Building A Covered Call Options Portfolio

When building a portfolio, the key is diversification.

When building an options portfolio, the key is also diversification – a point worth repeating twice.

We want to diversify across different underlyings.

We want to diversify across different expiration dates (or days-to-expiration, DTE).

And ideally, we want to diversify across different options strategies as well.

But for today, we’re focusing on the covered call strategy, as it’s often one of the first options strategies traders begin with.

Contents

Let’s build a $200,000 model portfolio with a handful of covered call positions.

In a pure options portfolio, it’s often prudent to keep a meaningful portion in cash (for example, around 50%) to help dampen large swings in the equity curve and provide flexibility for margin expansion in case certain positions go into drawdowns.

But since a covered call portfolio already has significant capital deployed in underlying stocks, it typically doesn’t require holding as much idle cash as a pure options portfolio.

Let’s start with an example of a covered call trade on Coca-Cola (KO), which is currently trading at $75.75 per share.

Date: April 17, 2026

Buy 100 shares of KO at $75.75/share

Sell one contract June 18th KO $77.50 call option at $1.65/share

The debit that we paid to purchase 100 shares of the stock is $7,575.

Since one option contract covers 100 shares, we collected $165 for selling the call option.

In return, we are obligated to sell our 100 shares of KO at the strike price of $77.50 per share whenever the option buyer exercises at any time before expiration.

If KO is above $77.50 per share at expiration on June 18th (which is in about two months), then for sure the call option is going to be auto-exercised, and our 100 shares will be sold, or “called away”, at $77.50 per share.

Coca-Cola is a dividend aristocrat stock, meaning it is a company in the S&P 500 that has increased its dividend payments to shareholders for at least 25 consecutive years.

It has an annualized dividend yield of 2.8%.

The next estimated ex-dividend date is on June 15, 2026, with an expected dividend of $0.53 per share.

So we plan to hold the stock until then, which is why we selected an option expiration of June 18th.

However, because the expiration falls so close to the ex-dividend date, there’s a possibility that the option buyer may exercise early – especially if KO is trading near or above $77.50 – resulting in the shares being called away a few days before expiration.

To reduce that risk, if the situation arises, we can buy back the short call a week before the ex-dividend date to remove our obligation under the contract.

While selecting a higher strike price (at, say, $85) would reduce the risk of losing the stock, it would yield a lower premium.

We want to sell calls that can generate between 1% and 4% in extrinsic time value per month.

An option’s value can consist of both extrinsic and intrinsic value.

You will understand intrinsic value later in the article.

Extrinsic time value refers to the portion of the option premium you receive that represents time value, expressed as a percentage of the cost you paid for the shares.

Because our call option is out-of-the-money (strike price above the current stock price), the option has no intrinsic value and is entirely extrinsic right now.

Therefore, the call option has $165 of extrinsic value, which is 2% of the $7575 investment over two months.

Hence, this covered call generates 1% per month of extrinsic value.

Selling strikes any higher would give less than this 1% of extrinsic value.

Remember that a covered call strategy is inherently bullish.

We want the price of the underlying to go up, even if it means having our stock called away.

After all, you can buy the stock again if that happens.

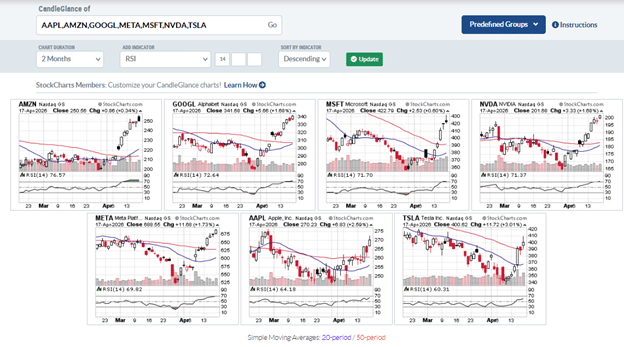

Therefore, let’s look for stocks with upward momentum.

When we sort the Magnificent Seven stocks by RSI over the past two months in descending order, we see that Amazon has been the strongest performer.

Source: StockCharts.com

While some may argue that its RSI is in overbought territory, stocks can remain overbought for extended periods.

Hence, we are still comfortable adding it to our portfolio.

Perhaps we will use a shorter days-to-expiration DTE.

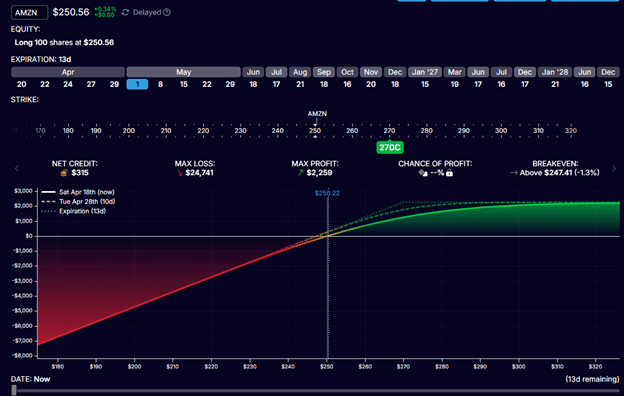

This is the P&L graph of an AMZN covered call with 2 weeks till expiration.

Date: April 17, 2026

Buy 100 shares of AMZN at $250.56/share

Sell one contract, May 1st, AMZN $270 call option at $3.15/share

$315 / $25056 = 1.2% in two weeks

This gives an extrinsic time value of 2.4% per month.

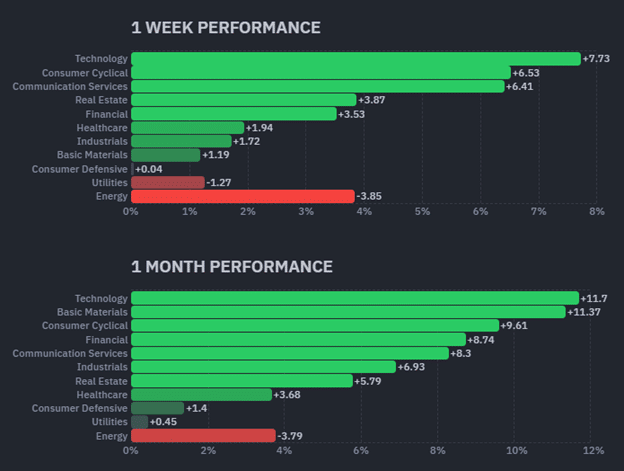

The technology sector has been leading the way both this month and this week.

Source: FinViz

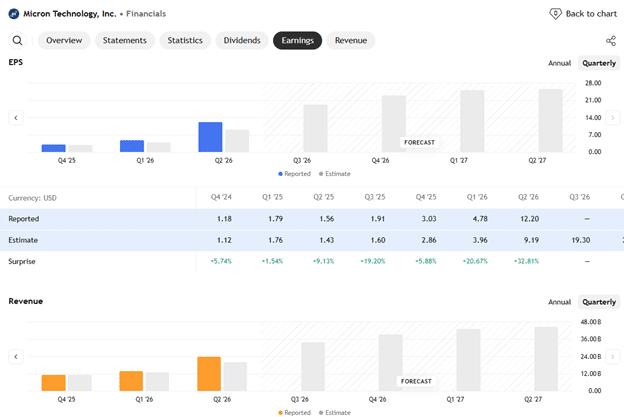

In the tech growth sector, we like seeing Micron (MU) earnings and revenue grow quarter after quarter…

Source: TradingView

We are buying 100 shares of Micron (MU) at $455.07 per share, and selling the $500-strike call option expiring in one month.

With a premium of $18.65 per share, we get.

$18.65 / $455.07 = 4% of extrinsic value per month.

Some traders like to size up when they have greater conviction.

This would be one such trade, as it represents a larger and more aggressive position.

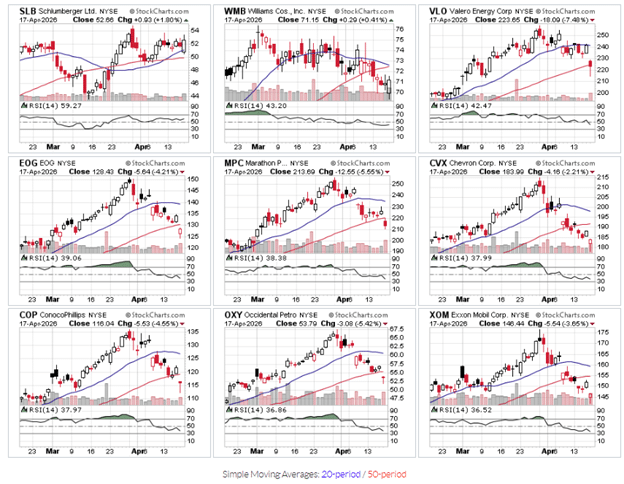

Although energy is underperforming right now, sectors can rotate quickly.

We will keep one small energy position in the portfolio for diversification and potential turnaround – only about a $5000 position.

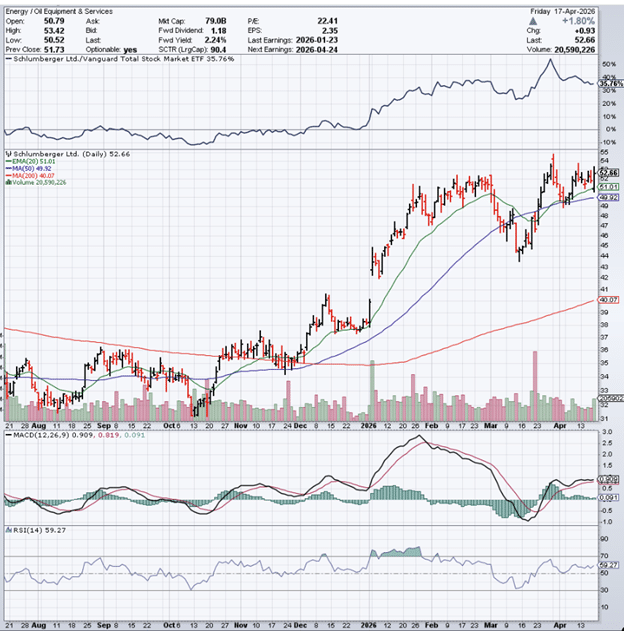

SLB is a stock with liquid options, holding up fairly well, with the price above its 20-, 50-, and 200-day moving averages, stacked in sequential order.

Source: StockCharts

Decent relative strength (top panel), positive MACD, and RSI above 50 make it a good pick over other energy names.

Source: StockCharts

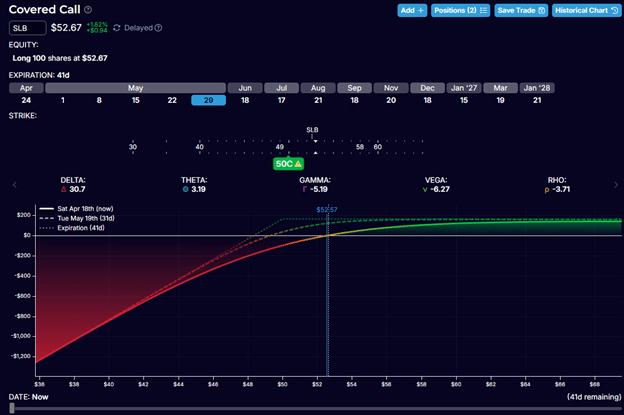

For better downside protection, we are going to sell an in-the-money covered call – that is, a call option with a strike price lower than the current stock price.

Date: April 17, 2026

Buy 100 shares of SLB at $52.66/share

Sell one contract, May 29th SLB $50 call option at $4.33/share

The P&L graph is similar in that we still want the stock price to go up…

One difference is that the bend in the expiration graph occurs at $50, below the white vertical line representing the current stock price, making this position more conservative.

With the option Greeks shown above, we already know it has a positive delta reflecting its bullish nature.

It also has positive theta, meaning time decay works in our favor.

It carries negative vega, so the position benefits from a decline in implied volatility (IV) over the life of the trade.

The stock only contributes to the overall positive delta.

Stock has zero theta and zero vega, so those are from the call option alone.

The stock will likely be called away at expiration, provided it is above $50.

That is fine because if we sell the stock at $50 per share, we still keep the $4.33 per share that was collected from the premium.

We would lose $2.66 per share on the stock.

$52.66 – $50.00 = $2.66

The net profit in the overall covered call trade would be $1.67 per share because…

$4.33 – $2.66 = $1.67

That is a net profit of $167 for the position if the stock is above $50 at expiration.

The $4.33 premium in the call option is composed of $2.66 of intrinsic value and $1.67 of extrinsic value.

The extrinsic time value captured is…

$1.67 / $52.66 = 3.2% over 41 days

On a per-month basis, this extrinsic time-value percentage represents 2.3% of invested capital, because…

3.2% x ( 30 / 41 ) = 2.3%

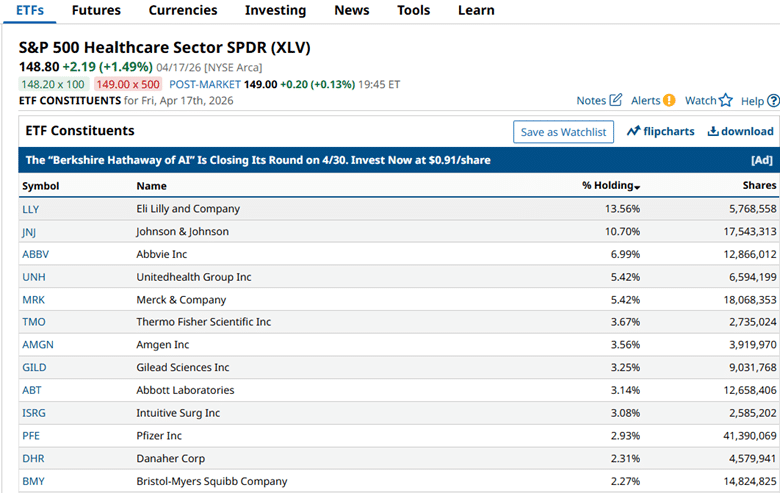

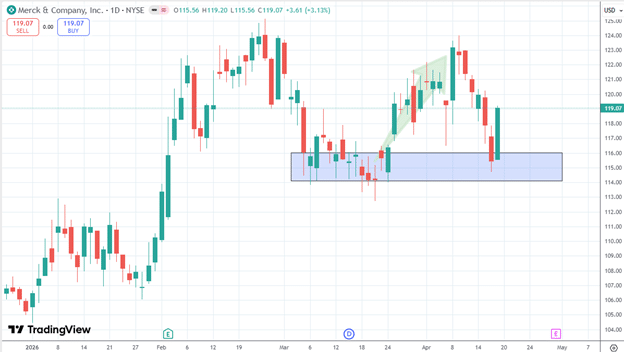

Taking a look at the top holding of the XLV healthcare sector ETF…

Merck (MRK) looks quite attractive, with its big green candle forming from a support buy zone…

Source: TradingView

We sell the at-the-money call option with a $ 120 strike and a May 22nd expiry, while simultaneously buying 100 shares of stock at $119.07 per share.

At a $ 4.28-per-share premium, we have a 3.6% extrinsic time value per month.

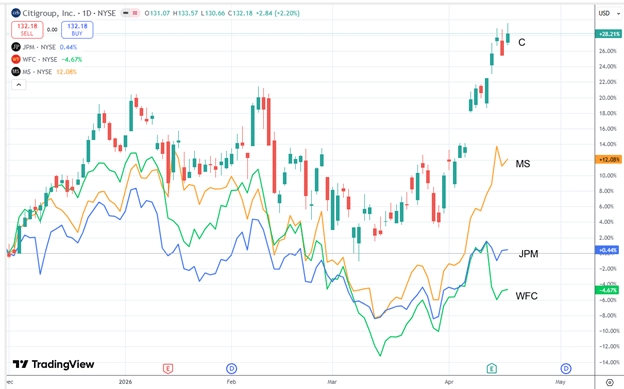

In the financials, we see that Citigroup has stronger relative strength than its competitors, including Morgan Stanley (MS), JPMorgan (JPM), and Wells Fargo (WFC).

We collect $3.20 per share by selling the $135-strike call with a May 15th expiry, giving us a 2.4% monthly capture rate.

At the same time, we buy 100 shares of C at $132.18 per share to cover our short call.

Adding GLD as a somewhat non-correlated commodity ETF to the mix, by selling the May 8th $460 call for $5.20 in premium.

And buying 100 shares of GLD at $445.88, giving us an overall 1.17% increase in extrinsic value over 19 days.

On a per-month basis, we are getting closer to 1.7% of monthly extrinsic value.

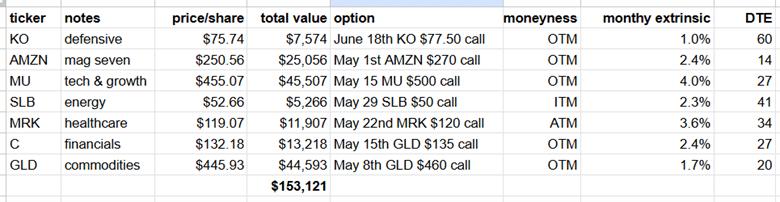

We have seven stocks across various sectors and with various days to expiry, using about $150,000 in capital, with about $50,000 in cash.

As is common, most of them are out-of-the-money covered calls.

They let us participate in some stock appreciation and collect premium income.

We have one in-the-money covered call and another at-the-money.

They all capture between 1% and 4% of the monthly extrinsic value, with expiration periods ranging from 2 weeks to 2 months.

By having staggered expiration cycles, we can rotate into new positions as the old position expires.

We don’t have to worry that our stock is called away.

When that happens, it means that the position has achieved its maximum profit.

The biggest risk is if the stock price falls too much.

Decide in advance where you need to exit the trade if the stock falls too much.

Additional considerations include earnings dates when the stock is likely to make a large move.

By purchasing quality stocks and selling covered calls, we allow the extrinsic value of those options to decay in our favor over time.

The premium we collect lowers our cost basis, and the dividend adds a second income stream.

We are effectively transforming the portfolio into one that is both capital-appreciating and income-generating.

Position sizing matters just as much as stock selection.

Allocating too much capital to any single covered call position, particularly in volatile sectors such as technology, exposes the portfolio to outsized drawdowns if that stock drops sharply.

A practical rule is to keep no single position above 20% of total deployed capital, and to revisit allocations whenever a position moves significantly against you.

We hope you enjoyed this article on building a covered call portfolio.

If you have any questions, send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Source link