CWS Market Review – October 7, 2025 Crossing Wall Street

CWS Market Review – October 7, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

On Tuesday, the stock market snapped its seven-day winning streak. This was the market’s longest winning streak since a nine-day run this spring. Perhaps the government should shut down more often!

For much of the morning, it looked like we were headed toward another up day, but the bears charged in and brought stock prices down. Interestingly, this was a day where defensive stocks did the best, and higher risk trailed the market.

It seems like it was years ago, but the market had a very rough time this past April. Not only did the S&P 500 have its largest daily point gain, but it also had three of its six largest daily point losses. This spring was one of the most raucous periods in recent market history, and it ended exactly six months ago today.

The current market isn’t anything like that. In fact, I continue to be impressed by how serene this market has been. Consider that from January 1 to June 16, the S&P 500 had 22 daily drops of more than 0.8%. Since then, it’s happened once.

It’s not just stocks that are rallying. The price of gold soared over $4,000 per ounce for the first time. Adjusted for inflation, gold is higher now than it was at its mega-peak from 35 years ago.

The Midas metal is on pace for its best year since 1979. This could be the third straight year of double-digit gains for gold. The gold rally may not be over. Goldman Sachs said gold will reach $4,900 per ounce before the end of next year.

Historically, gold has tended to move in two speeds: relentlessly higher and plunging downward. I’m exaggerating, but gold does tend run either hot or cold and not much in between. Right now, it’s hot.

Gold is certainly being helped by the Federal Reserve which is expected to continue cutting interest rates. Also, the U.S. dollar has slumped this year. Other safe investments like the Japanese yen have lost ground recently.

Gold now trades at 81 times silver. The gold/silver ratio is one of the oldest prices known to man. It’s been followed since antiquity. Plato mentioned that the ratio was 12-to-1.

In 1792, the U.S. Congress, at the advice of Alexander Hamilton, passed the Coinage Act of 1792. This was the government’s first attempt at price-fixing (and not the last). The act defined a U.S. dollar as 371.25 grams of silver or 24.75 grams of gold. In other words, Hamilton pegged the Gold/Silver ratio at 15. In 1834, Congress had to bump it up to 16. During Covid, the ratio got as high as 120.

We continue to be in an oddly news-free zone for Wall Street. Many of the important economic reports have been delayed due to the government shutdown. On Friday, for example, we didn’t get the big September jobs report.

The CPI report is due out next Wednesday, October 15, and that looks like it will be delayed as well. I don’t expect the government shutdown to last much longer than two or three weeks, but with politics involved, you never know what can happen.

Going by history, investors have little to worry about in a government shutdown. It’s odd how much attention we give these reports, even when they’re endlessly revised. Without the reports, the market appears to be doing just fine.

One agency that’s not impacted by the shutdown is the Federal Reserve. If you’re a fan of speeches by Fed officials, this is your lucky week. Five Fed officials gave public talks about the economy today. Another five will speak tomorrow, and a few more will speak on Thursday including Federal Reserve chairman Jay Powell. We’ll also get the minutes to the Fed’s last meeting.

We’re getting close to the start of Q3 earnings season. The stock market will be closed on Monday for Columbus Day, but on Tuesday we’ll start to get some early earnings reports.

The big banks and financial institutions usually report first. On Tuesday, Goldman Sachs, Wells Fargo, Citigroup, JPMorgan and BlackRock are set to report. Then on Wednesday, Morgan Stanley and Bank of America will report.

I’m expecting a mostly positive earnings season. The big concern for Wall Street isn’t so much the earnings for Q3 but rather what kind of guidance companies are willing to offer. This is especially important during the shutdown. I’m concerned that companies won’t be as optimistic as expected. The tariffs and labor market could be hurting the bottom line more than people expect.

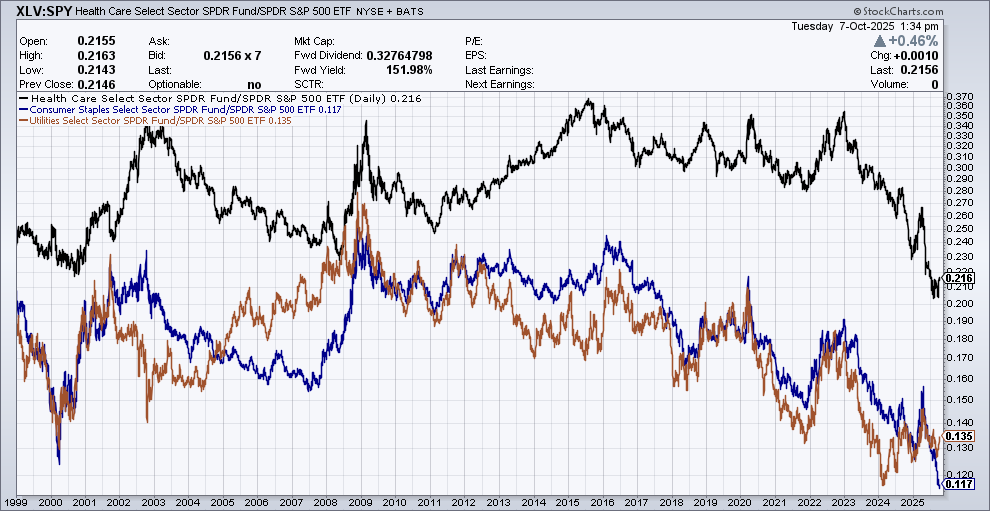

I want to discuss a topic I’ve touched on before, but it’s worth covering again because of its importance. The current market rally has been strongly skewed away from more conservative areas of the market.

In previous issues, I’ve refenced how Low Volatility stocks have trailed the market, but the real driver of this phenomenon is the under-performance of defensive sectors of the market. More specifically, I mean the lagging performance of Healthcare stocks, Consumer Staples and Utilities.

The chart below is a 25-year look at the relative performance of Healthcare (black), Staples (blue) and Utilities (brown):

Note how closely these three sectors follow each other. The correlation isn’t perfect, but it’s apparent even over a long period. I’m struck by how poorly these stocks have performed over the last three years. It seems that owning stability isn’t terribly important to investors right now.

Healthcare stocks rebounded a bit recently. On our Buy List, we had a nice 18% gain from Thermo Fisher (TMO) in just a few days.

Normally, investors favor the reliability of these stocks. The sales, earnings and dividends tend be very stable. That’s nice to see when the economy is falling apart. Notice how well all three lines did around 2007 to 2009.

While the economy isn’t falling apart, there are signs that it may not be doing as well as some people think. For example, if we look at Gross Output, which is a broader measure of the economy, we get a very different picture. During Q2, Gross Output rose at a 1.2% rate while GDP grew at a 3.8% rate.

Why is there such a discrepancy between the two stats? GDP tends to be consumer oriented while Gross Output is more focused on businesses. Dr. Mark Skousen, perhaps the leading advocate for Gross Output, said “the trade war is in fact wreaking economic havoc.”

Skousen’s wrote in the WSJ:

“If you include all transactions in wholesale and retail trade, the adjusted GO is up only 0.3%. More important, I calculate that overall business spending fell sharply, by an annualized 5.6% in real terms. For the first time since the financial crisis of 2008, we are seeing a huge gap between consumer and business spending. While consumption is still robust (up a real 2.6%), business is pulling in its horns, largely due to higher tariffs and the uncertainty of trade war.”

The Trump administration said it’s buying $34.5 million in Trilogy Metals (TMQ), which is a Canadian mining company. That’s a stake worth 10% of the company. Shares of TMQ jumped 211% today. Not bad for one day.

The government has warrants to buy another 7.5%. The goal is to reduce our reliance on China for important minerals.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on October 7th, 2025 at 6:24 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

Source link