US Government…Meet the AI Bond Market – Fat Tail Daily

“I want Kevin to be entirely independent”

—Trump swearing in new US Fed Chair Kevin Warsh (May 2026)

Who told Trump to pick Kevin?

And why did he have to say this?

It’s not who you think it is.

It’s not JD, Marco, Melania, Kushner or the usual suspects.

In fact, the answer is so boring.

And that’s why it’s so scary.

Knock down all the cards in this game of Guess Who…

Give up?

It’s the giants of the fixed-income market.

I’m talking about the heads of BlackRock, Vanguard, PIMCO and JPMorgan Asset Management.

Flashbacks and new realities

Now, please join me down the rabbit hole for a game of 5D global financial system chess…

In January, I wrote this piece about the bond market – where I highlighted this 3rd of December 2025 article in the Financial Times:

Source: The Financial Times

In November and December last year, the US Treasury did a pulse check.

Before Trump picked his new Fed Chair, his team rang around the big end of the bond market to take the temperature from the banks and the asset managers who actually own this debt.

The frontrunner was a bloke named Kevin Hassett, seen as very close to Trump and very keen to slash rates no matter what inflation was doing.

The bond crowd sent back a blunt message.

Pick Hassett, and we will treat it like a “Truss moment”.

If you remember my January note, that was the 2022 episode where the UK bond market chewed up and spat out Prime Minister Liz Truss in roughly 6 weeks.

Hassett got passed over.

Kevin Warsh got the nod instead and was sworn in on 22 May.

And there was Trump, in public, telling his own appointee to “be entirely independent”.

Trump was told what to do.

Or at the very least, he knew what he had to say.

Crazy.

So who actually runs the show?

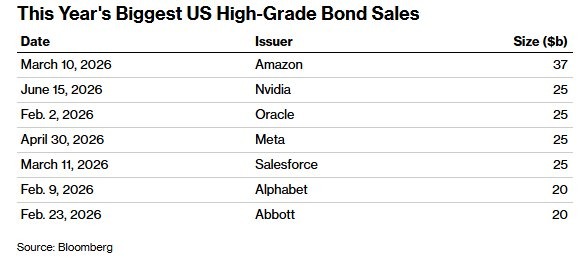

In 2026, five tech companies will issue more new investment-grade debt than the entire US financial sector did a decade ago:

Source: Bloomberg

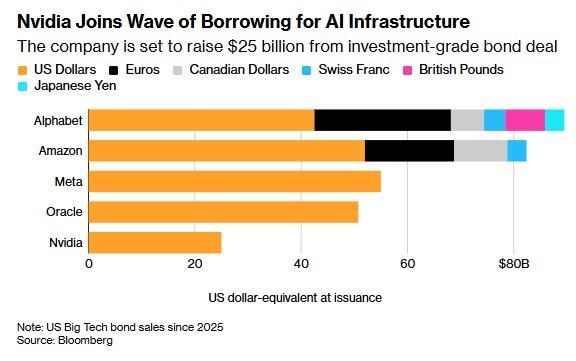

The latest news today is that Nvidia is now putting out the call for its own bonds to the tune of $25BN:

Source: Bloomberg

Here’s some context on how much investors like hyperscaler bonds…

Amazon’s March 2026 $37bn USD bond deal attracted $126 billion in peak orders — a 3.4x oversubscription — while the most recent comparable US 10-year Treasury auction of $39bn drew $93 billion in bids, at “a 2.4x bid-to-cover ratio”.

Roughly speaking — investors were 42% more eager, in relative terms, to lend to an AI/tech/retail company than to the US federal government.

The hyperscaler-fixed income industrial

complex makes the rules

The scale is getting hard to ignore.

Hyperscalers have already overtaken US banks as the single largest sector in the investment-grade bond market, accounting for roughly 15% of all issuance.

JPMorgan tips that to pass 20% by 2030, and Apollo reckons half of the ten largest US investment-grade borrowers will be hyperscalers by the end of the decade.

So, if hyperscaler bonds are one in every five dollars, and those same funds are stuffed with Treasuries, the health of Meta’s and Amazon’s debt is now wired directly into the institutions that keep governments honest.

(And not spending like madmen)

AND: If the AI debt pile wobbles — it bleeds straight into the funds that discipline Washington.

The biggest buyers of this mountain of hyperscaler debt are BlackRock, Vanguard, PIMCO and JPMorgan Asset Management.

Those same funds happen to be the biggest holders of US government bonds, AND they are the exact names the Treasury rang up about the Fed Chair job.

If bonds are boring, they are also the scariest thing to think about.

Nightmare sauce

Imagine this…a string of bad earnings from the hyperscalers.

Things get toxic.

Fast.

Hyperscaler capex hit 22% of revenue in 2025, against a historical average of 12.5%, and UBS calculates this year’s capex will swallow nearly 100% of operating cash flow versus a 10-year average of around 40%.

A couple of bad quarters, bond demand falls off… and the self-funding story falls apart.

And then big pressure builds in what is (for now) the biggest money tap in the world.

The US Fed might suddenly have to swing the other way and cut hard and fast to stop the bleeding.

Where does that leave us on the ASX?

How scared should we be?

Answer: Not as much as you think.

Depending on how much time you have.

The Aussie market lagging the

US might be a blessing

It’s been hard watching SpaceX and the AI IPO season push the US market to infinity while the ASX remains mired in yet another self-inflicted quagmire.

There is a silver lining though.

And it’s commodities.

Mining capex cuts over the last 10 years are flowing through to commodity prices.

Generally speaking, our ASX commodity stocks are still not fully absorbing the remarkable commodity price uplift.

The new mines simply are not there.

That is the supply side of the equation quietly tightening while everyone stares at AI stocks.

High prices today do the hard work by pushing forward the investment that eventually brings supply back and cools prices down the track.

Falling commodity prices over a long enough horizon then help pull inflation lower.

I think that single mechanism could do more heavy lifting on inflation than any rate-tightening cycle has managed so far, especially with the US deficit ballooning, debt servicing costs rising, and debt refinancing cliffs approaching.

The solution: Make things, real things, cheaper.

And then all our problems go away.

That’s the idea anyway.

Australia, the pressure release valve

When the proverbial hits the fan, the bond market, the Fed and the whole global financial system need somewhere for the pressure to escape.

Over a long enough horizon, that valve is real stuff coming out of the ground, and this is exactly where Australian investors and the ASX are sitting pretty.

We are the ones who can supply the world with the raw materials it needs when the financial engineering finally meets reality.

Keep your head

Look, there could be a big crash ahead.

In fact, there always is.

Trust in the boom and bust.

A third of fund managers surveyed by Bank of America in May named AI capex as the most likely trigger for the next systemic credit blow-up, double the share from a month earlier.

The parallel many are whispering about is the late-1990s telecom bubble, where fibre overbuild ended in mass defaults and a credit freeze that took six years to thaw.

The key is to keep your head while everyone else loses theirs.

See the big supply and demand forces in the world economy for what they are.

Imperative hungers that need to be satiated.

The hyperscalers borrowed against a future they have not built yet.

That means Australia has to dig up the present.

And keep digging into the future.

Source link