Looking Beyond the Hyperscalers: The Hidden AI Infrastructure Plays Most Investors Are Missing

The artificial intelligence investment narrative has become increasingly predictable.

Nvidia.

Microsoft.

Alphabet.

Meta.

Amazon.

Apple.

Tesla.

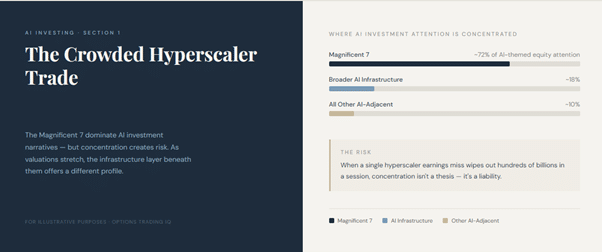

The Magnificent 7 dominate headlines, analyst reports, and portfolio allocations.

And while these companies have undeniably been central to the AI buildout, fixating on them risks missing what could be the more durable, less crowded opportunities sitting quietly in the infrastructure layer beneath them.

Goldman Sachs Asset Management has been making exactly this argument — that the real AI opportunity extends well beyond the hyperscalers, into the pick-and-shovel companies that enable the entire ecosystem.

Two areas in particular stand out: fiber optic infrastructure and AI-adjacent data and security software.

Neither is as flashy as a chatbot or a foundation model.

Both may prove more essential.

Contents

There’s nothing wrong with owning the Magnificent 7.

These are extraordinary businesses.

But as valuations have expanded on the back of AI enthusiasm, the margin for error has thinned.

When a single earnings miss from a hyperscaler wipes out hundreds of billions in market cap in a single session, it raises a reasonable question: are there other ways to participate in AI’s growth with a different risk profile?

The answer, increasingly, appears to be yes.

AI infrastructure is a massive, multi-decade buildout, and the hyperscalers are the customers, not the only suppliers.

The companies building the physical and digital backbone of the AI era are worth a closer look.

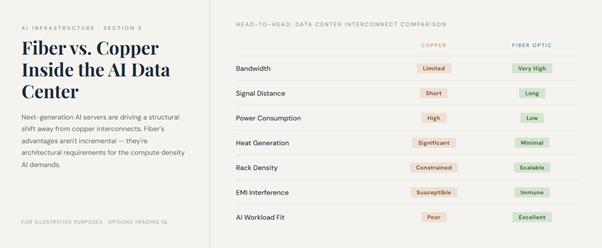

Most people associate fiber optic cables with long-haul internet connectivity – the undersea cables and transcontinental links that carry data between continents.

But a significant transition is now underway within data centers, where fiber is rapidly displacing copper as the interconnect of choice.

Next-generation AI servers demand extraordinary data transfer speeds.

The training frontier models for compute clusters are enormous, often spanning thousands of GPUs that must communicate with each other constantly and at very low latency.

Copper cables, which have served data centers adequately for decades, are hitting their physical limits.

They can only carry data so far before signal degradation becomes a problem; they consume more power, they generate more heat, and they simply can’t match the bandwidth fiber provides.

Fiber optic cables solve all of these problems simultaneously.

They offer superior bandwidth, carry signals over longer distances without degradation, consume less energy, and enable higher density configurations — meaning more compute can be packed into the same physical footprint.

For AI workloads, which are uniquely data-intensive and latency-sensitive, these advantages aren’t marginal improvements.

They’re architectural requirements.

Goldman Sachs Asset Management sees the companies supplying this fiber infrastructure as direct beneficiaries of the AI buildout, with demand that is structural rather than cyclical.

Every new AI data center built, every GPU cluster deployed, and every hyperscaler capacity expansion creates incremental demand for fiber-optic components.

This is a market that grows with AI capital expenditure, but the companies serving it tend to trade at much more modest valuations than the hyperscalers themselves.

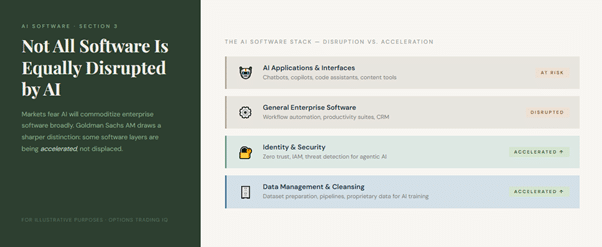

The second opportunity area is perhaps even more counterintuitive.

Conventional wisdom suggests that AI is disruptive to enterprise software — that large language models will commoditize functionality that previously required expensive, specialized tools.

For broad software categories, that concern may be legitimate.

But Goldman Sachs Asset Management draws an important distinction: not all software is equally exposed to AI disruption.

Some software is actually being accelerated by AI.

Data management and cybersecurity fall squarely into this category.

Consider what’s required to train a useful AI model on proprietary business data.

The data must first be collected, then cleaned and normalized, then structured and labeled, then stored in a format compatible with AI training pipelines.

Most enterprises find their data is a sprawling mess — siloed across legacy systems, inconsistently formatted, riddled with duplicates, and lacking the quality controls needed for reliable AI training.

The scramble to build AI capabilities is forcing companies to finally tackle the data hygiene problems they’ve deferred for years, and that’s driving significant investment in data management and cleansing software.

Security is similarly accelerated.

As AI agents — systems that take autonomous actions on behalf of users — become more prevalent, the attack surface for cybersecurity threats expands dramatically.

An AI agent with access to sensitive systems is a powerful capability and a significant vulnerability.

Identity and access management, zero-trust architectures, and advanced threat detection all become more critical as agentic AI proliferates.

Companies specializing in these areas are seeing demand pulled forward rather than disrupted.

While the market broadly discounts enterprise software amid AI disruption fears, Goldman Sachs Asset Management takes the opposite view in these specific segments: the AI transition is a tailwind, not a headwind.

Companies that help enterprises build trustworthy, secure AI pipelines are providing something the hyperscalers themselves can’t easily replicate — deep integration with existing enterprise infrastructure and the trust that comes from years of customer relationships.

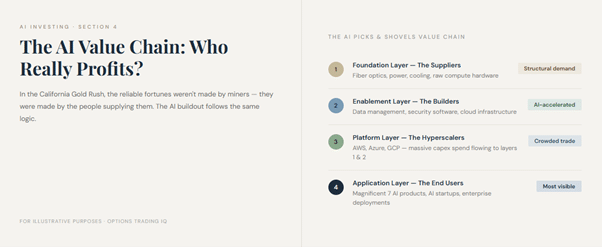

The gold rush analogy gets overused in technology investing, but it contains a useful insight: the most reliable fortunes in California’s gold rush weren’t made by miners.

The people selling picks, shovels, denim pants, and provisions to the miners made them.

The extractors took the risk; the suppliers took the revenue.

AI is not a zero-sum competition for who builds the best model.

It is a generational infrastructure buildout touching nearly every layer of the technology stack.

Fiber optics companies, data management vendors, and cybersecurity specialists aren’t speculative bets on AI succeeding — they’re businesses whose demand curves are already bending upward because AI is succeeding.

For investors looking to participate in AI’s continued growth with less concentration risk and potentially more attractive valuations, looking beyond the Magnificent 7 isn’t contrarianism.

It’s diversification with a thesis.

We hope you enjoyed this article on AI infrastructure beyond the hyperscalers.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Source link