Don’t Chase the Rocket Pt.1 – Fat Tail Daily

Everyone’s asking whether they should buy SpaceX.

It’s rockets. It’s space. It’s exciting — I get it.

In my opinion, the juice is not worth the squeeze.

Over the next two days, I’m going to give you two investment themes that can both ride and hedge against this moment instead.

Today is the setup. Why the world’s most important central bank has lost control of its own story. Tomorrow, the trade.

First, a little context.

Last Friday, more than US$1.3 trillion evaporated from the US stock market in a single session.

It was a two-punch combination.

The first blow came midweek, when Broadcom forecast US$16 billion in AI chip revenue for the quarter. Wall Street wanted more. In a sector priced for perfection, even a small miss was enough to start the bleeding.

Then came the knockout. A blowout US jobs report.

In normal times, strong employment is good news. But this market has been levitating on the promise of rate cuts. A hot labour market means those cuts are likely off the table.

Traders repriced accordingly, violently.

Chips led the wreck. Nvidia fell 6%, shedding more than US$300 billion (roughly an entire CBA) in an afternoon. Micron dropped double digits. The Philadelphia chip index logged its worst day since the ‘tariff tantrum’ selloff of April 2025.

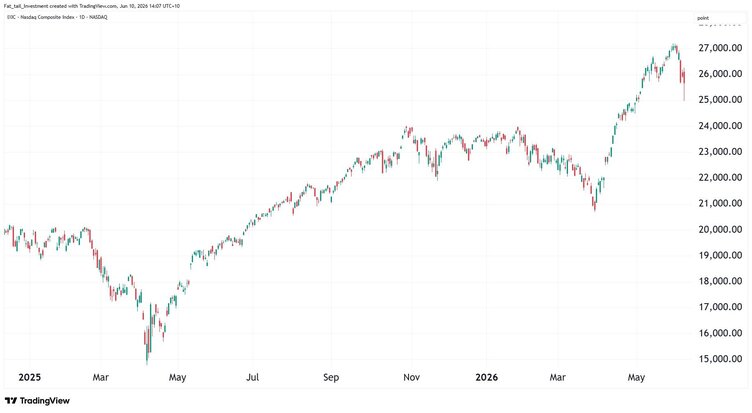

It was hardly a surprise; all good things must come to an end, and Nasdaq snapped a nine-week winning streak.

Source: TradingView

[Click to open in a new window]

At the time of writing, the selling hasn’t stopped. Tech has taken another leg down despite many retail investors eager to buy the dip, as institutional investors continue to offload.

All up, somewhere north of US$3 trillion has now been wiped from US stocks in just a few sessions.

And right on cue, the next shiny object arrives. SpaceX goes public this week at a US$1.75 trillion valuation. The largest IPO in history… and priced beyond perfection.

‘On to the next launchpad!’ The punters will say. I’d argue the only thing about to rocket is Musk’s net worth.

Some may agree, while others will laugh at me when the stock inevitably goes up 20% on debut.

Feel free to hop on, but just go in with eyes wide open.

Instead, here’s my different approach. But first, you need to understand why a good jobs number can vaporise trillions. And why the world’s most important central bank is stuck with no good options.

A Hawk Hired to Be a Dove

Next week, Kevin Warsh chairs his first meeting as head of the US Federal Reserve.

Markets have priced it as a non-event. I think that could be a mistake.

Not because of the rate decision, which will inevitably be a hold. Because of every bit of signalling that’s going to come from the man himself.

Remember the setup. Warsh spent his career as one of the most hawkish figures in central banking. Trump appointed him in January for one reason: he had publicly converted to the cause of lower rates.

Back then, the case was at least arguable. Inflation looked beaten, and the US jobs market was wobbling.

That case has since fallen apart.

US payrolls grew by an average of 188,000 a month from March to May. Unemployment has fallen to 4.3% and held. The Atlanta Fed has second-quarter growth running at a 3% annualised pace.

And the oil shock from the Iran conflict — the same one we’ve felt at every Australian bowser — has pushed US inflation to 3.8% on the Fed’s preferred measure. Nearly double its target, in an overshoot now running five years deep.

I wrote a fortnight ago about Warsh’s plan to shuffle the goalposts with a ’trimmed mean’ inflation measure to justify cuts. That tells you plenty. When the data won’t cooperate, change the data.

But by any honest reading, US rates should stay higher, not lower.

The street has caught on. Goldman Sachs just pushed its rate-cut call all the way out to 2027, and futures markets now price a rate hike by year’s end as the more likely outcome.

Imagine being hired to cut rates, then handed this economy.

Less Butter, Fewer Guns

Zoom out to the next decade, not the next meeting.

The US can no longer afford its own medicine.

Washington spent around US$970 billion servicing its debt last year. That’s more than the entire defence budget and nearly a fifth of every dollar collected in revenue.

Gross federal debt sits around 124% of GDP. Some may argue that this can go much higher under the protection of the US’s ‘exorbitant privilege’ — and it likely can, but there are always limits.

That privilege of the US dollar as the reserve currency rests on a fuzzy line that intersects geopolitics, financial expediency, and international trust.

We’re talking about trust in the US economy, its courts and institutions, and its democracy to hold it all together. History tells us that when trust erodes, the chessboard can inexorably shift.

A risk hedge here, a diversification there. Financially and politically, these stack up until a great power is no longer.

Economic historian Niall Ferguson describes one of these limits in his Ferguson’s Law. This law simply states:

‘Any great power that spends more on debt servicing than on defense risks ceasing to be a great power.’

Less butter, fewer guns. A simple heuristic, but it has a wider meaning in my eyes.

Debt at this level constrains choice. It narrows your wiggle room to respond to a crisis and diminishes your global influence.

Now bring this to the present moment:

- Warsh was confirmed by the narrowest margin for any Fed chair in modern history

- He inherits a central bank with inflation at a three-year high, and an oil shock pushing it higher

- Yet he was hired by Trump (who wants them lower), and he looks ready to oblige

Close to US$10 trillion of US debt rolls over in the next twelve months. Every extra point of yield feeds straight back into the deficit.

So play it forward. Hike to fight inflation, and the interest bill becomes the crisis. Cut to please the White House, and inflation expectations slip the leash.

There is no door marked ‘everything is fine’.

So that’s the box. A market priced for perfection, a Fed that doesn’t want to hike and can’t credibly cut, and dollars looking for a home.

On Saturday, I’ll show you where I think it ends up. Two themes.

Both, conveniently, sit under Australian dirt.

Until then.