Is It Wrong To Buy Calendar Spreads When VIX Is High?

This will be a debate – not about politics, religion, or the best diet to follow, but about the philosophy of trading calendar options only within a specific volatility range.

Like those other topics, there is no single correct answer.

One school of thought may favor trading calendar spreads only when the CBOE Volatility Index (VIX) is low.

However, we see others trading calendar spreads while VIX is high; that approach cannot simply be declared wrong.

Different traders operate with different philosophies and methods.

Just as some believe the Paleo Diet is the best nutritional approach while others favor a Vegan Diet, neither perspective is necessarily incorrect.

Both represent valid viewpoints.

Let me explain why – not about diets, but about calendar options.

Contents

Calendar spreads have positive vega, meaning they benefit when volatility rises during the trade and tend to lose value when volatility falls.

Entering a calendar spread when the VIX is already high is often frowned upon because volatility often mean-reverts, meaning that high volatility eventually will fall, exposing the position to a volatility crush.

Hence, the traditional view is to enter calendar spreads when volatility is relatively low.

In that environment, there is less room for volatility to decline and a greater chance that an increase in volatility will help the trade.

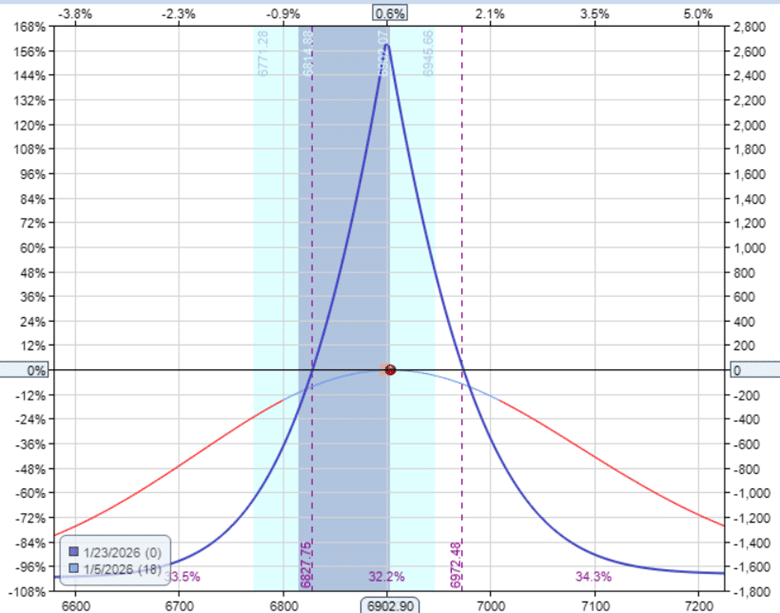

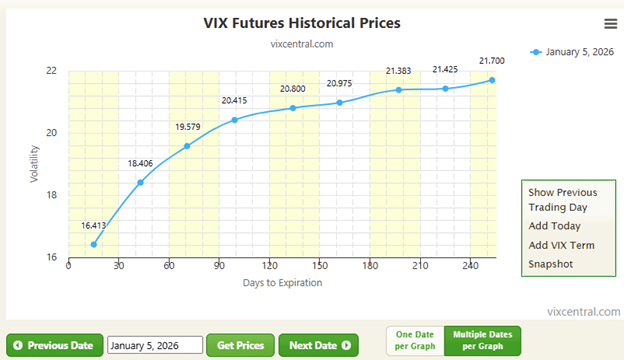

Let’s look at a textbook example of an SPX (S&P 500 Index) put calendar entered on low volatility with a VIX of 14.

Date: Jan 5, 2026

Price: SPX @ $6902

Sell to open one contract Jan 23 SPX 6900 put @ $64.00

Buy to open one contract Jan 30 SPX 6900 put @ $80.65

Debit: -$1665

The short option being sold expires in 18 days.

The long option being bought expires one week after that.

Both strikes are the same at 6900.

The implied volatility (IV) of the short option was 10.78, while the IV of the long option was 11.48.

This is typically the case, as the earlier-expiring option tends to have lower implied volatility.

The longer-dated option carries higher IV because it has more time before expiration and therefore greater exposure to potentially unpredictable events.

If we take a look at the VIX Futures Term Structure on that day…

We see that as the days to expiration increase, volatility increases.

This scenario produces this shape of the curve, known as contango.

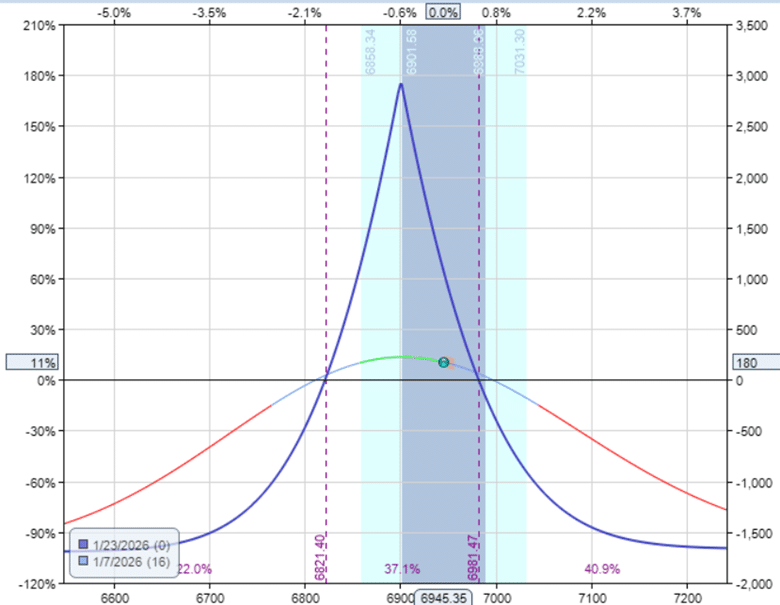

Let’s see what happened in our calendar example.

Two days after the trade was initiated, on January 7th, the position reached a 10% profit, generating $180 on $1,665 of capital at risk.

The calendar generated profit primarily from the passage of time through theta decay, while the price of the underlying cooperated by remaining within a defined range.

The implied volatility (IV) of the short option rose to 11.20, while the IV of the long option increased to 12.11.

Both options experienced a rise in IV, with the longer-dated option increasing slightly more.

Because IV is positively correlated with an option’s value, this development was favorable for the position.

The long option that was owned retained its value better than the short option.

This is exactly how the calendar should work and profit.

It validates the idea that calendars should be entered when the VIX is low.

While this idea is a good start for beginning options traders, it is an oversimplification.

And a rigid rule of buying calendars only when VIX is below 18 can lead traders to miss good trades.

As there are two sides to every debate.

Let’s look at an alternate perspective that can be equally valid.

Calendar spreads depend more on the volatility relationship between the two different expirations rather than on the absolute level of VIX.

The VIX represents the market’s expectation of 30-day volatility for the SPX as calculated from a wide range of SPX option prices, both puts and calls, across many strikes around the current price.

The formula essentially averages the implied volatility embedded in those options.

This will not exactly correspond to the IV of the individual options chosen for the calendar.

Just looking at the fix does not take into account the term structure of the individual strike and the chosen expirations.

A calendar spread can profit from changes in implied volatility between the short-term and longer-term options.

In particular, if the short-term IV is much higher than the longer-term IV (a condition known as backwardation), the calendar can have an extra edge independent of the general VIX environment.

A calendar in backwardation will cost less than a calendar not in backwardation, all else being equal.

This is because, in backwardation, we are selling a high-value option and buying a protective option at a relatively lower price.

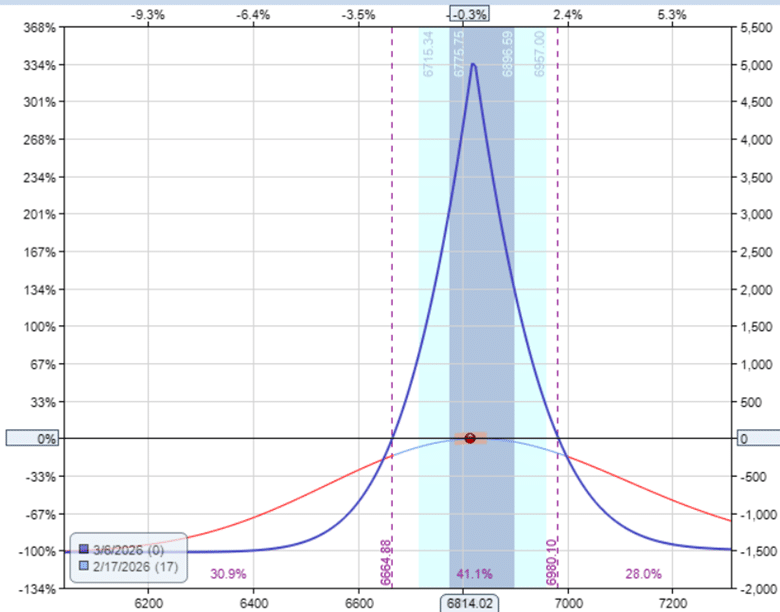

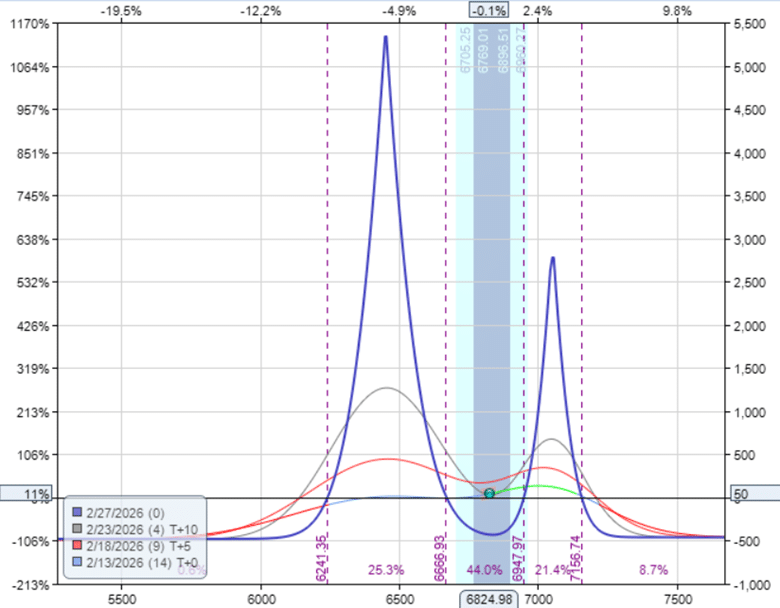

For the next example, we intentionally picked a date when VIX was moderately high at 22.5 and then dropped in the following days – a situation that would be considered unfavorable from a classic point of view.

Date: Feb 17, 2026

Price: SPX @ 6814

Sell to open one contract Mar 6 SPX 6820 put @ $109.70 (IV = 18.25)

Buy to open one contract Mar 13 SPX 6820 put @ $124.65 (IV = 17.53)

Debit: -$1495

Right away, this calendar’s shape looks slightly different.

It is tall and slender.

It has a theoretical max profit of $5000 while a max risk of $1500 – a reward-to-risk ratio of 3.3.

In contrast, the reward-to-risk ratio of the previous example calendar is only 1.8 (calculated by $3000/$1665)

Note that this calendar is in backwardation with its short-term option IV (18.25) being higher than its longer-term option IV (17.53).

For these three-week calendars, backwardation typically does not occur until the VIX is moderately high, when there is at least some market anxiety.

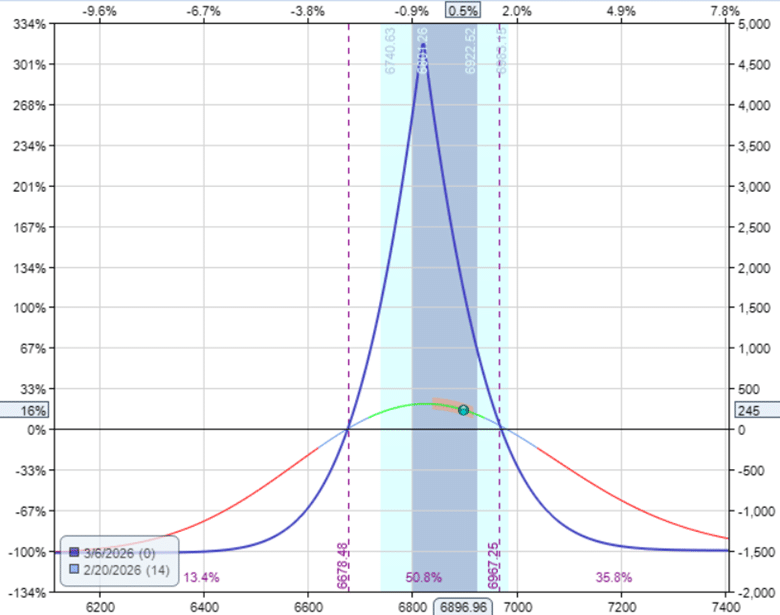

In this example, by February 20th, the trade could be exited with a 15% profit.

The position generated $245 on the trade, even though the VIX fell from 22.5 to 19.1 – contrary to the conventional wisdom that a drop in VIX is unfavorable for calendar spreads.

Looking at the individual IVs of the calendar at exit.

The short option IV had become 17.05 – a decrease of 1.2.

The long option IV had become 16.72 – a decrease of 0.8.

This is favorable for the calendar when the short option’s IV drops more than the long option.

Although the term structure remained in backwardation, the degree of backwardation had decreased – meaning that the term structure curve is normalizing.

The difference in IV between the short and long options is now only 0.4, down from 0.7 before.

When a calendar spread is initiated during backwardation, and the market later stabilizes or moves higher, the volatility term structure often begins to normalize.

This shift generally benefits the calendar spread.

The improvement from the term structure returning to a more typical shape can often offset the loss in value caused by the decline in volatility that typically accompanies market rises.

Some traders may initiate double calendars during backwardation.

For example…

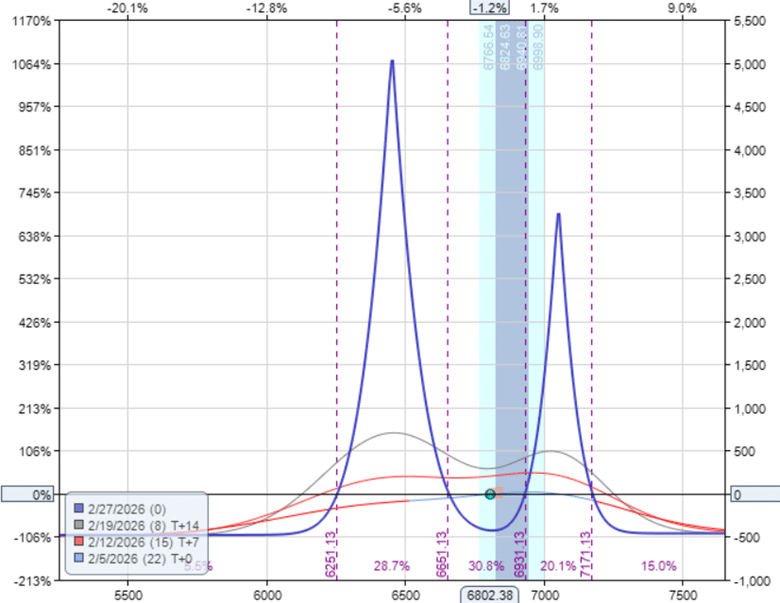

Date: Feb 5, 2026

Price: SPX @ 6802

VIX: 22.5

Sell one contract Feb 27 SPX 6450 put @ $42.45 (IV = 24.84)

Buy one contract Mar 2 SPX 6450 put @ $45.00 (IV = 23.85)

Sell one contract Feb 27 SPX 7050 call @ $24.10 (IV = 15.35)

Buy one contract Mar 2 SPX 7050 call @ $26.25 (IV = 14.85)

Net Debit: -$470

Notice this time, the long option has an expiration only 3 days after the expiration of the short option.

By narrowing the time difference between expirations, we can increase the likelihood of the calendars being in backwardation (which is the case here, given their IVs).

It also means the calendars will cost less because the short option’s price will be closer to the long option’s price.

This results in a high reward-to-risk ratio, as evidenced by the payoff graph.

If the price of SPX rallies, the term structure curve will normalize (good), and the price will move into the upper calendar.

If the price of SPX continues to drop, IVs will increase (good for calendars), and the price will move into the lower calendar.

If the price doesn’t move, theta decay will generate the profit.

The only problem is that if the price moves too far in one direction, it can overshoot the calendar.

This is why the two calendars were placed further apart from each other – so much so that the expiration graph sags below the zero profit horizontal in the middle.

But we plan to exit way before expiration, so this is less of a concern.

Because this double calendar has only four legs, a trader can place a good-till-cancel order to exit the calendars at 10% profit.

The GTC order would have triggered 8 days later, exiting the trade with a $47 profit.

Due to backwardation and a narrow time difference in expiration, these calendars were really low in max risk, given their low cost of $470 for the pair.

While a person may initially have been taught one perspective, they should be open to other viewpoints.

Calendars may not be as straightforward as it initially seems.

As we evolve in our trading journey, the rigid rule of buying only calendars when the VIX is under 18 may be too restrictive.

So to answer the original question:

No, it is not wrong to buy calendar options when the VIX is high, when done correctly and with an understanding of the right conditions.

We hope you enjoyed this article on buying calendar spreads when IV is high.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Source link