Forex overview. Diverging Central Bank Stories – ForexNews.PRO

On the same day that President Trump appointed a temporary, dovish ally to the FOMC, the Bank of England adopted a more hawkish stance, narrowly approving a further 25 basis point rate decrease. The U.S. economic calendar is light today, so attention will be on Canadian employment data. The EUR/USD pair may consolidate ahead of next week.

On the same day that President Trump appointed a temporary, dovish ally to the FOMC, the Bank of England adopted a more hawkish stance, narrowly approving a further 25 basis point rate decrease. The U.S. economic calendar is light today, so attention will be on Canadian employment data. The EUR/USD pair may consolidate ahead of next week.

USD: Trump Appoints Dovish FOMC Member President Trump nominated Stephen Miran to provisionally fill the FOMC seat until the end of January, subject to Senate confirmation in September. Miran has echoed Trump’s dovish sentiments and criticisms of the Fed, minimizing the inflationary effects of tariffs. He is expected to side with Christopher Waller and Michelle Bowman in the dovish camp during his brief tenure, with a possibility of advocating for a 50bp move.

This is a temporary appointment, and reports suggesting that Waller is now the leading candidate to replace Fed Chair Jay Powell may have lessened the negative impact on short-term rates. The US dollar experienced only a modest weakening following the announcement.

The US macro calendar is quiet today. Yesterday, initial jobless claims increased to 226,000 after a period of decline. Continuing claims rose to 1,974,000, the highest level since November 2021, indicating a worsening job market.

Given the lack of market catalysts and proximity to Tuesday’s CPI release, DXY is likely to stabilize around 98.0 today, although the overall trend remains bearish.

Canada will release jobs data today. We anticipate an increase in the unemployment rate, potentially rising to 7.0%. Our outlook for CAD remains bearish due to the market’s underestimation of the risk of two Bank of Canada rate cuts this year, stemming from the tariff fallout.

EUR: Markets Cautious About Ukraine Truce Hopes Following an initial boost to the euro from news of a potential Trump-Putin meeting, markets are now evaluating the likelihood of a truce. They are expected to proceed cautiously, considering the limited indications that Russia is prepared to agree to a complete ceasefire in Ukraine. Energy prices, EUR/USD, EUR/CHF, and EUR/JPY will be key indicators of market sentiment.

Scandinavian currencies should also benefit if geopolitical risks subside, with the Swedish krona potentially outperforming the Norwegian krone. Sweden reported an increase in July CPIF inflation to 3.0%, but this was widely anticipated, and core inflation slowed more than expected to 3.1%.

While we are not forecasting additional Riksbank rate cuts, this has become a closer call following the EU-US trade deal. However, markets have already priced this in, so we remain positive on SEK in the medium term.

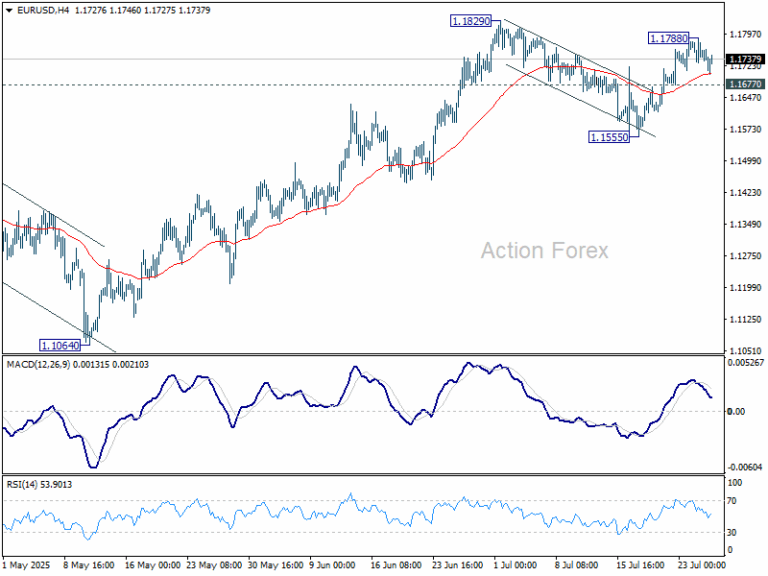

Regarding EUR/USD, we anticipate some stabilization in the 1.166-1.170 range. Next week’s US CPI data will determine whether a further break higher is possible.

GBP: Sharp Division at the BoE Yesterday’s 25bp rate cut by the Bank of England had a hawkish undertone. The MPC required two rounds of voting to achieve a 5-4 majority, revealing a larger-than-expected hawkish dissenting faction. Additionally, the BoE hinted at the nearing end of the easing cycle by stating that “the restrictiveness of monetary policy has fallen as Bank Rate has been reduced.”

Governor Andrew Bailey’s press conference was not as hawkish, but given the upward revision in inflation forecasts and lessened concerns about the jobs market, the bear flattening of the yield curve and sterling’s rally are justifiable. Another rate cut by year-end is now less than fully priced in.

Another key topic was the reduction in quantitative tightening. The MPC estimated that QT added 15-25bp to back-end yields, maintaining expectations of a reduction in September.

The hawkish dissent emphasizes the importance of future inflation data. A more convincing moderation now seems necessary for another 2025 cut to be fully priced in. Sterling is therefore in a stronger position, though adverse fiscal conditions and EUR strength may limit further EUR/GBP correction. Cable remains appealing, with a move above 1.35 possible.