Is It Possible To Buy An Options Calendar Spread For Zero Cost?

The short answer is no.

The traditional options calendar, where we sell a near-term option and buy a longer-term option at the same strike, would always be at a debit.

The two options must be both puts or both calls.

Let’s use a put-calendar as an example.

Contents

On January 27th, 2026, Kimberly-Clark (KMB) stock was trading at $101.38 per share.

An investor sells a 100-strike put option that expires on February 13, 2026 (17 days from now).

This is known as the short option because it is being sold.

He buys the 100-strike put option that expires on February 20th, 2026 (one week after the short option’s expiration).

Date: Jan 27, 2026

Price: KBM @ $101.38

Sell one contract Feb 13 KMB $100 put @ $1.55

Buy one contract Feb 20 KMB $100 put @ $1.75

Net Debit: -$20

The value of the short option is quoted at $1.55 per share.

The value of the long option is quoted at $1.75 per share.

It is only a $0.20 difference.

Therefore, a one-contract calendar will cost $20 since one contract represents 100 shares.

While this is certainly a low-cost calendar, it is not a zero-cost calendar.

With all other factors being equal, investors prefer to pay as little as possible for the calendar because the maximum risk of a calendar trade is the debit spread.

Therefore, the lower the cost, the lower the risk.

The lower the risk, the better the reward-to-risk ratio.

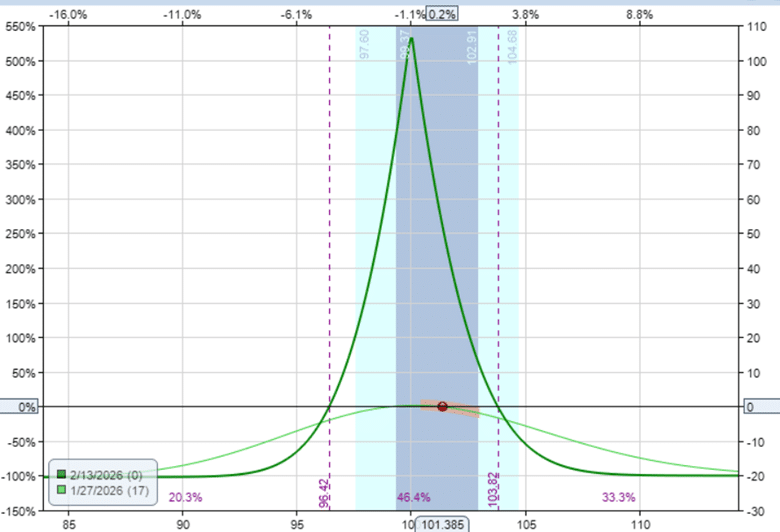

The payoff graph of our example shows that the calendar has a 5:1 reward-to-risk ratio, with the possibility of earning up to $100 by risking only $20.

The long option with more days to expiration is always priced higher.

That is because the extra days till expiration have value.

The holder of the option has more time to be right, or more time for the stock price to move in the investor’s favor.

Therefore, there is value in having more time.

This extra value is embedded in the “extrinsic value” of an option.

The other portion of the option’s value is the “intrinsic value”.

While some people loosely call extrinsic value the “time value”, this is not entirely accurate because the extrinsic value also contains the embedded value of the implied volatility of an option.

For options of the same type (puts, for example), and with the same strike on the same underlying, the option with more time will always cost more.

Therefore, a calendar executed in a single order cannot be provided at zero cost.

The value of the longer-dated option that is being bought will be higher than the value of the shorter-dated option that is being sold.

The longer-dated option is more valuable than the shorter-dated option even when the latter has a higher implied volatility (IV).

In general, an option with higher implied volatility will have a higher value.

Think of an option with high implied volatility as expensive, while an option with low IV as cheap (relatively speaking).

If the shorter-dated option has higher implied volatility, one might expect its value to increase until it equals that of the longer-dated option, thereby achieving a zero-cost calendar.

Having higher implied volatility in the shorter-dated option certainly helps reduce the cost of the calendar down, but never to the point of zero.

In our example, the IV of the shorter-dated option was 25.13, which exceeded that of the longer-dated option at 23.17.

This is a two-point difference, which is a very large IV skew in our favor.

We are selling an expensive option and buying a cheap option.

The cost of the calendar is low, but still not zero.

While the liquidity of Kimberly-Clark’s options is adequate, it is not considered highly liquid.

Hence, it may have a fair amount of bid/ask spread.

The option price quoted in our example was the mid-price.

In live markets, the trading platform may display the price of each option fluctuating between the bid and ask prices.

When both options are placed in a single order, the net quoted cost may fluctuate and may at times be zero.

This is due to momentary cross-quoting of the bid and ask.

However, it is highly unlikely that you would get filled at zero cost.

If you have, then consider yourself lucky because market makers (which are mostly machines) run arbitrage bots that remove such crossed quotes.

Similarly, you may see options analytical software displaying mid-prices that have crossed.

Understand that this will likely not be filled in live markets.

This is also why your analytical and backtesting software, which calculates P&L based on mid-prices, may show profits when, in reality, it is not present in live markets.

When we say “buying a calendar,” we mean buying the calendar in a single transaction.

We are not talking about selling a short-dated put option first and then buying a longer-dated option later.

This is known as “legging into a calendar.”

In that case, if the market moves in your favor after you enter the first leg, you might be able to buy the second leg at a more favorable price such that your calendar is at zero net cost.

We don’t call this buying the calendar at zero cost, because you are actually using the profits achieved by the first leg to help pay for the purchase of your second leg.

While the idea of a zero-cost calendar spread is appealing, the reality of modern options markets makes such a trade effectively impossible.

A true calendar, by definition, pairs a longer-dated option with a shorter-dated option at the same strike.

Because the longer-dated contract always contains more extrinsic value, the position must begin as a net debit.

Brief moments where the spread appears to cost nothing are simply caused by bid/ask fluctuations, which may not be able to fill at the prices shown.

Nevertheless, the trader seeks to pay as little as possible for the calendar to reduce risk and maximize the reward-to-risk ratio.

We hope you enjoyed this article on buying a zero-cost options calendar spread.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Source link