Frequently Asked Questions about Risk Reversals

Risk reversal is an options strategy that sells options to raise cash to buy options for a directional play.

When words are not sufficient to convey the concept, an example is needed.

Contents

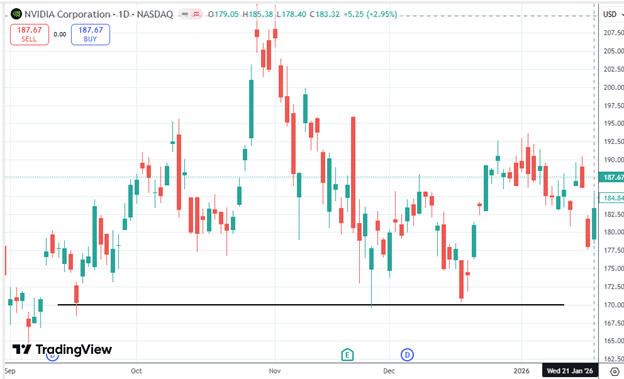

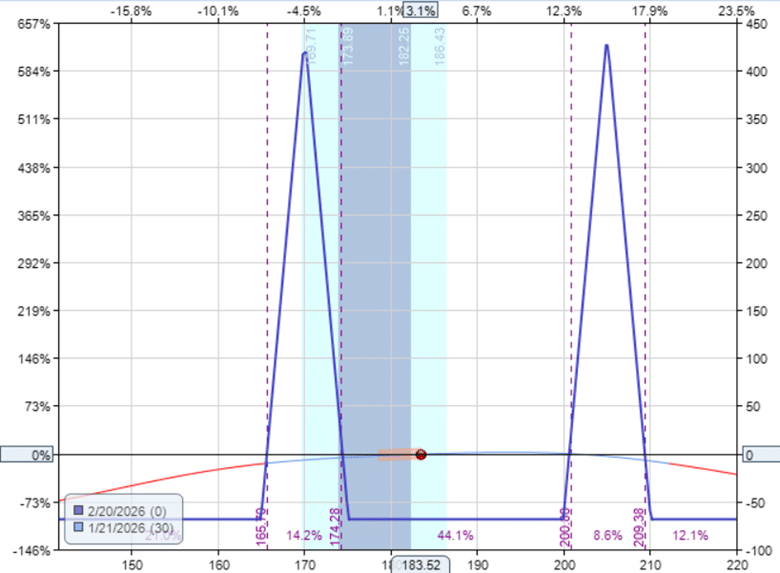

Suppose an investor is bullish on Nvidia (NVDA) and wants to buy an out-of-the-money bullish call spread like the one below.

This 200/205 call spread with 30 days to expiration would cost $88 per contract.

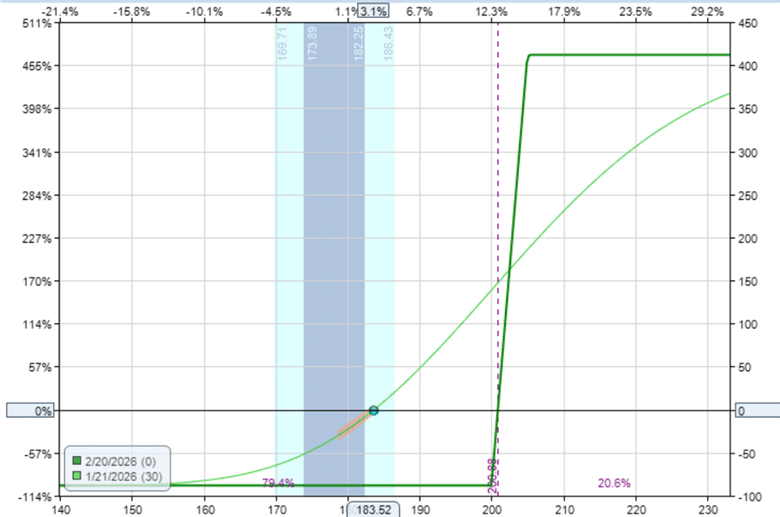

As of January 21, 2026, he also expects NVDA’s price to remain above $170 per share.

It looks like there is some support at $170, with a double bottom pattern.

Therefore, he can sell a 170/165 put credit spread below the $170 level.

This would give him $99 of credit per contract – enough to cover the cost of the call debit spread.

Putting the two orders together:

Date: Jan 21, 2026

Price: NVDA @ $183.50

Buy a call debit spread:

Buy to open one contract Feb 20 NVDA $200 call @ $2.36

Sell to open one contract Feb 20 NVDA $205 call @ $1.48

Debit: $88

Sell put credit spread:

Buy to open one contract Feb 20 NVDA $165 put @ $2.18

Sell to open one contract Feb 20 NVDA $170 put @ $3.17

Credit: $99

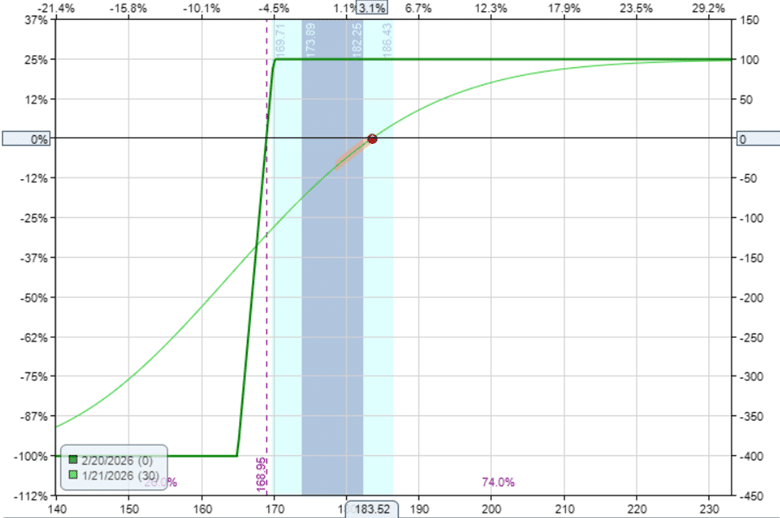

The combination of the two is known as a bullish risk reversal with the following payoff graph.

It is definitely bullish because both the call spread and the put spread are bullish.

The position delta in the example is 13.

The theta is negative but very small at -0.45.

Similarly, the vega is negligible at 0.33.

Gamma is also negligible.

So, essentially, this is primarily a direction play.

Maybe some might market it as that.

But that’s not really accurate.

If you sell your camera to buy a phone, are you getting a free phone?

We can say that the credit spread is financing the debit spread.

Because it transfers the risk from the call side to the put side.

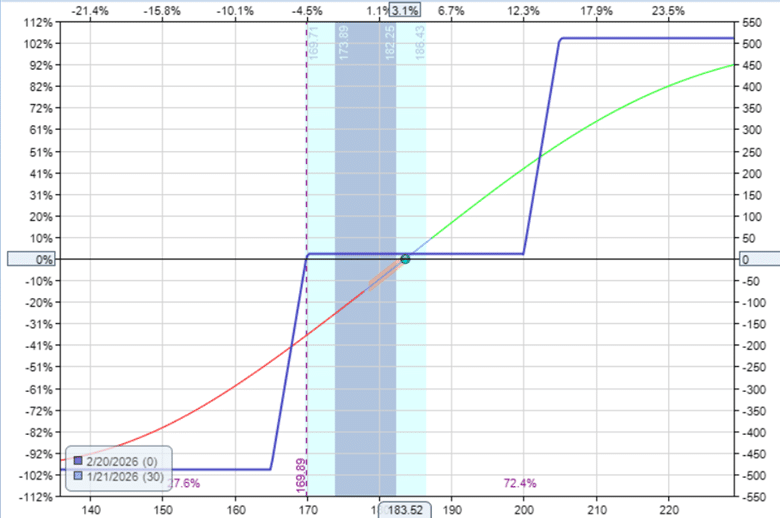

The maximum risk in a debit spread is that the spread value reaches zero, and the premium we paid is lost.

Because the call spread is fully paid for by the credit received from the put credit spread, there is nothing more that can be lost on the debit spread.

The debit spread is risk-free.

Price can completely breach the call spread, and the trade can still be profitable as long as the put spread is not breached at expiration.

Therefore, the trade is not risk-free.

The onus is on the put spread not be breached.

In our example, as long as the price is above $170 at expiration, the trade is profitable.

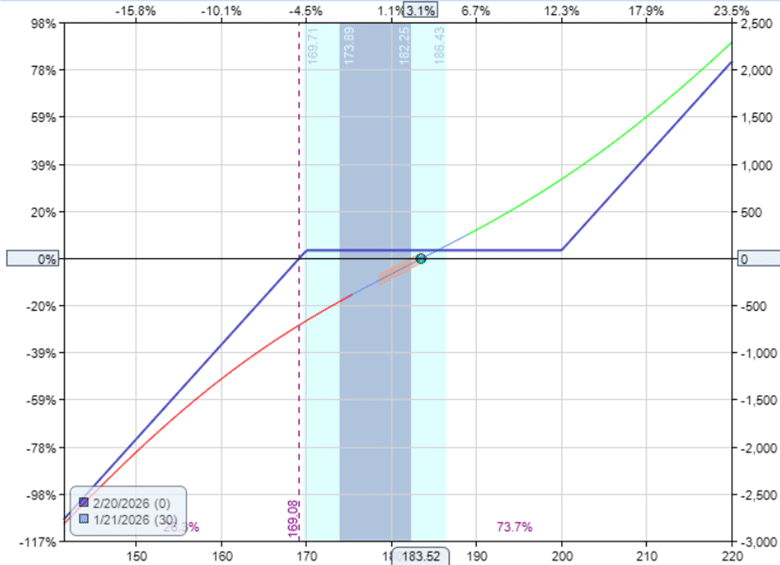

If we hadn’t sold the put credit spread, the call debit spread would be at a loss if the price is below $200.

The risk reversal had moved the breakeven point further away.

NVDA has to drop more to make the trade lose.

Yes. For example:

It can also be formed by other structures.

As long as the put structure helps pay for, or partially pays for, the call structure, we can generically call it a risk-reversal trade.

Yes. Everything we’ve talked about was for a bullish risk reversal.

Just apply the same concept for bearish.

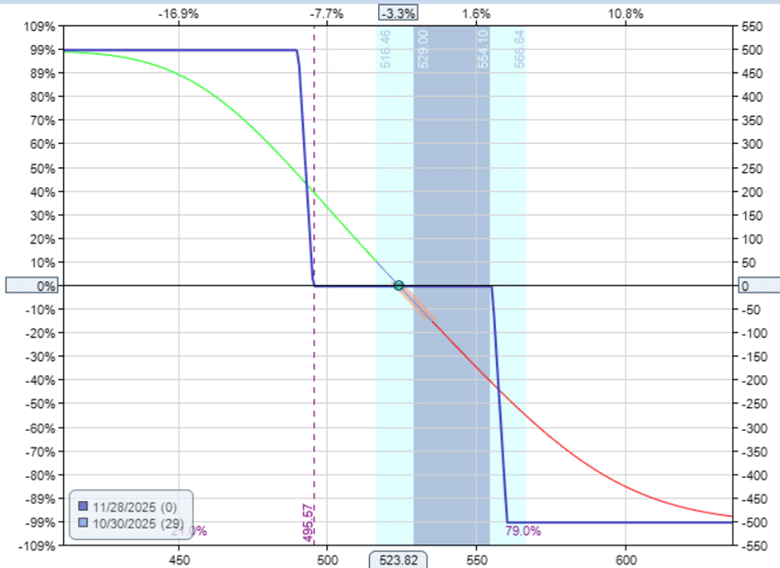

Here is an example of a bearish risk reversal on Microsoft (MSFT)…

Date: Oct 30, 2025

Price: MSFT @ $523.80

Sell one Nov 28 MSFT $490 put @ $2.79

Buy one Nov 28 MSFT $495 put @ $3.55

Sell one Nov 28 MSFT $555 call @ $3.62

Buy one Nov 28 MSFT $560 call @ $2.90

Net Debit: $4

Yes, as is shown in the last example.

Without the credit, the price range of $495 to $555 would be a loss if MSFT’s price closed there at expiration.

But it would be considered a very tiny loss of -$4.

Either. That is the trader’s choice.

The NVDA shows how it can be done in two transactions, which might make it easier to fill at fair prices.

The MSFT example shows how this can be done in a single transaction, so a trader who is not in a rush can set a Good-till-cancel order at a favorable price for the whole package.

You would neutralize the directionality of the trade and probably end up with a double butterfly like this or similar (depending on the strikes chosen).

Yes.

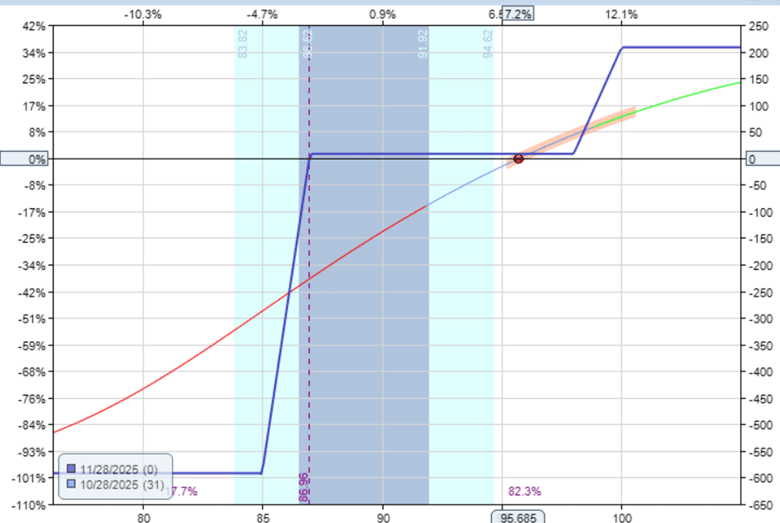

Here is a bullish risk reversal on Target (TGT) that required three put credit spreads to generate sufficient credit to cover the one debit spread…

Based on a technical analysis of the chart, the trader may have preferred the put credit spreads to be further out of the money, which would yield less credit.

In summary, risk reversals offer a flexible way to express a direction by selling an out-of-the-money option spread to finance the purchase of another option structure.

We hope you enjoyed this article answering frequently asked questions about risk reversals.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Source link