What Are Portfolio-Secured Short Puts?

To answer this question, bear with me as I go over some introductory concepts from the beginning for completeness, even though I know many of you already know this.

When an investor sells a put option, they collect a premium upfront.

In exchange, they agree to buy the underlying stock at a specified price if the option is exercised before or at expiration.

Contents

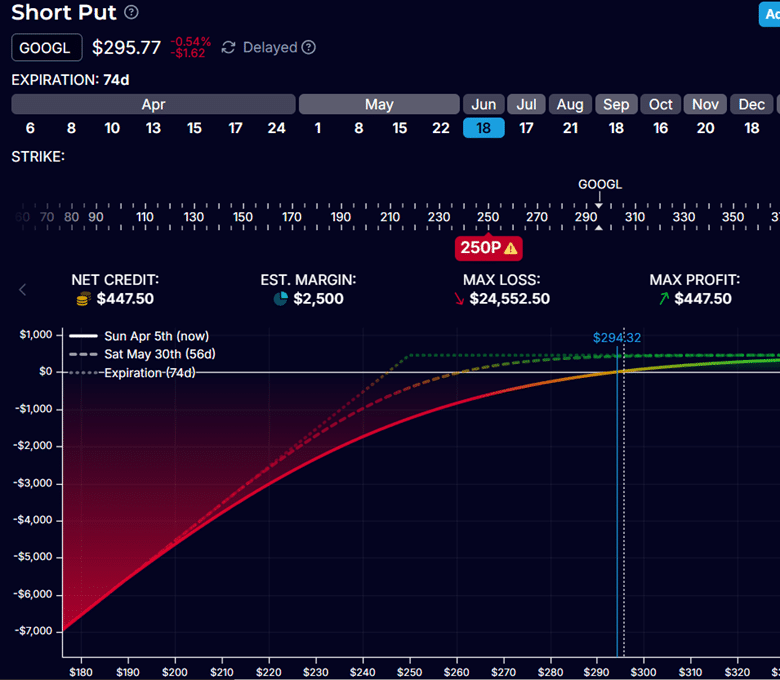

In the example below, an investor sells the $250-strike put option on Alphabet Inc. (GOOGL) expiring in 74 days and collects $447 of premium.

If GOOGL falls below $250 at expiration, the investor will be obligated to buy 100 shares at $250 per share.

This is perfectly fine if the investor intends or is willing to own the stock, as in the Wheel Strategy.

In certain types of retirement accounts, brokers may require investors to maintain enough cash in the account to fully cover the cost of purchasing shares if a short put option is assigned.

This is known as selling a cash-secured put, because the obligation of the short put is covered by existing cash on hand.

In our example, the investor would need $25,000 in cash.

The downside of a cash-secured put is that we have idle cash sitting on the sidelines.

Since that money is reserved for a possible stock purchase, it cannot be used for any other trades or investments.

As a result, the funds may sit idle for weeks or months, earning nothing while the investor waits for the option to either expire or be assigned.

Some investors may want to deploy that cash into use in the market (especially when the market is bullish).

Therefore, some traders use trading accounts with margin buying power to sell puts without having to set cash aside.

In our example, it is estimated that only $ 2,500 of margin buying power is needed.

This is known as selling a naked put option.

The broker will use the more politically correct term of selling an “uncovered put option”.

However, this flexibility comes with additional risk.

If the short put is assigned and the stock must be purchased, the trader must suddenly produce the cash required to buy those shares.

If they do not have sufficient available funds, the broker will issue a margin call, requiring the trader to deposit cash promptly.

To address the inefficiency of cash-secured puts and the riskiness of naked puts, some investors use a middle-ground approach known as a portfolio-secured put.

With this strategy, the investor still sells a put option, but instead of setting aside cash, the obligation is backed by the value of other assets already in the account.

These assets might include long stock positions, index funds, ETFs, U.S. Treasuries, or other investments.

The idea is that if the short put is assigned, the investor can sell some of their existing holdings to raise the cash needed to purchase the assigned shares.

This approach offers more efficient use of capital than a cash-secured put, because the investor’s entire portfolio remains actively invested rather than held in cash.

While portfolio-secured puts are less risky than fully uncovered short puts, they still require margin buying power.

This introduces some leverage beyond what is used in a cash-secured put.

A more aggressive investor, very bullish on Alphabet, might even increase leverage further by using the premium from selling GOOGL puts to purchase GOOGL call options.

However, during a sharp market selloff, the short put can be exercised at the worst possible time when both the assets backing the portfolio-secured position and the long call are also experiencing significant losses.

The decision to sell puts as cash-secured, portfolio-secured, or completely uncovered requires some planning to determine where on the risk and leverage spectrum the investor wants to be.

We hope you enjoyed this article on portfolio-secured short puts.

If you have any questions, send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Source link