Market Snapshot March 5th 2026 – The Concept Trading

Trump SAID COVERING the OIL SHIP!

Note: Please get yourself updated with the current status of this war as it will update per seconds, any volatility from the next morning is getting the charts among the highest levels. Stay in the highest cautious.

Data:

[🟦 Global Rates | Major 10Y yields] Core yields stayed firm as markets weighed geopolitics vs. policy. UST 10Y ~4.081% (up from ~4.056%) | Canada 10Y ~3.263% | UK 10Y ~4.4% (energy-inflation risk premium) | Australia 10Y ~4.79% (reported local surge on inflation/geopolitics concerns).

[🟩 Equity Indices | U.S.] Risk sentiment improved as oil paused and crypto surged. Dow +0.49% | S&P 500 +0.78% | Nasdaq +1.29%.

[🟩 Equity Indices | Europe] Europe staged a strong rebound from prior selloff. STOXX 600 +1.4% | DAX +1.7% (largest one-day gains since May, per Reuters); CAC 40 ~8,167.73 (+0.79%).

[🟥 Equity Indices | Japan] Asia de-risking remained acute on energy-shock fears. Nikkei 225 −3.76% to ~54,161 (large exporters/industrials hit; volatility elevated).

[🟥 Asia Risk | Korea stress] Regional selling intensified, with KOSPI down ~12% (circuit breaker triggered) amid oil-dependency concerns and broad deleveraging.

[🟨 Macro “Red News” | U.S. activity + jobs signals] U.S. data pushed back near-term easing hopes: ISM Services PMI 56.1 (Feb) (highest since Jul 2022); ADP private payrolls +63k (Feb).

[🟨 Commodities | Oil pauses, gold bid] WTI ~$74.66/bbl | Brent ~$81.40/bbl as oil took a breather after a sharp rally; safe-haven demand lifted gold to ~$5,136.91/oz (+0.99%).

[🟩 Crypto | Risk rebound] Crypto led the risk bounce: Bitcoin +7.64% to ~$73,245 | Ethereum +9.23% to ~$2,150.

[🟧 Policy/Financial Stability | Canada focus] Bank of Canada highlighted rising systemic risks from non-bank leverage (hedge funds/private credit), warning shocks could amplify sovereign bond volatility; CAD firmed near 1.3650 per USD (~73.26¢) as safe-haven demand eased.

[🟧 Geopolitics | De-escalation “talks” headlines move markets] Risk assets reacted to reports suggesting potential Iran-U.S. contacts (later challenged in parts), helping fuel Europe’s rebound while Asia remained fragile on supply-shock fears tied to Hormuz disruptions.

Companies.

+) CrowdStrike rose after reporting strong quarterly results driven by continued enterprise demand for endpoint protection and cloud security solutions, with subscription revenue growth exceeding analyst expectations.

+) GitLab traded higher following earnings that showed accelerating adoption of its DevOps platform and expanding enterprise contracts.

+) Pure Storage gained after delivering better-than-expected revenue and improving guidance tied to AI-driven data-center demand.

+) Box moved modestly higher after reaffirming full-year revenue outlook and highlighting strong enterprise adoption of its AI-enabled collaboration tools.

+) Target declined following cautious forward guidance that signaled continued pressure on discretionary consumer spending.

+) Tesla traded lower amid renewed discussion around EV price competition and slowing demand growth in key international markets.

+) Nvidia remained volatile as investors assessed sustainability of hyperscale AI-chip demand and potential supply-chain constraints.

+) Lockheed Martin advanced as defense stocks continued benefiting from rising global military spending and expanding missile-defense contracts.

+) Northrop Grumman gained on optimism around long-term U.S. strategic weapons and space-defense programs.

+) RTX Corporation traded higher as demand for missile-defense systems and aerospace components remained robust amid strong order backlogs.

General

PART 1 — Market & Macro Morning Summary (04.03.2026)

Global markets opened under continued geopolitical risk pressure as the U.S.–Iran conflict escalated further overnight, extending beyond the Middle East and deepening the disruption to global energy and shipping markets. Cross-asset sentiment remains fragile as investors assess the macro spillover from energy supply disruptions and heightened military activity.

Equities:

Global equity markets traded cautiously with defensive sector rotation continuing. Energy and defense stocks remain supported by elevated oil prices and rising geopolitical risk, while travel, logistics, and cyclical exporters remain under pressure due to fuel cost spikes and disrupted shipping routes.

Rates & Inflation Expectations:

Bond markets remain volatile as safe-haven demand competes with rising inflation expectations linked to higher oil prices. The persistence of energy supply disruptions is increasingly seen as a potential obstacle to global disinflation trends, which could complicate the timing of central-bank easing cycles.

FX & Safe Havens:

The U.S. dollar and gold remain supported by safe-haven flows as geopolitical uncertainty persists. Risk-sensitive currencies and emerging-market assets remain vulnerable to energy-price volatility and global trade disruptions.

Macro Theme:

Markets remain in a geopolitical-energy shock regime, where developments around Middle East security and maritime trade routes are dominating macro narratives and short-term asset pricing.

PART 2 — Commodities, FX & Sector Flows

Oil & Energy Markets:

Energy markets remain the key transmission channel of geopolitical risk. The Strait of Hormuz, which handles roughly 20% of global oil and LNG trade, has seen shipping activity collapse following Iranian threats to attack vessels attempting to transit the waterway.

Shipping companies, oil traders, and tanker operators have halted shipments due to safety concerns, leading to a sharp reduction in maritime traffic and forcing refiners to search for alternative supply sources.

Shipping & Trade Flows:

Satellite tracking data shows vessels clustering near ports such as Fujairah and other Gulf terminals, while insurers have withdrawn war-risk coverage and shipowners have delayed cargo movements. These disruptions are increasing freight costs globally and amplifying energy-price volatility.

Sector Rotation:

- Energy & Defense: Benefiting from supply disruption and rising security spending expectations

- Transport & Airlines: Under pressure due to fuel price spikes and route closures

- Industrials & Exporters: Impacted by logistics delays and supply-chain disruption

- Technology: Mixed performance amid broader risk volatility

PART 3 — Geopolitical Update & Strategic Market Impacts (Iran)

Conflict Escalation:

The war intensified overnight after a U.S. submarine sank an Iranian warship in the Indian Ocean, killing dozens of sailors and marking a rare naval engagement outside the Persian Gulf. The strike occurred as part of a broader U.S.–Israeli campaign targeting Iranian military capabilities.

U.S. military officials stated that operations have targeted over 2,000 Iranian military sites, including naval bases, missile launch facilities, and command centers, significantly degrading Iran’s naval capabilities.

Hormuz Shipping Crisis:

Energy supply disruptions remain severe as tanker traffic through the Strait of Hormuz has dropped sharply, with over 200 vessels stranded or unable to access Gulf ports while shipping companies suspend operations.

Iran has threatened to attack any ship attempting to pass through the strait, effectively turning the waterway into a conflict zone and dramatically increasing shipping and insurance costs.

Regional Conflict Spillover:

The conflict continues to expand across the region:

- Missile and drone attacks have targeted Bahrain, Kuwait, and Gulf infrastructure hosting U.S. forces, including strikes near the U.S. Fifth Fleet headquarters.

- Iranian drones have struck energy infrastructure and tankers near Oman, damaging ports and vessels.

- Air and missile defense systems across Turkey and Gulf states have intercepted multiple Iranian projectiles.

Strategic Market Transmission Channels:

- Roughly 20% of global oil supply exposed to chokepoint disruption

- Maritime insurance withdrawal driving freight cost spikes

- Energy-price volatility feeding global inflation expectations

- Global trade flows disrupted across energy, shipping, and aviation networks

Outlook:

If the Strait of Hormuz remains restricted and the conflict continues to expand geographically, global markets may face persistent energy inflation and trade disruptions, increasing downside risks to growth and complicating monetary policy decisions.

Upcoming News

Markets head into Thursday with a pre-payrolls, risk-managed stance, as investors fine-tune positioning ahead of Friday’s U.S. Non-Farm Payrolls report. Overall market sense is cautious but opportunistic, with FX and rates responding primarily to incremental labour-market and demand signals. Volatility is expected to cluster around U.S. macro releases, while broader conviction remains limited until the payrolls data provides a clearer direction for policy expectations.

In the United States, attention centers on Initial Jobless Claims and the Trade Balance, both offering important context for labour-market stability and external demand conditions. Jobless claims remain the most immediate indicator of labour stress ahead of payrolls; a stable print would reinforce the narrative of gradual normalization, while a sharp rise could intensify expectations for Fed easing later in the year. Meanwhile, trade data will provide insight into demand dynamics and global supply conditions, with potential implications for GDP tracking and the dollar.

Across Europe, the data calendar remains relatively light, leaving EUR trading largely as a function of U.S. yield differentials and global risk sentiment. In the Asia–Pacific region, Japan’s household spending and labour indicators offer incremental insight into domestic demand and the Bank of Japan’s normalization path, though JPY direction remains closely tied to global rate movements. Corporate catalysts remain limited, ensuring that macro signals and positioning adjustments dominate market behavior.

| Time (GMT+7) | Category | Country / Region | Event | Market Relevance |

| 06:30 | 🔴 Red News | Japan | Household Spending (y/y) | Domestic demand signal; JPY sensitivity |

| 20:30 | 🔴 Red News | United States | Initial Jobless Claims | Real-time labour stress indicator ahead of NFP |

| 20:30 | 🔴 Red News | United States | Trade Balance | External demand and GDP implications |

| All day | 🔶 Stress / Headlines | Global | Pre-NFP positioning / policy headlines | May amplify FX and rates volatility |

Snapshot (05.3.2026)

🔴 Dollar Pulls Back | DXY 98.78 (-0.30%)

The U.S. Dollar Index eased to 98.78, retreating slightly after the recent rally toward the 99 handle. The move reflects mild profit-taking as markets reassess risk positioning ahead of key macro catalysts.

🔄 G7 FX | EUR and AUD Recover

- EUR/USD 1.1643 (+0.08%)

- GBP/USD 1.3378 (+0.04%)

- USD/JPY 156.74 (-0.20%)

- USD/CHF 0.7786 (-0.07%)

The softer dollar allowed EUR and GBP to edge higher, while USD/JPY slipped below 157. Commodity currencies showed mild recovery with AUD supported by improving risk sentiment.

🪙 Crypto | Rally Extends

- BTC 72,944 (+0.35%)

- ETH 2,132 (+0.21%)

- SOL 90.95 (-0.01%)

Crypto markets continued to firm, with Bitcoin pushing above the 72k level. Ethereum followed higher while altcoins traded mixed after the recent surge.

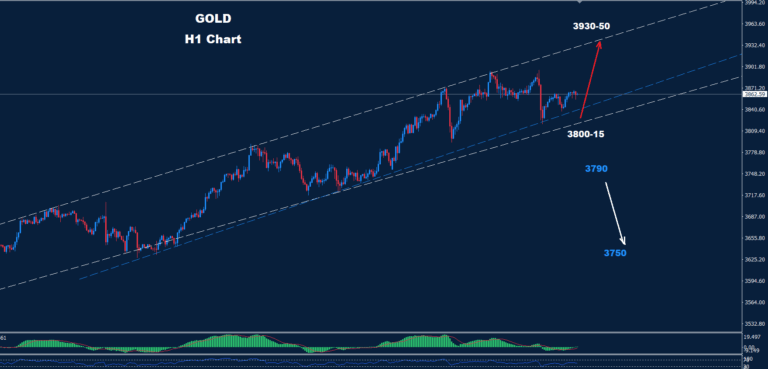

🥇 Metals | Broad Strength

- Gold 5,178 (+0.74%)

- Silver 84.28 (+0.91%)

Precious metals advanced alongside the softer dollar, with gold stabilizing near recent highs and silver maintaining strong momentum.

📊 Equities | Risk Appetite Improves

- S&P 500 6,890.56 (+0.25%)

- Dow Jones 48,846.42 (+0.12%)

- Nasdaq 100 25,093.68 (+1.51%)

- VIX 21.12 (-0.71%)

U.S. equity futures pointed higher, led by a strong rebound in tech shares. The decline in VIX suggests easing volatility and improving short-term market sentiment.

This report is provided to The Concept Trading from Van Hung Nguyen