Loma Negra Is Feeling The Argentinian Recession; The Stock Is Not An Opportunity (NYSE:LOMA)

RicAguiar

Loma Negra Compañía Industrial Argentina Sociedad Anónima’s (NYSE:LOMA) 2Q24 results were pretty bad, in line with a challenging Argentinian macroeconomy. Sold volumes were down 30%, and the company stopped its clinker production and grinding operations. The effect was not felt as much in operating earnings because of higher prices and cost-cutting measures (like the plant halts mentioned).

On the control side, and not mentioned during the call, Loma Negra’s controller, the Brazilian Intercement, had to file for a protective injunction last month, leaving the door open for a potential sale of Loma’s controlling stake to another player. For the time being, the Brazilian Companhia Siderurgica Nacional, CSN, maintains an exclusive negotiation right.

On the valuation side, the company has remained in a tight price range for the past three years without arousing the interest that other Argentinian stocks (for example, in energy) have generated since 2021, especially since the new administration took office. Given that the company’s earnings yield is not high enough to justify its purchase and that growth expectations are still negative for the rest of the year (with next year always being an unknown in Argentina), I still believe the stock is a Hold at these prices.

Terrible 1H24

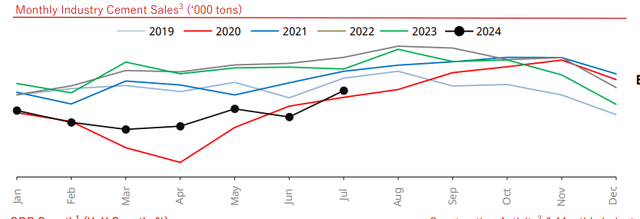

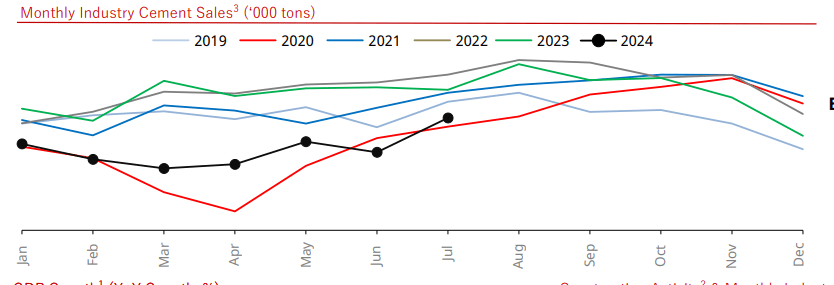

Cement downturn only comparable to the pandemic: Argentina is undergoing a significant recession, with the economy expected to fall to mid-to-high-single digits this year. The situation is even worse for cement for three reasons. First, retail buyers see their disposable income shrink and have less money to invest in building their homes. Second, real estate developers see the supply of properties increase without buyers, look at the dollar cost of building, at record highs measured at the parallel FX, and decide not to build. Finally, the national government decided to stop all public works in December, therefore totally drying up government demand. Cement has not had a worse year since the early pandemic, as seen below.

Argentinian cement dispatches (LOMA’s 2Q24 earnings presentation)

This has shown up in Loma’s volumes, collapsing 30% in 2Q24 versus last year. In the case of concrete, which is used in large construction projects, volumes are down 45%.

Short-term margin improvements: The company’s margins have actually increased despite the terrible topline situation, 500 basis points in both gross and EBITDA. This led to the company being able to post an 11% contraction in adjusted EBITDA and a 12% contraction in operating income.

There are two reasons for this. First, the company has not raised salaries much and has probably put some work shifts on hold, so OpEx has decreased in line with production by around 30%. The second reason is that the company literally halted production in key areas. Citing savings from not using electricity and natural gas during the more expensive winter months, Loma halted clinker cooking and limestone grinding. This can help reduce the energy bill and the payroll for some months, but stopping the plant is not viable long-term. In addition, when cement plants are not producing at scale, the inventories generated during those periods are more expensive (because they have to absorb more overhead per unit), which shows up in much lower margins in future months.

Some hope: Loma’s management cited the month of July as one of recovery, with dispatches down 14% versus last year. It also points to the positive trend between April and July, seen in the national chart above. This could very well be the case, particularly because during July, the FX gap expanded, leading to a reduction in dollar-denominated construction costs and, therefore, making real estate development more attractive. However, the gap has shrunk in August, and there are evident seasonal factors in 2Q and 3Q. I believe it is still too early to call an end to the current construction recession.

Controller trouble

Loma Negra’s controller, the Brazilian cement conglomerate Intercement, has been sagged by debt for years. This has led to IC offering Loma Negra’s stake for sale for some years (the first negotiations started in 2018). Although IC has been able to sell operations in Africa, it has not yet been able to sell its Loma stake.

The latest chapter in this story includes IC filing for asset protection in Brazil, as Loma informed the SEC last month. The injunction does not imply any operational problem for Loma but does make the sale of Loma’s equity sake more pressing.

In this respect, the main potential purchaser is another Brazilian company, Companhia Siderurgica Nacional, which has an exclusive negotiation right (recently renewed until early August and then automatically renewed again). CSN is negotiating to purchase all of IC’s assets, among which Loma is only a portion.

In any case, it is unlikely that either IC or CSN will sell Loma’s stock in the open market, dampening the stock price. However, the potential change of controller could spur more interest from other strategic players. One such player is an Argentinian businessman with stakes in Pampa Energía S.A. (PAM), involved in construction, and interested in purchasing Loma’s stake alone.

Valuation not attractive despite yield

Evaluating Loma’s situation this year is not very correct, given that the country is in a tremendous recession. It would be equivalent to valuing Loma based on 2020 profitability.

In my last article, I used a more long-term approach to forecasting Loma’s profitability; it includes EBITDA margins and cement dispatches during different periods, including booms like 2021/22 and busts like 2018/2020.

The most negative scenario, with current volumes and 2018 margins per ton, implies about $55 to $60 million in cash profits for the company. Compared with a market cap of about $820 million, this represents an elevated multiple of 15x. Therefore, in the most negative scenario, Loma offers a yield of approximately 6.6%.

If we assume that margins do not fall to 2018 levels or that eventually, volumes improve (say to 15% lower than the booming 2023 levels), then we could be talking of $70 million in profits. I believe this yield is more fair, albeit not particularly attractive, given that Argentina consistently fails to grow above the 2021/22 levels. If Loma is destined to cycle between booms and busts, then we cannot project cycle-average profitability way above $70 million, and therefore, the stock is not an opportunity. For that reason, I maintain my Hold rating.

Source link