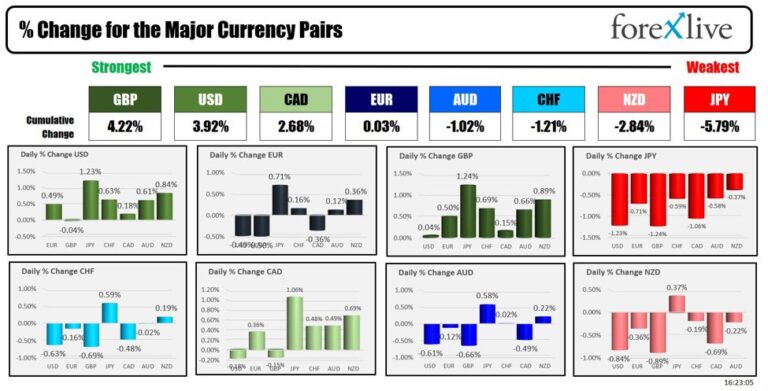

Forex overview. US Dollar Stabilises as Markets Digest Fed Signals – ForexNews.PRO

The US dollar stabilises after post-Fed selling, pressured by lower rate expectations and seasonality. Attention is moving to the ECB and German inflation to test the hawkish market switch. CEE markets remain calm ahead of key central bank meetings next week, while Turkey cut rates by 150bp amid easing inflation

The US dollar stabilises after post-Fed selling, pressured by lower rate expectations and seasonality. Attention is moving to the ECB and German inflation to test the hawkish market switch. CEE markets remain calm ahead of key central bank meetings next week, while Turkey cut rates by 150bp amid easing inflation

USD: Dollar Stabilises after Fed Meeting

Following Wednesday’s Fed meeting, the US dollar extended its decline yesterday, with the DXY closing near 98.00, close to our expectations. The bearish wind is coming not only from interest rates but also from end-of-year seasonality, in our view. Dollar rates saw another calibration of Fed expectations lower, with the 2-year falling to 3.50% and the market pricing in 3.05% as the Fed terminal rate at the end of next year, keeping pressure on the US dollar.

Today’s US calendar does not have much to offer, and the market should stabilise somewhat after the risk event. Some risk-off sentiment coming from equities should, on the other hand, provide some floor for the dollar. Overall, DXY around 98.350 with a small downside to 98.200 seems fair for now, in our view.

EUR: Attention Shifts to Eurozone Central Bankers

German inflation figures for November are expected to come in at 2.6% year-on-year, the highest level in nine months, as another piece to the puzzle of higher euro rates and a shift in market pricing to the hawkish side. Following the Fed meeting this week, the market’s attention will shift to the ECB meeting next Thursday. President Christine Lagarde will present a new forecast, which should be the first test of the current pricing of no further rate cuts, in line with our view.

The front of the EUR curve saw a significant upward move this week, by 10bp in the 2y tenor, which directly countered the movement of USD rates, supporting further spread tightening in favour of the EUR. After EUR/USD touched 1.175 yesterday, the stabilisation of the US dollar should bring a slight correction in EUR/USD more towards the middle of the 1.170-175 range.

Elsewhere, UK GDP figures for October surprised slightly lower, with the economy unexpectedly contracting by 0.1% MoM, dragged down by manufacturing, supporting the Bank of England cutting case next week with 22bp priced in currently. The pound is little changed this morning, but the opening suggests some pressure to weaken closer to 0.878 EUR/GBP.