Dr Reddy’s Laboratories Ltd: Fundamental Analysis – Dr Vijay Malik

The current section of the “Analysis” series covers Dr Reddy’s Laboratories Ltd (DRL), a leading Indian pharmaceutical company with global operations across North America, Europe, Russia, South America and the rest of the world. DRL has products in generics, active pharmaceutical ingredients (APIs), custom products, biosimilars etc. It focuses on therapeutic areas like the central nervous system, gastrointestinal, oncology, cardiovascular etc.

Please note that to get maximum benefit from this article; an investor should focus on the analysis process instead of looking for good or bad aspects of the company. She should learn the interpretation of diverse types of data and transactions and pay attention to the parts of annual reports etc. used to get the information. This will help her in improving her stock analysis skills.

Dr Reddy’s Laboratories Ltd: Detailed Fundamental Analysis

Dr Reddy’s Laboratories Ltd has investments in various subsidiaries both within India and abroad as well as investments in many joint ventures, associate companies etc. As a result, Dr Reddy’s Laboratories Ltd reports both standalone as well as consolidated financials.

On March 31, 2024, the company had 50 subsidiaries, one associate company, two joint ventures and two trusts/foundations that are included in its consolidated results. (Q4-FY2024 results announcement, page 2).

We believe that while analysing any company, an investor should always look at the company as a whole and focus on financials, which represent the business picture of the entire company including its subsidiaries, joint ventures etc. Consolidated financials of a company present such a picture. Therefore, if a company reports both standalone as well as consolidated financials, then the investor should prefer the analysis of the consolidated financials of the company.

As a result, while analysing the past financial performance of Dr Reddy’s Laboratories Ltd, we have analysed its consolidated financials.

Further recommended reading: Standalone vs Consolidated Financials: A Complete Guide

With this background, let us analyse the financial performance of Dr Reddy’s Laboratories Ltd.

Financial and Business Analysis of Dr Reddy’s Laboratories Ltd:

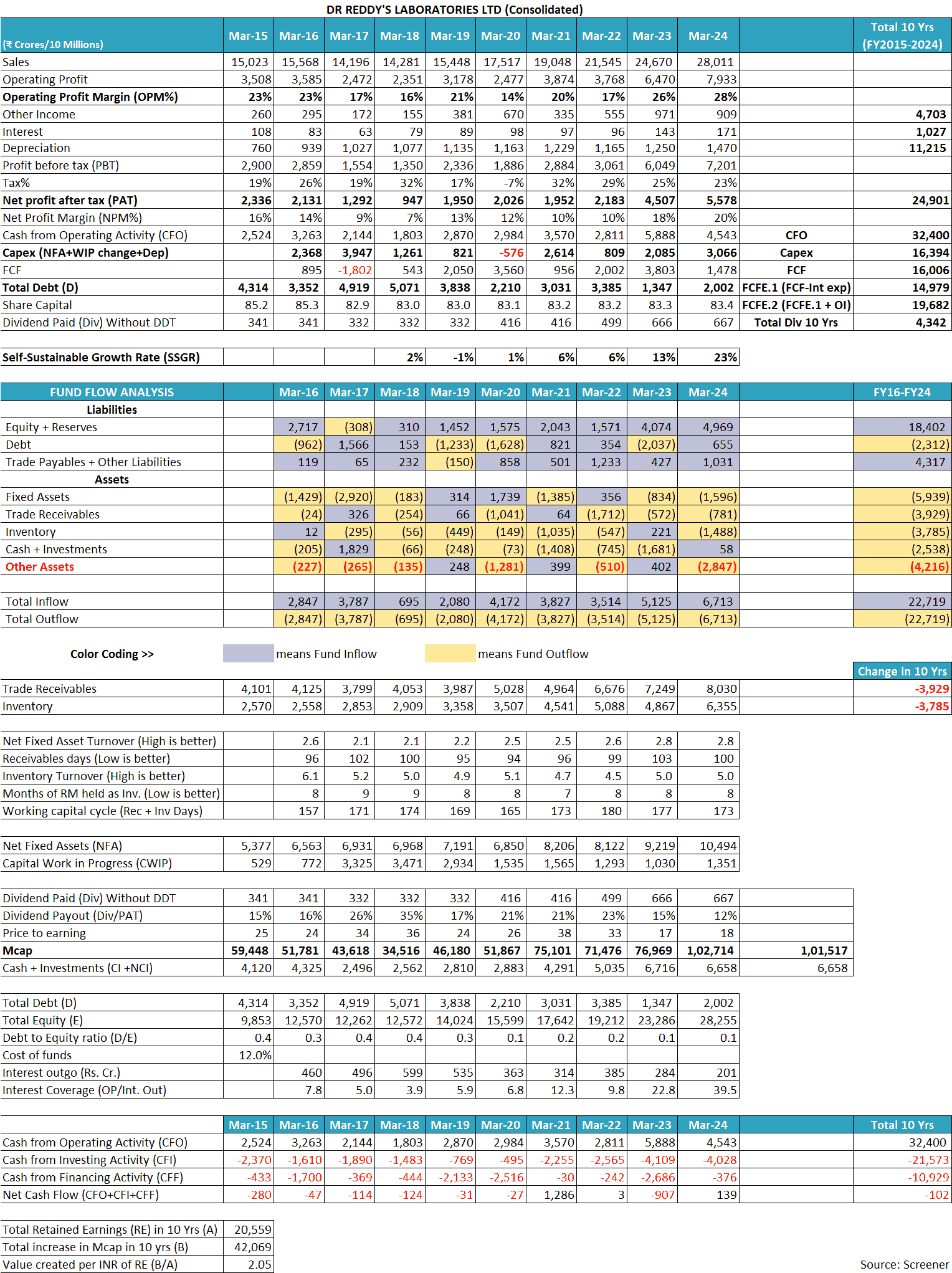

In the last 10 years (FY2015-FY2024), the sales of Dr Reddy’s Laboratories Ltd have increased at 7% year on year, from ₹15,023 cr in FY2015 to ₹28,011 cr in FY2024. During this period, the sales of the company have increased almost consistently, year on year except in FY2017 when sales declined by 9% to ₹14,196 cr from ₹15,568 cr in FY2016.

However, over the years, the operating profit margin (OPM) of Dr Reddy’s Laboratories Ltd has seen large fluctuations between 14% to 28%. The OPM was 23% in FY2015, which continuously declined year-on-year to 16% in FY2018. The OPM then increased to 21% in FY2019; however, declined sharply to 14% in FY2020. OPM recovered to 20% in FY2021, then declined to 17% in FY2022 and thereafter, has recovered to an all-time high of 28% in FY2024.

The net profit margin (NPM) of Dr Reddy’s Laboratories Ltd has shown similar fluctuations from 7% to 20% during the last 10 years (FY2015-FY2024).

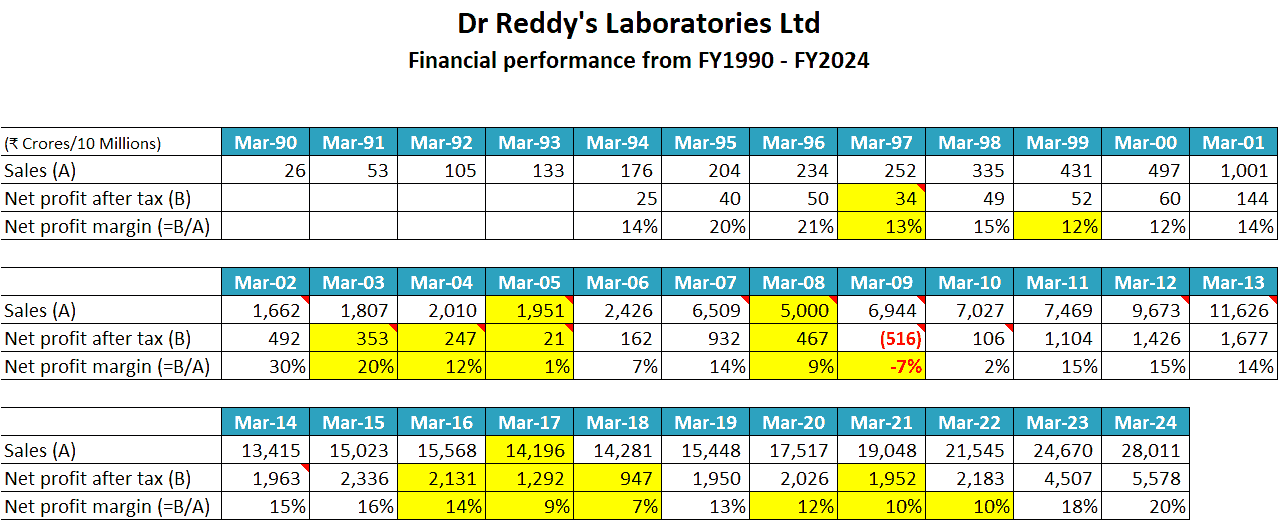

If an investor extends the horizon of her analysis to the maximum duration of data availability for DRL i.e. for the last 34 years from FY1990 to FY2024, then she notices that even though the sales of the company have grown rather consistently except for a few years like FY2005, FY2008 and FY2017; it NPM has always fluctuated.

The below table showing the financial performance of DRL from FY1990 to FY2024 shows that the NPM of the company declined sharply in FY1997, FY1999, FY2003-FY2005, FY2008-FY2009, and FY2016-FY2018. The company even reported deep losses (₹516 cr) in FY2009.

To understand the reasons for the business growth of DRL along with such fluctuating profit margins, an investor needs to read the publicly available documents of the company like its annual reports from FY1999 onwards, conference call transcripts, credit rating reports by ICRA and its corporate announcements submitted to stock exchanges.

In addition, an investor should also read the following article on conducting business analysis of pharmaceutical companies: How to do Business Analysis of Pharmaceutical Companies

The above-mentioned documents show that the following key factors have influenced the business of Dr Reddy’s Laboratories Ltd, which are critical to understand for any investor.

1) Extensive spending on research & development (R&D) leading to exclusive selling opportunities in large markets like USA:

DRL has been spending about 8-10% of its sales on R&D every year. At times, the R&D spend has even exceeded 15% of revenue like in FY2017 when it spent 15.18% on R&D.

FY2017 annual report, page 87:

As a result of substantial R&D spending, DRL has a large portfolio of drugs that it can sell both as API and formulations (ready-to-consume drugs) in highly regulated markets like the USA, Canada, Western Europe etc.

As per ICRA, in FY2024, USA formed 47% of its overall revenues. Moreover, every year, the company is doing more global filings for its products.

Conference call transcript, Q4-FY2024 results, May 2024, page 8:

Erez Israeli: Total number of global filings for the year stands at 43, with 17 ANDAs and 2 NDAs in the U.S.

As a result of its R&D, DRL is able to get approvals for exclusive sale of its generic products for 180 days after the expiry of the patent, which, at times, has led to a substantial jump in its sales and profitability.

For example, in FY2002, when the company increased its sales by 60% from ₹1,001 cr in FY2001 to ₹1,662 cr in FY2002 along with a substantial jump in its NPM from 14% in FY2001 to 30% in FY2002, it was due to its first win of exclusivity period for a drug called Fluoxetine.

FY2002 annual report, page 8:

Your Company’s 58 per cent growth in sales in 2001-02 was very much due to the 180-days exclusivity granted to its fluoxetine 40 mg capsules.

However, after the exclusivity period ends, numerous other generic players enter the market and the price of the drug falls substantially resulting in a sharp decline in sales as well as profitability for manufacturers

Also read: How to do Business Analysis of Pharmaceutical Companies

Therefore, the very next year, in FY2003, the NPM of the company declined to 20% from 30% in FY2002 because the revenue from sales of Fluoxetine fell by almost 50%.

FY2003 annual report, pages 2 and 51:

The reasons for this significant decrease in profit after taxation was primarily due to a decline in profits generated from sale of Flouxetine 40 mg during the year in US market.

Fluoxetine capsules 40mg revenues at Rs. 1,896 million as against Rs. 3,664 million in the previous year, which included one-time marketing exclusivity revenues.

Therefore, the gain exclusivity period in the sale of drugs in one year and then loss of exclusivity in the next year has been one of the reasons for fluctuating profit margins of DRL over the years.

In FY2007, DRL increased its sales to almost 2.5 times to ₹6,509 cr from ₹2,426 cr in FY2006 with a doubling of NPM from 7% in FY2006 to 14% in FY2007, which was due to the launch of 4 drugs with exclusivity periods of 180 days.

FY2012 annual report, page 3:

I remember FY2007 when, in a single year, we launched four exclusive 180-days products: simvastatin, finasteride, ondansetron and fexofenadine.

Even in the later periods, the company has continued to win exclusivity periods for its drug launches in the USA. For example, Olanzapine (FY2012), Finasteride (FY2013), Lenalidomide (FY2023) etc.

2) Out-licensing: selling out its products, marketing rights etc. to other pharmaceutical companies to generate profits:

Right from the 1990s, Dr Reddy’s Laboratories Ltd has out-licensed its drugs to other companies for further clinical development, commercialization/marketing etc. to generate money.

In FY1998, for the first time, the company out-licensed one of the drugs developed by it, Balaglitazone (DRF 2593), to Novo Nordisk (Denmark) for further clinical development and marketing and generated profits.

FY1998 annual report, page 6:

insulin sensitizer molecule, DRF 2593, was licensed to Novo Nordisk of Denmark and is in clinical development. Dr. Reddy’s Laboratories received…payments totalling Rs. 151.50 million…the Company will continue to receive further milestone payments as DRF 2593

It is a different story that Novo Nordisk could not successfully develop this drug further and after 7 years, returned it to DRL in FY2005.

FY2005 annual report, page 157:

…with the discontinuation of further development of DRF 4158 and DRF 2593 by our partners…

Nevertheless, DRL entered into an agreement with another company, Rheoscience for its development and was progressing with its clinical trials even in FY2010.

FY2006 annual report, page 7:

Dr. Reddy’s and Rheoscience A/S have agreed to co-partner the development of balaglitazone (DRF 2593)…which is expected to move to Phase III clinical trials.

FY2010 annual report, page 27:

Dr. Reddy’s and Rheoscience announced the first Phase III clinical trial of Balaglitazone (DRF 2593) with results of significant reduction in HbA1c (glycosylated haemoglobin) and improved safety profile.

It shows the very prolonged nature of drug development. Nevertheless, subsequently, Dr Reddy’s Laboratories Ltd has developed many products and sold/out-licensed them to other companies for substantial gains.

For example, it sold some of its brands to other companies and earned a license fee of about ₹677 cr.

FY2023 annual report, page 338: (the numbers mentioned are in ₹ millions)

this primarily includes the following amounts: a) ₹2,640 from sale of certain non-core dermotology brands in India to Eris Lifesciences Limited. b) ₹1,399 from sale of brands Styptovit-E, Finast, Finast-T and Dynapres to Torrent Pharmaceuticals Limited and c) ₹902 from sale of brands Z&D, Pedicloryl, Pecef and Ezinapi to J B Chemicals and Pharmaceuticals Limited

In FY2020, the company earned ₹748 cr of license fee when it sold its US territory rights for ZEMBRACE® SYMTOUCH® (sumatriptan injection) 3 mg and TOSYMRA® (sumatriptan nasal spray) 10 mg to another company.

FY2020 annual report, page 178: (the numbers mentioned are in ₹ millions)

Definitive agreement with Upsher-Smith Laboratories…Company agreed to sell…its U.S. and select territory rights for ZEMBRACE® SYMTOUCH®…and TOSYMRA®…received US$ 70 millions as upfront…and is entitled to receive up to US$ 40.5 millions…upon the achievement of near term milestones…the Company recognised ₹7,486 (US$ 108.7 millions) as a license fee

In FY2022, it sold all rights of an anti-cancer drug for ₹295 cr and other large contingent milestone-linked payments to another company.

FY2022 annual report, page 268: (the numbers mentioned are in ₹ millions)

definitive agreement with Citius Pharmaceuticals, Inc. (“Citius”) for the sale of all of its rights relating to its anti-cancer agent E7777…Company received ₹ 2,951 (US$40 million)…entitled to additional payments on achievement of milestones of up to US$40 million upon the CTCL (cutaneous Tcell lymphoma) indication regulatory approval, up to US$70 million in milestone payments upon additional indication regulatory approvals

In FY2018 and FY2019, DRL earned more than ₹300 cr by out-licensing its product for development and marketing rights for others to another company.

FY2019 annual report, page 260: (the numbers mentioned are in ₹ millions)

Agreements with Encore Dermatology, Inc…for sale and assignment of US rights relating to three of its dermatology brands…by 31 March 2019…Company recognised ₹1,807 as revenue

year ended 31 March 2018, the Company entered into an agreement with Encore for out-licensing one of its products, DFD-06. The consideration for this arrangement consists of up to ₹1,301 (US$ 20 million)

Therefore, as and when the company finds such opportunities to out-license its drugs/marketing rights, it leads to a significant contribution to revenues.

Also read: How to do Business Analysis of a Company

3) Acquisition of drugs/marketing rights/manufacturing plants/filings of other companies:

Over the years, Dr Reddy’s Laboratories Ltd has entered into multiple such transactions to increase its business size. For example, in FY2020, it bought a business segment from Wockhardh Ltd in India, Nepal, Sri Lanka, Bhutan and Maldives markets along with a manufacturing plant for about ₹1,850 cr.

FY2020 annual report, page 178: (the numbers mentioned are in ₹ millions)

agreement with Wockhardt Limited In February 2020 ..to acquire select divisions of its branded generics business in India and a few other international territories of Nepal, Sri Lanka, Bhutan and Maldives for a consideration of ₹18,500…62 brands…manufacturing plant located in Baddi

In FY2016, it purchased US rights to a new drug from Xenoport at a valuation up to $490 mn (about ₹4,000 cr). Out of this, in FY2017, DRL paid about ₹330 cr.

FY2016 annual report, page 2017:

Company is granted exclusive U.S. rights for the development and commercialization of Xeno Port’s clinical stage oral new chemical entity…Company will pay a USD 47.5 million up-front payment and an additional USD 2.5 million for the transfer of certain clinical trial materials…up to USD 190 million upon…certain regulatory milestones…up to USD 250 million upon…certain commercial milestones, and royalty payments

In 2023, it acquired the US generic portfolio of Mayne Pharma, Australia for about $93 million (about ₹750 cr).

FY2023 annual report, page 399:

On 27 February 2023, the Company entered into an asset purchase agreement with Australia based Mayne, to acquire its U.S. generic prescription product portfolio…The acquisition was consummated on 6 April 2023…Company paid net consideration of US$ 93 million.

In FY2023, it also acquired the drug Cidmus from Novartis for ₹463 cr.

FY2023 annual report, page 323: (the numbers mentioned are in ₹ millions)

The acquisition of the cardiovascular brand and trademark Cidmus® in India from Novartis AG for total consideration of ₹ 4,633 (U.S.$61).

Dr Reddy’s Laboratories Ltd has relied on acquisitions to grow its business for a long time. In fact, in FY2006, it made the largest foreign acquisition by any Indian company until then when it bought Betapharm Group of Germany for EUR 483 million (₹2,750 cr at then rate of about ₹57/EUR).

FY2006 annual report, page 5:

Company completed the acquisition of the betapharm Group, Germany’s fourth largest Generics pharmaceutical company for an all cash deal of €483 million– which, I am told is largest international acquisition made by an Indian company up to date.

However, it is a different story that this debt-funded acquisition turned out to be a big mistake as we discuss later in the article.

In FY2015, the company purchased a nicotine brand, Habitrol, replacement therapy transdermal patches from Novartis for more than ₹500 cr.

FY2015 annual report, page 218: (the numbers mentioned are in ₹ millions)

Company…entered into an asset purchase agreement with Novartis Consumer Health Inc. to acquire the title and rights to its Habitrol® brand…and to market the product in the United States…The total purchase consideration was ₹ 5,097 (USD 80 million).

In FY2017, the company bought 8 ANDAs from Teva/Allergan for $350 million (about ₹2,380 cr at then prevailing rate of ₹68/USD).

FY2017 annual report, page 40:

Acquired eight ANDAs from Teva/ Allergan across various dosage forms for US$ 350 million.

Additionally, over the years, apart from increasing the manufacturing capacity of its plants, DRL has acquired plants and research units of multiple other companies across the world to both increase its manufacturing size as well as to gain entry into those markets and their customers.

Currently, when DRL is generating surplus cash, the management has confirmed that the main use of its surplus cash is to make acquisitions and grow its business size.

Conference call transcript, Q2-FY2024 results, Oct. 2023, page 11:

Erez Israeli:…primarily use it for inorganic activities, which can serve us both in the short-term, like we did with Mayne as well as in the longer-term…Absolutely, this is the main use of the money

Moreover, the company is collaborating with large MNCs to form joint ventures e.g. the newly announced JV with Nestle in 2024 in the nutraceuticals space where both DRL and Nestle will transfer their nutraceutical products to the JV company for sale in the Indian market.

Also read: How to analyse New Companies in Unknown Industries?

4) Economies of scale from a large-sized backwards integrated business model:

DRL’s key business segments, both generics and APIs, are commodity businesses where its product is non-differentiable from its competitors. Therefore, manufacturers end up competing on price.

Conference call transcript, Q2-FY2010 results, Oct. 2009, pages 20, 21:

GV Prasad: This is a generics business we compete on price. And this is always been the case, it will continue to be that…Certain products which are in short supply the price will go up and this is basically a commodity business you have to compete on price and the situation continues.

As a result, DRL frequently faces intense price competition for its drugs, which leads to a decline in profitability. For example, in FY2017, when the company saw a decline in its revenue, profits as well as margins, then it was due to intense price-based competition in the US market.

FY2017 annual report, page 5:

new competitors launching some of our niche and high salience drugs and dramatically pushing prices down; and the significant consolidation of our key US trade channels which gave the buyers greater pricing power than before.

In any commodity business, it becomes essential that manufacturers try to become the lowest-cost producers of goods. Therefore, over the years, DRL has tried to expand its manufacturing capacity to benefit from scale benefits, both, by way of installing new plants as well as acquiring them from other players across the world.

As per ICRA, currently, the company has 33 manufacturing and research units spread across India and different parts of the world.

Credit rating report by ICRA, June 2024, page 4:

DRL has nine API manufacturing facilities, of which six are in India, one in Mexico, one in the US and one in the UK. It also has 13 formulations manufacturing facilities in India, and one each in the US and China. In addition, the company has one biologics facility in India and eight technology development and R&D centres in India and overseas.

Additionally, Dr Reddy’s Laboratories Ltd’s backward-integrated business model where it manufactures APIs, which are used in-house in the production of generic formulations, helps it in further cost reduction. As per ICRA, it produces about 60% of its API requirements in-house.

Credit rating report by ICRA, December 2018, page 2:

well-diversified business model supported by…backward integration in APIs. More of 60% of the global generics segment sales are from its vertically integrated APIs.

Due to low-cost production in its plants, the company follows a strategy where it acquires companies in the developed world and then shifts production of its drugs to India so that it can offer lower prices to its customers there.

Recommended reading: How to do Financial Analysis of a Company

5) Running a pharmaceutical business means compulsory involvement in litigations:

Patents are the biggest competitive advantage to innovative pharmaceutical companies that restrict entry of competing generics players and allow the companies to make significant profits. As a result, such companies face continuous litigations where generics companies file court cases to prove that the patents are invalid.

On the contrary, innovative pharma companies also file court cases against generics players to block launches of their low-priced drugs in the market.

As a result, most of the pharmaceutical companies including Dr Reddy’s Laboratories Ltd are continuously involved in legal battles.

The outcome of these litigations is never certain and therefore, they might lead to large monetary gains when successful or large monetary payouts when unsuccessful.

Over the years, Dr Reddy’s Laboratories Ltd has paid large amounts of money to other pharmaceutical companies and also got significant sums when the litigation/settlement was in its favour.

For example, in FY2009, the company had to pay about ₹90 cr when a German court ruled in favour of the patent owner, Eli Lilly for the drug Olanzapine.

FY2009 annual report, page 164: (the numbers mentioned are in ₹ millions)

Federal Court…maintain the olanzapine patent in favor of Eli Lilly, the innovator…Eli Lilly, as part of the litigation has claimed damages from the Company…recorded a liability towards the damage claim amounting to Rs. 916 under the head operating and other expenses

In FY2016, DRL had to pay ₹43 cr to Novartis for violating its patents and to seek permission for future sales of its products.

FY2016 annual report, page 192: (the numbers mentioned are in ₹ millions)

Company made a one-time payment to Novartis in exchange for a license to all relevant patents…Pursuant to this agreement, the Company paid ₹ 430 (USD 6.5 million) to Novartis as a settlement amount for past and future sales of the products

However, it’s not that always DRL had to pay under these settlements. In FY2023, the company won a settlement and Indivior agreed to pay ₹563 cr to Dr Reddy’s Laboratories Ltd to settle the dispute.

FY2023 annual report, page 83

recognition of an income of ₹5,638 million from a settlement agreement with Indivior Inc, Indivior UK Limited, and Aquestive Therapeutics Inc, resolving all claims between the parties relating to the generic buprenorphine and naloxone sublingual film

Similarly, in FY2020, DRL received ₹345 cr from Celgene to settle the dispute.

FY2020 annual report, page 147: (the numbers mentioned are in ₹ millions)

amount of ₹ 3,457 (US$50 millions) received from Celgene pursuant to a settlement agreement entered into in April 2019. The agreement effectively settles any claim the Company or its affiliates may have had for…generic version of REVLIMID ® brand capsules (Lenalidomide)

Recommended reading: How to study Annual Report of a Company

6) Very high regulatory risk in the business of Dr Reddy’s Laboratories Ltd:

The pharmaceutical industry has a direct impact on the health and financial costs of the general population; therefore, almost all govts. keep tight control on the quality and prices of drugs.

6.1) Strict inspection of manufacturing plants:

Every country has a drug regulator that inspects the plants where companies manufacture drugs for selling in their country. From India, so many companies sell drugs in the USA that now, USFDA has a local office in India from where it conducts frequent audits of companies’ manufacturing plants.

Such inspections are usually very stringent and at times, even plants of the best of the companies fail the inspections.

Dr Reddy’s Laboratories Ltd failed USFDA inspection multiple times in the past where at times, it took some years for it to clear all the observations and then resume selling to the US from these plants.

FY2016 annual report, page 3:

USFDA inspected three of our plants…In November 2015, they sent a warning letter to your Company.., this event and the remedial steps that followed have delayed launches of key products and certain APIs which, in turn, significantly lowered incremental revenues

This had a significant impact on the company’s business as its revenue from the North America Generics division declined by 16% in the next year, FY2017.

The company could not clear two of these plants even in FY2018 and its plans to launch more drugs in the US market got delayed.

FY2018 annual report, page 2:

However for the other two plants, there is no change in status vis-a-vis the USFDA. Consequently, launches of key molecules, injectables, as well as certain APIs from these sites have been delayed

It is not only the USFDA, which is strict in its assessment. In FY2018, one of the plants of DRL could not clear the inspection from the German drug regulator. It took the company four months to clear all the observations of the regulator and resume supplies from the plant to Germany, which impacted the business.

FY2018 annual report, page 2:

Germany audited your company’s formulation unit 2 (FTO-2) at Bachupally, Hyderabad (Telangana). This resulted in the good manufacturing practices (GMP) compliance certificate not being renewed in August, 2017…After a follow-up audit, the GMP non-compliance status was withdrawn in January, 2018. However, stoppage in sale to Europe for four months led to lesser revenue

In the case of the German audit, DRL could clear the shortcomings in a 4-month duration. However, in the case of USFDA observations for its API plant at Srikakulam, issued in Nov. 2015, it could not clear them in 4 years (Nov. 2019).

Credit rating report by ICRA, Nov. 2019:

The company is also yet to resolve the warning letter issued to its API plant at Srikakulam in November 2015

Even in 2024, the company has received multiple observations from the USFDA after the inspection of its plants.

6.2) Pricing controls by govt on pharmaceutical drugs:

Almost every country controls the price of drugs in one way or another to lower the health costs for its people. At times, govt. actions in this direction lead to a very drastic impact on companies.

For example, Dr Reddy’s Laboratories Ltd faced a shock in the German market after it bought Betapharm Group for EUR 483 million (₹2,750 cr at then rate of about ₹57/EUR) in FY2006.

Until then, Germany used to be a branded generics market and Betapharm owned many well-known brands of drugs. DRL had expected to earn higher revenue by increasing sales of these brands and to earn more profits by manufacturing them at its low-cost plants in India.

However, the German govt. changed its pharmaceutical market to tender-based where insurance companies (Sick Funds/AOK) started allocating tenders of drug supplies to lowest bidders, which in turn, eroded the profitability and competitive advantages of Betapharm group.

As a result, over the next few years, Dr Reddy’s Laboratories Ltd lost all of its investment of ₹2,750 cr done in Betapharm by way of write-offs and it had to put in more money to keep the company running.

- In FY2007, DRL wrote off ₹155 cr of intangible assets.

- In FY2008, it wrote off ₹236 cr of intangibles.

- In FY2009, DRL wrote off a massive ₹1,402 cr in goodwill and intangible assets impairment. This was the reason for the loss of ₹516 cr reported by the company in FY2009.

FY2009 annual report, page 3:

German generics market is rapidly transiting to a lowest-price tender model…betapharm intangibles for possible impairment…write-down of intangible assets amounting to Rs. 317 crore. In addition, the betapharm goodwill on the balance sheet was also tested for impairment…charge of Rs. 1,086 crore. In the aggregate…impairment charge was around Rs. 1,402 crore

- In FY2010, DRL wrote off an additional ₹847 cr of goodwill and intangibles. (FY2010 annual report, page 3). Additionally, DRL incurred ₹91 cr as charges for employee termination at Betapharm (FY2010 annual report, page 26)

- In FY2012, the company recognized a further impairment of ₹210 cr (FY2012 annual report, page 119).

Thereafter, in FY2014, after 8 years of investment in Betapharm group, the company got rid of it by disposing of shares of Lacock Holding Ltd, the SPV using which it had invested in Betapharm. On such disposal, it recognized a further loss of ₹16 cr.

FY2014 annual report, page 123: (the numbers mentioned are in ₹ millions)

Company disposed its investment in Lacock Holdings Limited…to its wholly owned subsidiary Dr. Reddy’s Laboratories SA, Switzerland. The aggregate loss on such disposal of investment recorded under “Other expenses” is ₹166.

So, overall, from FY2006-FY2014, Dr Reddy’s Laboratories Ltd lost its entire initial investment of about ₹2,700 cr and about ₹1,500 cr of incremental investment done over these years to sustain Betapharm operations.

- FY2007, it gave a loan of ₹101 cr to Lacock Holdings Ltd, which is the SPV using which DRL had acquired Betapharm group (FY2007 annual report, page 107).

- FY2008, it invested a further ₹760 cr in Lacock Holdings Ltd (FY2008 annual report, page 104).

- In FY2009, it invested an additional about ₹470 cr (₹133 cr in equity and ₹335 cr as debt) in Lacock (FY2009 annual report, pages 107 and 140).

- In FY2010, it invested ₹252 cr (FY2010 annual report, page 101)

This acquisition was primarily debt funded as DRL had taken about EUR 196 mn debt for it. Therefore, the interest paid by the company on this debt is an additional loss to shareholders.

Conference call transcript, Q3-FY2009 results, page 22:

Umang Vohra: Yeah so we have 196 million Euros of debts which is the debt we took on account of our acquisition at Betapharm.

So, overall, during FY2006-2014, shareholders of Dr Reddy’s Laboratories Ltd lost more than ₹4,000 cr due to a regulatory change in Germany when the market changed from branded generics to tender-based and the largest international acquisition by any Indian company until then proved unsuccessful.

Betapharm was not the only acquisition on which DRL lost significant money

It is not only Germany that has resorted to high control of the pharmaceutical industry. In the past, DRL was impacted when Russia took steps to control drug prices by forcing doctors to prescribe trade/generic-generics (i.e. without the brand name of the drug), banning meetings of doctors with representatives of pharmaceutical companies and offering incentives to local manufacturing of drugs for import substitution (FY2012 annual report, page 42, FY2013 annual report, page 36).

Chinese govt. manages drug prices via an Essential Drug List (EDL) and a National Reimbursement Drug List (NRDL). Pharmaceutical companies have to offer substantial discounts on drugs on these lists. (FY2019 annual report, page 39)

In India, govt. control prices of the National List of Essential Medicines (NLEM) via the Drug Prices Control Order (DPCO) issued by the National Pharmaceutical Pricing Authority (NPPA). Over the years, the company’s business has suffered whenever DPCO put price caps on its key drugs.

For example, in FY2017, when the revenue of DRL declined by about 10% from FY2016, the decrease in prices of its key drugs due to the price cap under DPCO was one of the key reasons.

FY2017 annual report, pages 2-3:

revenue growth was constrained by the notified decline of prices of a large number of drugs, including your company’s leading brands, in the National List of Essential Medicines (NLEM) issued by the National Pharmaceutical Pricing Authority (NPPA).

Recommended reading: How to do Financial Analysis of a Company

7) Geopolitical and foreign exchange risk faced by Dr Reddy’s Laboratories Ltd:

The business operations of DRL are spread across numerous countries in the world. As a result, it is exposed to political and socioeconomic changes in its target markets.

In the past, the company lost substantial money in Venezuela when, after the death of its president, Hugo Chavez, the country faced a lot of social and economic instability.

As the crisis in Venezuela deepened, the country kept on devaluing its currency and increased controls on the outflow of money from the country.

Signs of troubles in Venezuela’s economic position started to appear in FY2011 when it devalued the preferential rate of forex conversion from 2.6 Venezuelan Bolivars (“VEB”) per US$ to 4.3 (FY2011 annual report, page 148).

However, Dr Reddy’s Laboratories Ltd continued to increase its focus on Venezuela and grow its business and investments there.

FY2015 annual report, page 48:

Venezuela has been the growth driver. We have stayed committed to the country despite its economic difficulties…Consequently, we have enjoyed a revenue CAGR of 52% between FY2011 and FY2015. In FY2015, sales in Venezuela increased by 187% to become Dr. Reddy’s fourth largest market.

However, soon the reality caught up with the company and in the next year, FY2016, it suffered a write-off of ₹500 cr on its investments in Venezuela when the country refused it outflow of money from the country.

FY2016 annual report, page 3:

continuing economic crisis in Venezuela led to a clampdown on foreign exchange outflows due to which your Company received no approvals from the Venezuelan government to repatriate amounts beyond US$ 4 million. The remaining Venezuelan net monetary assets were translated using the DICOM rate resulting in a write-down of ₹ 5.09 billion.

And in the next year, FY2017, it chose to restrict its business in Venezuela.

FY2017 annual report, page 3:

we have consciously chosen to limit our business to supplying consignments only against remittance of funds from Venezuela. Since such repatriations are minuscule, so too is the size of our business.

Moreover, in FY2017, it wrote off a further ₹84 cr of its investments in Venezuela (FY2017 annual report, page 143).

Apart from Venezuela, Dr Reddy’s Laboratories Ltd has faced a significant impact due to the devaluation of the Russian currency (Ruble) due to issues there.

Revenues from Russia declined by 29% due to economic problems and the devaluation of the Ruble in FY2016. (FY2016 annual report, page 3).

In FY2015, the revenue from Russia had declined 11% due to a sharp depreciation of Ruble (FY2015 annual report, page 41).

In FY2021, the revenue from Russia declined by 6% due to the depreciation of Ruble (FY2021 annual report, page 43).

Over the years, the company has experienced significant losses on account of adverse foreign exchange movements. For example, it had forex losses of ₹138 cr in FY2015, ₹78 cr in FY2012, ₹63 cr in FY2009 and ₹53 cr in FY2005.

Over the years, the tax payout ratio of Dr Reddy’s Laboratories Ltd has been below the standard corporate tax rate in India. Key reasons for the same are significant earnings from foreign countries that have different tax rates than India, tax incentives available to the company on its R&D expenses, manufacturing in states that offer incentives etc.

Until FY2023, the company had a lot of tax incentives, minimum alternate tax (MAT) credits etc. Therefore, it was continuing with the old corporate tax regime. However, from FY2024, the company has opted for the new corporate tax regime of lower taxes. (Conference call transcript, Q4-FY2024 results, May 2024, page 5).

Operating Efficiency Analysis of Dr Reddy’s Laboratories Ltd:

a) Net fixed asset turnover (NFAT) of Dr Reddy’s Laboratories Ltd:

Over the years, the NFAT of the company had stayed between 2.1 and 2.8. A rangebound asset turnover indicates that the company has maintained its asset utilization efficiency.

Going ahead, an investor should monitor the NFAT of Dr Reddy’s Laboratories Ltd to understand whether it continues to efficiently utilize its assets.

Further advised reading: Asset Turnover Ratio: A Complete Guide for Investors

b) Inventory turnover ratio (ITR) of Dr Reddy’s Laboratories Ltd:

Over the years, the ITR of Dr Reddy’s Laboratories Ltd has declined from 6.1 in FY2016 to 4.5 in FY2022. In FY2024, the ITR has recovered to 5.0. However, the inventory management efficiency of the company has gone down over the years.

The company’s operations are working capital intensive as it has to maintain a large amount of inventory at its plants, under transportation on ships in the sea trade, and warehouses near customers so that it can supply goods on short notice to the customers.

Moreover, for cases like 180-day exclusivity sales, the demand for the drugs shoots up on launch and falls down drastically after the end of exclusivity as other competitors enter the market. In such cases, the company faces significant inventory refunds/chargebacks (Conference call transcript, Q3-FY2007 results, January 2007, pages 18-19).

Over the years, Dr Reddy’s Laboratories Ltd has faced significant inventory write-downs and refunds. For example, in FY2023, it faced an inventory write-down of ₹486 cr and had refund liabilities of about ₹460 cr. The same figures for FY2022 were ₹458 cr and ₹440 cr respectively. (FY2023 annual report, pages 297 and 3440).

Therefore, having a long supply chain from India and spreading across the world costs the company about ₹900cr – ₹1,000 cr every year in inventory write-downs and refunds.

However, maintaining high inventory across the system is compulsory for Dr Reddy’s Laboratories Ltd because any delay in supplying drugs to the customer will lead the customers to source them from any of its competitors. The company faced a loss of business due to a delay in supply in FY2010 when it voluntarily recalled some of its products and could not meet demand on time. During this period, customers started buying from its competitors, which hurt its business.

Conference call transcript, Q3-FY2010 results, January 2010, page 4:

Umang Vohra: In September this fiscal, one lot each of four of our products were voluntarily recalled by us. This caused a temporary slow-down of production resulting in diversification of supply sources by few of our customers. As a result, our base business revenues have been flat for this quarter

Going ahead, an investor should monitor the inventory position of Dr Reddy’s Laboratories Ltd to assess whether it is able to manage its inventory efficiently.

Further advised reading: Inventory Turnover Ratio: A Complete Guide

c) Analysis of receivables days of Dr Reddy’s Laboratories Ltd:

Over the years, the receivables days of Dr Reddy’s Laboratories Ltd have ranged from 94 days to 103 days.

The year-on-year change in receivables days also depends on the mix of export and domestic sales in the overall revenue. The company has to give a higher credit period (about 180 days) in export sales in comparison to a lower credit period (about 90 days) in domestic sales.

FY1998 annual report, page 39:

The credit period extended on export sales is 180 days and 90 days for domestic sales.

Going ahead, an investor should watch the trend of receivables days of Dr Reddy’s Laboratories Ltd to assess whether it continues to collect its receivables on time.

Further recommended reading: Receivable Days: A Complete Guide

When an investor compares the cumulative net profit after tax (cPAT) and cumulative cash flow from operations (cCFO) of Dr Reddy’s Laboratories Ltd for FY2015-FY2024, then she notices that over the years (FY2015-FY2024), the company has converted its profit into cash flow from operations.

Over FY2015-24, Dr Reddy’s Laboratories Ltd reported a total net profit after tax (cPAT) of ₹24,901 cr. During the same period, it reported cumulative cash flow from operations (cCFO) of ₹32,400 cr.

It is advised that investors should read the article on CFO calculation, which would help them understand the situations in which companies tend to have the CFO lower than their PAT. In addition, the investors would also understand the situations when the companies would have their CFO higher than PAT.

Further recommended reading: Understanding Cash Flow from Operations (CFO)

Learning from the article on CFO will show an investor that the following factors led to a higher cCFO compared to cPAT:

- Depreciation expense of ₹11,215 cr (a non-cash expense) over FY2015-FY2024, which is deducted while calculating PAT but is added back while calculating CFO.

- Interest expense of ₹1,027 cr (a non-operating expense) over FY2015-FY2024, which is deducted while calculating PAT but is added back while calculating CFO.

Going ahead, an investor should keep a close watch on the working capital position of Dr Reddy’s Laboratories Ltd.

The Margin of Safety in the Business of Dr Reddy’s Laboratories Ltd:

a) Self-Sustainable Growth Rate (SSGR):

Read: Self Sustainable Growth Rate: a measure of Inherent Growth Potential of a Company

Upon reading the SSGR article, an investor would appreciate that if a company is growing at a rate equal to or less than the SSGR and it can convert its profits into cash flow from operations, then it would be able to fund its growth from its internal resources without the need of external sources of funds.

Conversely, if any company attempts to grow its sales at a rate higher than its SSGR, then its internal resources would not be sufficient to fund its growth aspirations. As a result, the company would have to rely on additional sources of funds like debt or equity dilution to meet the cash requirements to generate its target growth.

An investor may calculate the SSGR using the following formula:

SSGR = NFAT * NPM * (1-DPR) – Dep

Where,

- SSGR = Self Sustainable Growth Rate in %

- Dep = Depreciation rate as a % of net fixed assets

- NFAT = Net fixed asset turnover (Sales/average net fixed assets over the year)

- NPM = Net profit margin as % of sales

- DPR = Dividend paid as % of net profit after tax

(For systematic algebraic calculation of SSGR formula: Click Here)

An investor would notice that over the years, Dr Reddy’s Laboratories Ltd had reported an SSGR of 13-23% whereas, over the last 10 years (FY2014-FY2022), it has grown its sales at a rate of 7% year on year. As a result, the company has grown its sales within the levels that its business profits can sustain.

Therefore, in the last 10 years (FY2015-FY2024), Dr Reddy’s Laboratories Ltd has kept its debt under check. DRL had a debt of ₹4,314 cr in FY2015, which declined to ₹2,002 cr in FY2024.

The investor gets the same conclusion when she analyses the free cash flow position of Dr Reddy’s Laboratories Ltd.

b) Free Cash Flow (FCF) Analysis of Dr Reddy’s Laboratories Ltd:

While looking at the cash flow performance of Dr Reddy’s Laboratories Ltd, an investor notices that during FY2015-FY2024, it generated cash flow from operations of ₹32,400 cr. During the same period, it did a capital expenditure of about ₹16,394 cr.

Therefore, during this period (FY2015-FY2024), Dr Reddy’s Laboratories Ltd had a free cash flow (FCF) of ₹16,006 cr (=32,400 – 16,394).

In addition, during this period, the company had a non-operating income of ₹4,703 cr and an interest expense of ₹1,027 cr. As a result, the company had a total free cash flow of ₹19,682 cr (= 16,006 + 4,703 – 1,027). Please note that the capitalized interest is already factored in as a part of the capex deducted earlier.

Dr Reddy’s Laboratories Ltd has used its surplus cash to reduce its debt, pay dividends to shareholders (₹4,342 cr excluding dividend distribution tax), buy back of shares in FY2017 (₹1,569 cr) and increase its cash & investments. On March 31, 2024, the company has cash & investments of about ₹6,658 cr.

An investor would see that in the last 10 years (FY2015-2024), DRL has been a highly cash surplus company. However, in the previous decades, it had faced significant cash shortfalls to fund its R&D expenses and acquisitions.

As a result, previously, it had to raise equity by diluting its equity capital on a frequent basis.

Initially, the company came out with a GDR (Global Depository Receipts) issue of $48 million in FY1995 (FY2000 annual report, page 11) i.e. about ₹150 cr assuming then prevailing rate of about ₹32/$.

Thereafter, in FY2002, it raised $132.78 million by issuing American Depository Shares (ADS) (FY2001 annual report, page 60) i.e. about ₹625 cr assuming then prevailing rate of ₹47/$.

The company used these funds to repay its high-cost debt. However, in FY2006, it did the acquisition of Betapharm, Germany, which increased its debt sharply.

Therefore, in FY2007, it again diluted its equity and raised money by ADR (American Depository Receipts) issue of ₹1,000 cr.

Other than these equity issuances, the company also found novel ways of raising funds where it got investments from funds like ICICI Venture, Citi etc. for its R&D activities. In FY2005, ICICI Venture agreed to fund $56 million (about ₹250 cr assuming then prevailing rate of ₹44/$) (FY2005 annual report, page 3).

Thereafter, in FY2006, it entered into another agreement with ICICI Venture and Citigroup Venture where they agreed to fund $45 million (about ₹200 cr assuming then prevailing rate of ₹45/$) for its R&D activities (FY2006 annual report, page 5).

Going ahead, an investor should keep a close watch on the free cash flow generation by Dr Reddy’s Laboratories Ltd to understand whether the company continues to generate surplus cash from its business and how it utilizes the same.

Further recommended reading: Free Cash Flow: A Complete Guide to Understanding FCF

Self-Sustainable Growth Rate (SSGR) and free cash flow (FCF) are the main pillars of assessing the margin of safety in the business model of any company.

Further advised reading: 3 Simple Ways to Assess “Margin of Safety”: The Cornerstone of Stock Investing

Additional aspects of Dr Reddy’s Laboratories Ltd:

On analysing Dr Reddy’s Laboratories Ltd and after reading annual reports, credit rating reports and other public documents, an investor comes across certain other aspects of the company, which are important for any investor to know while making an investment decision.

1) Management Succession of Dr Reddy’s Laboratories Ltd:

Dr Reddy’s Laboratories Ltd was established by Dr. K Anji Reddy who left this world in 2013. Currently, his son, Mr K Satish Reddy (aged 56 years) is the chairman and his son-in-law, Mr G V Prasad (aged 63 years) is the Co-Chairman & MD of the company.

Due to the presence of the next generation, there was a seamless transition of leadership from the founder promoter to the next generation.

The presence of a well-thought-out management succession plan is essential in the case of promoter-run businesses as it provides for a smooth transition of leadership over the generations and provides continuity in the business operations of any company.

Further advised reading: How to do Management Analysis of Companies?

2) Related party transactions of Dr Reddy’s Laboratories Ltd with its promoters:

Over the years, DRL has entered into a few transactions with its promoter group entities, which had the potential to transfer economic benefits from public shareholders to promoters.

For example, in FY2001, DRL merged one of its group companies, Cheminor Drugs Ltd (CDL) with itself. CDL was primarily run by Mr G V Prasad, the son-in-law of Dr K Anji Reddy. As per the then media articles, the merger share-swap ratio favoured the shareholders of CDL over the shareholders of DRL. (Source: Dr Reddy’s Cheminor merger: A pharma wedding finalized)

Dr. Reddy’s Holdings (DRH), currently holds 25.40% in DRL and 35.34 % in Cheminor…Dr. Anji Reddy and his immediate family members hold 1.76% in DRL and 13.42% in CDL…The merger ratio too seems to be slightly weighted in favour of the Cheminor

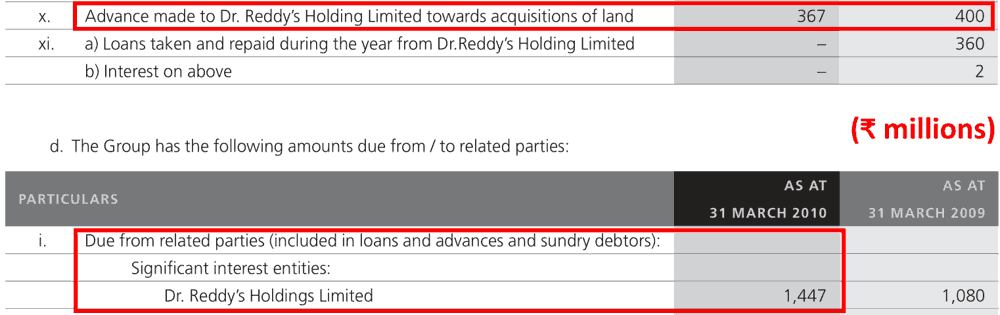

On other occasions, DRL purchased land from its promoter group entities.

For example, in FY2004, DRL purchased a company named Dr Reddys Bio-Sciences Ltd. (DRBSL) for ₹27 cr, which had a land parcel with some dispute.

FY2004 annual report, page 121:

On 9 July 2003, the group acquired 100% equity stake in DRBSL for a consideration of Rs. 277,463 thousands. A part of consideration amounting to Rs. 26,075 thousands was withheld on account of boundary dispute on a portion of land.

During FY2008-FY2010, when DRL was expanding its manufacturing capacity by installing more manufacturing plants, then it purchased land from its promoter group company, Dr Reddy’s Holdings Limited for ₹144 cr.

FY2010 annual report, page 166:

In FY2014, the company purchased assets for ₹126 cr from another related party company, Ecologic Chemicals Limited.

FY2014 annual report, page 152: (the numbers mentioned are in ₹ millions)

Company entered into an asset purchase agreement with Ecologic Chemicals Limited (“Ecologic”), where in two directors of the Company have equity interests. The Company has paid ₹ 1,264 excluding taxes and duties for purchase of fixed and current assets.

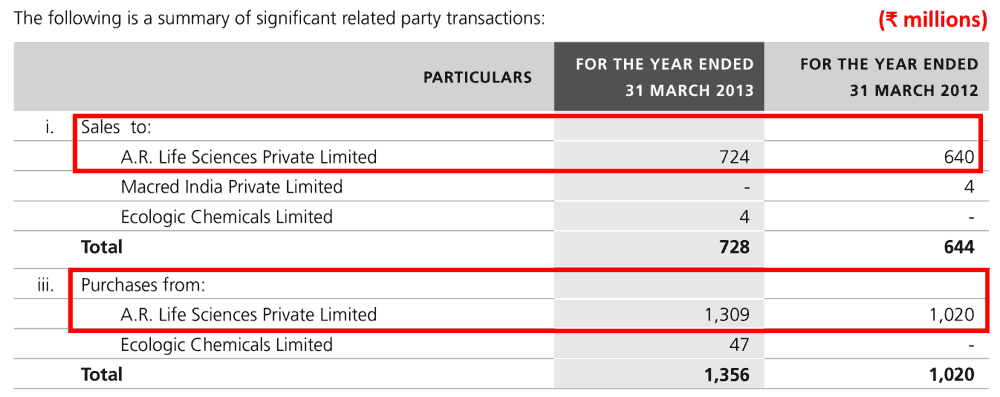

Other than these large asset purchase transactions, on a regular basis, Dr Reddy’s Laboratories Ltd enters into sales and purchase transactions for goods and services with related parties.

For example, it had sales and purchase transactions worth hundreds of crores of rupees with A R Life Sciences Pvt. Ltd.

FY2013 annual report, page 172:

An investor would appreciate that all these related party transactions between the company and promoter group entities have the potential of shifting economic benefits from public shareholders to promoters if the listed company buys goods and services from promoters at a price higher than fair market price or sells them to promoters at a price lower than fair market price.

Also read: How Promoters benefit from Related Party Transactions

3) Numerous write-offs undertaken by Dr Reddy’s Laboratories Ltd on its acquisitions:

As discussed above, DRL lost/had to write off more than ₹4,000 cr on its acquisition of Betapharm in Germany; however, that was not the only time when it lost/wrote off substantial money on an acquisition

In FY2020, the company wrote off/impaired ₹1,675 cr, which were primarily the investments done to acquire drugs from Teva Pharmaceutical, Israel. It wrote off ₹1,113 cr out of ₹1,426 cr spent to acquire the generic version of the drug “Nuvaring” and ₹355 cr from the acquisition cost of Tobramycin, Ramelteon, and Imiquimod, all from Teva Pharmaceutical.

Credit rating report by ICRA, June 2020, page 1:

net profits were adversely impacted in FY2020 due to the Rs. 1,676.7 crore of impairment…Of this, Rs 1,113.7 crore pertained to gNuvaring– the ANDA of which was acquired from TEVA for Rs. 14.26 billion in FY2016. DRL had also taken an impairment charge of Rs 355.1 crore on three product related intangibles acquired from TEVA in August 2016 (viz., Ramelteon, Tobramycin and Imiquimod).

Whatever remaining value was remaining out of gNuvaring acquisition from Teva, was impaired in the next year, FY2021, when DRL took another hit of write-off/impairment of ₹854 cr.

FY2021 annual report, page 48:

In FY2021, there has been an impairment charge of ₹ 8,542 million which pertains to charges of…₹ 3,180 million for…generic equivalent to Nuvaring…₹ 1,587 million for the product Saxagliptin/Metformin…₹ 3,291 million for the product Xeglyze…₹ 484 million on other products

It looks like the sellers of Betapharm group as well as the above drugs exited at a perfect time by selling them to Dr Reddy’s Laboratories Ltd.

Nevertheless, the series of large impairments continued in FY2022 when DRL took another hit of ₹930 cr.

Credit rating report by ICRA, July 2022, page 1:

In FY2022, DRL recognised an impairment of Rs. 930.4 crore towards product related intangibles and Shreveport subsidiary related assets, which moderated the net margin to an extent.

In the next year, FY2023, another acquisition proved wrong for Dr Reddy’s Laboratories Ltd. In the previous year, FY2022, it had acquired Nimbus Health GmbH in Germany, which dealt in medical cannabis. The company had paid an upfront amount of ₹33 cr and there were further performance and milestone-linked payments to be done in the future. (FY2022 annual report, page 323)

However, in the very next year, in FY2023, DRL had to write off its investment in Nimbus Health GmbH. In FY2023, the company wrote off a total of about ₹70 cr out of which ₹27 cr was on account of Nimbus Health GmBH i.e. more than 80% of investment in Nimbus was written off within a year. (FY2023 annual report, pages 83, 322).

Therefore, Dr Reddy’s Laboratories Ltd very frequently has lost substantial sums of money on its acquisitions. However, apart from these, over the years, DRL has undertaken many other ventures where it lost capital.

At one time, it even manufactured automotive halogen lamps; however, it led to a loss of capital for shareholders.

In FY1997, DRL started manufacturing automotive halogen lamps via its wholly-owned subsidiary, Compact Electric Limited (CEL). (FY1997 annual report, page 32).

However, right from the start, CEL faced challenges of low demand, high competition from low-priced lamps, and cheaper imports from China, Taiwan and Korea (FY1998 annual report, page 60).

CEL reported losses year after year and DRL had to impair its investment, write off loans given to CEL (₹2.6 cr) and finally sell the company at a loss in FY2004 (51% stake) and FY2005 (remaining 49% stake) resulting in loss of about ₹6.5 cr (FY2005 annual report, page 94)

Similarly, in FY1998, DRL entered into the diagnostics business and started production of “sophisticated diagnostic kits” and “ELISA-based products” (FY1997 annual report, page 16). In FY1999, it launched the pregnancy detection kit “Velocit”.

However, within a few years, in FY2003, the company decided to close down the diagnostic division as it was not fitting in its overall strategy and it wrote off its investment of about ₹5 cr (FY2003 annual report, pages 45, 50, 162). Finally, DRL sold off the SPV created for its diagnostics business Pathnet (India) Private Limited in FY2006 (FY2006 annual report, page 145).

Recently, in FY2024, DRL started an e-commerce venture, “Celevida Wellness”. However, soon enough, it closed down this direct-to-consumer website (Conference call transcript, Q4-FY2024 results, May 2024, page 7).

In FY2010, it wrote off ₹32 cr invested in its subsidiary in Spain, Reddy Pharma Iberia (FY2010 annual report, page 103). In FY2014, the company wrote off further investment of ₹24.5 cr in this subsidiary (FY2014 annual report, page 151).

In FY2011, the company wrote off about ₹50 cr of its investment in its Brazilian subsidiary, Dr Reddy’s Farmaceutica Do Brasil Ltda (FY2011 annual report, page 107). In FY2015, DRL fully wrote off its investments of ₹102 cr in Brazilian (₹46 cr) and Spanish (₹56 cr) subsidiaries (FY2015 annual report, page 129). However, the company reentered Brazil in FY2018.

APR LLC: the company started investing money in APR LLC, which was developing an API, in FY2004 and over the years, invested about ₹40 cr (₹2 cr Class B equity and 38 cr debt) (FY2011 annual report, page 175). Class A equity was owned by two individuals whose identity was not disclosed in the annual reports by DRL.

By FY2011, the entire investment of DRL in APR LLC was written down to zero due to losses incurred by APR. However, still, in FY2012, the company paid a further ₹14 cr to take over entire assets, rights etc. (FY2012 annual report, page 184). Effectively DRL gave an exit to the two individuals (Class A shareholders) by paying ₹14 cr when it had already lost its entire investment of ₹40 cr until then.

In FY2016, DRL invested ₹66 cr in a company DRL Impex Limited and wrote it off fully, within the same year. (FY2016 annual report, page 126).

In FY2019, the company invested ₹36 cr in Reddy Antilles N.V., Netherlands and wrote it off in the same year. (FY2019 annual report, page 137). DRL liquidated this subsidiary in FY2020 by writing off everything (FY2020 annual report, page 138).

Also read: Steps to Assess Management Quality before Buying Stocks

4) Loss of money in equity shares:

Dr Reddy’s Laboratories Ltd lost money in equity instruments, especially twice.

In FY2020, it lost ₹240 cr in the shares of CURIS, INC as instead of cash, it accepted shares of Curis for its collaboration agreement for R&D and commercialization of oncology drugs (FY2020 annual report, page 276).

In FY2015, when the company entered into a collaboration agreement with Curis, then it accepted shares of Curis, which gave it a 16.6% stake in the company. At that time, the market value of these stocks was ₹145 cr, which were listed on NASDAQ (FY2015 annual report, page 219).

Thereafter, as per the agreement, in FY2017, when DRL was to receive a payment of $24.5 million, then it chose to accept 10.28 million shares of Curis instead of cash payment. The market value of these shares was about ₹124 cr. (FY2017 annual report, page 239).

So, instead of taking cash, the company accepted shares of Curis as consideration and lost ₹240 cr in FY2020 when the price of these shares declined.

This was not the only time when DRL lost money by taking exposure to equity markets. Previously, in the 1990s, when it had raised money through the GDR issue, then, instead of keeping the money in a bank account/deposits, it chose to invest the money in the share market.

In FY1997, when the company needed to use this money, the share market was down and it lost nearly ₹10 cr by selling those shares at a loss.

FY1997 annual report, page 17:

When we made the GDR issue a couple of years ago, the inflow did not go immediately into asset creation. We made financial investments instead – a mistake…The financial markets nosedived in 1996-97 and since we needed to fund our working capital requirements, we thought it best to sell the investments. The resulting loss was written off from the profit and loss account

Going ahead, an investor should monitor whether the company takes unnecessary risks in stock markets with its investments.

Also read: How to Identify if Management is Misallocating Capital

5) Contingent liabilities of Dr Reddy’s Laboratories Ltd:

DRL has been facing a few investigations and litigations for a long time where it has even deposited part of the penalty amount on the court’s insistence while its appeals are going on. An investor needs to keep a close watch on the outcome of these litigations.

Since the 1990s, DRL has been involved in litigation with the National Pharmaceutical Pricing Authority (“NPPA”) over the price of its drug, Norfloxacin. NPPA has put a penalty of ₹28.5 cr on DRL in FY2006 for overcharging for Norfloxacin. The appeal by DRL against the demand is currently going on.

Similarly, there is another demand by NPPA of ₹77 cr raised in FY2017 for overcharging of cardiovascular and anti-diabetic drugs, which is also under appeal.

In the USA, two former employees (whistleblowers) of the company complained to the U.S. Department of Justice (the “DOJ”) that the company has not done child-resistant packaging for some of its drugs. As DOJ started its investigation, the company entered into a settlement agreement with DOJ by paying ₹32 cr ($5 mn). However, the whistleblowers have filed an appeal against the settlement, which is currently going on.

In FY2020, DRL voluntarily recalled its Ranitidine medication from the USA as it contained a carcinogen, NDMA. Thereafter, thousands of cases were filed against the company in the USA, which are still ongoing.

There are numerous cases going on against the company in the USA on the allegations that it did the price-fixing of drugs with its competitors and also divided the market geography in collusion with other companies, which was alleged to be anti-competitive practices.

There are a few litigations against the company by its former overseas partners alleging that it did not meet the terms of the contract e.g. in Switzerland by Hatchtech Pty Limited, for which it had to pay $46.25 million (about ₹340 cr).

Currently, the company is facing an investigation by the Securities and Exchange Commission (“SEC”), USA for allegations that the company paid improper money (?bribes) to doctors in Ukraine to sell its products.

Additionally, there are a few cases where US govt. authorities claim that DRL did not file the correct data to them and instead filed misleading data. In one such case, DRL agreed to pay $9 million on complaints of the Public Employees’ Retirement System of Mississippi. In another case, DRL agreed to pay $12.9 million to the State of Texas. Currently, many other such cases are going on.

In India, DRL is facing cases against the pollution of land in Medak district against the Telangana State Pollution Control Board (“TSPCB”). Similarly, it is facing cases of water and air pollution in areas of its manufacturing plants.

The Margin of Safety in the market price of Dr Reddy’s Laboratories Ltd:

Currently (June 17, 2024), Dr Reddy’s Laboratories Ltd is available at a price-to-earnings (PE) ratio of about 18.2 based on consolidated earnings of FY2024.

We recommend that an investor read the following articles to assess the PE ratio to be paid for any stock, which considers the strength of the business model of the company as well. The strength in the business model of any company is measured by way of its self-sustainable growth rate and the free cash flow generating the ability of the company.

In the absence of any strength in the business model of the company, even a low PE ratio of the company’s stock may be a sign of a value trap where instead of being a bargain; the low valuation of the stock price may represent the poor business dynamics of the company.

Analysis Summary

Overall, Dr Reddy’s Laboratories Ltd seems a company that has worked hard on its research capabilities and has made its place in the global pharmaceutical world. Due to its significant R&D investments, it has become a big player in the largest pharmaceutical market of the world, the USA, which has led its sales to grow more than 1,000 times from FY1990.

During the initial years, when the company’s scale of operations was small, then it raised money through debt, equity dilution, funding partnerships to keep its high R&D spending and acquisitions to grow its market size. Nevertheless, in the last 10 years, the company’s scale of operations has grown big and it is able to produce a lot of surplus cash that it has used to do buybacks, pay dividends and make acquisitions.

The company has collaborated with many large overseas pharmaceutical companies to develop drugs, marketing and distribution. The increased scale of operations has helped the company to be low-cost in the commoditized business of generics and APIs and offer greater value to customers.

Nevertheless, the company has faced numerous litigations on its growth path. In some, it lost and had to pay others whereas in a few and gained significant money from opposite parties.

Its business is highly regulated and at times, changes in govt. policies have led to significant losses to its business e.g. in Germany (₹4,000 cr write-offs of Betapharm acquisition) and Venezuela (about ₹700 cr write-offs). At times, it lost business when foreign regulators did not provide approval to its plants.

Dr Reddy’s Laboratories Ltd’s business is working capital intensive as it has to keep a lot of inventory in its global supply chain to meet customers’ demand on short notice and it has to provide a longer credit period to overseas customers. Nowadays, every year, it loses almost ₹900-1000 cr in inventory write-offs and refund obligations.

Over the years, the company has entered into a few related party transactions with its promoter-group entities like acquiring land, sales & purchases of goods and services, buying/merging companies etc. which provide opportunities to shift economic value from public shareholders to promoters.

Over the years, the company has done numerous impairments/write-offs of investments with almost ₹800-1,500 cr annual write-offs on its recent drug acquisitions. In the past, it lost money by taking exposure to equity markets and even by investing the GDR money into stocks.

The company faces numerous litigations in India and abroad including the USA, with govt. authorities and private parties, where it might have to pay substantial money to settle the charges. An investor needs to closely monitor the outcome of such litigations.

Going ahead, an investor should keep a close watch on the regulatory developments in the pharmaceutical markets served by DRL, and the resolution of observations raised by USFDA on its plants.

Further recommended reading: How to Monitor Stocks in your Portfolio

These are our views on Dr Reddy’s Laboratories Ltd. However, investors should do their own analysis before making any investment-related decisions about the company.

You may use the following steps to analyse the company: “Selecting Top Stocks to Buy – A Step by Step Process of Finding Multibagger Stocks”

I hope it helps!

Regards,

Dr Vijay Malik

P.S.

Disclaimer

Registration status with SEBI:

I am registered with SEBI as a research analyst.

Details of financial interest in the Subject Company:

I do not own stocks of the companies mentioned above in my portfolio at the date of writing this article.

Source link

{kind=link}