Pack your cash in the BOXX ETF

That is BOXX, spelled with double X, not to be confused with BOX, which is Box Inc., a provider of cloud content management.

BOXX is the EA Series Trust Alpha Architect 1-3 Month ETF.

Issued by Alpha Architect, its ETF presentation page says BOXX is “an options-based alternative to an ultrashort duration bond position.”

Using European-style options on the S&P 500 or a similar diversified index/stocks/ETFs, the fund constructs box spreads with expirations ranging from one to three months.

European-style options are cash-settled, so they do not have assignment risk.

Contents

What Are Box Spreads?

Now we see why the ticker symbol is BOXX.

A box spread is an advanced options strategy that combines a synthetic long position with an equivalent synthetic short position, which should make no money.

However, it does generate a small amount of revenue due to the “cost of carry,” which explains why forward prices differ from spot prices.

The box spread has a fixed payout at expiration regardless of the directional movement of the underlying.

The profit is derived from the difference between the cost of entering the trade and the fixed payoff.

The net outcome is that it behaves like a risk-free bond, mirroring the risk-free rate of return.

Example Of A Box Spread

This example is intended to illustrate the concept of the box spread and is not an exact representation of the one used by the BOXX fund.

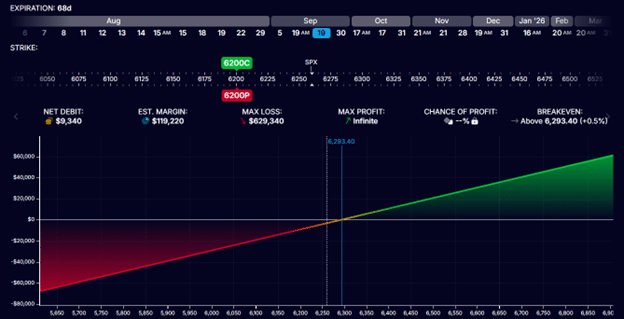

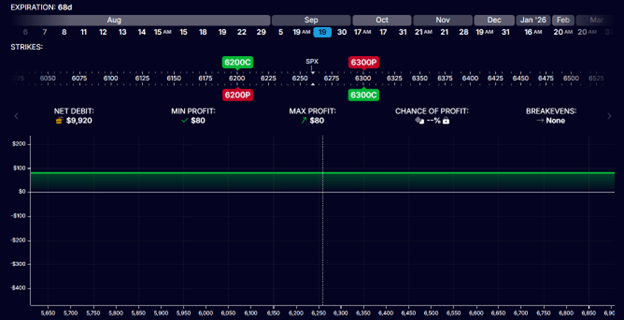

If an investor is to buy a call option on the SPX at the 6200 strike and sell a put option at the same strike and same expiration, that is about 68 days out, the investor has created a synthetic long position:

If an investor sells a call option on the SPX at the 6300 strike and buys a put option at the same strike, the investor creates a synthetic short position…

By combining all four legs into a single order, the investor has created a box spread.

As can be seen in this hypothetical simulation, the cost of entering the box spread is $ 9,920 debit.

The BOXX fund enters the box spread as a single order and does not attempt to break it into legs.

You will also note that the box spread is a combination of bull call spread and a bear put spread of the same width of $100.

Therefore, if the price of the underlying is above $6,300 at expiration, the bull call spread receives its maximum profit of $10,000, while the bear put spread expires worthless.

Since one contract controls 100 shares, we have $100 x 100 = $10,000.

If the price of the underlying is below 6200 at expiration, the bear put spread pays out its max profit of $10,000 while the bull call spread becomes worthless.

If the price of the underlying is in between the two strikes, the math would show that it too will have a payout of $10,000.

This box spread has a payout of $10,000 at expiration regardless of the price of the underlying.

Since it only costs $ 9,920 to enter the spread, this box earns $80 for every $10,000 in 68 days.

This is equivalent to an annualized return of 4.3%.

Because $80 / $10,000 * 365 / 68 = 4.3%

Performance Of BOXX

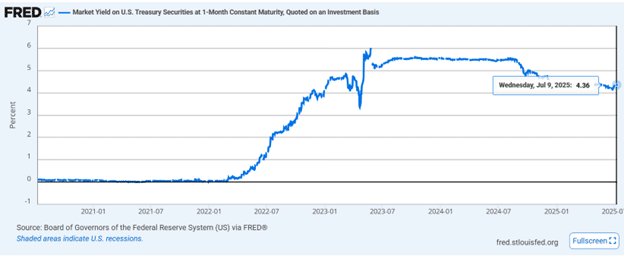

The BOXX fund’s performance objective is to achieve yield and price performance comparable to that of the 1- to 3-month U.S. Treasury Bill market, which, as of July 13, 2025, is 4.36% according to FRED (Federal Reserve Economic Data).

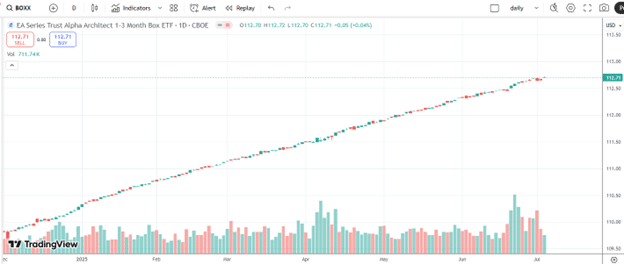

Looking at the candlestick chart of BOXX and doing some quick math:

The price opened at $110.29 for one share at the start of 2025.

By the end of June, it had risen to $ 112.68, up $ 2.39.

By the end of the year, one would expect to have $4.78 (if rates remain the same)

Therefore, $4.78 / $110.29 = 4.3% annual yield.

Yes, I would say that BOXX performance matches expectations.

Comparison To BIL ETF

Can the investor buy the BIL ETF instead of BOXX?

Sure, they can.

Since the BIL invests in fixed income U.S. Treasuries known to match the risk-free rate of return, both BIL and BOXX should perform the same. Let’s see.

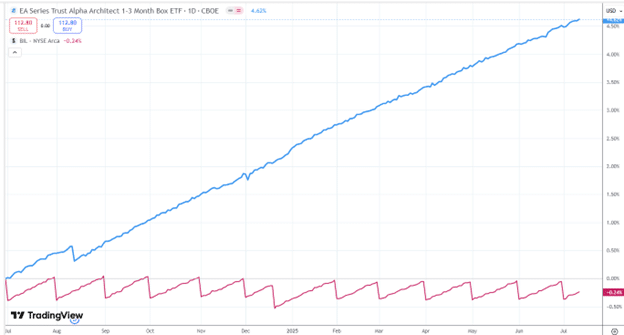

Normally, we can compare the relative performance of two assets by charting both of them together with percentage gain/loss on the y-axis.

For example, here is the relative performance of Pepsico (PEP), graphed on the blue line, and Coca-Cola (KO) is graphed on the red line for the trailing 12 months…

Source: tradingview.com

However, this can not be done between BOXX (blue line) and BIL (red line)…

This is because BIL’s NAV (net asset value) drops every time it pays out a dividend, which is once a month.

BOXX has only one dividend payout per year, yielding approximately 0.26% annually.

Therefore, we need to manually compute the gain in value for the trailing twelve months from July 1, 2024, to June 30, 2025.

BIL opened at $91.42 and closed at $91.73, receiving a total of $ 0.31 in dividends during that period.

That represents a gain of $4.51, or 4.9%, for the trailing twelve months.

BOXX opened at $107.84 and closed at $112.68 and received a total of $0.291 in dividends during that same period.

That is a gain of $5.13, or 4.8%, for the trailing twelve months.

We can say that the performance of BIL and BOXX is comparable because they are both expected to return the risk-free rate of return.

The annual rate of 4.8% is slightly higher in this calculation than the 4.3% because the risk-free rate of return was slightly higher in July 2024 than it is in July 2025.

Conclusion

The box spread is typically used only by institutional investors because options synthetics can be complicated for retail investors.

And there is the real danger of making a mistake.

If, for example, an American-style option was incorrectly used on an assignable underlying (such as SPY), it is possible for a short option to be assigned early before expiration – particularly in-the-money short calls before ex-dividend dates.

This can break the box structure and expose the investor to directional risk, where they may lose a significant amount of money if the underlying asset moves in the wrong direction.

It is for this reason that box spreads are restricted in certain types of accounts.

If you have extra cash lying around, don’t mess around trying to construct box spreads.

Just pack your cash into the BOXX ETF instead.

Although it has been seen that certain accounts held at certain banks have been known to restrict even the BOXX ETF.

In that case, just buy U.S. Treasuries via BIL.

That’s the simplest, and there’s no need to get any fancier, since there is no good way to squeeze more performance out of products designed to return the risk-free rate.

We hope you enjoyed this article on the Boxx ETF.

If you have any questions, send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Source link