Iron Condor Adjustment Strategy

After learning how to set up an iron condor options strategy, learning to adjust an iron condor is the next step.

We will explain all this via one long example covering multiple adjustment techniques.

The key is to understand the fundamental concepts that underlie all of the adjustment techniques.

These techniques are categorized as either an attacking adjustment or a defending adjustment.

Contents

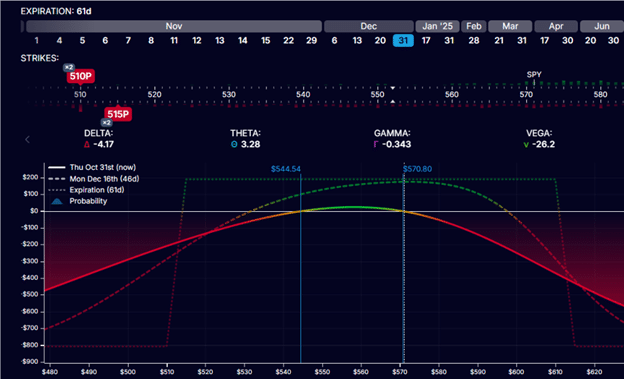

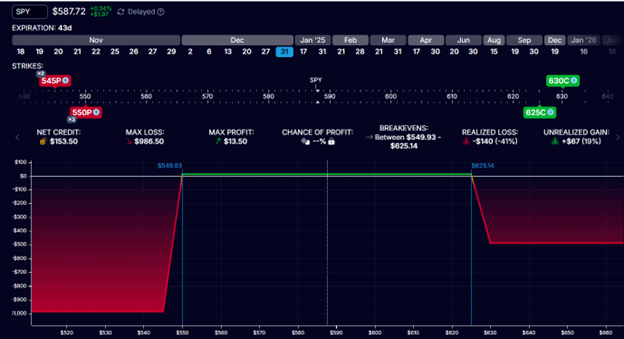

An iron condor involves selling an out-of-the-money call spread and an out-of-the-money put spread, like the following iron condor on SPY (the S&P 500 ETF) initiated on Halloween day of 2024, about one week before the 2024 United States presidential election.

So, this will likely move the market a bit and give us some adjustment opportunities.

Date: Oct 31, 2024

Price: SPY @ $570

Buy two Dec 31 SPY 615 call

Sell two Dec 31 SPY 610 call

Sell two Dec 31 SPY 515 put

Buy two Dec 31 SPY 510 put

Credit: $190

The investor receives a net credit of $190 for selling two contracts with the risk graph looking as follows:

The important things to monitor on the risk graph and modeling software are:

- Where the price (indicated by the vertical white line) is located in relation to the two credit spreads.

- How far above zero is the max profit of the expiration line (dotted straight line).

- How far below zero is the maximum risk of the expiration line.

- The delta of the short put and the short call.

- The curvature of the T+0 current profit line (the solid red-and-green curved line)

With the price of the underlying on the horizontal bottom axis and the P&L on the left vertical axis, we see that the current price of SPY is $570.

The max profit at expiration is $200, and the max loss is $800, giving us a condor with an initial risk-to-reward for 4-to-1.

The put credit spread has the short put at $515, which is around the 12-delta on the option chain.

The call credit spread has the short put at $610, also around 12-delta.

The curvature of the T+0 line is sloping slightly but within acceptable limits.

It is sloping in such a direction that if SPY increases in price, the P&L drops.

If the price goes down, the P&L rises.

This means the position has a negative delta.

You can see the positional delta in the modeling software is showing -4.17.

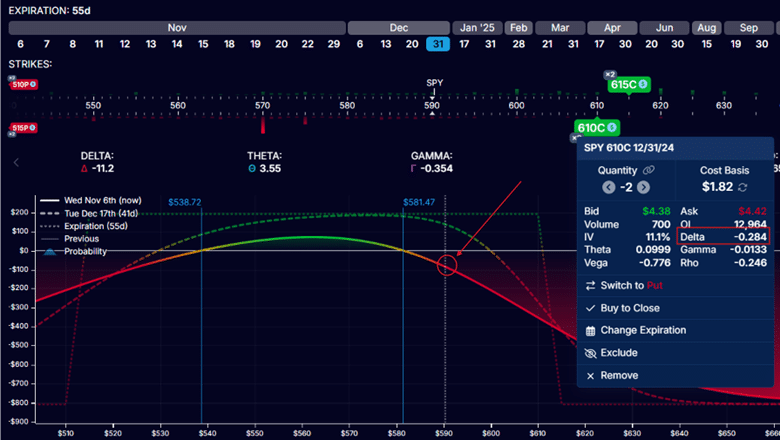

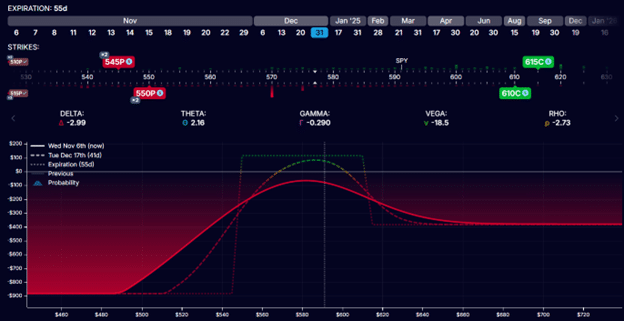

The market rallied after the election results were announced on Nov 6, threatening the call spread. P&L is -$84.

The short call is now at 28-delta, a significant increase from its original 13-delta.

Notice where the white vertical line (price of SPY) crosses the T+0 curve.

The slope has increased, as shown by its more negative position delta of -11.2.

It is time to adjust.

We sold two contracts for the Iron Condors to give us a bit more flexibility and enable us to demonstrate a defending adjustment.

The call spreads are threatened because the price is moving towards the call spreads.

We reduced the number of call spreads by closing one of the call spreads by paying a debit of $135.

Buy one to close $610 call

Sell one to close $615 call

Debit: -$135

Next, we see that the short put is very far away at the 5-delta.

We will also perform an attacking adjustment by rolling the spread up closer to the SPY price for a net credit of $40.

Buy two to close $515 put

Sell two to close $510 put

Debit: -$30

Sell two to open $550 put

Buy two to open $545 put

Net credit: $70

Our new position has a reduced positional delta of -2.99.

You can also see that the slope of the T+0 line has decreased.

Remember, the call spread is a bearish spread.

The put spread is a bullish spread.

When the price of the underlying moves up, we need to make the trade more bullish.

Therefore, we increase the power of the put spread by moving it closer to price.

And we decrease the power of the call spread by reducing its contracts.

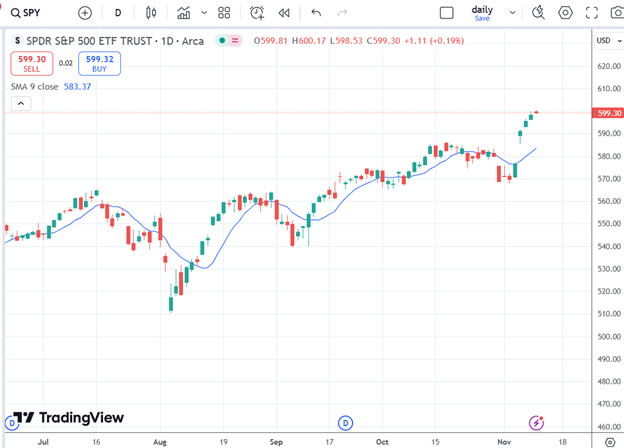

On Nov 11, SPY continued to go up, reaching 600.

Price is attacking the call spread again.

See how much closer the white vertical line is to the call spread compared to the put spread.

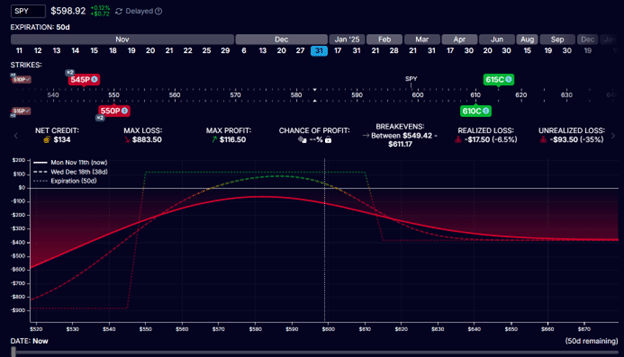

This time, we defend the call spread by rolling the call spread up away from the price.

Date: Nov 11

Price: SPY @ $599

Buy to close one Dec 31st SPY 610 call

Sell to close one Dec 31st SPY 615 call

Debit: -$186

Sell to open one Dec 31st SPY 625 call

Buy to open one Dec 31st SPY 630 call

Credit: $80

This is a net debit of -$106 for the rolling adjustment.

The resulting graph shows we now have more room for the call spread.

Also, we have a flatter T+0 curve.

One problem is that the maximum profit of the expiration graph has dropped.

It is getting very close to the zero profit horizontal.

But the trade still has 50 more days till expiration.

We will find an opportunity to raise this profit potential later.

While the short $550 put is far out of the money at the nine delta, we opted not to make an attacking adjustment with the put spread at this time for fear that SPY might pull back and drop in price and the put spread will become too close.

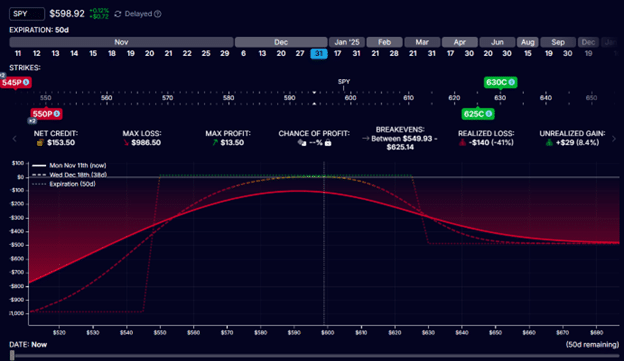

On Nov 18, the SPY price dropped to $588, and the short call was at the 5-delta.

Since we have two put spreads and only one call spread at the moment, we can add back another call spread without increasing the max risk in the trade:

Sell one Dec 31 SPY 615 call

Buy one Dec 31 SPY 620 call

Credit: $50

We positioned the short call of the new call spread at around the 15-delta for a credit of $50.

This is an attacking adjustment because we make the call spreads more powerful.

Note that it has the effect of increasing our maximum potential profit in the expiration graph.

This is typical when we receive a net credit for an adjustment.

AFTER:

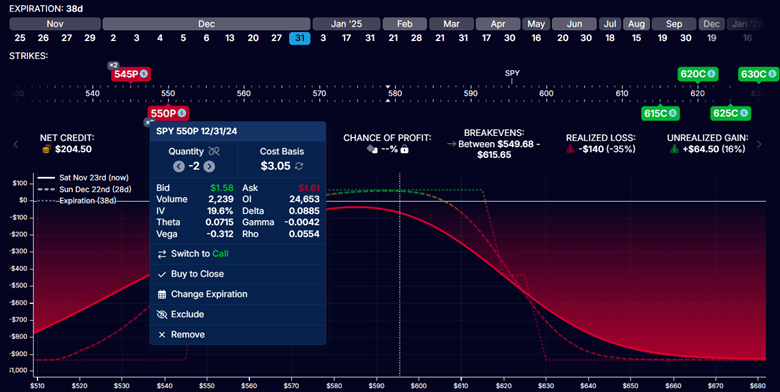

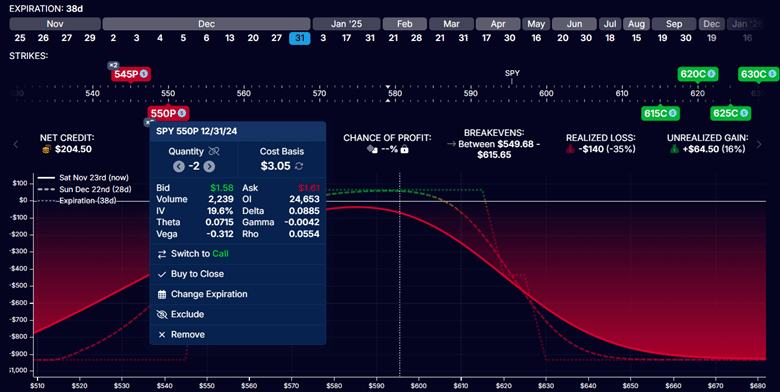

On Nov 22, the short $550 put option has moved far out of the money at the 8-delta:

BEFORE:

Note that the max profit is $65, and the max risk is $935 right now before we show you the next adjustment.

This adjustment will be an attacking adjustment, making the put credit spread stronger with wider wings.

We will roll the short puts up without moving the long puts.

Buy to close two contracts Dec 31 SPY $550 put

Sell to open two contracts Dec 31 SPY $555 put

Credit: $48

AFTER:

The max potential profit increased to $112.

It had increased by the amount of the credit received.

However, the max risk has risen to $1887, which some investors may not want to have.

By widening the wings of the put credit spread from 5 points wide to 10 points wide, we doubled the risk in the trade.

There are a variety of ways to adjust iron condors, which involve decreasing or increasing the number of contracts, rolling spreads, and changing wing widths.

These are the most common adjustments; others have created even more creative ones.

By knowing the Greeks and understanding the risk graph, you can also develop your own adjustments.

They all try to achieve the same thing: keep the directional risk of the trade within a certain tolerance while maintaining a decent profit potential.

We are attacking and getting a credit by moving spreads closer to the price.

We are defending and paying a debit by moving the threatened spreads away from the price.

By decreasing the number of contracts in a spread or narrowing a spread, we are defending by weakening the spread.

We are attacking and making the spread stronger by increasing the number of contracts or widening the spread.

As in any game, sometimes you want to play offense and sometimes play defense.

We hope you enjoyed this article on different iron condor adjustment strategies.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Source link