Why Investors Should Not Fear Assignment on Covered Calls

Many investors new to covered calls worry about “getting assigned.”

But in reality, the assignment is usually just the strategy working as intended.

Whenever an investor is assigned on a covered call, they have made money.

It doesn’t matter whether the short call is far out of the money or far in the money.

In fact, some covered call writers sell calls specifically to be assigned.

We will give examples of each and why.

Contents

The terms “covered call writers” and “covered call sellers” are synonymous.

The investor is selling one call option for every 100 shares of stock they own.

Selling an option is also referred to as writing an option.

Although we don’t write anything with pen and paper anymore, imagine that the investor is effectively writing a contract that gives someone else the right to buy their shares at a specific strike price before a specific expiration date.

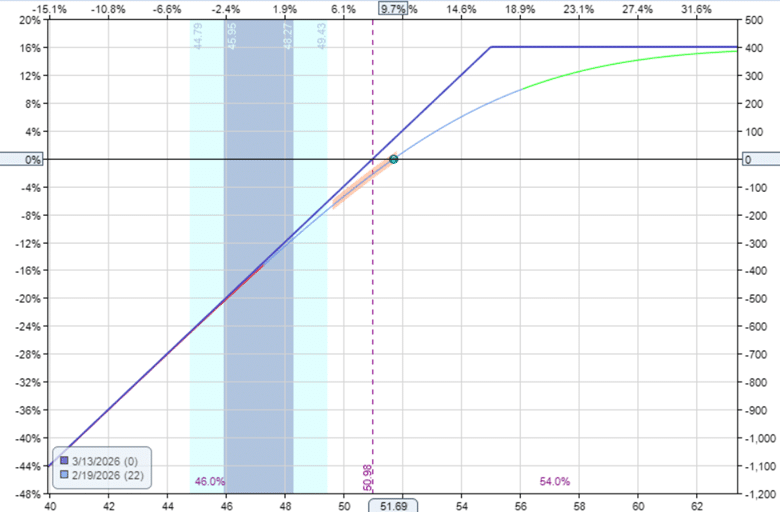

Here is an example of a covered call on Occidental Petroleum (OXY) initiated on February 19, 2026:

Buy 100 shares of OXY at $51.69 per share

Sell to open one contract Mar 13 OXY $55 put at $0.69 per share

Net Debit: -$5169 + $69 = -$5100

The investor paid a total of $5100 to enter the trade.

The premium from the sale of the call option partially helped finance the cost of the stock.

Looking at the following payoff graph…

The real risk is not the assignment.

The real risk is the stock going down.

If an assignment happens, it’s because the stock went up and the investor profited.

On the expiration date, March 13, 2026, OXY closed at $57.88.

Since this is above the strike price of $55, this option is automatically “exercised”.

The investor who sold the option is “assigned” and is obligated to sell 100 shares at $55 per share (even though the market price is at $57.88).

Did the investor lose money from the covered call?

Not at all.

He bought 100 shares at $51.69 and sold them at $55.

That’s a gain of $3.31 per share, or a gain of $331 for the 100 shares.

Plus, he collected $69 in premium from the sale of the call option.

Net profit is $331 + $69 = $400

This is the maximum possible profit, as shown by the profit graph at expiration…

If you want your covered calls to make max profit without having to roll the call option, then having the stock called away at expiration is the way to achieve this.

Netflix (NFLX) was in a downtrend heading into 2026:

But the investor was optimistic in seeing a bullish green candle post-earnings on January 21, 2026.

He believes that the stock will not drop below $80 per share and decides to use a covered call to collect some premium.

To reduce the risk of the stock going down, some investors like to sell in-the-money covered calls in a downtrending market.

The investor does not want the stock to go down and would like the stock to go up.

However, due to market conditions, there is a higher chance the stock will drop.

So the investor would like to collect as much premium as possible from the sale of the call option to offset potential stock depreciation.

To collect a higher premium, he needs to sell an in-the-money call as follows.

Date: Jan 21, 2026

Price: NFLX at $84.75

Buy 100 shares of NFLX at $84.75

Sell to open one contract Feb 6 NFLX $80 call at $5.62

Net debit: -$8475 + $562 = -$7913

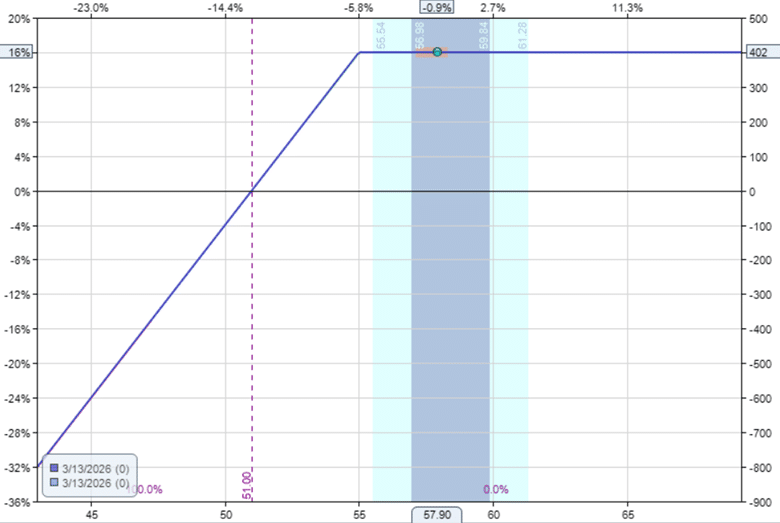

The payoff graph looks just like any other covered call…

The investor had chosen $80 as the strike price because he didn’t think NFLX would drop below it.

In fact, he hopes that NFLX stays above $80 at expiration so that the 100 shares of stock are called away, giving him the max profit on the covered call.

If NFLX is below $80 at expiration, he would not make as much.

And if NFLX is below $79.18, he would be losing money on the covered call.

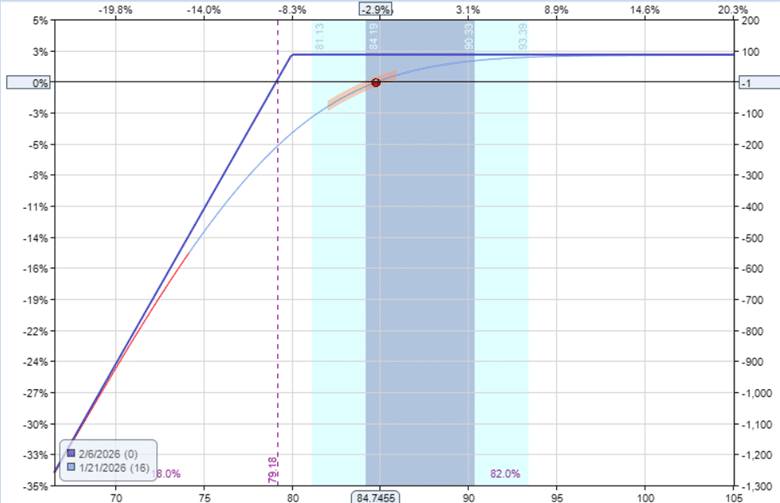

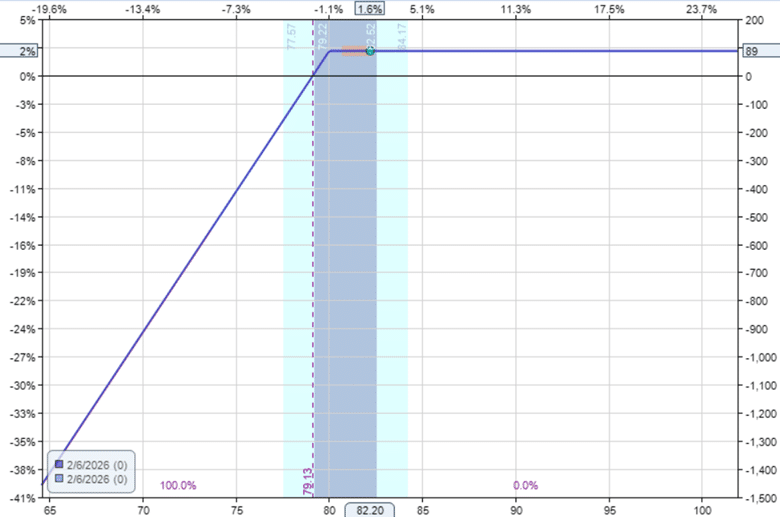

Let’s see what happens at expiration on February 6th:

The stock closed at $82.20.

This is above the strike price of $80. And 100 shares of NFLX were sold at $80 per share. The investor is happy.

His plan had worked out, and he profited by capturing the extrinsic value of NFLX over the two weeks of the trade.

He had bought 100 shares at $84.75 and was happy they sold at $80, even though that represented a $ 4.75-per-share loss, or $475 on 100 shares.

However, this was more than offset by the large $562 premium he collected from selling that particular call option.

Therefore, his total profit was $87

$562 – $475 = $87

This is also confirmed by the payoff graph hitting max profit at expiration on February 6th:

He had used $ 8,500 in capital to generate $87 in income.

That is 1% return in two weeks, or 26% annualized – assuming that he could do this consistently for a whole year (which is a big assumption).

And it did not require the stock to go up.

Where did this profit come from?

It came from the extrinsic value of the sold call option.

Embedded in the $562 premium are both the option’s intrinsic and extrinsic values.

The $475 in intrinsic value compensates the investor for the unfavorable discrepancy between the strike price and the stock’s price.

The remaining $87 is the option’s extrinsic value.

He keeps the full extrinsic value if the call option goes in-the-money.

And that means that his stock must be called away.

Don’t worry if this example is advanced.

It is a bit of a brain-twister.

All you have to remember is that all covered calls (regardless of type) are a bullish strategy, which means that you want the stock price to go up.

The higher the stock price goes, the more likely it is that the short call goes in the money and your stock gets called away.

So if you get assigned on a covered call, the strategy is working as intended.

Nothing, the investors sold their stocks and pockets the profit.

They have received cash into their account.

Now they can reinvest in another stock.

Make another covered-call setup.

Or use that capital in a different strategy entirely.

Think of the assignment as “forcing” the investor to lock in their gains.

If the investor still likes the stock and wants to continue owning it after assignment, they can simply buy the shares back.

With today’s near-zero commissions and transaction fees, repurchasing the stock is essentially inconsequential.

The only consequence may be that the sale of the stock may trigger a taxable event.

Or it could be that the investor wants to continue holding the stock for the dividend or for other reasons.

In another article, we will talk about a primary method for avoiding assignment.

Fear not of being assigned on covered calls.

Whenever an investor is assigned on a covered call, the trade is profitable.

Whether the call was far out-of-the-money or deep in-the-money doesn’t change the fact that assignment locks in gains.

The only other fear is the “fear-of-missing-out”.

This is when the stock continues to rise after assignment, and investors feel they “missed out” on additional gains.

This is such a common emotion in trading that it has its own acronym – FOMO.

And it is not known as a good thing.

It is often seen as an emotional trap in trading.

When it comes to being assigned on covered calls, the only thing to fear is fear itself.

We hope you enjoyed this article on assignment on covered calls.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Source link