1.20, with the bid/ask at $7.90 to $9.10.

Since bid/ask spreads are naturally wider on higher-priced assets, we also look at the spread width as a percentage of the asset price.

AAPL’s stock price is around $270, so $0.10/$270 = 0.04%.

The stock price of HON is around $200, so $0.30/$200 = 0.15%.

The stock price of PALL is around $150, so $1.20/$150 = 0.80%.

Teva Pharmaceuticals (TEVA) is a lower-priced stock at $30 per share.

So even though its bid/ask spread of $0.20 may seem small.

As a percentage of its stock price, it is $0.20/$30 = 0.70%.

This is considered illiquid.

As a general guideline for a one-option contract:

: excellent liquidity

0.05% – 0.15%: tradable, but work orders

0.15% – 0.30%: marginal, be cautious with multi-leg trades

> 0.30%: poor liquidity; expect slippage

Traders will also look at the volume and open interest.

The higher these numbers are, the more liquid the options are.

This is not a concern for very liquid options such as SPY and AAPL.

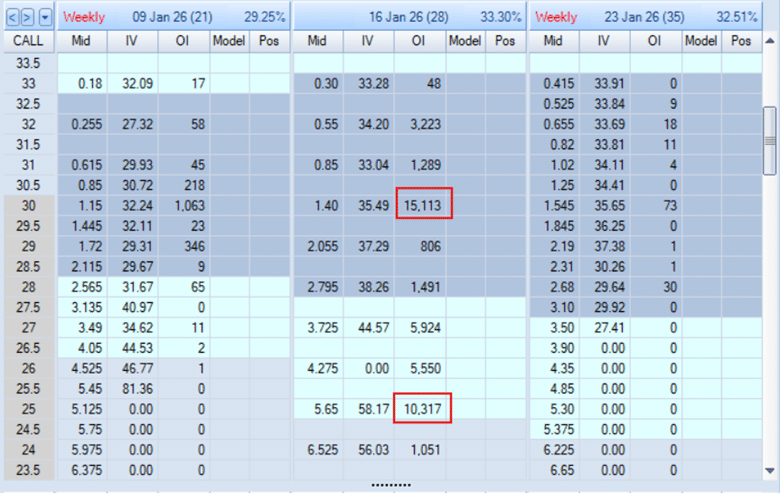

But liquidity can vary across strikes and expirations for less liquid underlyings, such as TEVA…

Here we see that the open interest of 15,000 is particularly high for the $ 30 call option with the January 16th expiration.

The next-highest is at the $25 strike, with 10,000 of open interest.

That is because these are round numbers or at 5-point increments rather than odd strikes such as $27 or $27.50.

We also notice that the monthly expiration of Jan 16 has higher open interest than the weekly expirations of Jan 9th and Jan 23rd.

With TEVA currently trading at $30, we see that near-the-money strikes are where volume and open interest cluster, so spreads tend to be tighter there than in far-out-of-the-money wings.

Similarly, nearer-dated expirations generally trade with heavier volume than options with long-dated expirations, making them easier to exit at a fair price.

During the course of a trade, an option may have gone far out-of-the-money with the strike price being very far away from the current price of the underlying.

If an option is far out of the money (OTM) and no one wants to buy it, the trader might not be able to exit or sell it to close it.

This is especially true for options expiring on the same day, because far OTM options have very little extrinsic value left, and no one wants them.

They may be worth less than $0.05.

It will be difficult to close.

They might just have to leave it to expire.

When a trade has multiple legs, poor liquidity is compounded.

For example, a bullish put spread credit on TEVA consists of selling one put option and buying another put option.

These two option legs create one order.

The bid-ask spread for the order may be a credit of $0.10 to $1.08.

That is nearly a $1.00 difference in price.

For a one-contract bull put spread, that is a $108 credit on the trade versus a $10 credit, nearly a $100 difference.

In this case, the trader may want to consider alternative ways to be bullish on TEVA.

Perhaps buying a call option or selling a put option, since slippage on a single option is less than with a multi-leg order.

But because this is such a low-priced stock, the trader may need to buy multiple contracts for profits to be meaningful.

So now commissions and fees are stacked on top of slippage.

In this case, maybe just buy the stock instead (as an options investor, I don’t say this often).

The bid-ask spread for stock orders is tighter than that for options orders.

Or perhaps sell a put option to potentially own the stock as a Wheel trade.

Iron condors and the like are four-legged trades.

To get better fill execution, some traders will break up the iron condor into two orders instead of filling the whole condor in one order.

The trader would use one order to fill the put spread and another order to fill the call spread.

Just make sure the two orders fill around the same time to avoid directional risk.

With that said, there are some underlyings where the liquidity is just too low for doing a four-legged trade.

In our examples, TEVA and PALL would not be good candidates for condors.

Even credit spreads would be difficult.

Working the order means negotiating fills with patient limit orders to secure better pricing, both on entry and exit.

Don’t use market orders with options.

When entering an order, start by putting in a favorable price.

If selling an option, you want to sell at a high price (higher than the quoted mid-price).

When buying an option, you want to buy it below the mid-price, if possible.

This is known as a “resting order”.

The order sits there waiting for your favorable price to fill.

It is up to the trader how long to wait based on urgency and availability.

It may be a few minutes or perhaps a few hours.

If not filled, the trader would cancel and replace the order to move the price closer to the mid-price, little by little, until filled, if filled, at around mid-price, that is good.

For less liquid options, it may not fill at mid-price.

The trader may go beyond the middle, giving in to an unfavorable price.

The amount the trader is willing to give up to get a fill is known as slippage.

By giving up some slippage, a trader may still get illiquid options to fill.

But the trade had better be good in order to achieve a large enough profit to compensate for this slippage.

If the trade turns bad (such as during a market crash when prices are moving quickly), exiting the trade may become a problem.

The trade can be entered, but now it cannot be exited.

Or at least, not exited at a fair price.

The problem with illiquid options is that now the trader loses on slippage to enter and on slippage to exit.

Many analytical or backtesting software use mid-price for its calculations.

This can lead to misleading profit and loss figures in risk graphs and paper trading results because it does not account for slippage.

For illiquid options, they don’t get filled at mid-prices due to market factors.

They get filled at prices less favorable than mid.

A position may look profitable on paper, but if you can’t exit at a fair price, slippage and widening spreads can destroy returns.

The liquidity of the options that you trade should not be an afterthought.

It should be considered in the trade from the beginning.

A trader may be able to enter the trade or even be willing to accept some slippage.

Still, market factors can affect the bid-ask spread during the trade in ways that make exiting the trade difficult, or the trader might have to accept unfavorable pricing at the exit.

This erodes the profits.

Q: Can I just use market orders to guarantee my exit?

Absolutely not. Market orders on illiquid options will destroy you with slippage. You might get filled, but at a price 50-100% worse than mid-price. Always use limit orders and work them patiently. Only cross the spread incrementally when necessary. Market orders should be your absolute last resort in emergencies only.

Q: What if my analytical software shows the position is profitable, but I can’t close at those prices?

Many analytical and backtesting software use mid-price for calculations. This gives misleading P&L values because real fills don’t happen at mid on illiquid options – they happen at prices less favorable than mid. Always mentally subtract 30-50% from theoretical profits on illiquid names to account for slippage. If it’s still worth doing, proceed. If not, skip it.

Q: Should I avoid weekly options entirely on less liquid stocks?

For stocks with bid/ask spreads over 0.15%, yes – avoid weeklies. Weekly expirations have lower volume and open interest than monthlies. On illiquid names, this makes exit problems worse. Stick to monthly expirations where the options have better liquidity. Weeklies are fine on SPY, QQQ, AAPL – terrible on TEVA, PALL, or small-cap names.

Q: What’s the best way to exit a multi-leg trade on an illiquid stock?

Break the trade into smaller pieces. For iron condors, close the put spread and call spread as separate orders (nearly simultaneously). For credit spreads that are far OTM and worthless, close the tested leg and let the untested leg expire worthless – don’t pay slippage to close something worth $0.05. Work each piece patiently with limit orders.

Q: How much slippage should I budget for on each trade?

On liquid names (SPY, AAPL): 5-10% of the premium. On moderately liquid names: 15-25% of premium. On illiquid names: 30-50%+ of premium. If slippage eats more than 20% of your expected profit, the trade probably isn’t worth doing. Factor slippage into your profit targets before entering.

Q: Can I improve my fills by trading during specific times of day?

Yes. Best liquidity occurs during market open (9:30-10:30 AM ET) and the last hour (3:00-4:00 PM ET). Avoid trading options during lunch (12:00-2:00 PM) when volume dries up, and spreads widen. For illiquid names, stick to peak trading times when market makers are most active.

Q: What if I absolutely need to exit and can’t get filled at any reasonable price?

You have a few options: (1) Wait – sometimes stepping away for 30-60 minutes and trying again helps, (2) Break multi-leg orders into pieces, (3) For undefined risk positions, consider hedging with stock instead of closing options, (4) Accept significant slippage if you truly must exit immediately. This is why pre-trade liquidity checks are so critical – to avoid this situation entirely.

Q: Are there any brokers or platforms better for getting fills on illiquid options?

Active trader platforms like Interactive Brokers and Thinkorswim offer better smart routing, which can improve fills. They try to find liquidity across multiple exchanges. But no platform can create liquidity that doesn’t exist. Even the best routing won’t help much on truly illiquid options. Focus on trading liquid names rather than depending on technology to fix liquidity problems.

Liquidity problems aren’t obvious when you enter trades during calm markets – but they become painfully clear when you need to exit, especially during volatility.

Key Lessons:

✓ Check liquidity BEFORE entering – Use the pre-trade checklist

✓ Calculate spread percentage – Not just dollar width

✓ Multi-leg = multiply problems – Each leg adds slippage

✓ Work orders patiently – Never use market orders

✓ Budget for slippage – Factor it into profit expectations

✓ Match strategy to liquidity – Iron condors need better liquidity than single options

✓ Exit problems worsen in volatility – Spreads widen during crashes

The fundamental truth: You can enter an illiquid trade and even accept some slippage. But if the trade goes bad or markets crash, exiting becomes a crisis. Slippage on entry + massive slippage on exit can turn manageable losses into disasters.

The solution: Trade only sufficiently liquid names for your strategy. Accept lower premiums on liquid names rather than chasing extra pennies on illiquid ones.

Learn to measure liquidity properly: How to Measure Options Liquidity: Ultimate Guide.

Understanding which strategies work on which stocks – considering liquidity, volatility, and other factors – is crucial for consistent profitability:

Options Income Mastery: Learn systematic approaches to selecting strategies and managing positions with proper risk management ($397)

The Accelerator Program: Advanced training covering position management, adjustment techniques, and portfolio-level strategy ($997)

We hope you enjoyed this article on options slippage and exit problems.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Source link