Market Snapshot March 25th 2026 – The Concept Trading

4 days left to negotiate…

Note: Please get yourself updated with the current status of this war as it will update per seconds, any volatility from the next morning is getting the charts among the highest levels. Stay in the highest cautious.

Data:

- [🟦 Global Rates | Yields consolidate at elevated levels amid persistent inflation risks]

Global sovereign yields stabilized after recent volatility but remained near cycle highs as markets continued to price “higher-for-longer” policy paths.

S.: 2Y ~3.83% | 5Y ~3.90% | 10Y ~4.27% | 30Y ~4.90%

UK 10Y ~4.70% | Germany 10Y ~2.95% | France 10Y ~3.60% | Italy 10Y ~3.72%

Canada 10Y ~3.46% | Australia 10Y ~4.95% | Japan 10Y ~2.20% | China 10Y ~1.83% | New Zealand 10Y ~4.62%

Rates remain anchored by energy-driven inflation expectations and central banks’ cautious stance on easing. - [🟨 U.S. Equities | Mild rebound as markets stabilize after prior selloff]

S. equities posted modest gains as investors engaged in selective dip-buying following recent declines.

S&P 500 (US500) ~6,555 (+0.2%)

Dow Jones ~45,920 (+0.3%)

Nasdaq Composite ~21,880 (+0.1%)

Gains were supported by defensives and energy, while technology remained subdued amid higher yields. - [🟨 Europe Equities | Slight recovery but upside remains limited]

European equities edged higher following prior weakness, though macro risks continue to cap gains.

Euro Stoxx 50 (EU50) ~5,670 (+0.5%)

DAX (GER40) ~23,180 (+0.6%)

CAC 40 ~7,900 (+0.4%)

The region remains sensitive to energy prices and weak industrial momentum. - [🟨 Asia Equities | Mixed performance across the region]

Asian markets traded mixed as investors balanced global headwinds with local stabilization.

Nikkei 225 ~54,800 (+0.2% to +0.4%)

Japanese equities stabilized after recent volatility, though energy and FX dynamics remain key risks. - [🟥 Macro “Red News” | PMIs highlight divergence between U.S. resilience and global softness]

S. Flash PMIs: Continued expansion in services sector, signaling economic resilience.

Eurozone PMIs: Manufacturing contraction persists, especially in Germany, while services show limited growth.

UK PMIs: Indicate ongoing price pressures despite slowing activity.

China: Activity indicators show gradual stabilization supported by targeted policy measures.

The macro backdrop reflects resilient U.S. growth contrasted with weaker European momentum. - [🟧 High-impact headlines]

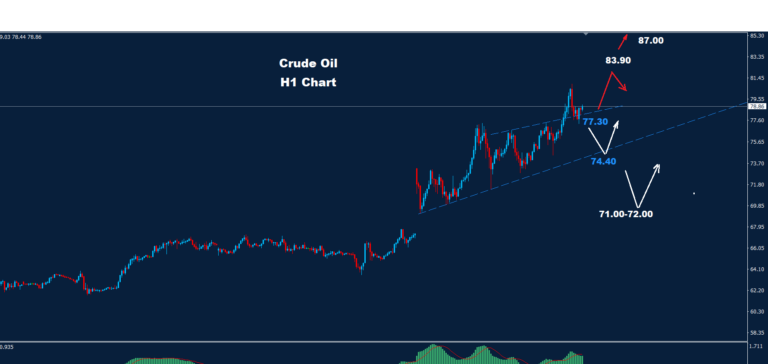

- Oil remains elevated near $100/bbl, sustaining inflation pressure and cross-asset volatility

- Global bond markets stabilize after sharp repricing, though yields remain near highs

- Equity markets attempt technical rebound following recent declines

- European growth concerns persist, driven by weak industrial and sentiment data

- USD remains supported by yield differentials and relative growth strength

- Investor positioning remains defensive, favoring commodities and low-beta assets

- Financial conditions remain tight globally, weighing on risk appetite

Companies.

+) Nvidia remained the primary market driver as investors continued to price in strong AI-chip demand and sustained hyperscaler capital expenditure into 2026.

+) Microsoft traded higher as enterprise adoption of AI-powered tools across Azure and Copilot continued to accelerate.

+) Apple remained under pressure amid ongoing concerns about iPhone demand and intensifying competition from Chinese smartphone manufacturers.

+) Tesla stayed volatile as continued price adjustments raised concerns about margin compression and global EV demand.

+) Meta Platforms gained modestly as digital advertising demand remained resilient and AI-driven engagement metrics improved.

+) Alphabet traded mixed as investors weighed long-term monetization of AI services against rising infrastructure costs.

+) Semiconductor equipment firms ASML and Lam Research remained supported by strong long-term demand for advanced chip manufacturing capacity.

+) Cybersecurity companies including CrowdStrike and Palo Alto Networks stayed firm amid continued enterprise spending on cloud security.

+) Defense contractors such as Lockheed Martin, Northrop Grumman, and RTX attracted steady inflows as geopolitical tensions supported defense spending expectations.

+) Energy majors Exxon Mobil and Chevron traded stable to slightly higher as crude oil prices consolidated near recent highs.

+) Cryptocurrency-linked companies such as Coinbase moved in line with fluctuations in Bitcoin, which remained volatile but supported by institutional demand.

+) Analysts continued to highlight the AI ecosystem—from semiconductors to cloud, cybersecurity, and software—as the dominant structural growth theme driving global equities in 2026.

General

Global markets opened with a moderately constructive tone, as investors extended the prior session’s relief rally following geopolitical de-escalation signals, while remaining cautious about the durability of the move.

Equities:

Global equities advanced modestly, supported by a rotation into cyclicals and previously lagging sectors. U.S. markets were led by transport and consumer names benefiting from lower fuel cost expectations, while energy and defense stocks underperformed after recent outperformance.

European markets also moved higher, though gains were capped by lingering macro uncertainty and weak growth expectations.

Rates & Monetary Policy:

Bond yields eased slightly as oil prices corrected, reducing near-term inflation concerns. Markets began to reassess the likelihood of earlier monetary easing if energy prices continue to stabilize.

However, central banks—particularly the Fed—remain cautious, with policy still dependent on sustained disinflation trends.

FX & Safe Havens:

The U.S. dollar softened modestly as safe-haven demand declined, while gold extended its pullback following reduced geopolitical risk.

Macro Theme:

Markets shifted into a “relief rally / recalibration phase”, driven by easing geopolitical risk premium and lower energy prices.

Upcoming News

Markets move into Wednesday with a growth- and policy-sensitive tone, as investors balance recent confidence and housing signals against expectations for central bank trajectories into Q2. Overall market sense is cautiously neutral with a slight defensive tilt, as FX and rates continue to react to yield differentials and commodity-driven inflation risks rather than fresh inflation data. Volatility is expected to remain moderate but event-driven, with positioning still adjusting after last week’s central bank cycle.

In the United States, attention centers on New Home Sales and energy-related flows (EIA inventories), both offering insight into demand resilience and inflation dynamics. Housing demand remains a key transmission channel for financial conditions; stabilization in new home sales would support the soft-landing narrative and help anchor yields, while renewed weakness could reinforce expectations of gradual economic cooling and weigh modestly on the USD. Oil inventory data will also be closely monitored given the recent energy price volatility, as it may influence inflation expectations and commodity-linked FX.

Across Europe, the calendar is relatively light, leaving EUR trading primarily on U.S. yield movements and residual PMI repricing. In the Asia–Pacific region, Australia’s inflation indicators provide incremental insight into domestic price pressures relevant for the RBA, while Japan remains largely reactive to global rate dynamics. Corporate catalysts remain limited, keeping macro interpretation and positioning adjustments as the dominant drivers mid-week.

| Time (GMT+7) | Category | Country / Region | Event | Market Relevance |

| 08:30 | 🔴 Red News | Australia | CPI Indicator (y/y) | Inflation signal; RBA policy sensitivity |

| 20:30 | 🔴 Red News | United States | New Home Sales | Housing demand; USD & rates impact |

| 22:30 | 🔴 Red News | United States | Crude Oil Inventories (EIA) | Energy prices; inflation-linked flows |

| All day | 🔶 Stress / Headlines | Global | Commodity volatility / policy headlines | May influence FX and rates direction |

Snapshot (25.3.2026)

🛢 Oil | Continued Pullback

- WTI Crude 87.53 (-0.96%)

- Brent Crude 99.76 (-0.38%)

Oil prices extended declines, with WTI slipping below $90 and Brent easing toward the $100 level, indicating fading momentum after the recent surge.

🟢 Dollar Flat | DXY 99.15 (-0.04%)

The U.S. Dollar Index traded sideways just below 100, suggesting a neutral stance as markets consolidate.

🔄 G7 FX | Mild USD Weakness

- EUR/USD 1.1620 (+0.11%)

- GBP/USD 1.3423 (+0.09%)

- USD/JPY 158.78 (+0.06%)

- USD/CHF 0.7877 (-0.07%)

The dollar softened slightly against European currencies, while yen remained broadly stable.

🪙 Crypto | Mixed, Slight Uptrend in BTC

- BTC 70,641 (+0.17%)

- ETH 2,154 (-0.05%)

- SOL 90.86 (-0.58%)

Crypto markets were mixed, with Bitcoin holding above 70k while altcoins showed mild weakness.

🥇 Metals | Strong Rebound

- Gold 4,553 (+1.86%)

- Silver 73.31 (+2.84%)

Precious metals rallied strongly, supported by softer dollar and renewed safe-haven demand.

📊 Equities | Mixed Performance

- S&P 500 6,609.28 (+0.12%)

- Euro Stoxx 50 5,659.26 (+0.12%)

- Dow Jones 46,520.47 (+0.16%)

- Nasdaq 24,002.45 (-0.77%)

- VIX 24.07 (-0.82%)

Equities showed mixed moves, with broader indices slightly higher while Nasdaq underperformed, indicating rotation away from tech.

This report is provided to The Concept Trading from Van Hung Nguyen