March DDD 2026

The ETF traded at record volume today and is now up +289% year-to-date and roughly +605% over the past year.

$BWET is a financial proxy for global crude shipping demand, and today’s action suggests tanker utilization remains elevated.

The Takeaway: Historic strength in tanker shipping continues as the ETF extends to new record highs.

Decapitation is not the end. A rattlesnake thrashes around for minutes after losing its head. The guillotined showed signs of sensation and responded to stimuli in macabre 19th century experiments. Anne Boleyn’s lips moved as her head was displayed to the crowd after her execution.

All of this gruesome detail is to demonstrate that killing the top leaders doesn’t mean that the Iranian regime is over. It may well yet be able to acquire a new head (not an option for flailing chickens). Even if not, its death throes could be violent and unpredictable.

And if these images are distasteful, there is also something rather distasteful — as always — about the many market notes of the last 24 hours explaining that carnage and loss of life will probably not cost investors much money. Oil supply is highly unlikely to be disrupted in the way that it was in the 1970s, and other factors, such as strong earnings growth and likely lenient fiscal and monetary policy, are more important. This analysis is historically correct, but it’s still unpleasant.

And the facts remain that Iran is determined to inflict pain on its attackers (even if it cannot win a conventional war). This is not how it reacted last summer when the US bombed its nuclear facilities, and there have been no significant military reprisals in any of the other Trump 2.0 geopolitical events to date. Even though beheaded, the Islamic Republic is unpredictable and dangerous.

Bearing all this in mind, the market reaction to a war that has suddenly expanded to include peaceable enclaves like Dubai has been remarkable for its calmness.

Oil

This chart from Jim Reid of Deutsche Bank shows that the rise in Brent crude qualified as only the 38th biggest jump since 1980. As Bloomberg News colleague Cameron Crise put it, this was a “once-a-year response to a once-a-decade shock.” And Brent fell back a little after this graph was published:

Even with the Strait of Hormuz now de facto closed, the oil market is not yet that alarmed. Investors are accustomed to taking their cue from the oil price during events like this, and the relative calm in energy markets affected all other asset classes.

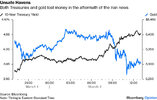

Havens

The two most important safe haven assets, gold and Treasury bonds, were the most truly dissonant with the geopolitical alarm, as both actually lost their investors money on Monday:

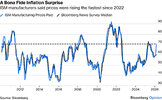

If this seems baffling, there was other news — which admittedly most people would consider less important than the dispatches from the Middle East. Most importantly, the regular Institute of Supply Managers survey for the US, long regarded as one of the better leading indicators of the economy, offered alarming signs of inflationary overheating. In particular, the number complaining of higher prices leapt to its highest since 2022, in the biggest surprise on record:

All else equal, this would tend to hurt bonds and cause yields to rise. And tariffs offer a natural explanation. The ISM publishes quotes from respondents, and they were unstinting in their anger over tariff policy. One said:

With complaints like this, the chances of rate cuts would seem to diminish, and with them the case for buying bonds. After a strong run in the last few days, the result was a big decline for a haven asset, even on a day when people needed shelter.Today, American-produced commodities like steel and aluminum are the highest-priced in the world, by far. Hence, the Section 232 tariff policy is having the exact opposite effect of their intention on an American manufacturer like us: It is raising prices while lowering demand and profitability.

The Dollar

The most traditional safe haven of all is the dollar, and it had its best day in eight months, with the DXY dollar index gaining almost 1%. That brought it above its 200-day moving average, the most widely followed measure of the long-term trend, for only the third time since Liberation Day nearly a year ago. Its first two tests of the trend in recent months proved fleeting. Whether this dollar gain is longer-lived will depend on whether the war expands:

How to explain the dollar’s strength, even though Treasuries were selling off? Freya Beamish of TS Lombard suggests that investors are slowly realizing that there is more risk of a pickup in inflation (a natural result of an oil price spike) than they’d thought. That explains the rise in the premium they demand to hold bonds for the long term:

The prospect of higher yields ahead, meanwhile, bolsters the dollar.We are in a world where those shocks are more likely but it takes investors a while to realize that, just as it took them a while to realize that these shocks were less likely in the 80s than the 70s.

Developed Equities

Most counterintuitively, US stocks had an unremarkable day, with the main indexes almost exactly flat. This wasn’t true of Europe, where the Stoxx 50 dropped 2.5%. It was also notable that some recently reliable trades are working less well. Defense stocks outperformed the index, as might be expected, but the effect has grown more muted with each of the Trump 2.0 shocks:

This is arguably a sign that investors are getting used to the new reality where US military support cannot be relied on, and believe that it is now adequately reflected in prices. In the US, Eric Liu of Vanda Securities shows that the relative strength was helped by strong interest from retail investors who bought aggressively at the opening of trade for the third day in a row, and also by institutions, many of whom will have been buoyed by research showing that it usually pays to buy geopolitically-driven dips.

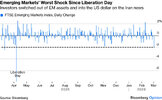

The flip side to all of this was an awful day for emerging markets.

Emerging Troubles

The Iran situation risks upending emerging markets’ recent poster-child status. While US stocks largely shrugged off the news, the FTSE emerging markets index dropped 2% for the day, its worst showing since last April in the aftermath of the Liberation Day tariffs.

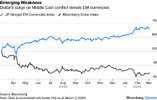

Other measures of emerging-market health show signs of stress, with currencies sliding as traders sought haven in the dollar. The JPMorgan basket of emerging market currencies is on a three-day losing streak, falling by the most in a month:

Whether this downturn lingers has a lot to do with the dollar’s performance. A weaker dollar is part of President Donald Trump’s flagship policy of reviving American industry. It’s plausible to expect a dollar rally to be relatively short-lived. However, the scale of the ongoing conflict and its potential to expand further may increasingly shape the dollar’s course.

EM strength has historically coincided with a weaker dollar, which explains why the sudden course reversal caused by the conflict had such a drastic impact:

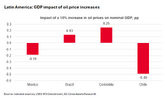

Still, how much shock emerging markets can withstand depends on idiosyncratic factors. Higher oil prices are beneficial for exporters and very much detrimental for net importers. In Latin America, the price surge might shore up growth in Brazil and Colombia while weighing on Mexico and Chile. Societe Generale’s Dev Ashish points out that this can still be a double-edged sword. Strong oil prices strengthen growth, fiscal accounts, and currencies in exporters but also push domestic inflation higher:

EM optimism has been driven to a large extent by strong earnings growth, and by the fact that many countries have been under-owned during years of American Exceptionalism. That gave them room to rise, and last year, the cohort gained nearly 33%. Sam Suzuki of AllianceBernstein points out that EM equities still trade at a sizable discount — which explains 2026 forecasts predicting that they would outpace developed markets again:

Monetary policy, with rates expected to come down from lofty levels, is a further support. These factors won’t change overnight, but would be unlikely to survive a devastating, prolonged war. The pass-through from an extended episode of higher oil prices could derail the projected easing and raise inflation risks. But Suzuki suggests that’s a reason for more cautious optimism, not outright pessimism:

Importantly, many countries have their fiscal house in order, which could help mitigate whatever shock the Iran fallout might bring. Oxford Economics’ Joshua Fisher notes that the emerging world has a better medium-term fiscal sustainability outlook than the developed markets.EM are not without risk and haven’t always lived up to their promise. Nonetheless, improving corporate fundamentals and corporate earnings growth could be signs that this isn’t just another short-cycle rebound —especially given the structural trends creating new opportunities.

Source: Oxford Economics

It’s a diverse picture, but the EM world is not in seriously bad health. The great risk would be resumed strength for the dollar. As long as the assumption of more rate cuts from the Fed still holds, emerging markets have a buffer to withstand shocks from the Middle East. The sooner this is all over, the better for everyone.

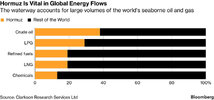

The biggest question in global energy markets this week is how willing and able Iran will be to enforce the closure of the Strait of Hormuz, and defense experts are warning not to underestimate the country’s capabilities.

On Monday, a senior Revolutionary Guards official told state media that the strait, which carries about 20% of global oil and LNG traffic, is “closed” and that Iranian forces “will set those ships ablaze” if they try to pass. Time is a critical factor: If Hormuz traffic is disrupted for a week or so, market prices should settle down quickly, and at around $80 per barrel, prices are still much lower, inflation-adjusted, than they were during most of the war in Iraq. But a closure much longer than that could trigger the biggest energy bottleneck in decades, with dire consequences for consumers.

Iran has a few options for enforcing this closure, defense experts told me. They could confront tankers directly with their own warships, but that would increase their vessels’ vulnerability to engagement with US forces, which, President Donald Trump said on Sunday, have already sunk nine Iranian warships.

The second option is to use land-launched missiles and drones to target passing ships. As of Tuesday morning, at least seven tankers, including one of Iran’s own, have been damaged in this way. Attacking those missile launchers is a high priority for the US and Israel; according to Israeli media, half have already been destroyed.

The third option is to lay sea mines in the Strait, which would make the situation “much more complicated,” Jonathan Panikoff, a former senior US intelligence official and director of the Atlantic Council’s Scowcroft Middle East Security Initiative, said. In the past, Iran has even used civilian vessels to lay mines, Mark Montgomery, a retired US Navy rear admiral and senior fellow at the Foundation for Defense of Democracies, told me. Sinking a few warships won’t solve the problem, he said: “We really need to destroy all Iranian Navy storage, logistics, and command facilities, so there’s a lot of work to be done.”

In the meantime, US Secretary of State Marco Rubio said the administration will announce on Tuesday measures to blunt the impact of price spikes on American consumers — but reportedly will not consider selling oil from the Strategic Petroleum Reserve.

The Iran conflict is creating a windfall for US natural gas exporters. Gas prices in Europe jumped more than 20% on Tuesday after Qatar said it had suspended operations at the Ras Laffan LNG export facility, the world’s largest, following drone attacks. That’s the biggest spike in European energy prices since the 2022 Russian invasion of Ukraine. And as in that case, this latest disruption will pit European and Asian LNG buyers against each other, to the benefit of US exporters. Mike Sobel, CEO of LNG exporter Venture Global, told shareholders on Monday the company “stands ready to help keep the markets stabilized.” The company’s share price closed up nearly 20% on Monday; rival Cheniere Energy also saw a sizable jump.

The gas market doesn’t have the same degree of supply flexibility as oil; there are few strategic reserves and little spare production or export capacity to fire up on short notice. Even the US can’t completely fill the gap left open by Qatar. For now, the price jump is far smaller than what Europe experienced in 2022. But if prices remain elevated, Goldman Sachs analysts warned, many lower-income countries could be forced to switch their power plants back to coal.

Insurance prices for oil tankers passing through the Strait of Hormuz could more than double, a leading broker told Semafor. Before conflict broke out over the weekend, insurance rates for most oil tankers in the region were around 0.25% of the value of the ship, said Marcus Baker, global head of marine and cargo for the brokerage and risk advisory firm Marsh. Now that Iranian forces have threatened to attack any ship entering the Strait, and followed through in several cases, many insurers are cancelling pre-existing war risk policies and looking to renegotiate at higher prices.

Although some insurers quickly angled for sky-high rates that Baker described as “nonsense,” the market hasn’t yet coalesced around a standard rate. But Baker said he expects that within the next day or so, rates will shake out at a level at least double what they were prior to the weekend. Still, he pointed out, that’s far lower than the eye-watering 5% rate that ships faced navigating the Black Sea at the beginning of the Ukraine invasion. Rates are likely to remain highly volatile until there’s a clearer indication of what the US Navy is willing and able to do, including potentially escorting convoys of tankers through the Strait. Even then, Baker said, some shipping companies and captains may decide that, insured or not, they simply don’t want to take the risk.

The upswing in global oil prices could drain political momentum for enforcing stronger sanctions against Russia. Russia’s oil and gas revenue is down by 27% compared to pre-2022 levels, thanks to US and European sanctions and overall low oil prices. But the Kremlin could be a key winner, at least temporarily, from turmoil in the Middle East, Luke Wickenden, sanctions analyst at the Center for Research on Energy and Clean Air, told Semafor. If major disruptions to physical oil supply materialize over the coming days, it will erode the leverage that countries such as China and India have used to extract steep discounts from Russia, Wickenden said. Western governments may also be less inclined to enforce existing sanctions or apply new ones in a highly-constrained energy market — although Belgium seized a Russian shadow fleet tankeras recently as Saturday, and the new sanctions bill in the US Senate was already bogged down before the Iran situation began.

In the meantime, Senate Democrats are still pushing for a separate bill to target Russia’s shadow fleet. “We would hope that Western sanctions policy remains anchored in Russia’s geopolitical aggression rather than short-term oil price movements,” Svitlana Romanko, director of the Ukrainian advocacy group Razom We Stand, told Semafor.

Green energy generation in the US hit record highs last year, despite repeated efforts by the Trump administration to sideline it.

More than a quarter of US electricity came from renewable sources in 2025, up from 10% the prior year, the EIA found. Solar and wind, both of which lost their federal tax credits last year and have been frequent targets of US President Donald Trump’s broadsides, remained the fastest-growing electricity source in the country. Although a surge in energy demand has driven up power generated from fossil fuels, renewables are accelerating beyond those gains, mostly for economic reasons. The cost of photovoltaic panels, wind turbines, and grid-scale batteries has fallen low enough that building new renewable capacity remains cheaper than most alternatives, with or without government subsidies. Investors have evidently caught on: Nearly 80% of the power plant capacity planned over the next decade is tied to renewable sources.

|

|

|

| The US Dollar Index $DXY has been stuck in a tight, messy range for over a year — moving just enough to keep traders second-guessing, trapping bears on breakdown attempts and bulls on short squeezes. Ranges like this are stored energy, and right now, the DXY is sitting at one of its most compressed volatility levels in years. |

| |

That makes the next move potentially explosive — in either direction. For me, the key level to watch remains 100. As long as the dollar stays below the lows from 2023 and 2024, the downtrend remains intact. That’s bullish for equities and other risk assets—not due to accounting quirks or currency effects, but simply because when investors are profiting in stocks, there’s less pressure to sit in cash. In short, demand for safety fades, and risk appetite grows. Now flip the scenario. If the dollar starts reclaiming those former lows and pushes above 100, money will rotate out of aggressive assets and back into safety. So, if you want to gauge potential stress in equities, keep one eye on the dollar. Right now, it’s the clearest early warning signal in the market. |

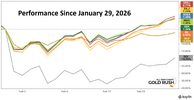

| Over the past few weeks here at Gold Rush, we’ve talked a lot about January 29, 2026. That was the day the character of this market changed, at least temporarily. Silver printed a ten-standard-deviation downside move in a single session. The entire precious metals complex was hit with aggressive selling pressure. It was the kind of volatility event that forces you to step back, reassess positioning, and respect the possibility of a deeper corrective phase. At the time, that made sense. Going into late January, Gold, Silver, and Platinum were historically extended from their 200-week moving averages. We had been obnoxiously bullish since March 4, 2024, and rightfully so, but trends that stretched don’t glide back to equilibrium. They snap. And snap they did. But here’s what’s fascinating. Since that January 29 peak, Silver is still down roughly 20%. Gold is down about 2.5%. On the surface, that looks like damage. Yet beneath the surface, something very different is happening. |

| |

Every major precious metals mining ETF, GDXJ, SILJ, GOEX, RING, GDX, and SIL, is positive since that same January 29 peak. Let that sink in. The metals corrected. The miners did not. What’s more, the Junior Gold Miners ETF $GDXJ and the Junior Silver Miners ETF $SILJ are at the top of the leaderboard. This isn’t defensive positioning into mega-cap names. This is risk appetite expanding inside the precious metals complex. That’s not what a topping process looks like… When precious metals peak as an asset class, Gold outperforms miners. Capital hides in the metal. Risk contracts. And you do not see aggressive flows into the junior miners. But that’s exactly what we’re seeing right now. |

Traders Go Full Bull as Brent Defies Oversupply Worries

– The Israel-US-Iran conflict engulfing most of the Persian Gulf has pushed $10 per barrel higher, LNG prices went up by $15 per MMBtu, and key refined products such as diesel and jet have been spiralling out of control throughout the Atlantic Basin.

– Whilst market watchers almost unanimously define the closure of the Strait of Hormuz as the main bullish factor ahead, very few have, in fact, noted that the Strait has been closed for the past two days.

– There have been no crude oil or LNG transits via the Strait of Hormuz on March 2-3, with dozens of fully loaded ships expecting the end of the regional conflagration, anchored across the Persian Gulf.

– The US Central Command, seeking to placate fears, stated today that the Strait of Hormuz is ‘not closed despite statements by Iranian officials’, even as Saudi Arabia officially announced that it would move all its oil exports to the Red Sea, in avoidance of Hormuz.

– According to Kpler, there are already 55 fully loaded VLCC tankers in the Gulf, up by 18 ships since Israel’s initial attack on Iran that took place on February 28.

.

Market Movers

– UK-based energy major Shell (LON:SHEL) is reportedly considering selling its minority stake in Australia’s North West Shelf LNG project, potentially garnering $24 billion for the sale as both ADNOC and MidOcean Energy declared interest.

– Angola’s national oil firm Sonangol is moving ahead with its plans for an initial public offering, completing debt sales and establishing an investor relations office as 30% of its shares could be offered in the IPO.

– Norway’s state-controlled Equinor (NYSE:EQNR) is reportedly looking to divest its Angolan assets, building on its 2024 exits from Azerbaijan and Nigeria, seeing quicker returns in Brazil and US deepwater.

– Global trading giant Trafigura signed a 5-year LNG term supply contract with US developer Venture Global (NYSE:VG) starting from Q2 2026, the latter’s first mid-term deal concluded since its arbitration deals with Shell, BP and Repsol.

Tuesday, March 3, 2025

Events are escalating with unprecedented speed across the Middle East. Drone strikes on Saudi Arabia’s largest refinery, strikes on the world’s largest liquefaction facility in Qatar, the bombing of several tankers, widespread insurance policy cancellations – all that would be usually scattered across several months in a normal year; however, in 2026, that’s just one day’s worth of action. With the Strait of Hormuz seeing no navigation for several days already, ICE Brent is up at $84 per barrel, and it could very well test the $90 per barrel if the pressure on Gulf producers increases.

Goldman Sachs Embraces Its Internal Bull. OPEC+ Opted for Caution Amidst War Pressures. Members of OPEC+ agreed to a relatively modest oil production increase of 206,000 b/d for April 2026, defying the pressure to triple its usual monthly quota on fears that Iranian supply would be curtailed, just as the Strait of Hormuz was set to close.

Qatar Halts World’s Largest LNG Plant. Qatar’s state-owned QatarEnergy has haltedproduction at its Ras Laffan liquefaction plant, the world’s largest LNG object, following reports that Iranian drones have targeted an ‘energy facility’ in Qatar as well as an adjacent power plant in Mesaieed.

Saudi Arabia’s Refining Takes a Hit From Iran. Saudi Arabia’s largest refinery, the 550,000 b/d Ras Tanura plant on the country’s eastern coast, halted operations completely after a drone attack sparked a large fire on Monday morning, raising the risk of Saudi production shut-ins.

Chinese Refiners Go for Run Cuts. China’s leading private refiners Zhejiang Petrochemical and Fujian Refining, which both happen to be partially owned by Saudi Aramco, have announced curtailments in refinery operations rates in response to stalled crude oil deliveries from the Middle East.

Stranded Oil Tankers Push Oil Freight to Records. Iran’s closure of the Hormuz Strait and the risk of seeing tankers struck or stranded in the Persian Gulf lifted freight rates for VLCC tankers to a new high, with a Gulf-to-China voyage now costing $89 per metric tonne, up 560% since early January.

Asia’s Naphtha Cracks Balloon Out of Control. Fears that Middle Eastern naphtha, a 1.2 million b/d stream mostly fed by the UAE and Qatar, could become stranded in the Persian Gulf have lifted Asian naphtha cracks to their highest since April 2022, reaching a $135 per tonne premium vs Brent.

Platts Doesn’t Know What Dubai to Assess. Global price reporting agency S&P Global Platts has suspended bids and offers for some of its Middle Eastern crude, refined product, and LNG price assessments, allowing only Murban and Oman trades as all other grades load deep in the Gulf.

Israel Shuts Down Offshore Gas Fields. The Israeli Energy Ministry has ordered the temporary shutdown of the country’s offshore gas platforms, including the Chevron-operated (NYSE:CVX) Leviathan field that supplies 40% of the country’s gas needs, switching to alternative fuels.

Insurers Avoid Hormuz as Much as They Can. Marine insurers are cancelling war risk coverage for tankers set to enter the Strait of Hormuz, with Gard, Skuld, NorthStandard, the London P&I Club, and the American Club collectively claiming they would fully cut coverage from March 5.

Keystone XL Might Be More Alive Than Dead. Canada’s midstream giant South Bow (TSE:SOBO), spun out of TC Energy in 2024, is reportedly seeking to revive the Keystone XL pipeline by re-routing it through Montana, potentially boosting Canada-to-US crude flows by another 550,000 b/d.

Nigeria Gets Creative With Its Blocks. The government of Nigeria has broken up the OPL 245 offshore license block into four new assets operated by European majors ENI (BIT:ENI) and Shell (LON:SHEL), paving the way for the long-stalled development of Nigeria’s largest untapped field.

Kurdish Producers Cut Output Amidst Drone Hits. Following massive Iranian drone strikes on US military installations in Erbil, oil companies operating in the semi-autonomous Iraqi Kurdistan have started to shut in production, with Gulf Keystone and Shamaran shuttering 110,000 b/day of output.

Brace Yourself for a New Copper Disruption. Copper prices could be up for another supply disruption-driven price spike after widespread flooding caused the collapse of a bridge linking the Democratic Republic of Congo to Zambia, the main export conduit for its 3.5 mtpa exports.

Saudi Aramco Reinvents the Red Sea. Saudi Arabia’s state oil firm Saudi Aramco (TADAWUL:2222) has alerted its buyers that from now on, for an undefined period, it would only load crude oil tankers from its Red Sea port of Yanbu, sending oil to the west through its 5 million b/d East-West pipeline.

jog on

duc

Source link