Laddering Covered Call Strikes Based on Market Assessment and Risk Tolerance

What strike should I select for my covered call trades? In-the-money (ITM), out-of-the-money (OTM), how far out, how far in? This apparent dilemma can easily be navigated by identifying our return goals, market assessment and personal risk tolerance. Another important factor is that, when selling multiple contracts, we can use different strikes, a process I refer to as laddering strikes. I borrowed this term from the bond market.

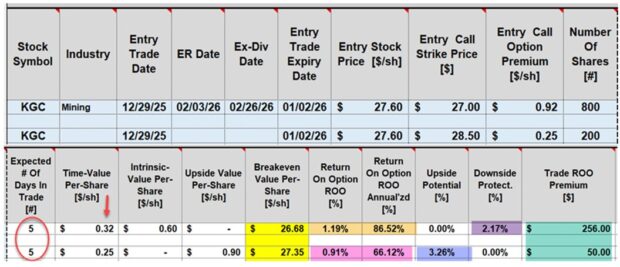

A Real-Life Example with Kinross Gold Corp. (NYSE: KGC) on 12/29/2025 (5-day, holiday-shortened trade)

- 12/29/2025: Buy 1000 x KGC at $27.60

- 12/29/2025: STO 8 x 1/2/2026 $27.00 (TM) calls at $0.92

- 12/29/2025: STO 2 x 1/2/2026 $28.50 (OTM) calls at $0.25

What are these strike selections telling us?

Of the 10 contracts sold, 8 were ITM, a defensive approach; 2 were OTM, a more aggressive approach. Overall, I was leaning defensively, with a cautious overall market assessment, which aligned with my personal risk tolerance at the time of these trades.

What about option premium return goals?

I, typically, target 2% – 4% per month and 1/2% – 1% per week. In these trades, I was at the high end of these ranges.

Initial Covered Call Trade Calculations: BCI Trade Management Calculator (TMC)

- Brown cells: The ITM strikes generated initial returns of 1.19%, 86.52%, with 2.17% downside protection of that time-value profit (purple cell)

- Pink cells: The OTM strike generated 0.91%, 66.12% annualized, with 3.26% of upside potential (blue cell)

- Green cells: A total of $306.00 in time-value premium was generated into my brokerage account

Post expiration results

- KGC closed at $28.30, leaving the $27.00 call expiring ITM and 800 shares were sold at $27.00

- The $28.50 strike expired slightly OTM, so 200 shares were retained

- The initial cash outlay for 1000 shares was $27,600.00

- The realized loss on the sales of 800 shares (ITM strike) was $480.00

- The unrealized gain on 200 shares is $140.00

- Net return on the stock side: -$340.00

- Net realized option premiums: $736.00 + $50.00 = $786.00

- Net realized/unrealized return is +$446.00 = 1.61%, 84% annualized (52 periods)

Discussion

- Significant returns can be generated with 5-day covered call trades even during holiday-shortened weeks

- Option trades can be crafted to align with all market environments and personal risk tolerance

- In the case of KGC, significant 5-day returns were initially captured and realized

- These are low risk, not no risk trades

THE POOR MAN’S COVERED CALL

Online Streaming video course with Downloadable Workbook

This program will highlight in great detail:

- PMCC definition

- Pros and Cons

- Risk/reward profile

- Best stocks and ETFs to consider

- How to construct a PMCC trade

- Hypothetical example

- Multiple real-life examples

- The BCI PMCC Calculator

- Option Greeks

- Position management

- Rolling LEAPS

Click here for a video & more.

Free training resources

Your generous testimonials

Over the years, the BCI community has been incredibly gracious by sending our BCI team email testimonials sharing stories as to what our educational content has meant to their families. Moving forward, we have decided to publish several of these testimonials in our blog articles. We will never use a last name unless given permission:

Good evening, Alan,

Thank you so much for your generous gift of time and knowledge. As always, your explanation of the “Wheel Strategy” was excellent, actionable and much appreciated. Also, thanks to Barry for addressing the questions in the Chat window.

Several members said they enjoyed the presentation and inquired about more information regarding the strategy.

We hope that you will agree to address our group at some time in the future and I look forward to sharing a drink in Orlando at The MoneyShow.

Best regards,

Bob S. President of the Sarasota Investment Club

_____________________________________________________________________

_____________________________________________________________________

Upcoming events

1. BCI Educational Webinar #10: The Put-Call-Put (PCP) or “Wheel Strategy”

Thursday May 14, 2026, at 8 PM ET

Using both covered call writing & cash-secured puts in a multi-tiered option selling strategy. A 68-day real-life example taken from one of Alan’s portfolios will be analyzed.

BONUS: Barry will share a real-life credit spread trade using our BCI Conservative Credit Spread Management System.

Discount coupons and a live Q&A session will follow the presentation.

Click here for more information and to register (scroll down).

2. Mad Hedge Investor Summit

June 3, 2026

12 PM ET – 1 PM ET

Details & registration link to follow.to follow.

3. American Association of Individual Investors: NYC Chapter

June 10, 2026, at 6 PM – 8 PM ET

More information to come.

4. MoneyShow Masters Symposium Las Vegas

July 20 – 22, 2026

Caesars Palace Hotel

Las Vegas

Details to follow.

5. Toronto Money Show

September 24 – 25, 2026

MaRS Center, Toronto Canada

6. Orlando Money Show

October 5 – 7, 2026

Hilton Orlando Lake Buena Vista

Details to follow.

Source link