Forex. US Dollar Caught in Limbo as Missing Data and Rising Vols Cloud Fed Outlook – ForexNews.PRO

If you were anticipating dramatic market fireworks following Washington’s reopening, you likely walked away with little more than a flickering sparkler and a shrug. The “lights-back-on” story had already been priced in before the shutdown began—and even during the pause, markets barely reacted, treating resolution as the default assumption.

If you were anticipating dramatic market fireworks following Washington’s reopening, you likely walked away with little more than a flickering sparkler and a shrug. The “lights-back-on” story had already been priced in before the shutdown began—and even during the pause, markets barely reacted, treating resolution as the default assumption.

Yes, Congress reopened its doors, but the market hardly blinked. The focus has shifted away from political theatrics, landing squarely in the engine room of economics. It is here where AI capital expenditures, liquidity mechanics, and overextended valuations churn like strained machinery approaching their limits.

The next decisive market movement is set to emerge from rate markets. After weeks of subdued activity, implied volatility in swaptions is beginning to stir as traders anticipate a return to crucial data points. With a December Fed rate cut priced at roughly 64-65%, uncertainty looms as the White House warns that important metrics like October payrolls and CPI data might remain unseen. This vacuum leaves the front-end exposed, yet without quantitative triggers for repricing. Meanwhile, rising interest in bullish Treasury options signals that the market leans toward the “soft data → dovish Fed” narrative. Should this materialize, the dollar may face more downside than the yield curve currently anticipates.

At the long end of the curve, trading sentiment isn’t driven by reopening optimism but by impending regulatory adjustments. Revisions to leverage ratio rules are already expanding theoretical balance sheet capacity for Treasuries among banks, effectively narrowing the UST-swap spread by over 10 basis points in recent months. According to reports, these regulatory changes could be finalized soon—far outshining any influence from Washington’s negotiations and driving long-term yields lower even as risk assets remain resilient.

On the other side of the Atlantic, Europe basks in its own phase of low volatility. France’s OAT-Bund spread compression to 72 basis points illustrates traders betting on continued near-term tranquility. Progress on budget discussions, suspended pension reforms, and optimistic GDP projections from the Bank of France offer temporary reprieve. Yet, beneath the calm surface lies the recognition that sustained fiscal challenges will hit multi-year milestones, particularly nearing the 2027 presidential cycle. For now, subdued volatility makes tactics like spread trading seem almost effortless.

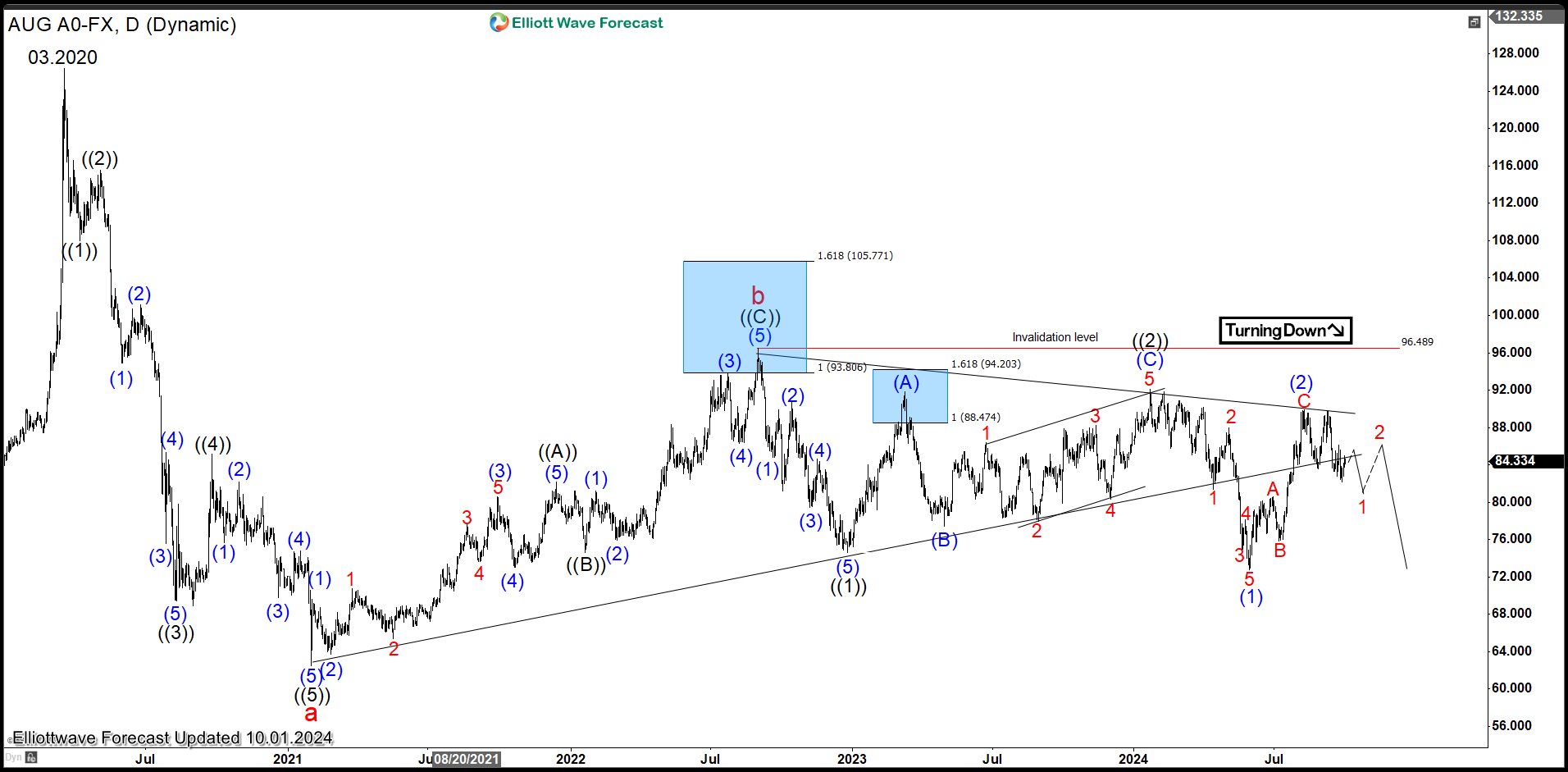

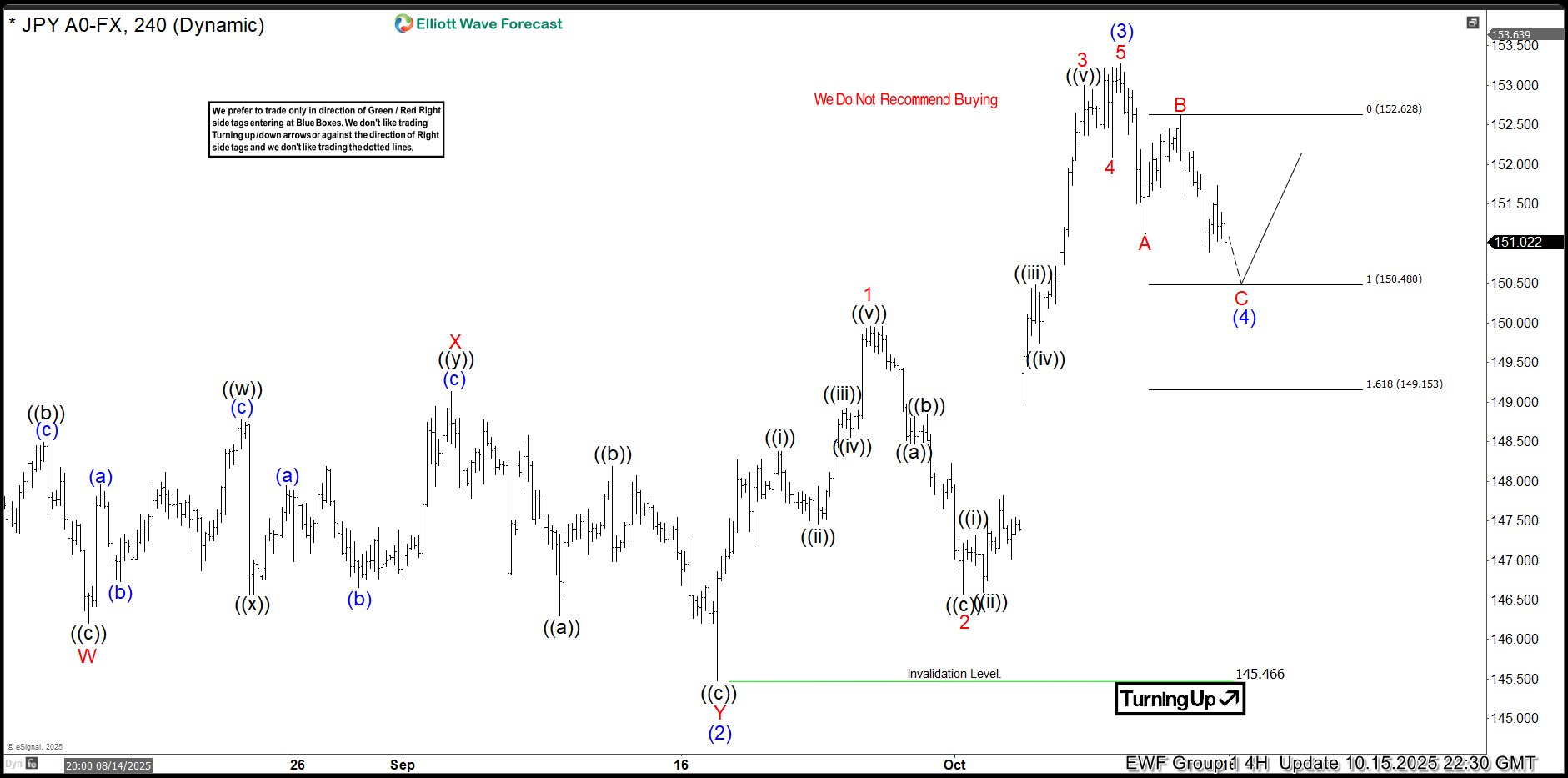

In FX markets, USD/JPY remains firmly at the heart of activity. Tokyo traders report sustained demand for dollars despite cooling fixing pressures. Japan’s Ministry of Finance appears unwilling to act until US data offers clarity, even as USD/JPY drifts past 155 into what is widely perceived as intervention territory. While verbal warnings remain their primary strategy for now, history suggests a deviation from traditional intervention patterns—last July’s response came after a sharp yen rally rather than during a slide. If this playbook holds, their next move might occur during a dollar decline rather than its rise. Until fresh data emerges, verbal threats are the only ammunition, leaving markets to probe new heights like 156–158 in search of structural resistance.

Meanwhile, the Australian dollar has seized positive momentum with solid economic performance. Unemployment dropped back to 4.3%, and the economy added an impressive 42,000 full-time jobs, prompting markets to push expectations for central bank easing further down the timeline. Unlike its G10 counterparts, AUD rises with justified strength; it currently stands as the sole currency with genuine bidirectional potential. A climb toward 0.68 heading into mid-2026 now looks like a baseline scenario rather than mere optimism.

EUR/USD continues to flirt with 1.16 in slow motion. Market forecasts for 2026 project a bullish range of 1.20–1.25, bordering on overconfidence given current dynamics. However, near-term upward movement lacks momentum; with undervaluation gaps mostly closed and no catalytic shift from Federal Reserve policy on the horizon, shorting the dollar against carry advantages remains challenging. To see a decisive breakout above 1.17, truly weak US data will be required rather than recycled narratives about soft landing expectations. Until then, EUR/USD remains rangebound while volatility sellers enjoy their extended run.

The broader FX landscape persists along familiar lines forged over 2024 and 2025. USD/JPY teeters near intervention thresholds; AUD shines as G10’s star performer backed by credible fundamentals; EUR/USD wades through sluggish momentum awaiting data catalysts; and the overall dollar remains locked in stasis until pivotal US macroeconomic releases resume. Washington may have flipped the switch back on, but for now, the eFX engine room needs active data inputs to ignite meaningful shifts in momentum.