Double Calendars On Pricey Stocks

A calendar spread in options consists of selling a short-term option and buying a longer-term option.

Both options are at the same strike price and underlying asset.

The calendar can consist of both call options – one short option (the call option that we are selling) and one long option (the call option that we are buying).

Or the calendar can consist of both put options – one short put and one long put.

A double calendar is an options strategy that combines a call calendar and a put calendar.

The call calendar is placed with the strike price above the current price of the underlying.

The put calendar is placed below the current price.

Contents

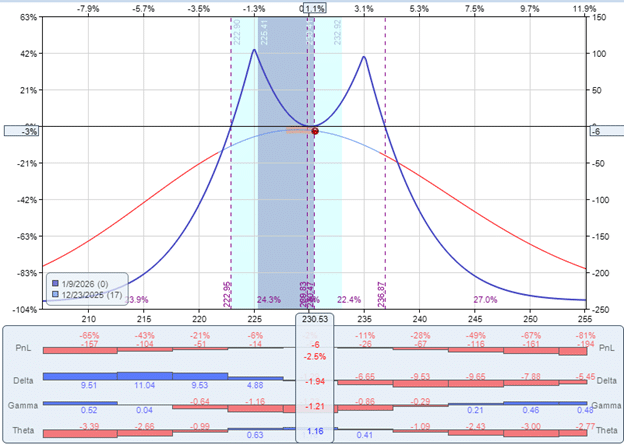

In this example of a double calendar on AbbVie (ABBV), the short put option and short call option expire in 17 days.

The long put and long call options expire one week after that.

Date: Dec 23, 2025

Price: ABBV @ $230.50

Buy to open one contract Jan 16 ABBV $225 put @ $3.72

Sell to open one contract Jan 9 ABBV $225 put @ $2.22

Buy to open one contract Jan 16 ABBV $235 call @ $3.33

Sell to open one contract Jan 9 ABBV $235 call @ $2.43

Debit: -$240

Commission: $2.60

Here we paid a debit of $240 for both calendars.

This is the max that we can lose on the trade.

Assuming that commission costs $0.65 per contract to open and close, we calculated the commissions to open the double calendar to be $2.60.

The strike prices of $225 and $235 are quite far apart.

We don’t want it any further apart than this.

Looking at the expiration payoff diagram, we see that the sag in the middle is quite low.

It shows zero profit at expiration if the price stays at $230.

If we move the strike prices further apart, the graph may dip below the zero-profit horizontal, showing negative profits at that point.

We would not want this.

Keep in mind that the sag only occurs at or near expiration.

During the course of the trade, it is better to watch the T+0 line.

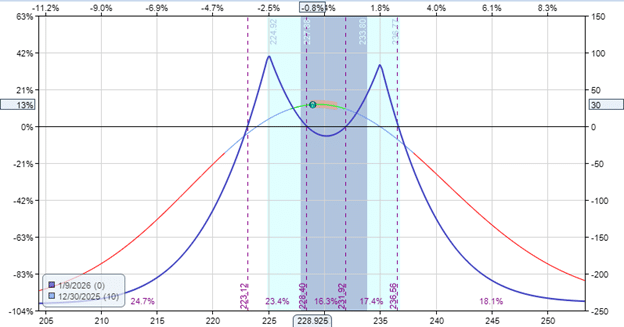

One week later, midway through the trade, we see that the T+0 line has popped above the expiration graph:

This is the positive theta at work, raising the T+0 line and giving the trade $30 of profits.

We close the trade by…

Date: Dec 23, 2025

Price: ABBV @ $228.9

Sell to close one contract Jan 16 ABBV $225 put @ $2.75

Buy to close one contract Jan 9 ABBV $225 put @ $1.22

Sell to close one contract Jan 16 ABBV $235 call @ $2.83

Buy to close one contract Jan 9 ABBV $235 call @ $1.66

Credit: $270

Commission: $2.60

Since we paid $240 and we now sell at $270, the profit is $30.

This is a 12.5% return on the capital at risk, excluding commission.

$30 / $240 = 12.5%

However, the total commissions to open and close all those options amounted to $5.20, which would have degraded this return by about 2%.

$5.20 / $240 = 2%

The net profit returned, taking into account commission, is about 10%.

$24.80 / $240 = 10%

This is the minimum profit target that we would want for double calendars.

Because the double calendar consists of four option legs, commissions should be a consideration.

Fortunately, this trade did not need to be adjusted; otherwise, commissions would even higher.

This example was for a pricey stock like AbbVie, which trades at about $230 per share.

If we were to try this on a low-priced stock like Cisco (CSCO) at $75 per share or Intel (INTC) at $40 per share, the achievable profits per contract would be too small relative to the commissions we would have to pay.

Therefore, it is best to trade double calendars on pricey stocks.

Low-priced stocks also lack the granularity of strike prices to choose from.

With pricey stocks like ABBV, we can better select different strike prices.

We can select strikes that are closer together.

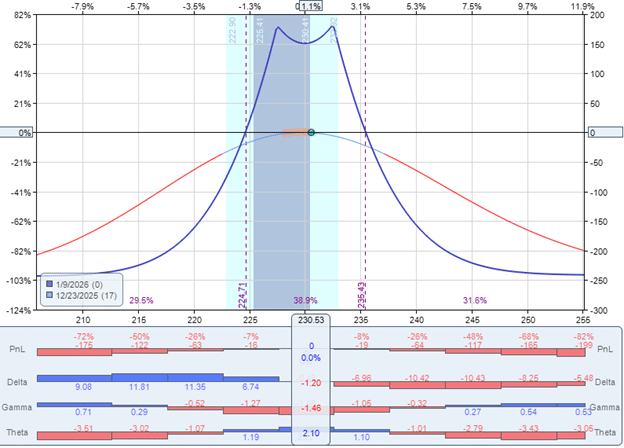

Here is another example.

Date: Dec 23, 2025

Price: ABBV @ $230.50

Put calendar:

Buy to open one contract Jan 16 ABBV $227.50 put @ $4.48

Sell to open one contract Jan 9 ABBV $227.50 put @ $2.95

Debit: -$153

Commission: $1.30

Call calendar:

Buy to open one contract Jan 16 ABBV $232.50 call @ $4.53

Sell to open one contract Jan 9 ABBV $232.50 call @ $3.63

Debit: -$90

Commission: $1.30

This time, we are placing two orders: one for the put calendar and one for the call calendar.

No difference; we still have to pay the same in total commissions.

The expiration graph looks quite different because the strike prices of the calendar are closer together…

The sag in the middle is much higher up.

This is indicative of much higher theta at the start of the trade.

Reading the theta from this histogram at the center of the graph, where the price is at $230, we see this trade has a theta of 2.10.

The example before only has a theta of 1.16.

Note also that the larger theta is, the larger gamma’s magnitude is too.

The gamma of -1.46 in this example versus the gamma of -1.21 in the previous example.

The tradeoff is that this trade has a narrower profit range.

Here we see that the expiration breakeven points are $225 and $235.

These are the prices at which the expiration graph crosses the zero-profit horizontal axis.

It means that the trade is profitable as long as ABBV is between $225 and $235 at expiration.

In the previous example, the breakeven points are further apart at $223 and $236.

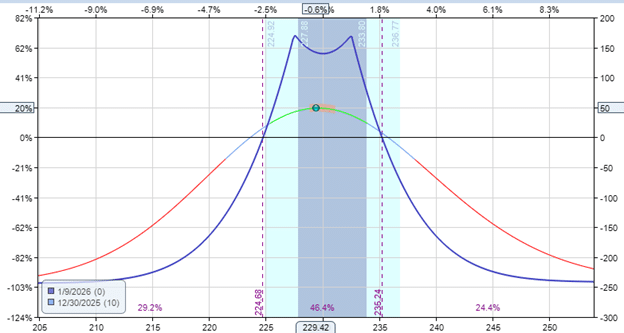

Note that breakeven points for time spreads can change slightly over the course of the trade.

In this case, the narrower double calendar turned out to have a slightly better profit of $50, or about 20% return on capital (excluding commissions)

One reason this trade worked out is that the price stayed within a one-standard-deviation range, and the 20-day and 50-day simple moving averages were relatively flat at the start of the trade.

Also, in general, we don’t want to hold the double calendar trade through stock earnings announcements, as the price can make a big move.

Some pricey underlyings suitable for double calendars may include the large indices such as SPX and RUT.

Or their ETF equivalents: SPY and IWM.

DIA is a good one for the Dow Jones ETF.

The Magnificent Seven stocks have grown to high and healthy prices:

Apple (AAPL)

Microsoft (MSFT)

Alphabet (GOOGL)

Amazon (AMZN)

NVIDIA (NVDA)

Meta Platforms (META)

Tesla (TSLA)

Some more potential individual stocks to try double calendars may include…

ABBV – AbbVie

LLY – Eli Lilly

GLD – gold ETF

ORCL – Oracle

IBM – IBM

CVX – Chevron

BA – Boeing

DIS – Disney

GILD – Gilead

Double calendars are best done on expensive stocks, because commissions can eat up about 2% of the profits (before adjusting the trade).

High-priced stocks also have more strikes to choose from, enabling the trader to configure the expiration graph for either better theta or a wider profitability range.

We hope you enjoyed this article on double calendar spreads for high-priced stocks.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Source link