What Is A Debit Spread? The Ultimate Beginner’s Guide To Options

If you are new to the world of options trading, the terminology alone is enough to make your head spin. You’ve probably heard veteran traders throwing around terms like “iron condors,” “gamma scalping,” and “credit spreads.” The barrier to entry can feel incredibly high.

But if there is one foundational, multi-leg strategy you need to master before you do anything else, it is the debit spread.

Debit spreads are the essential bridge between beginner-level trading (simply buying a single call or a put) and advanced, mathematically driven options strategies. They are specifically designed by professional traders to do two incredibly important things: drastically lower your trading costs and strictly define your absolute maximum risk.

In this ultimate beginner’s guide, we are going to completely strip away the complex Wall Street jargon. We will break down exactly what a debit spread is, why the pros use them every single day, how they neutralize the hidden dangers of the options market, and how you can start using them to build a more consistent, risk-managed trading portfolio.

The Trap: The Problem with Buying “Naked” Options

To truly appreciate why debit spreads are so powerful, we first have to understand the inherent flaw with the way 90% of beginners start trading options: buying single, “naked” calls or puts.

Let’s say you are looking at a chart, and you are highly confident that a particular stock is going to go up. The beginner’s instinct is to log into their brokerage account and simply buy a Call option. It makes logical sense, right? If the stock goes up, the call option goes up.

However, when you buy a standard, single option, you are walking into an arena where you are fighting two massive, invisible enemies that are actively working to drain your account:

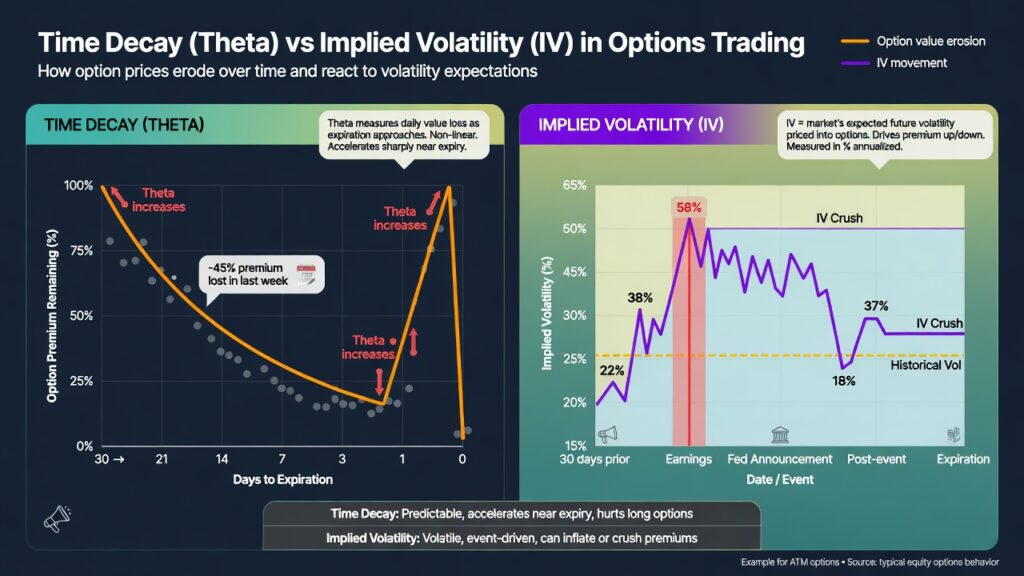

- Time Decay (Theta): Unlike buying shares of a stock, which you can hold forever, options are decaying assets. They have an expiration date. Every single day you hold that option, it loses a little bit of its intrinsic value simply because time is passing. This is measured by the option Greek called “Theta.” If the stock moves in your direction, but it doesn’t move fast enough, time decay will completely eat your profits. You can be right about the direction and still lose money.

- Implied Volatility (Vega): When you buy an option, the price you pay (the premium) is heavily influenced by the “hype” or expected volatility surrounding that stock. If a stock is heavily hyped (like right before an earnings report), options are expensive. If you buy a call option and the stock goes up, but the hype suddenly dies down (causing volatility to drop), your option can actually lose value. This is known as a “Volatility Crush.”

Buying single options is notoriously expensive, incredibly risky, and gives you a surprisingly low mathematical probability of success because the underlying stock has to make a massive, explosive move just for you to break even.

This is exactly where the debit spread comes to the rescue.

So, What Exactly is a Debit Spread?

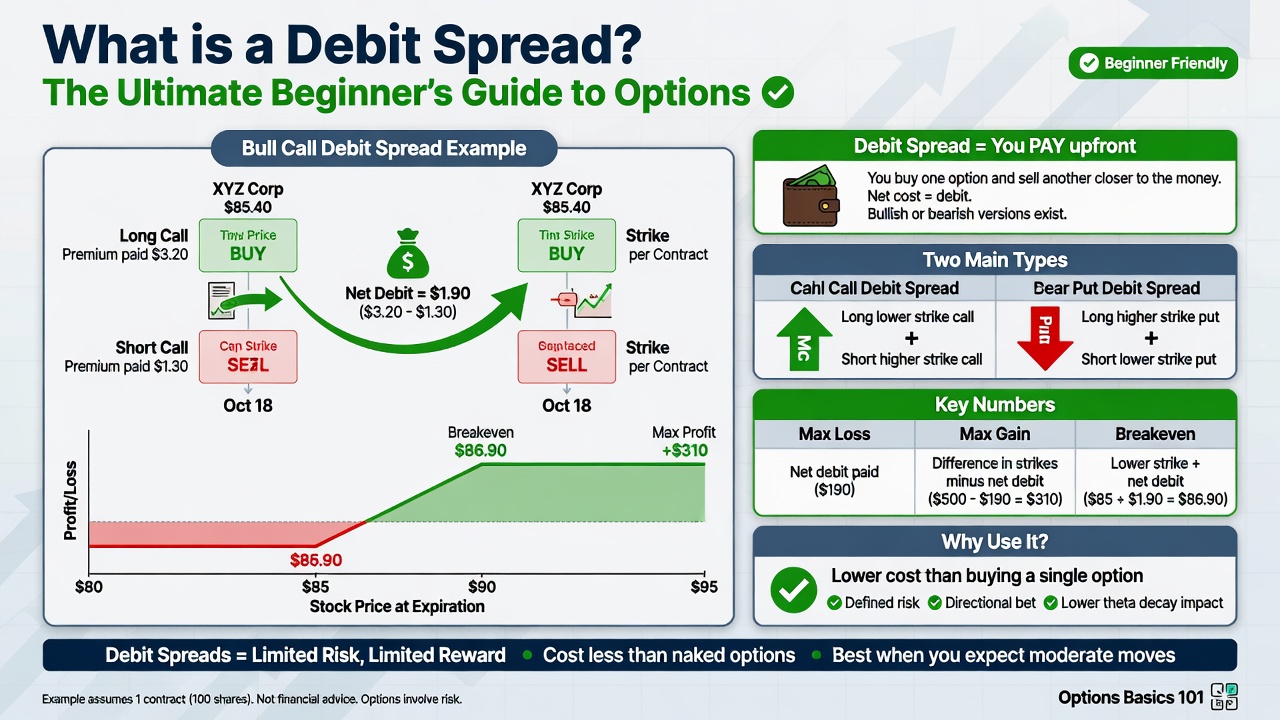

A debit spread is a “multi-leg” options strategy. Instead of just making one move (like buying a single call), you are executing two moves at the exact same time within the same expiration cycle on the same stock.

In a standard debit spread, you are simultaneously:

- Buying an option closer to the current stock price (which costs you money).

- Selling another option further away from the current stock price (which pays you money).

Because the option you are buying is closer to where the stock is currently trading (closer to “the money”), it will always be more expensive than the option you are selling further out.

Therefore, when you combine the two transactions, more money is leaving your account than coming in. In accounting terms, this results in a net debit to your brokerage account. Hence the name: Debit Spread.

You are paying money upfront to enter the trade, but because you collected some money by selling the second leg, your total out-of-pocket cost is heavily subsidized. Most importantly, the final net debit you pay is the absolute maximum amount of money you can lose on the trade.

The Two Primary Types of Debit Spreads

Debit spreads are directional trades. You use them when you have a strong opinion on where a stock is headed. Depending on your market outlook, you will use one of two variations:

- The Bull Call Spread (For Upward Movement): You use this when you think the stock is going to go UP. You buy a call option near the current price, and sell a call option at a higher price.

- The Bear Put Spread (For Downward Movement): You use this when you think the stock is going to go DOWN. You buy a put option near the current price, and sell a put option at a lower price.

Both operate on the exact same mechanical principles. You are buying the more expensive, powerful option to capture the direction of the stock, and you are selling the cheaper, further-out option to help finance your purchase.

The Mechanics: A Real-World Math Walkthrough

Theory is great, but let’s look at the actual math to see why this strategy is an absolute game-changer. We will use a hypothetical Bull Call Spread for a fictional tech company, XYZ Corp.

Imagine XYZ Corp is currently trading at exactly $100 per share. After doing your technical analysis, you firmly believe the stock is going to rally up to $105 over the next three weeks.

Scenario A: The Beginner Way (Buying a Single Call)

You decide to buy the $100 Strike Call Option. Let’s say the market is pricing this option at $5.00 per share. Since standard options contracts always represent 100 shares of the underlying stock, this single trade costs you **$500** out of pocket ($5.00 x 100).

- Your Max Risk: $500. If XYZ stock drops or simply stays flat at $100, your option expires worthless and you lose your entire $500 investment.

- Your Breakeven Point: The stock must reach $105 ($100 strike + $5.00 premium paid) by expiration just for you to make $0. You only start seeing a profit if the stock crosses $105.01. That is a steep hill to climb.

Scenario B: The Professional Way (The Debit Spread)

You realize that risking $500 is too much for your account size, and you want to lower your breakeven point. So, you structure a debit spread instead.

- Leg 1: You BUY the same $100 Strike Call for $5.00. (You pay out $500).

- Leg 2: You simultaneously SELL the $105 Strike Call for $2.00. (You instantly collect $200).

Now, let’s calculate your actual net cost. You paid $500 to the market, but the market immediately handed you $200 back for the option you sold. Your total cost (your Net Debit) is now only **$300**.

Look at the massive mathematical advantages you just created for yourself:

- You slashed your risk by 40%. Instead of risking $500 on the trade, your maximum possible loss is now only $300.

- You lowered your breakeven point. Because you only paid a net of $3.00 for the spread, XYZ stock only needs to reach **$103** ($100 strike + $3.00 net debit) for you to break even, rather than $105.

By selling that further-out option, you did sacrifice the “infinite” upside potential of the single call option. If the stock explodes to $150, your profits are capped. But in exchange for giving up that lottery-ticket upside, you gained a vastly higher probability of actually walking away from the trade with a profit.

Want to Master Weekly Debit Spreads?

Take the guesswork out of trading. Discover our highly effective Layered Options strategy, designed specifically for generating weekly setups and trading debit spreads the right way.

Learn the Layered Options Strategy TodayCalculating the “Box”: Max Profit, Max Loss, and Spread Width

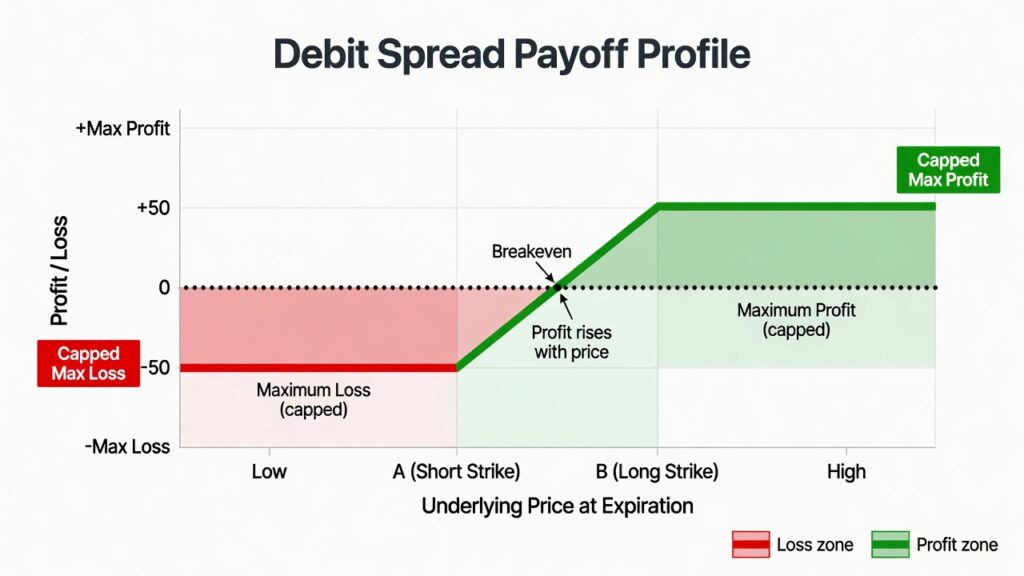

When trading debit spreads, your profit and loss are firmly locked inside a specific mathematical box. You know your absolute worst-case scenario and your absolute best-case scenario before you even click the “Submit Order” button.

To figure out your numbers, you need to understand the spread “Width.” The Width is simply the distance between the strike price you bought and the strike price you sold. In our XYZ example, we bought the $100 strike and sold the $105 strike. Therefore, the width of the spread is $5.00.

Here are the golden formulas you will use for every debit spread you ever trade:

- Maximum Loss: This is the easiest calculation. It is exactly what you paid for the trade (The Net Debit). In our example, your max loss is $300. You cannot lose a single penny more than this, even if XYZ stock drops to zero or files for bankruptcy overnight.

- Maximum Profit: To find this, take the Spread Width and subtract your Net Debit. (Width of $5.00 – Net Debit of $3.00 = $2.00). Multiply by 100 shares, and your max profit is **$200**. You achieve maximum profit if the stock simply closes anywhere above your sold strike ($105) at expiration.

- Breakeven Point: Take the strike price you bought and add your net debit. ($100 + $3.00 = **$103**).

If you risk $300 to make $200, you have created a trade with an incredibly solid risk-to-reward ratio, while simultaneously lowering the hurdle the stock needs to clear to make you money.

How Debit Spreads Neutralize “The Greeks”

Earlier, we mentioned that buying single options exposes you to the dangers of Time Decay (Theta) and Implied Volatility (Vega). Here is the secret weapon of the debit spread: it essentially neutralizes those threats.

Because you are both buying an option and selling an option, the Greeks cancel each other out to a large degree.

- Fighting Theta: As time passes, the option you bought loses value. That hurts you. However, the option you sold is also losing value as time passes. Because you are the seller of that second leg, time decay on that specific option actually makes you money. The decay of the sold option subsidizes the decay of the bought option.

- Fighting Vega: If implied volatility suddenly drops across the market, the option you bought loses value. But, just like with time decay, the option you sold also loses value. As the seller, a drop in volatility helps you on that leg, softening the blow to your overall position.

By trading spreads, you are stripping away the complex variables of time and volatility, and turning the trade into a pure question of: “Will this stock go in my direction by this date?”

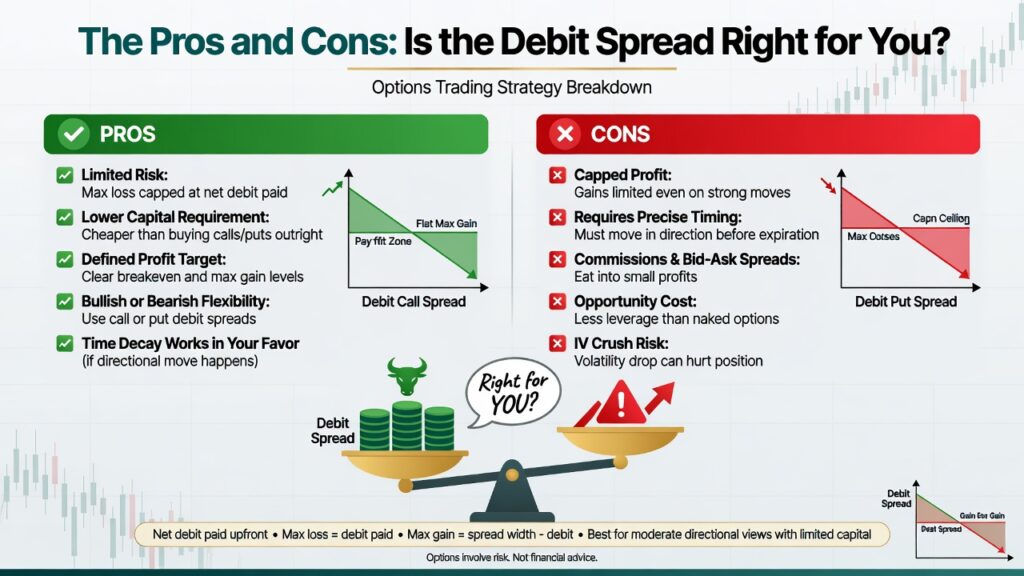

The Pros and Cons: Is the Debit Spread Right for You?

Like every strategy in the financial markets, debit spreads are a specialized tool. And every tool has specific market environments where it excels, and environments where it falls short. Let’s weigh the ultimate benefits and drawbacks.

The Pros: Why Professionals Love Them

- Built-in Sleep-at-Night Risk Management: You never have to worry about a massive gap-down wiping out your account. Your risk is strictly defined before you enter the trade.

- Capital Efficiency: Because you are selling an option to finance your purchase, you can trade expensive, high-dollar stocks (like Nvidia, Meta, or Microsoft) without needing a massive $50,000 account balance.

- Higher Probability of Profit: By lowering your breakeven point compared to buying single options, you statistically increase your chances of walking away with a winning trade.

- Forgiving Mechanics: As explained above, the multi-leg structure naturally hedges your portfolio against the destructive forces of time decay and volatility crush.

The Cons: The Trade-Offs You Must Accept

- Capped Profit Potential: You have to give up the “home run” trades. If you buy a debit spread on a stock and it suddenly explodes 150% upward due to a buyout rumor, your profits are strictly capped at the width of your spread. You will not capture that massive windfall.

- Direction and Timing are Still Required: While debit spreads are safer, they are not magic. You still need the stock to move in your chosen direction within the specific timeframe of your expiration date to realize your max profit.

- Wider Bid-Ask Spreads: Because you are trading two legs instead of one, you have to cross the bid-ask spread twice, which can result in slightly higher slippage (the difference between what you want to pay and what the market fills your order at) on less liquid stocks.

What’s Next in the Ultimate Guide?

Debit spreads are the ideal strategy for traders who want to express a bullish or bearish opinion on a stock, but want to do so responsibly and consistently. They force you to be disciplined, define your risk upfront, and accept realistic base hits rather than constantly swinging for the fences and striking out.

Want to Master Weekly Debit Spreads?

Take the guesswork out of trading. Discover our highly effective Layered Options strategy, designed specifically for generating weekly setups and trading debit spreads the right way.

Learn the Layered Options Strategy TodayNow that you deeply understand the foundational mechanics, the math, and the why behind debit spreads, it’s time to start applying this knowledge directly to the options chain.

In our next article in this Ultimate Guide series, Call Debit Spreads vs. Put Debit Spreads, we are going to dive deep into the specific structural differences between the two, exactly how to read your broker’s options chain to find the best setups, and the specific market conditions that dictate when you should deploy a bullish strategy versus a bearish one.

Source link